Tendenze, domanda e crescita del mercato dei letti ospedalieri entro il 2034

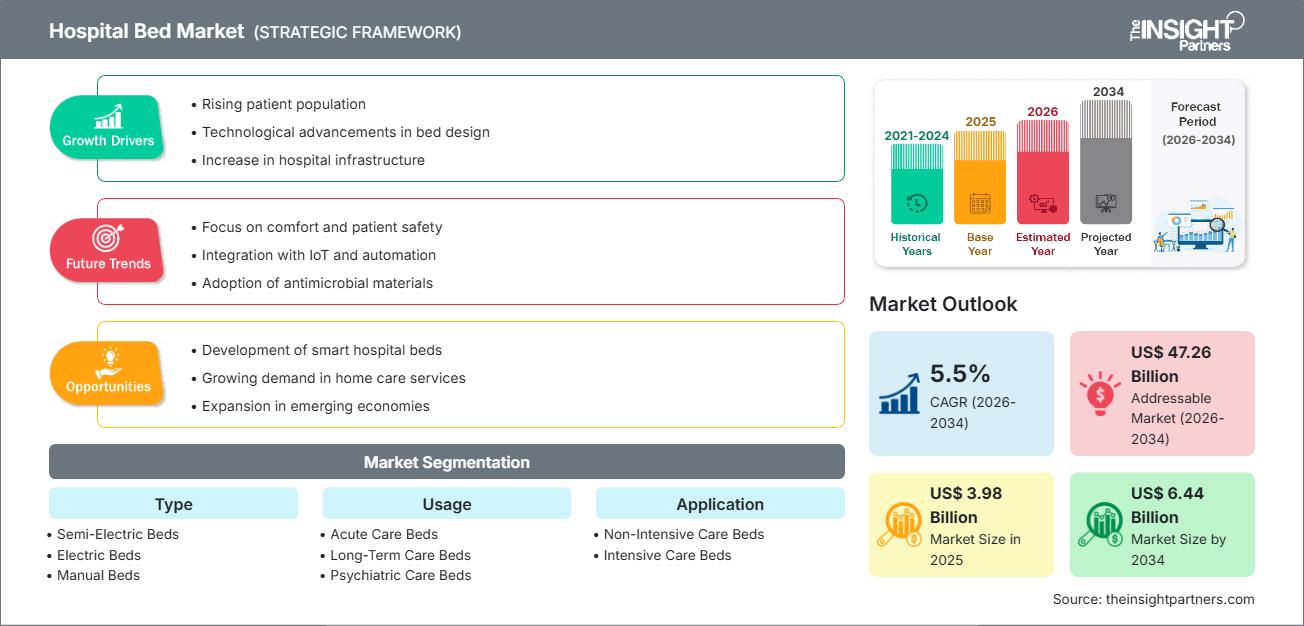

Dati storici : 2021-2024 | Anno base : 2025 | Periodo di previsione : 2026-2034Dimensioni e previsioni del mercato dei letti ospedalieri (2021-2034), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tipo (letti semielettrici, letti elettrici e letti manuali), utilizzo (letti per terapia intensiva, letti per cure a lungo termine, letti per cure psichiatriche e altri), applicazione (letti per terapia non intensiva e letti per terapia intensiva) e utente finale (ospedali e cliniche, strutture di assistenza agli anziani, centri chirurgici ambulatoriali e strutture di assistenza domiciliare).

- Stato : Prossimo

- Codice del report : TIPRE00029326

- Categoria : Beni di consumo

- Numero di pagine : 150

- Formati di report disponibili :

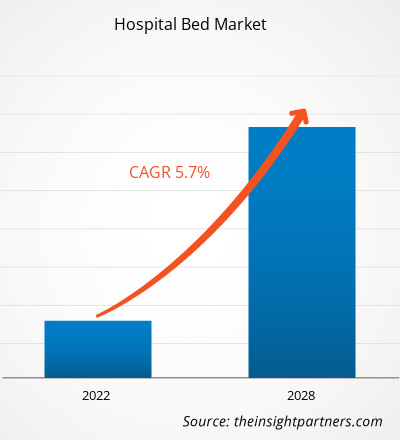

Si prevede che il mercato globale dei letti ospedalieri raggiungerà i 6,44 miliardi di dollari entro il 2034, rispetto ai 3,98 miliardi di dollari del 2025. Si prevede che il mercato registrerà un CAGR del 5,5% nel periodo di previsione 2026-2034.

Le principali dinamiche di mercato includono una crescente attenzione globale alla modernizzazione delle infrastrutture mediche, l'aumento dei tassi di ricovero dei pazienti a causa di malattie croniche e infettive e un significativo passaggio a soluzioni sanitarie digitali integrate. Inoltre, si prevede che il mercato trarrà beneficio dalla crescente popolazione geriatrica che necessita di cure a lungo termine, dall'espansione della capacità sanitaria nelle economie emergenti e dalla crescente inclusione di tecnologie di monitoraggio intelligenti nelle unità di terapia intensiva ad alto valore aggiunto.

Analisi del mercato dei letti ospedalieri

L'analisi del mercato dei letti ospedalieri indica un periodo di trasformazione in cui gli operatori sanitari stanno andando oltre le funzionalità meccaniche di base verso ecosistemi clinici integrati. Gli attuali dati di mercato rivelano un'impennata della domanda di letti che fungano da hub diagnostici, in grado di raccogliere dati in modo continuo per supportare l'assistenza infermieristica predittiva. Mentre il segmento dei letti manuali rimane un punto fermo ad alto volume nei mercati rurali ed emergenti sensibili ai costi, i segmenti elettrici e semi-elettrici stanno ottenendo un valore maggiore grazie a un'ergonomia superiore e alla riduzione dello sforzo fisico degli operatori. L'analisi strategica suggerisce che la differenziazione del mercato è sempre più determinata dalla capacità del produttore di integrare sensori di prevenzione delle lesioni da pressione e di rilevamento delle cadute direttamente nella struttura del letto. Inoltre, il mercato sta assistendo a una spinta locale verso letti sostenibili ed eco-progettati che riducano l'impronta di carbonio durante il loro ciclo di vita, in linea con le iniziative globali per un'assistenza sanitaria verde.

Panoramica del mercato dei letti ospedalieri

Il mercato dei letti ospedalieri è passato dalla semplice fornitura di piattaforme di riposo a sofisticati dispositivi medici fondamentali per l'assistenza incentrata sul paziente. Le attuali analisi del settore evidenziano che i letti ospedalieri sono ora classificati non solo in base alla fonte di alimentazione, ma anche in base alla loro applicazione clinica specializzata, come l'assistenza bariatrica, psichiatrica o pediatrica. Il mercato dei letti ospedalieri mostra un solido panorama competitivo in cui i marchi leader utilizzano rivestimenti antimicrobici e design modulari per affrontare la crescente minaccia delle infezioni nosocomiali (ICA). Nelle regioni sviluppate come il Nord America e l'Europa, il mercato è guidato da un ciclo di sostituzione in cui le infrastrutture obsolete vengono sostituite da letti intelligenti che si collegano perfettamente alle cartelle cliniche elettroniche (EHR). Nel frattempo, nella regione Asia-Pacifico, la rapida costruzione di ospedali e l'aumento del turismo medico stanno alimentando un massiccio afflusso sia di unità di terapia intensiva di fascia alta che di letti medico-chirurgici standard, posizionando la regione come il segmento geografico in più rapida crescita.

Il mercato statunitense è un mercato maturo e sofisticato, caratterizzato da infrastrutture sanitarie avanzate e standard clinici elevati. La crescita è alimentata dall'invecchiamento demografico e dal crescente carico di malattie croniche, che richiedono degenze prolungate. Gli ospedali danno sempre più priorità ai letti intelligenti e connessi per migliorare la sicurezza dei pazienti e l'efficienza operativa.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato dei letti ospedalieri: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato dei letti ospedalieri

Fattori trainanti del mercato:

- Aumento della popolazione geriatrica globale: l'aumento degli anziani aumenta significativamente la domanda di letti specializzati che rispondano ai problemi di mobilità e alla gestione della salute a lungo termine legati all'età.

- Integrazione tecnologica nell'assistenza ai pazienti: l'adozione di letti intelligenti basati su IoT e intelligenza artificiale che monitorano i parametri vitali dei pazienti e automatizzano il riposizionamento sta innescando un ciclo di sostituzione delle obsolete apparecchiature manuali.

- Espansione delle infrastrutture sanitarie: gli ingenti investimenti governativi e privati nella costruzione di nuovi ospedali multispecialistici, in particolare nei paesi in via di sviluppo, stanno creando una domanda costante di posti letto medici.

Opportunità di mercato:

- Crescente domanda di soluzioni per l'assistenza sanitaria domiciliare: oltre agli ospedali tradizionali, c'è una crescente opportunità per letti di livello ospedaliero progettati per contesti di assistenza domiciliare, concentrandosi sulla portabilità e sulla facilità d'uso per i familiari che prestano assistenza.

- Crescita nella salute comportamentale specializzata: l'espansione delle infrastrutture per la salute mentale offre opportunità per posti letto di assistenza psichiatrica progettati con specifiche caratteristiche di sicurezza e anti-legatura.

- Modernizzazione delle unità di terapia intensiva: le partnership strategiche tra produttori di letti e fornitori di software medico possono facilitare l'implementazione di letti di terapia intensiva connessi e ad alto margine di profitto nei reparti ad alta acuzie.

Analisi della segmentazione del rapporto di mercato dei letti ospedalieri

La quota di mercato dei letti ospedalieri viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per tipo:

- Letti semielettrici: un segmento versatile che combina la regolazione manuale dell'altezza con i comandi elettrici per testa e piedi, rendendoli popolari nelle cliniche di fascia media e nell'assistenza domiciliare.

- Letti elettrici: la nicchia in più rapida crescita, che offre automazione completa e funzionalità avanzate di monitoraggio dei pazienti, preferite dalle strutture di terapia intensiva e acuta di alto livello.

- Letti manuali: il principale motore di volume nei mercati con budget limitati e nelle cliniche rurali, grazie alla loro semplice affidabilità meccanica e alla convenienza.

Per utilizzo:

- Letti per terapia intensiva: progettati per il trattamento a breve termine di lesioni o malattie gravi, con particolare attenzione all'elevato turnover dei pazienti e alla facilità di igienizzazione.

- Letti per cure a lungo termine: pensati per case di cura e centri di riabilitazione in cui il comfort e la prevenzione delle ulcere da pressione sono requisiti primari.

- Letti per cure psichiatriche: progetti specializzati che mettono al primo posto la sicurezza, utilizzati nelle strutture di salute comportamentale per ridurre al minimo i rischi per i pazienti e garantire al contempo la durevolezza.

Per applicazione:

- Letti di terapia intensiva: letti di alto valore dotati di sensori avanzati e supporto per le apparecchiature di monitoraggio della vita utilizzate nelle terapie intensive.

- Letti di terapia non intensiva: letti medici standard utilizzati nei reparti di degenza generale e nelle sale di risveglio per pazienti stabili.

Da parte dell'utente finale:

- Ospedali e cliniche: il principale contributore di fatturato, trainato dai continui aggiornamenti delle infrastrutture e dall'elevato volume di pazienti.

- Strutture di assistenza agli anziani: un segmento in crescita alimentato dal cambiamento demografico globale verso una popolazione anziana che necessita di supporto alla vita assistita.

- Centri chirurgici ambulatoriali: traggono vantaggio dalla tendenza verso le procedure ambulatoriali e dalla necessità di posti letto di degenza di alta qualità.

- Ambienti di assistenza domiciliare: un canale emergente e in forte crescita per i letti medicali adattati all'uso residenziale.

Per geografia:

- America del Nord

- Europa

- Asia-Pacifico

- America meridionale e centrale

- Medio Oriente e Africa

Ambito del rapporto sul mercato dei letti ospedalieri

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 3,98 miliardi di dollari USA |

| Dimensioni del mercato entro il 2034 | 6,44 miliardi di dollari USA |

| CAGR globale (2026 - 2034) | 5,5% |

| Dati storici | 2021-2024 |

| Periodo di previsione | 2026-2034 |

| Segmenti coperti |

Per tipo

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato dei posti letto ospedalieri: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei letti ospedalieri è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato dei letti ospedalieri per area geografica

Si prevede che la regione Asia-Pacifico crescerà più rapidamente nei prossimi anni. Anche i mercati emergenti in America meridionale e centrale, Medio Oriente e Africa offrono numerose opportunità di espansione inesplorate per i produttori di arredi medicali e i fornitori di strutture specializzate.

Il mercato dei letti ospedalieri sta attraversando una profonda trasformazione, passando dalla tradizionale utilità manuale a ecosistemi medico-chirurgici ad alto valore aggiunto. La crescita è trainata dalla crescente prevalenza di patologie croniche, dall'aumento della domanda di posti letto in terapia intensiva specializzata e dall'espansione dell'assistenza a lungo termine. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

1. Nord America

- Quota di mercato: detiene una quota di mercato leader a livello mondiale, trainata dall'adozione di tecnologie di alta qualità e dall'elevata spesa sanitaria.

-

Fattori chiave:

- Sostituzione diffusa dei letti tradizionali con sistemi intelligenti per ridurre le patologie acquisite in ospedale

- Solidi finanziamenti governativi per l'ammodernamento delle terapie intensive e l'ampliamento dei centri traumatologici

- Crescente preferenza per i letti di assistenza domiciliare ad alta tecnologia per il recupero post-operatorio

- Tendenze: integrazione di sensori basati sull'intelligenza artificiale per il monitoraggio continuo dei pazienti e attenzione a progetti specifici per pazienti bariatrici per soddisfare le esigenze demografiche.

2. Europa

- Quota di mercato: detiene una quota globale significativa, supportata da solidi sistemi sanitari pubblici in Germania, Francia e Regno Unito.

-

Fattori chiave:

- Rigorosi standard normativi per la sicurezza dei pazienti e la protezione ergonomica del personale infermieristico

- Infrastruttura di elaborazione consolidata per la sterilizzazione e la manutenzione dei letti ospedalieri su larga scala

- L'invecchiamento della popolazione determina un'elevata domanda di posti letto per la riabilitazione e l'assistenza a lungo termine

- Tendenze: un passaggio strategico verso letti eco-progettati, utilizzando materiali sostenibili e superfici avanzate per il controllo delle infezioni, per soddisfare gli standard del Green Deal europeo.

3. Asia-Pacifico

- Quota di mercato: la regione in più rapida crescita, con Cina e India che agiscono come principali motori dello sviluppo delle infrastrutture ospedaliere.

-

Fattori chiave:

- Ingenti investimenti pubblici e privati nella costruzione di ospedali intelligenti e centri multispecialistici

- Rapida urbanizzazione e iniziative governative per migliorare il rapporto posti letto-pazienti

- Segmenti di reddito medio-alto in crescita che cercano esperienze di ricovero di lusso occidentalizzate

- Tendenze: forte dipendenza dai contratti B2B per l'implementazione di letti su larga scala e crescita di centri di produzione locali per modelli sia manuali che elettrici.

4. America meridionale e centrale

- Quota di mercato: mercato emergente con un settore ospedaliero privato in crescita in paesi come Brasile e Cile.

-

Fattori chiave:

- Modernizzazione delle strutture esistenti per attrarre il turismo medico e migliorare i risultati per i pazienti locali

- Crescente consapevolezza dei letti specializzati per la maternità e l'assistenza psichiatrica

- Passaggio dai letti manuali a quelli semielettrici nelle cliniche private urbane

- Tendenze: crescita di centri chirurgici ambulatoriali boutique e introduzione di catene di fornitura "farm-to-bed" per la manutenzione localizzata delle attrezzature.

5. Medio Oriente e Africa

- Quota di mercato: sviluppo del mercato in transizione verso standard sanitari formalizzati attraverso investimenti strategici.

-

Fattori chiave:

- Progetti ospedalieri su larga scala in Arabia Saudita e negli Emirati Arabi Uniti (ad esempio, Neom e Dubai Healthcare City)

- Elevata richiesta di letti durevoli e a bassa manutenzione nei climi aridi

- Focus strategico sull'aumento della sicurezza alimentare locale e della resilienza della catena di approvvigionamento medico

- Tendenze: implementazione di moderne tecnologie di mungitura e refrigerazione (per letti terapeutici) e attenzione al supporto ad alto contenuto di nutrienti per gli ospedali pediatrici.

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando grazie alla presenza di leader affermati come Baxter International Inc. (Hillrom), Stryker Corporation e Getinge AB. Anche specialisti regionali e operatori di nicchia come LINET Group SE (Repubblica Ceca) e Paramount Bed Co., Ltd. (Giappone), insieme ad aziende innovative nel settore delle apparecchiature medicali come Invacare Corporation e Arjo AB, contribuiscono a creare un panorama di mercato diversificato e in rapida espansione.

Questo ambiente competitivo spinge i fornitori a differenziarsi attraverso:

- Trasformazione digitale: trasformare i letti d'ospedale in hub intelligenti che raccolgono dati, avvisano gli infermieri dei movimenti dei pazienti e si integrano con le cartelle cliniche elettroniche.

- Focus sulle applicazioni specializzate: offriamo soluzioni su misura per esigenze cliniche specifiche, tra cui letti pediatrici, telai bariatrici e piattaforme specializzate per terapia intensiva.

- Controllo della catena di fornitura: gestione dell'intero processo, dalla progettazione ergonomica all'assemblaggio locale, per garantire qualità e conformità.

Opportunità e mosse strategiche

- Collaborare con piattaforme sanitarie digitali di alto livello e fornitori IT per soddisfare la crescente domanda di letti ospedalieri connessi e intelligenti nei mercati dell'Asia-Pacifico e del Nord America.

- Incorporare pratiche di produzione sostenibili e certificazioni di economia circolare per attrarre amministratori sanitari e agenzie di sanità pubblica attenti all'ambiente.

Le principali aziende che operano nel mercato dei letti ospedalieri sono:

- Hill-Rom Holdings, Inc. (Baxter)

- Stryker

- Arjo

- Invacare Corporation

- PARAMOUNT BED CO., LTD.

- GF Health Products, Inc.

- Malvestio SpA

- Span America (Savaria Corporation)

- Savion Industries

- Stiegelmeyer GmbH & Co. KG

- Medstrom

Disclaimer: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e sviluppi recenti sul mercato dei letti ospedalieri

- A settembre 2025, Invacare ha annunciato il lancio del nuovo letto Accent Medical Profiling, progettato per migliorare il riposo, il sonno e l'indipendenza quotidiana. Offre soluzioni confortevoli che soddisfano i più elevati standard di sicurezza e qualità. Il nuovo Accent non fa eccezione e offre una soluzione di qualità semplice, conveniente e senza compromessi.

- Nel febbraio 2025, Stryker ha annunciato il lancio del letto ospedaliero ProCeed, che offre semplicità e migliora l'assistenza in diverse regioni. ProCeed contribuisce alla sicurezza dei pazienti e del personale sanitario grazie a diversi elementi di design, tra cui l'altezza ridotta del letto, che favorisce la mobilità del paziente e riduce il rischio di lesioni da caduta.

Copertura e risultati del rapporto sul mercato dei letti ospedalieri

Il rapporto sulle dimensioni e le previsioni del mercato dei letti ospedalieri (2021-2034) fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato dei letti ospedalieri a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato dei letti ospedalieri, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi del mercato dei letti ospedalieri che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti nel mercato dei letti ospedalieri

- Profili aziendali dettagliati

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Sblocca sconti esclusivi sui report

Richiedi ora

Ottieni un campione gratuito per - Mercato dei letti ospedalieri

Ottieni un campione gratuito per - Mercato dei letti ospedalieri