Analisi delle dimensioni, della quota, della crescita e delle previsioni del mercato Backshell fino al 2034

Dimensioni e previsioni del mercato dei gusci posteriori (2021-2034), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tipo (guscio posteriore circolare e guscio posteriore rettangolare), materiale (alluminio, nichel, acciaio inossidabile e altri), standard militari (AS85049, MIL-DTL-38999, MIL-DTL-83723, MIL-DTL-5015, MIL-DTL-26482 e altri) e applicazione (terrestre, navale e aerea).

- Stato : Dati rilasciati

- Codice del report : TIPRE00024272

- Categoria : Aerospaziale e difesa

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : December 22, 2025

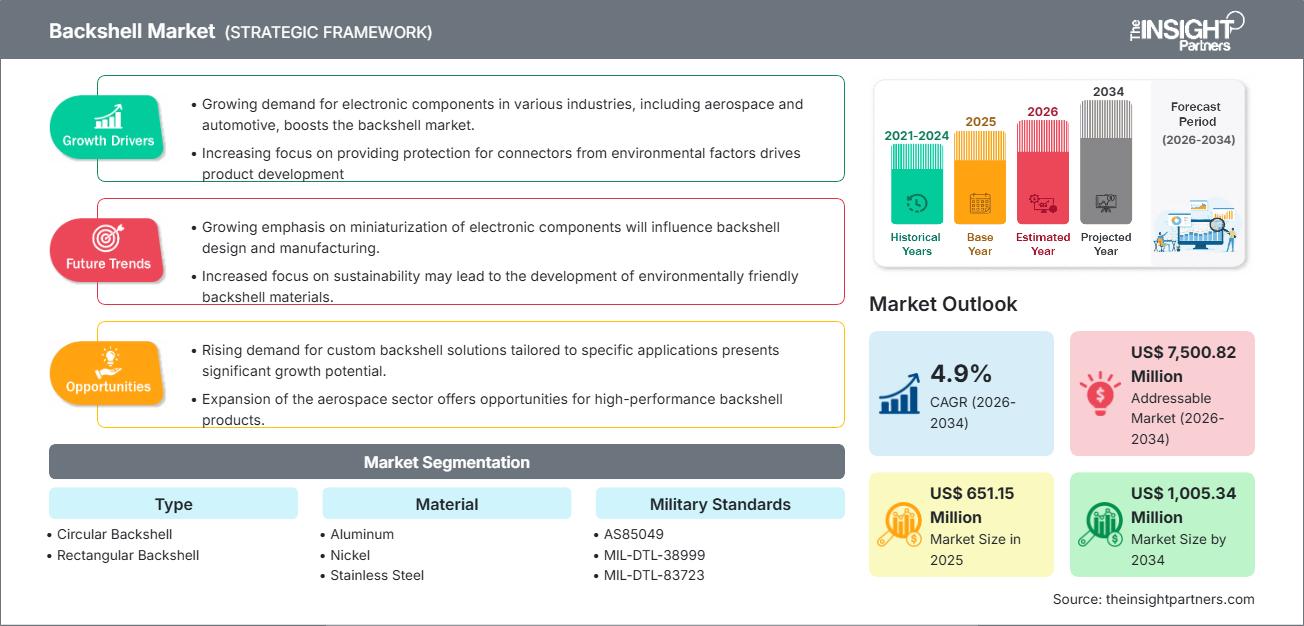

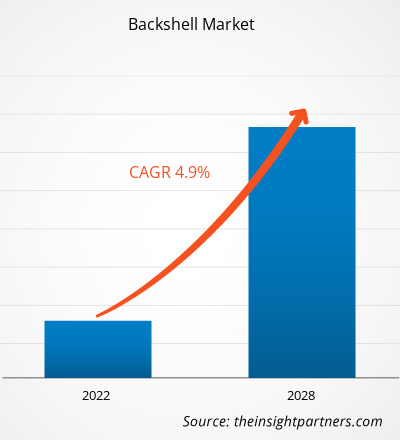

Si prevede che il mercato dei backshell raggiungerà i 1.005,34 milioni di dollari entro il 2034, rispetto ai 651,15 milioni di dollari del 2025. Si prevede che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 4,9% nel periodo di previsione 2026-2034.

Analisi di mercato del guscio posteriore

L'analisi del mercato dei backshell indica una crescita costante e costante, trainata principalmente da programmi di modernizzazione della difesa su larga scala e dall'aumento della produzione di velivoli commerciali e militari a livello globale. I requisiti critici per la protezione EMI/RFI nei sistemi elettronici sensibili che operano in ambienti difficili aprono la strada alla crescita del mercato. Inoltre, i crescenti requisiti normativi, in particolare i rigorosi standard militari come AS85049, richiedono l'utilizzo di backshell ad alte prestazioni e conformi. Il mercato sta inoltre assistendo a un'accelerazione dovuta all'adozione di materiali compositi leggeri, poiché i settori aerospaziale e industriale danno priorità alla riduzione del peso senza compromettere la protezione.

Panoramica del mercato dei gusci posteriori

I gusci posteriori sono componenti protettivi essenziali utilizzati nei connettori elettrici per gestire e salvaguardare il punto critico in cui un cavo termina con una spina o una presa. Questi componenti offrono protezione antistrappo, tenuta stagna (contro umidità, polvere e liquidi) e una robusta schermatura EMI/RFI. Sono ampiamente adottati in settori chiave, tra cui quello militare, aerospaziale e dell'industria pesante, garantendo durata a lungo termine e integrità del segnale, nel rispetto dei più rigorosi standard operativi. Il guscio posteriore offre un'ottima protezione contro minacce esterne come elevati livelli di vibrazioni, temperature estreme e agenti corrosivi, ed è un componente importante per il mantenimento dell'affidabilità e delle prestazioni del sistema.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, incluse parti di questo report, analisi a livello nazionale, pacchetto dati Excel e potrai usufruire di fantastiche offerte e sconti per start-up e università.

Mercato dei gusci posteriori: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato Backshell

Fattori trainanti del mercato:

- Programmi di modernizzazione della difesa in aumento a livello globale: l'aumento dei programmi di modernizzazione della difesa in tutto il mondo alimenta l'interesse per diversi connettori e gusci posteriori schermati ad alta affidabilità installati su aerei militari, navi militari e veicoli terrestri aggiornati, utilizzati per gestire sistemi complessi di guerra elettronica e di comunicazione.

- Crescente domanda di protezione EMI/RFI: il crescente utilizzo di componenti elettronici e sistemi in rete nelle applicazioni aerospaziali e industriali aumenta la domanda di soluzioni di schermatura efficaci, che contribuiscano a evitare il degrado del segnale e a garantire la funzionalità del sistema.

- Crescita nell'aviazione commerciale e nell'esplorazione spaziale: l'aumento del traffico aereo globale e l'espansione dei programmi spaziali (sia governativi che privati) stimolano la domanda di soluzioni di interconnessione durevoli, leggere e ad alte prestazioni.

Opportunità di mercato:

- Sviluppo di materiali leggeri e resistenti alla corrosione: privilegiare compositi avanzati e leghe di alluminio speciali per ottenere prestazioni superiori, risparmio di peso e maggiore durata in ambienti marini o estremamente difficili.

- Integrazione di Smart Backshell con sensori: le future opportunità di sviluppo di backshell "intelligenti" dotati di sensori miniaturizzati per il monitoraggio della temperatura, delle vibrazioni e dell'efficacia dello scudo aiuteranno a prevedere la manutenzione e a rilevare i guasti in tempo reale.

- Espansione nei mercati emergenti: la rapida industrializzazione e i crescenti budget per la difesa nei paesi dell'Asia-Pacifico e del Medio Oriente offrono un potenziale inutilizzato per i principali attori del mercato.

Analisi della segmentazione del rapporto di mercato Backshell

Il mercato dei backshell è ampiamente segmentato per tipologia, materiale, conformità agli standard militari e applicazione finale, offrendo una visione dettagliata delle dinamiche di mercato e delle aree di crescita. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per tipo:

- Guscio posteriore circolare: il segmento è leader di mercato grazie alla diffusa adozione di connettori circolari, come MIL-DTL-38999, nei settori aerospaziale e della difesa. Ciò garantisce una schermatura e una tenuta a 360 gradi, rendendolo la scelta ideale quando è richiesta un'elevata affidabilità.

- Backshell rettangolare: questo segmento si rivolge a specifici sistemi industriali e militari in cui lo spazio e il fattore di forma impongono l'uso di connettori rettangolari. La domanda è concentrata in apparecchiature specializzate e installazioni fisse.

Per materiale:

- Alluminio: il segmento più comune, che offre un eccellente equilibrio tra resistenza, peso e convenienza. L'alluminio è ampiamente utilizzato in tutte le principali applicazioni ed è spesso nichelato per la resistenza alla corrosione e una maggiore conduttività.

- Nichel/Acciaio inossidabile: questi materiali sono preferiti per applicazioni che richiedono un'eccellente resistenza alla corrosione, tolleranza alle alte temperature e una durata eccezionale, come ad esempio in ambienti navali o con motori ad alta temperatura.

- Composito: questo materiale è il segmento in più rapida crescita, spinto dalla necessità di una significativa riduzione del peso negli aerei moderni, offrendo prestazioni meccaniche e schermatura comparabili se opportunamente metallizzato.

Secondo gli standard militari:

- AS85049

- MIL-DTL-38999

- MIL-DTL-83723

- MIL-DTL-5015

- MIL-DTL-26482

Per applicazione:

- Terra (veicoli e attrezzature): veicoli terrestri militari, macchinari pesanti, automazione industriale; gusci posteriori estremamente robusti e sigillati, resistenti a urti estremi, vibrazioni e polvere.

- Navale (marittimo e marittimo): richiede gusci posteriori in acciaio inossidabile o alluminio di grado marino altamente specializzati e resistenti alla corrosione, a causa della costante esposizione all'acqua salata e all'elevata umidità.

- Aerospaziale e aviazione: il segmento più ampio, che comprende aerei commerciali, jet militari, elicotteri e veicoli spaziali. Questa applicazione richiede soluzioni estremamente leggere, altamente affidabili e schermate dalle interferenze elettromagnetiche.

Per geografia

- America del Nord

- Europa

- Asia-Pacifico

- America meridionale e centrale

- Medio Oriente e Africa

Approfondimenti regionali sul mercato Backshell

Le tendenze e i fattori regionali che hanno influenzato il mercato dei Backshell durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione analizza anche i segmenti e la distribuzione geografica del mercato dei Backshell in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato Backshell

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 651,15 milioni di dollari USA |

| Dimensioni del mercato entro il 2034 | 1.005,34 milioni di dollari USA |

| CAGR globale (2026 - 2034) | 4,9% |

| Dati storici | 2021-2024 |

| Periodo di previsione | 2026-2034 |

| Segmenti coperti |

Per tipo

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato Backshell: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei Backshell è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni una panoramica dei principali attori del mercato Backshell

Analisi della quota di mercato di Backshell per area geografica

Si prevede che la regione Asia-Pacifico registrerà la crescita più rapida nei prossimi anni. Anche i mercati emergenti del Sud e Centro America, del Medio Oriente e dell'Africa offrono numerose opportunità di espansione inesplorate per i fornitori di componenti per backshell. Il mercato dei backshell mostra una traiettoria di crescita diversa in ciascuna regione a causa di fattori quali la spesa per la difesa, l'attività manifatturiera aerospaziale, gli investimenti nell'automazione industriale e l'adesione a rigorosi standard militari. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

1. Nord America

- Quota di mercato: detiene la quota di mercato più ampia grazie al suo avanzato settore della difesa e alla consolidata base di produzione aerospaziale commerciale.

- Fattori chiave: elevata spesa in ricerca e sviluppo, adozione diffusa di rigorosi standard militari e programmi di modernizzazione degli aeromobili in corso negli Stati Uniti e in Canada.

- Tendenze: passaggio continuo verso sistemi di interconnessione complessi e ad alta larghezza di banda che richiedono tecnologie avanzate di schermatura EMI/RFI e soluzioni composite leggere.

2. Europa

- Quota di mercato: detiene una quota significativa, trainata dai principali attori aerospaziali regionali (ad esempio Airbus) e dai solidi settori dell'automazione industriale, in particolare in Germania e Francia.

- Fattori chiave: digitalizzazione dell'automazione industriale, forte crescita nei settori ferroviario e automobilistico e progetti di difesa collaborativi che richiedono componenti standardizzati.

- Tendenze: crescente attenzione alla miniaturizzazione e alla connettività ad alta densità, unita alle richieste normative per una protezione ambientale affidabile nelle applicazioni industriali.

3. Asia-Pacifico

- Quota di mercato: si prevede che sarà la regione in più rapida crescita durante il periodo di previsione, grazie alla rapida industrializzazione e all'aumento dei budget per la difesa.

- Fattori chiave: significativi investimenti governativi nella produzione nazionale di difesa (ad esempio, Cina, India), rapida crescita nella produzione di elettronica ed espansione della flotta commerciale.

- Tendenze: adozione di standard militari occidentali e aumento della domanda di soluzioni backshell convenienti ma di alta qualità per supportare nuove linee di produzione.

4. America meridionale e centrale

- Quota di mercato: rappresenta un mercato emergente con crescita graduale.

- Fattori chiave: espansione dei settori industriali (minerario, petrolifero e del gas) e aumento degli investimenti nelle infrastrutture di telecomunicazione, che richiedono componenti di connettività affidabili.

- Tendenze: i connettori e i backshell industriali basati su cloud, convenienti e convenienti, stanno guadagnando terreno, soprattutto tra i fornitori industriali di piccole e medie dimensioni.

5. Medio Oriente e Africa

- Quota di mercato: un mercato in via di sviluppo con un forte potenziale di crescita grazie alla crescente spesa per le infrastrutture militari.

- Fattori chiave: iniziative strategiche nazionali in materia di sanità elettronica e infrastrutture, insieme all'espansione delle infrastrutture sanitarie.

- Tendenze: implementazione di gusci posteriori specializzati e robusti per resistere alle temperature estreme e agli ambienti desertici ostili tipici delle applicazioni militari ed energetiche regionali.

Densità degli attori del mercato Backshell: comprendere il suo impatto sulle dinamiche aziendali

Elevata densità di mercato e concorrenza

Il mercato dei backshell è altamente competitivo, caratterizzato dalla presenza di grandi multinazionali e produttori specializzati di nicchia. Questo scenario è in gran parte determinato dalla natura altamente critica e tecnica di garantire l'integrità del segnale, la tenuta stagna e la schermatura EMI/RFI in applicazioni complesse come l'aerospaziale e la difesa.

La concorrenza si sta intensificando a causa della presenza di importanti attori specializzati in soluzioni di interconnessione complete, come Amphenol Corporation e TE Connectivity, insieme a produttori di componenti specializzati come Glenair, Inc., che forniscono prodotti backshell core ad alta affidabilità.

Questo ambiente competitivo spinge i fornitori a differenziarsi attraverso:

- Integrazione perfetta: sviluppo di backshell che offrono un assemblaggio più rapido, una vestibilità garantita e un'integrazione solida con serie di connettori specifiche e molto richieste (ad esempio, D38999).

- Innovazione dei materiali: investimenti in soluzioni composite leggere e termoplastiche avanzate per applicazioni sensibili al peso nelle moderne piattaforme aeronautiche e di difesa.

- Personalizzazione e conformità: offriamo soluzioni altamente personalizzate e manteniamo una conformità rigorosa e aggiornata con le specifiche militari e aerospaziali in continua evoluzione (ad esempio, AS85049) per garantire l'accettazione normativa globale.

- Gestione termica e ambientale: specializzati in progetti che migliorano la dissipazione termica e garantiscono una tenuta superiore contro temperature estreme, pressioni e fluidi corrosivi.

Opportunità e mosse strategiche

- Collaborare con i principali produttori di aeromobili e difesa: collaborare con i principali OEM (Original Equipment Manufacturer) per sviluppare congiuntamente architetture di interconnessione di nuova generazione e progetti di backshell ottimizzati per le nuove piattaforme.

- Incorpora tecnologie di schermatura avanzate: integra rivestimenti e materiali specializzati per una migliore mitigazione delle interferenze elettromagnetiche/interferenze radio (EMI/RFI) su gamme di frequenza più ampie, affrontando la complessità dei moderni sistemi digitali.

Le principali aziende che operano nel mercato Backshell sono:

- Amphenol Corporation

- Connettività TE

- Glenair, Inc.

- Collins Aerospace

- Curtiss-Wright Corporation

- Souriau Sunbank (Eaton)

- PEI-Genesis

- Isodyne Inc.

- Arrow Electronics

Disclaimer: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e sviluppi recenti sul mercato Backshell

- Amphenol Corporation ha lanciato i backshell AlumaLite: Amphenol Corporation ha presentato la sua serie di backshell AlumaLite, che offre un risparmio di peso fino al 50% rispetto ai design tradizionali. Questi backshell offrono una schermatura EMI e una resistenza alla corrosione superiori, ideali per applicazioni aerospaziali e di difesa.

- TE Connectivity amplia il portfolio di backshell AMPSEAL 16: TE Connectivity ha annunciato nuove varianti di backshell AMPSEAL 16, tra cui configurazioni a 90° e 180° con classificazione di resistenza al fuoco UL94 V-0. L'azienda ha inoltre presentato i backshell a gomito curvo Tinel-Lock, che riducono il peso del 20% per i connettori aerospaziali e militari.

- Glenair sottolinea la rapidità di consegna dei backshell MIL-Spec: Glenair ha messo in evidenza il suo ampio catalogo di backshell conformi allo standard AS85049, con disponibilità in giornata per connettori circolari e rettangolari. L'azienda promuove i backshell a fascetta della serie QT per una rapida installazione e una maggiore protezione EMI.

- Collins Aerospace firma un accordo di manutenzione predittiva con Qatar Airways: Collins Aerospace ha stretto una partnership con Qatar Airways per l'implementazione della sua soluzione di analisi Ascentia nelle flotte Boeing 787, dimostrando ulteriormente il suo impegno nei confronti di sistemi aerospaziali avanzati e soluzioni di affidabilità.

- Curtiss-Wright si aggiudica contratti per la difesa e migliora le previsioni: Curtiss-Wright ha annunciato diversi contratti per la difesa, tra cui sistemi di stabilizzazione della torretta per i veicoli da combattimento XM30 e registratori di volo criptati per gli aerei Bell Textron MV-75. L'azienda ha inoltre migliorato le sue previsioni finanziarie per l'intero anno.

Copertura e risultati del rapporto di mercato Backshell

Il rapporto "Dimensioni e previsioni del mercato Backshell (2021-2034)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato Backshell a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato Backshell, nonché dinamiche di mercato come driver, restrizioni e opportunità chiave

-

Analisi PEST e SWOT dettagliate

Analisi di mercato Backshell che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato - Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti nel mercato Backshell

- Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative