Marché des dispositifs d'arthroscopie : demande, part de marché et prévisions jusqu'en 2034

Taille et prévisions du marché des dispositifs d'arthroscopie (2021-2034), parts de marché mondiales et régionales, tendances et analyse des opportunités de croissance : Couverture du rapport : Par produit (arthroscopes, implants arthroscopiques, systèmes de gestion des fluides, systèmes de radiofréquence (RF), systèmes de rasage motorisés, systèmes de visualisation, autres équipements arthroscopiques) ; Application/Type d'arthroscopie (arthroscopie du genou, arthroscopie de la hanche, arthroscopie de l'épaule et du coude, arthroscopie du rachis, arthroscopie du pied et de la cheville/petites articulations et autres) ; et Zone géographique

- Statut : Données publiées

- Code du rapport : TIPRE00020213

- Catégorie : Sciences de la vie

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : January 23, 2026

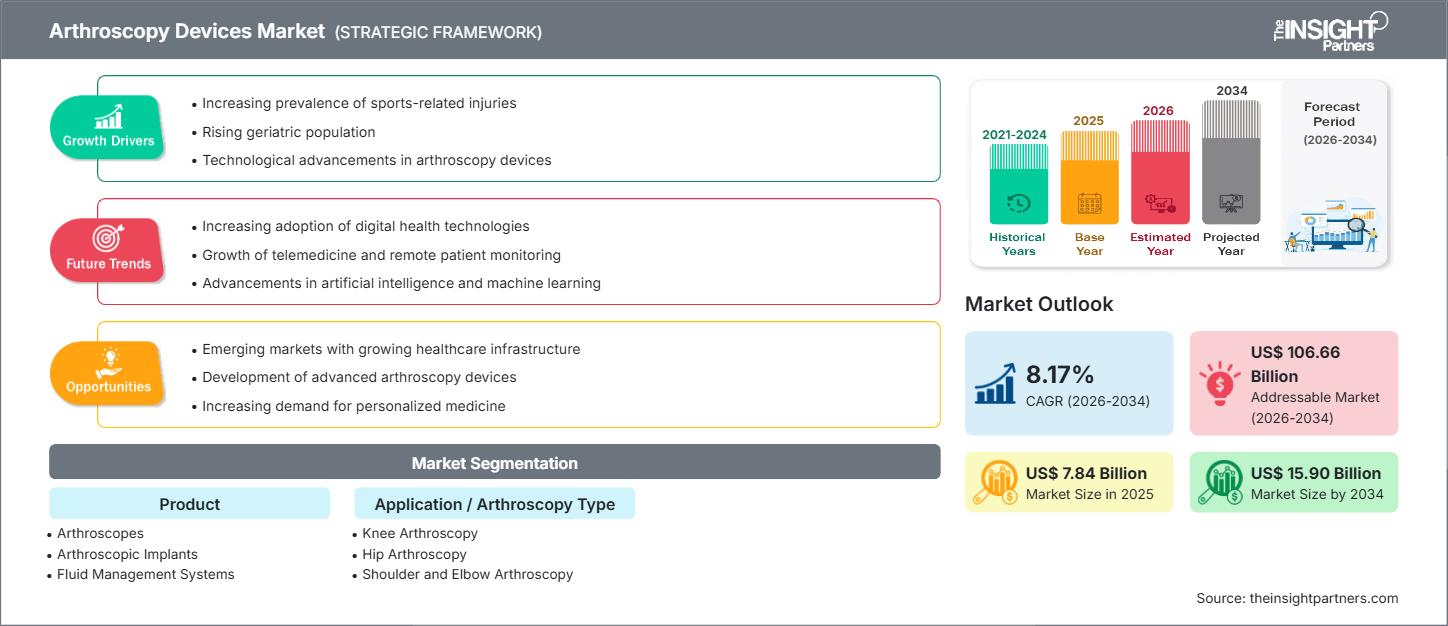

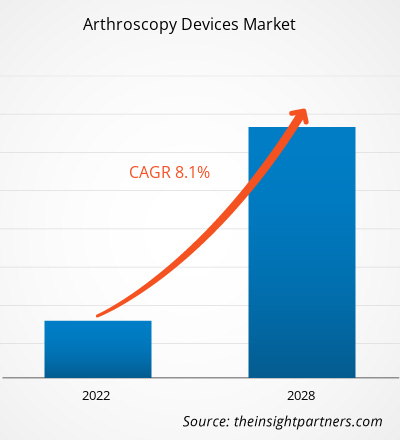

Le marché des dispositifs d'arthroscopie était évalué à 7,84 milliards de dollars américains en 2025 et devrait atteindre 15,90 milliards de dollars américains en 2034, avec un taux de croissance annuel composé (TCAC) de 8,17 % entre 2026 et 2034.

Analyse du marché des dispositifs d'arthroscopie

La croissance du marché des dispositifs d'arthroscopie est stimulée par une prévalence croissante des troubles musculo-squelettiques, une incidence accrue des blessures articulaires liées au sport et une préférence grandissante pour les interventions chirurgicales minimalement invasives.

Les progrès en matière de technologie chirurgicale, tels que l'amélioration des systèmes de visualisation arthroscopique, les instruments motorisés, les systèmes de radiofréquence et les implants biocompatibles, améliorent les résultats des interventions, réduisent les temps de récupération et favorisent une adoption plus large des procédures arthroscopiques à l'échelle mondiale.

De plus, le développement des infrastructures orthopédiques, l'augmentation des dépenses de santé et la croissance de la population gériatrique (plus sujette aux troubles articulaires) soutiennent la demande à long terme d'appareils d'arthroscopie.

Aperçu du marché des dispositifs d'arthroscopie

Les dispositifs d'arthroscopie désignent un large éventail d'instruments et de systèmes médicaux utilisés pour réaliser des interventions arthroscopiques, des chirurgies mini-invasives permettant de diagnostiquer et de traiter les affections articulaires. Ces dispositifs comprennent les arthroscopes, les systèmes de visualisation, les systèmes de gestion des fluides, les systèmes de radiofréquence (RF), les systèmes de rasage motorisés, les implants arthroscopiques, les forets et les systèmes de fixation, ainsi que d'autres équipements connexes.

Ces outils permettent aux chirurgiens orthopédistes de visualiser l'intérieur des articulations, d'effectuer des interventions réparatrices (par exemple, la réparation des ligaments, la restauration du cartilage, la réparation du ménisque), de gérer l'irrigation et le flux de fluides, et d'implanter du matériel de stabilisation, tout en minimisant les traumatismes tissulaires et en permettant une récupération plus rapide.

Les dispositifs d'arthroscopie jouent un rôle essentiel dans de nombreuses articulations, notamment le genou, la hanche, l'épaule, la colonne vertébrale, le pied/la cheville et les petites articulations, aidant les cliniciens à fournir des soins efficaces et moins invasifs dans les hôpitaux, les centres de chirurgie ambulatoire (ASC), les cliniques orthopédiques et les centres spécialisés.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché des dispositifs d'arthroscopie : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs de croissance et opportunités du marché des dispositifs d'arthroscopie

Facteurs de marché :

- Incidence croissante des troubles musculo-squelettiques et des lésions articulaires : la hausse des cas d’arthrose, de déchirures ligamentaires, de lésions méniscales et de blessures sportives alimente la demande d’interventions arthroscopiques et de dispositifs connexes.

- Préférence pour la chirurgie mini-invasive (MIS) : Les chirurgiens et les patients préfèrent de plus en plus l'arthroscopie à la chirurgie articulaire ouverte en raison de ses avantages tels que des incisions plus petites, un risque moindre, une récupération plus rapide et une durée d'hospitalisation réduite.

- Progrès technologiques dans le domaine des équipements arthroscopiques : les innovations, notamment les systèmes de visualisation haute définition, les rasoirs motorisés, la gestion avancée des fluides, les implants bio-absorbables et métalliques et les systèmes RF, améliorent la précision chirurgicale, les résultats pour les patients et élargissent le champ des affections articulaires traitables.

- Développement des infrastructures orthopédiques et des investissements dans les soins de santé : l’expansion des hôpitaux, des centres de chirurgie ambulatoire et des cliniques spécialisées en orthopédie, notamment dans les économies émergentes, accroît l’accessibilité aux interventions arthroscopiques.

Opportunités:

- Expansion sur les marchés émergents : des régions comme l’Asie-Pacifique (y compris des pays comme l’Inde et la Chine) présentent un fort potentiel de croissance en raison de l’augmentation des investissements dans les soins de santé, de la sensibilisation croissante aux procédures minimalement invasives, de l’augmentation des blessures sportives chez les jeunes et du vieillissement de la population, qui est sujette aux troubles articulaires.

- Innovation et différenciation des produits : le développement d’implants de nouvelle génération, de systèmes de visualisation améliorés, de dispositifs portables de gestion des fluides et d’outils RF/motorisés avancés permet aux fabricants de dispositifs d’offrir des solutions à valeur ajoutée, susceptibles de conquérir une plus grande part de marché.

- Croissance des centres de chirurgie ambulatoire (ASC) et des procédures ambulatoires minimalement invasives : À mesure que les ASC se développent à l'échelle mondiale, la demande d'appareils d'arthroscopie optimisés pour les milieux ambulatoires (systèmes compacts, efficaces et moins coûteux) est susceptible de croître.

- Demande croissante de réparation et de réadaptation articulaire due au vieillissement de la population : L’augmentation mondiale de la population âgée sujette à l’arthrose et aux affections articulaires dégénératives stimule la demande à long terme d’appareils et d’interventions arthroscopiques.

Marché des dispositifs d'arthroscopie : analyse de segmentation

Le marché est généralement segmenté selon plusieurs dimensions, comme suit :

Par produit :

- Arthroscopes

- Implants arthroscopiques

- Systèmes de gestion des fluides

- Systèmes de radiofréquence (RF)

- Systèmes de rasage motorisés

- Systèmes de visualisation

- Autres équipements arthroscopiques

Par application / type d'arthroscopie :

- Arthroscopie du genou

- Arthroscopie de la hanche

- Arthroscopie de l'épaule et du coude

- Arthroscopie de la colonne vertébrale

- Arthroscopie du pied et de la cheville / Petites articulations et autres

Par géographie :

- Amérique du Nord

- Europe

- Asie-Pacifique

- Moyen-Orient et Afrique

- Amérique du Sud et centrale / Amérique latine

Aperçu régional du marché des dispositifs d'arthroscopie

Les tendances régionales et les facteurs influençant le marché des dispositifs d'arthroscopie tout au long de la période prévisionnelle ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments de marché et la répartition géographique du marché des dispositifs d'arthroscopie en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et centrale.

Portée du rapport sur le marché des dispositifs d'arthroscopie

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2025 | 7,84 milliards de dollars américains |

| Taille du marché d'ici 2034 | 15,90 milliards de dollars américains |

| TCAC mondial (2026 - 2034) | 8,17% |

| Données historiques | 2021-2024 |

| Période de prévision | 2026-2034 |

| Segments couverts |

Sous-produit

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des dispositifs d'arthroscopie : comprendre son impact sur la dynamique commerciale

Le marché des dispositifs d'arthroscopie connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux. Cette demande est alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages du produit. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, ce qui contribue à stimuler la croissance du marché.

- Découvrez un aperçu des principaux acteurs du marché des dispositifs d'arthroscopie

Analyse des parts de marché des dispositifs d'arthroscopie par zone géographique

- L’Amérique du Nord détient actuellement une part prépondérante sur le marché des dispositifs d’arthroscopie, grâce à une infrastructure de soins de santé avancée, à une forte adoption des procédures orthopédiques mini-invasives, à une population gériatrique et sportive importante et à des politiques de remboursement favorables.

- L’Europe demeure un marché clé en raison de l’incidence croissante de l’arthrose et des maladies articulaires dégénératives, de systèmes de santé bien établis et d’une demande croissante de réparations articulaires mini-invasives.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide au cours de la période de prévision, grâce à l'expansion des infrastructures orthopédiques, à la hausse des revenus disponibles, à une meilleure connaissance des procédures mini-invasives, à la croissance du tourisme médical et à un nombre croissant de cas de lésions articulaires parmi les populations sportives âgées et jeunes.

- Le Moyen-Orient, l'Afrique et l'Amérique latine représentent des marchés émergents où l'accès croissant aux soins de santé, les investissements dans les infrastructures médicales et la demande croissante de procédures de réparation articulaire abordables offrent d'importantes opportunités pour l'expansion de l'adoption des dispositifs d'arthroscopie.

Marché des dispositifs d'arthroscopie : paysage concurrentiel et acteurs clés

Le marché mondial des dispositifs d'arthroscopie se caractérise par un mélange de fabricants multinationaux de dispositifs médicaux bien établis et d'entreprises spécialisées dans les dispositifs orthopédiques. Les principaux acteurs se font souvent concurrence sur la base de l'innovation technologique, de l'étendue de leur gamme de produits (implants, instruments, systèmes de visualisation et de fluides), de la qualité et de leur réseau de distribution mondial.

Des rapports antérieurs de The Insight Partners ont identifié une segmentation par produits tels que les arthroscopes, les implants, les systèmes de gestion des fluides, les systèmes de visualisation, les rasoirs électriques, les systèmes RF et autres équipements arthroscopiques.

Face à la demande croissante dans les régions émergentes et à l'augmentation du nombre d'interventions dans le monde, la concurrence s'intensifie, les entreprises cherchant à se différencier par des technologies de pointe (par exemple, la visualisation haute définition, l'instrumentation minimalement invasive, les implants biocompatibles), des solutions rentables et une présence géographique étendue.

Les principaux acteurs du marché sont :

- Arthrex, Inc.

- Société CONMED

- Services Johnson & Johnson, Inc.

- KARL STORZ SE & Co. KG

- Medtronic

- Richard Wolf GmbH.

- Smith & Nephew

- Société Stryker

- Zimmer Biomet

Autres joueurs analysés au cours de la période de recherche :

- United Orthopedic Corporation

- Instruments chirurgicaux Sklar

- Cannuflow Inc.

- Parcus Medical

- Bioventus LLC

- Groupe médical Wright NV

- Société d'implants orthopédiques (OIC)

- GPC Medical Ltd.

- Hofer GmbH

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- B. Braun Melsungen AG

Actualités et développements récents du marché des dispositifs d'arthroscopie

- Stryker a présenté une plateforme de visualisation arthroscopique améliorée, dotée d'une imagerie 4K optimisée et d'une meilleure différenciation des tissus mous, afin de favoriser la précision des interventions mini-invasives.

- Arthrex a élargi sa gamme de produits avec de nouvelles ancres de suture bio-résorbables conçues pour favoriser l'intégration osseuse et réduire les complications associées aux implants métalliques.

- Smith+Nephew a déployé une plateforme de médecine sportive intégrée numériquement qui connecte les instruments d'arthroscopie intelligents aux outils de planification chirurgicale afin d'améliorer l'efficacité du flux de travail.

- ConMed a reçu l'autorisation réglementaire pour un système de résection motorisé de nouvelle génération équipé d'une technologie de détection de couple afin d'améliorer le contrôle de la coupe et la précision chirurgicale.

- Karl Storz a lancé un logiciel d'optimisation d'images basé sur l'IA pour les tours d'arthroscopie, automatisant les ajustements d'éclairage et de contraste afin d'améliorer la visualisation en temps réel.

Rapport sur le marché des dispositifs d'arthroscopie : contenu et livrables

Le rapport « Marché des procédures et produits d’arthroscopie (2021-2034) » de The Insight Partners propose une analyse complète et structurée, comprenant :

- Taille et prévisions du marché mondial, régional et national (USD) pour tous les segments clés (produit, application, utilisateur final, zone géographique).

- Dynamique du marché : examen détaillé des facteurs moteurs, des contraintes, des opportunités et des tendances émergentes dans le domaine des dispositifs d’arthroscopie.

- Paysage concurrentiel : profilage des principaux fabricants, analyse de la concentration du marché, analyse comparative des technologies et perspectives stratégiques.

- Analyse approfondie basée sur la segmentation : segmentation par types de produits, types d’applications/d’arthroscopies, catégories d’utilisateurs finaux et marchés régionaux.

- Scénarios prévisionnels : projections de la demande probables, optimistes et prudentes sur l’horizon prévisionnel (jusqu’en 2031), permettant aux parties prenantes d’évaluer les opportunités à court et à long terme.

- Analyses complémentaires : chaîne de valeur, environnement réglementaire, aperçu de l’offre et de la demande, facteurs de croissance et contraintes.

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires