Dimensioni, quota e tendenze del mercato dei pagamenti digitali entro il 2034

Dimensioni e previsioni del mercato dei pagamenti digitali (2021-2034), quota globale e regionale, trend e analisi delle opportunità di crescita. Copertura del report: per componente (soluzioni e servizi), implementazione (on-premise e basata su cloud), dimensione dell'organizzazione (piccole e medie imprese e grandi imprese) e settore (servizi finanziari e assicurativi, vendita al dettaglio ed e-commerce, sanità, viaggi e ospitalità, media e intrattenimento, IT e telecomunicazioni e altri).

- Stato : Dati rilasciati

- Codice del report : TIPRE00007577

- Categoria : Servizi bancari, finanziari e assicurativi

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : March 17, 2026

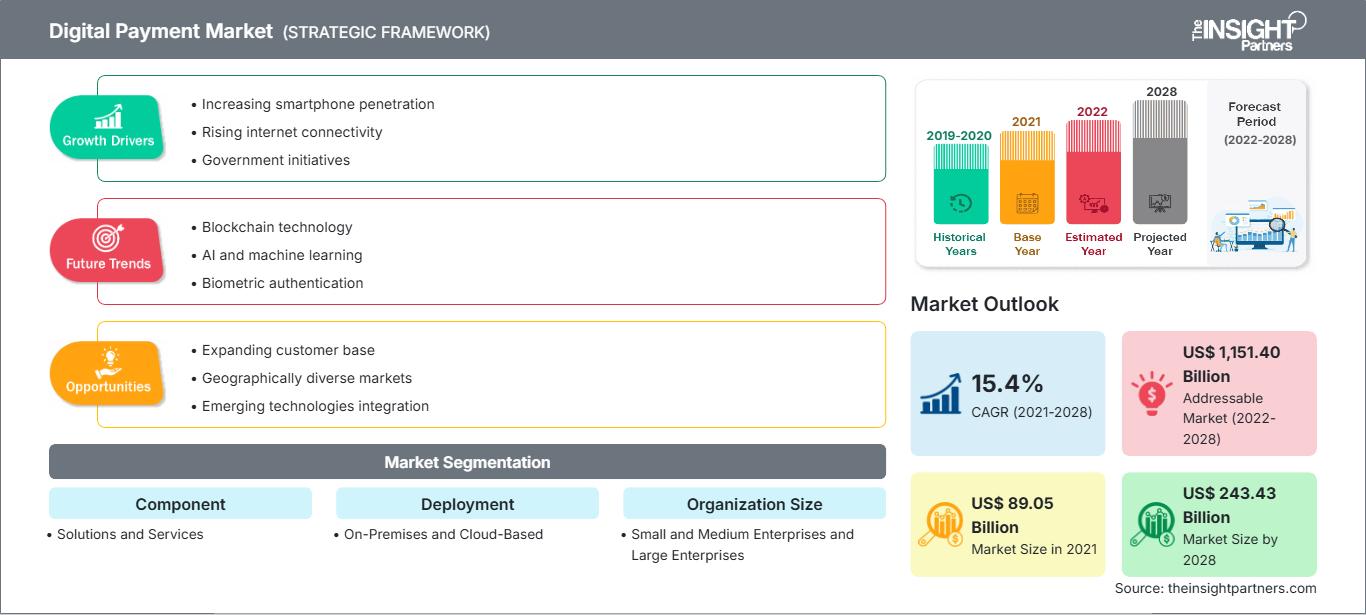

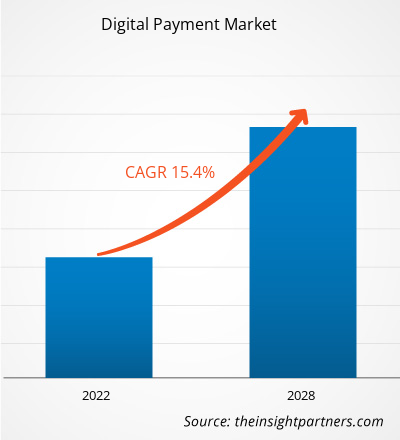

Si prevede che il mercato globale dei pagamenti digitali raggiungerà un valore di 753,14 miliardi di dollari entro il 2034, rispetto ai 170,22 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 15,66% nel periodo di previsione 2026-2034.

Tra le principali dinamiche di mercato si annoverano la crescente attenzione globale verso le transazioni finanziarie contactless, la maggiore consapevolezza dei consumatori in merito alla sicurezza e alla velocità dei portafogli digitali e un significativo spostamento verso ecosistemi di pagamento integrati e basati su software. Inoltre, si prevede che il mercato beneficerà della crescente popolarità dei sistemi di pagamento in tempo reale (RTP), dell'espansione dei canali di e-commerce organizzati nelle economie emergenti e della crescente integrazione della finanza in segmenti ad alto valore aggiunto come assicurazioni, sanità e viaggi.

Analisi del mercato dei pagamenti digitali

L'analisi del mercato dei pagamenti digitali mostra una transizione verso soluzioni integrate ad alto valore aggiunto, in quanto le aziende danno priorità all'efficienza operativa e alla fidelizzazione dei clienti. Le tendenze degli acquisti indicano che il mercato si sta suddividendo tra i settori tradizionali di elaborazione dei pagamenti guidati dalle banche e le piattaforme fintech in rapida crescita, focalizzate su servizi specializzati di "Compra ora, paga dopo" (BNPL) e peer-to-peer (P2P). Si stanno delineando opportunità strategiche nella digitalizzazione delle piccole e medie imprese (PMI) e nei pagamenti B2B transfrontalieri, dove commissioni di transazione inferiori e regolamento in tempo reale offrono un chiaro vantaggio competitivo rispetto ai sistemi di bonifico tradizionali. L'analisi rileva inoltre che l'espansione del mercato dipende dall'integrità della sicurezza informatica per i gateway basati su cloud e dall'interoperabilità tramite API dei sistemi di pagamento nazionali. La differenziazione competitiva si basa ora su un branding che enfatizza la privacy dei dati, interfacce utente intuitive e la capacità di gestire transazioni multivaluta a livello globale.

Panoramica del mercato dei pagamenti digitali

I pagamenti digitali si stanno trasformando da semplice strumento transazionale a pilastro strategico dell'economia digitale. Sebbene storicamente incentrato sull'elaborazione di carte di credito e di debito, il mercato si sta espandendo verso prodotti a valore aggiunto come la verifica dell'identità digitale, l'integrazione con i programmi fedeltà e l'analisi delle frodi basata sull'intelligenza artificiale. Sia i colossi tecnologici globali che le startup fintech locali fanno parte di questo mercato, sfruttando la rapida diffusione degli smartphone e di Internet ad alta velocità. I consumatori europei e nordamericani, sempre più attenti alla sicurezza, cercano alternative al contante, il che ha contribuito alla popolarità dei portafogli digitali come scelta sicura e igienica. L'Asia-Pacifico rimane il principale motore del volume di transazioni. Tuttavia, il Medio Oriente e l'Africa sono diventati leader nell'innovazione del mobile money, soprattutto grazie all'utilizzo di pagamenti tramite codice QR e servizi bancari basati su USSD. Ad esempio, il mercato statunitense è caratterizzato da un ecosistema finanziario maturo in transizione verso esperienze "mobile-first". Spinto da un'elevata spesa dei consumatori e da un solido panorama dell'e-commerce, il mercato sta assistendo a una significativa integrazione della tecnologia contactless nei punti vendita fisici. Le tendenze emergenti si concentrano sulla diffusione dei portafogli digitali e sulla rapida adozione di sistemi di regolamento in tempo reale.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato dei pagamenti digitali: spunti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato dei pagamenti digitali

Fattori trainanti del mercato:

- Proliferazione dell'e-commerce e del m-commerce: la crescita inarrestabile dello shopping online richiede esperienze di pagamento fluide. I metodi di pagamento digitali offrono la comodità, la sicurezza e la portata globale necessarie per supportare negozi online ad alto volume, favorendone così l'adozione su larga scala.

- Spinta governativa verso economie senza contanti: molti governi nazionali stanno implementando politiche per ridurre la dipendenza dal contante al fine di migliorare la trasparenza fiscale e l'inclusione finanziaria. Gli incentivi per l'adozione del digitale e la modernizzazione delle infrastrutture di pagamento nazionali fungono da potenti catalizzatori per la crescita del mercato.

- Progressi tecnologici nella sicurezza: l'integrazione di biometria, tokenizzazione e rilevamento delle frodi basato sull'intelligenza artificiale ha notevolmente migliorato la fiducia dei consumatori. Queste tecnologie riducono i rischi associati alla criminalità informatica, rendendo le transazioni digitali più attraenti rispetto ai metodi tradizionali.

Opportunità di mercato:

- Espansione della finanza integrata: l'integrazione dell'elaborazione dei pagamenti direttamente in applicazioni non finanziarie, come i servizi di trasporto condiviso, i portali sanitari e le piattaforme educative, rappresenta un'enorme opportunità per catturare il valore delle transazioni nel punto di erogazione del servizio.

- Modernizzazione dei pagamenti B2B transfrontalieri: i trasferimenti internazionali tradizionali sono spesso lenti e costosi. Le soluzioni basate su blockchain e DLT offrono un'importante opportunità per fornire alternative più rapide, trasparenti ed economiche per il commercio globale.

- Inclusione finanziaria nei mercati emergenti: l'ampia popolazione non bancarizzata nelle regioni rurali offre un terreno fertile per i fornitori di servizi di pagamento mobile-first. Offrendo punti di accesso a bassa barriera come codici QR e pagamenti tramite cellulare, i fornitori possono raggiungere vaste fasce di popolazione precedentemente escluse dai servizi.

Analisi di segmentazione del mercato dei pagamenti digitali

La quota di mercato dei pagamenti digitali viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per componente:

- Soluzioni: include gateway di pagamento, piattaforme di elaborazione e strumenti di gestione delle frodi. Questo segmento rappresenta la principale fonte di ricavi, poiché le aziende ricercano una sicurezza completa per le transazioni.

- Servizi: Comprende servizi professionali quali consulenza, implementazione e supporto gestito, essenziali per le organizzazioni che migrano da sistemi legacy a moderne infrastrutture digitali.

Per implementazione:

- On-Premises: soluzione preferita dalle grandi istituzioni finanziarie con rigidi requisiti normativi per il controllo dei dati, sebbene richieda un significativo investimento iniziale.

- Basato sul cloud: il modello di implementazione in più rapida crescita, che offre scalabilità e costi operativi inferiori, risultando particolarmente interessante per le PMI e le startup fintech agili.

In base alle dimensioni dell'organizzazione:

- Grandi imprese: dominanti in termini di volume di transazioni, utilizzano sistemi di pagamento sofisticati e multilivello per gestire operazioni globali e ambienti di vendita al dettaglio ad alto traffico.

- Piccole e medie imprese: un segmento in forte crescita, poiché le piccole imprese adottano sempre più soluzioni POS digitali e piattaforme online per raggiungere una base clienti più ampia.

Per settore industriale:

- BFSI: Il settore leader, focalizzato su servizi bancari digitali, premi assicurativi e pagamenti tramite piattaforme di investimento.

- Vendita al dettaglio ed e-commerce: un fattore chiave per l'innovazione, con particolare attenzione ai portafogli digitali, ai servizi "Compra ora, paga dopo" e alle esperienze di pagamento personalizzate.

- Assistenza sanitaria: crescente utilizzo di pagamenti digitali per richieste di rimborso assicurativo, consulti di telemedicina e fatturazione contactless ai pazienti.

- Viaggi e ospitalità: si basano sul supporto multivaluta e su sistemi di prenotazione intuitivi per i viaggiatori internazionali.

- Media e intrattenimento: trainati dall'impennata dei modelli basati su abbonamento per i servizi di streaming e i contenuti digitali.

- IT e telecomunicazioni: elevato volume di fatturazione ricorrente e cicli di pagamento automatizzati per i fornitori di servizi.

- Altri: include i servizi governativi, l'istruzione e i settori dei trasporti.

Per area geografica:

- America del Nord

- Europa

- Asia Pacifico

- Sud e Centro America

- Medio Oriente e Africa

Ambito del rapporto sul mercato dei pagamenti digitali

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 170,22 miliardi di dollari USA |

| Dimensioni del mercato entro il 2034 | 753,14 miliardi di dollari |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 15,66% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per componente

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori nel mercato dei pagamenti digitali: comprenderne l'impatto sulle dinamiche di business.

Il mercato dei pagamenti digitali è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi offerti dal prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato dei pagamenti digitali per area geografica

Si prevede che la regione Asia-Pacifico registrerà la crescita più rapida nei prossimi anni. Anche i mercati emergenti del Sud e Centro America, del Medio Oriente e dell'Africa offrono numerose opportunità inesplorate per l'espansione di fornitori di fintech di alta qualità e operatori di servizi di pagamento mobile.

Il mercato dei pagamenti digitali sta attraversando una profonda trasformazione, passando da una struttura dominata dalle carte a un ecosistema di transazioni ad alta velocità gestite da software. La crescita è trainata dalla crescente diffusione del commercio tramite smartphone, dall'aumento della domanda di pagamenti in tempo reale e dall'espansione del settore bancario digitale. Di seguito una sintesi delle quote di mercato e delle tendenze per regione:

America del Nord

- Quota di mercato: Detiene una quota di mercato leader, grazie a un'infrastruttura finanziaria matura e alla rapida adozione dei portafogli digitali.

-

Fattori chiave:

- Elevata preferenza dei consumatori per i pagamenti contactless (tap-to-pay) e l'integrazione dei portafogli digitali negli acquisti al dettaglio quotidiani.

- Ampia disponibilità da parte degli esercenti e presenza di giganti globali dei pagamenti come PayPal, Visa e Mastercard.

- Espansione aggressiva dei servizi "Compra ora, paga dopo" (BNPL) tra le generazioni Z e Millennial.

- Tendenze: Si osserva un passaggio ai pagamenti invisibili, in cui le transazioni sono integrate direttamente nei dispositivi IoT e nel commercio al dettaglio autonomo. Si registra inoltre un aumento significativo dell'utilizzo dell'autenticazione biometrica basata sull'intelligenza artificiale (riconoscimento facciale e delle impronte digitali) in sostituzione delle password tradizionali.

Europa

- Quota di mercato: Un attore globale di primaria importanza, caratterizzato da solidi quadri normativi e da una forte spinta verso la sovranità finanziaria.

-

Fattori chiave:

- Attuazione del Digital Operational Resilience Act (DORA) e della PSD3 per garantire un sistema bancario aperto sicuro e standardizzato.

- L'ascesa dei pagamenti da conto a conto (A2A), che bypassano i tradizionali circuiti delle carte per ridurre le commissioni degli esercenti.

- Forte sostegno governativo all'euro digitale e alle iniziative di pagamento paneuropee come Wero.

- Tendenze: Il sistema di pagamento tramite bonifico bancario si sta diffondendo sempre di più, riducendo significativamente i tempi di regolamento per gli esercenti. Inoltre, si sta ponendo sempre maggiore attenzione al Portafoglio di identità digitale dell'UE per collegare direttamente la verifica dell'identità all'autorizzazione del pagamento.

Asia-Pacifico

- Quota di mercato: la regione in più rapida crescita, con Cina e India che fungono da principali motori per l'innovazione dei portafogli digitali e dei codici QR.

-

Fattori chiave:

- Un'enorme base di consumatori utilizza super app come Alipay, WeChat Pay e Grab per servizi finanziari completi.

- Iniziative sostenute dal governo come l'UPI indiana, che ha superato il traguardo dei 10 miliardi di transazioni mensili.

- La rapida urbanizzazione e una popolazione che privilegia l'utilizzo dei dispositivi mobili hanno in gran parte saltato la tradizionale fase delle carte di credito.

- Tendenze: Forte dipendenza da standard QR interoperabili (come SGQR e QRIS) che consentono la scansione transfrontaliera tra paesi. Si registra inoltre un'impennata nell'Agentic Commerce, dove gli assistenti basati sull'intelligenza artificiale gestiscono autonomamente abbonamenti e piccoli acquisti per gli utenti.

America meridionale e centrale

- Quota di mercato: Un mercato emergente caratterizzato dalla rapida sostituzione del contante con i sistemi di pagamento istantaneo, in particolare in Brasile.

-

Fattori chiave:

- Pix ha riscosso un successo senza precedenti in Brasile, gestendo ora un numero di transazioni superiore a quello delle carte di credito e di debito messe insieme.

- Modernizzazione delle leggi locali in materia di fintech in Argentina (CoDi) e Colombia per migliorare l'inclusione finanziaria delle persone con accesso limitato ai servizi bancari.

- Crescente interesse per le criptovalute e le stablecoin come strumento di copertura contro la volatilità delle valute locali.

- Tendenze: Crescita degli ecosistemi di Super-App che integrano microcredito e assicurazioni direttamente nel flusso di pagamento. La regione sta inoltre assistendo a una transizione verso gli standard di messaggistica ISO 20022 per facilitare gli scambi commerciali internazionali.

Medio Oriente e Africa

- Quota di mercato: un mercato in via di sviluppo con radici profonde nel settore dei pagamenti tramite dispositivi mobili, che ora sta passando a sistemi commerciali formalizzati in tempo reale.

-

Fattori chiave:

- Il predominio tradizionale dei pagamenti tramite cellulare (ad esempio, M-Pesa) si sta evolvendo verso piattaforme bancarie digitali più sofisticate.

- Nei Paesi del Consiglio di Cooperazione del Golfo (GCC) si registra un'elevata domanda di integrazioni per i pagamenti nelle Smart City, con l'Arabia Saudita che ha raggiunto una quota del 79% di pagamenti elettronici nel settore della vendita al dettaglio.

- Investimenti strategici nei sistemi nazionali di pagamento istantaneo (come Aani negli Emirati Arabi Uniti) per ridurre la dipendenza dal contante.

- Tendenze: Implementazione di modelli di Agency Banking che utilizzano reti di commercianti locali per fornire punti di accesso digitali nelle aree rurali. Grande attenzione è inoltre rivolta alla sicurezza di ambienti di elaborazione sempre attivi 24 ore su 24, 7 giorni su 7, per contrastare le frodi più sofisticate.

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando a causa della presenza di leader finanziari affermati come Finserv Inc. e PayPal Holdings, Inc. Giganti fintech regionali come Ant Group (Alipay) e Tencent (WeChat Pay), insieme a operatori innovativi e dirompenti come Stripe, Inc. e Adyen NV, contribuiscono a un panorama di mercato diversificato e in rapida espansione.

Questo contesto competitivo spinge i fornitori a differenziarsi attraverso:

- Finanza integrata e personalizzazione: posizionare le piattaforme di pagamento come hub finanziari che offrono più delle semplici transazioni, tra cui credito, assicurazioni e programmi fedeltà gestiti dall'intelligenza artificiale.

- Flessibilità multi-rail: le aziende leader offrono ora un approccio commerciale unificato, che consente ai commercianti di accettare carte, trasferimenti A2A e portafogli digitali tramite un'unica integrazione.

- Soluzioni verticali specifiche: Sviluppo di sistemi di pagamento specializzati per settori come la sanità (fatturazione conforme a HIPAA) e i viaggi (pagamenti in tempo reale in più valute).

- Infrastruttura di sicurezza avanzata: utilizzo di tokenizzazione, apprendimento automatico per il rilevamento delle frodi e chiavi di accesso biometriche per garantire un'elevata sicurezza delle transazioni.

Opportunità e mosse strategiche

- Puntare al segmento B2B transfrontaliero: collaborare con fornitori di blockchain e DLT per semplificare il processo, tradizionalmente lento e costoso, di rimesse aziendali internazionali.

- Adotta l'efficienza operativa basata sull'intelligenza artificiale: integra la riconciliazione automatizzata e l'instradamento intelligente per aiutare i commercianti a ridurre al minimo i costi di transazione e massimizzare i tassi di successo.

Le principali aziende operanti nel mercato dei pagamenti digitali sono:

- ACI WORLDWIDE, INC

- Adyen Financial Software & Systems Pvt. Ltd.

- Fiserv, Inc.

- Global Payments Inc.

- Novatti Group Ltd

- PayPal Holdings, Inc.

- Paysafe Limited

- Block, Inc.

- PayU

Nota: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e ultimi sviluppi sul mercato dei pagamenti digitali

- Nel febbraio 2025, Stripe ha completato l'acquisizione di Bridge. Questa acquisizione strategica è stata finalizzata per accelerare l'integrazione delle stablecoin nella rete globale di pagamenti digitali di Stripe, fornendo alle aziende strumenti più efficienti per le transazioni finanziarie transfrontaliere.

- Nel dicembre 2024, Visa ha completato l'acquisizione di Featurespace, azienda sviluppatrice di tecnologie di protezione dei pagamenti basate sull'intelligenza artificiale (IA) in tempo reale. Questa mossa strategica è stata concepita per rafforzare le capacità di Visa in materia di protezione dalle frodi e migliorare la sicurezza dei propri clienti di pagamenti digitali e dei consumatori di tutto il mondo, prevenendo e mitigando i rischi di criminalità finanziaria.

Copertura e risultati del rapporto sul mercato dei pagamenti digitali.

Il rapporto "Dimensioni e previsioni del mercato dei pagamenti digitali (2021-2034)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni e previsioni del mercato dei pagamenti digitali a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato dei pagamenti digitali, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave.

- Analisi PEST e SWOT dettagliata

- Analisi del mercato dei pagamenti digitali, con particolare attenzione alle principali tendenze di mercato, al quadro globale e regionale, ai principali operatori, alle normative e ai recenti sviluppi del mercato.

- Analisi del panorama di settore e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa termica, ai principali operatori e ai recenti sviluppi nel mercato dei pagamenti digitali.

- Profili aziendali dettagliati

Ankita è una dinamica professionista della ricerca di mercato e della consulenza con oltre 8 anni di esperienza nei settori della tecnologia, dei media, dell'ICT, dell'elettronica e dei semiconduttori. Ha guidato e portato a termine con successo oltre 100 incarichi di consulenza e ricerca per clienti globali come Microsoft, Oracle, NEC Corporation, SAP, KPMG ed Expeditors International. Le sue competenze principali includono la valutazione del mercato, l'analisi dei dati, le previsioni, la formulazione di strategie, l'intelligence competitiva e la redazione di report.

Ankita è esperta nella gestione di cicli di progetto completi, dalla progettazione di proposte pre-vendita e discussioni con i clienti fino alla fornitura di insight fruibili post-vendita. È esperta nella gestione di team interfunzionali, nella strutturazione di moduli di ricerca complessi e nell'allineamento delle soluzioni agli obiettivi aziendali specifici del cliente. Le sue eccellenti capacità di comunicazione, leadership e presentazione le hanno permesso di fornire costantemente risultati orientati al valore in contesti di mercato in rapida evoluzione.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative