Analisi e previsioni del mercato dei sistemi di sorveglianza e avvistamento optronici militari per dimensioni, quota, crescita, tendenze 2031

Dati storici : 2021-2022 | Anno base : 2023 | Periodo di previsione : 2024-2031Dimensioni e previsioni del mercato dei sistemi di sorveglianza e avvistamento optronici militari (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tipo (intensificazione dell'immagine, sistemi laser militari ed elettroottica o infrarossi), componente (dispositivi per la visione notturna, dispositivi di imaging termico portatili, apparecchiature di osservazione integrate, sensori autonomi a infrarossi, sismici e acustici e altri), utenti finali (terrestri, aerei e navali) e geografia.

- Stato : Edito

- Codice del report : TIPRE00025007

- Categoria : Aerospaziale e difesa

- Numero di pagine : 208

- Formati di report disponibili :

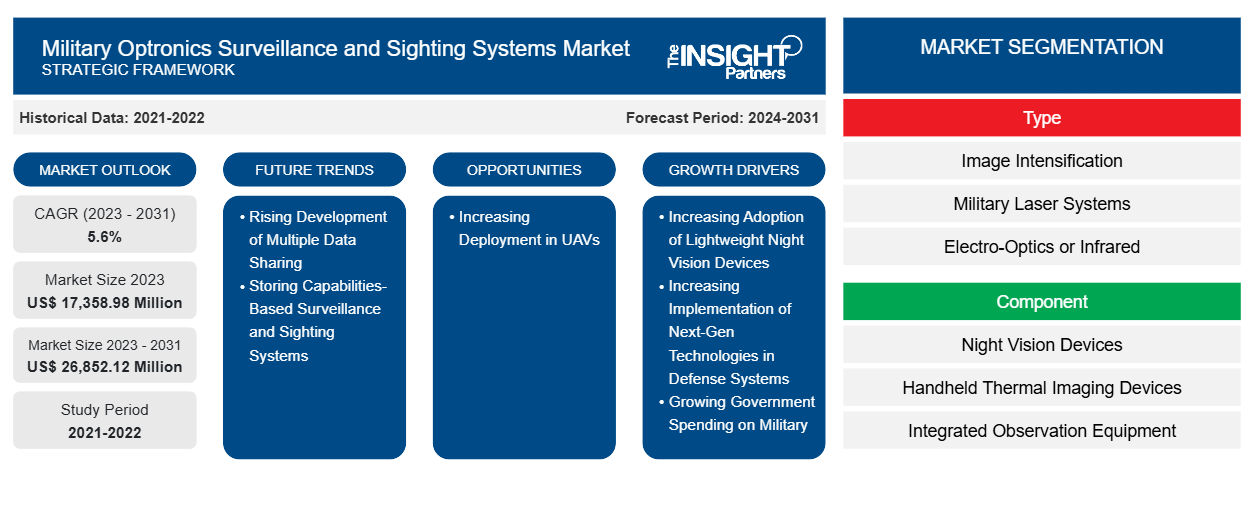

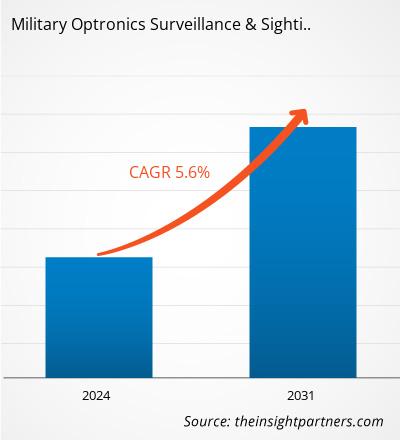

Si prevede che il mercato dei sistemi di sorveglianza e avvistamento optronici militari raggiungerà i 26.852,12 milioni di dollari entro il 2031, rispetto ai 17.358,98 milioni di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 5,6% nel periodo 2023-2031. È probabile che il crescente sviluppo di sistemi di sorveglianza e avvistamento basati su capacità di condivisione e archiviazione di dati multipli porti nuove tendenze chiave nel mercato nei prossimi anni.

Analisi di mercato dei sistemi di sorveglianza e avvistamento optronici militari

Con la crescente innovazione e la crescente minaccia di attacchi terroristici notturni, l'adozione di dispositivi per la visione notturna è in aumento. Allo stesso modo, l'imaging termico aiuta i soldati a localizzare un bersaglio in condizioni di scarsa visibilità. I dispositivi per la visione notturna con imaging termico stanno guadagnando popolarità in tutto il mondo per rafforzare i sistemi individuali dei combattenti. I dispositivi per la visione notturna forniscono ai soldati una maggiore consapevolezza della situazione illuminando l'ambiente circostante durante le operazioni notturne. Le crescenti iniziative governative per sviluppare e adottare dispositivi per la visione notturna leggeri basati su tecnologie avanzate hanno creato un'enorme domanda per la crescita del mercato dei sistemi di sorveglianza e avvistamento optronici militari. Ad esempio, a gennaio 2022, la Defence Advanced Research Projects Agency (DARPA) del Dipartimento della Difesa degli Stati Uniti ha selezionato 10 team di ricerca universitari e di difesa per lo sviluppo di ottiche leggere per la visione notturna per i soldati militari in America. Il dipartimento ha progettato il programma Enhanced Night Vision in Eyeglass Form (ENVision) per adottare la nuova tecnologia per sviluppare sistemi per la visione notturna.

Si prevede che l'aumento dell'impiego di UAV in tutto il mondo per proteggere i territori dai paesi confinanti creerà ampie opportunità per la crescita del mercato dei sistemi di sorveglianza e avvistamento optronici durante il periodo di previsione. Ad esempio, nel 2022, l'esercito indiano ha schierato il primo lotto di oltre 25 UAV di fabbricazione israeliana denominati Searcher Mark II. Inoltre, a maggio 2024, il governo degli Stati Uniti ha iniziato a consegnare UAV ai propri militari come parte del suo programma governativo per contrastare le capacità di difesa della Cina. Inoltre, a marzo 2023, gli scienziati in Cina hanno sviluppato un drone militare in grado di dividersi rapidamente in sei unità separate a mezz'aria. Questi droni sono realizzati con tecnologie di separazione dell'aria. Si prevede che tali crescenti investimenti e l'impiego di UAV da parte dei governi di diversi paesi creeranno ampie opportunità per il mercato dei sistemi di sorveglianza e avvistamento optronici durante il periodo di previsione.

Panoramica del mercato dei sistemi di sorveglianza e avvistamento optronici militari

I sistemi di optronica, sorveglianza e avvistamento militari forniscono al personale strumenti sufficienti per identificare, tracciare, monitorare e affrontare minacce in ambienti di guerra aerea, terrestre e navale. Questi sistemi forniscono alle forze armate rilevamento, riconoscimento e identificazione precisi di obiettivi e consapevolezza della situazione utilizzando un'integrazione di componenti ottici ad alte prestazioni e sensori avanzati. Inoltre, i sistemi di optronica, sorveglianza e avvistamento trovano applicazione nel soddisfare i requisiti delle missioni di controllo delle frontiere, protezione delle basi, ricognizione e raccolta di informazioni. I progressi tecnologici nei sistemi di optronica e sorveglianza, uniti alla continua richiesta delle forze di difesa di aggiornare le proprie apparecchiature e sistemi esistenti, stanno guidando il mercato globale dei sistemi di optronica, sorveglianza e avvistamento militari.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dei sistemi di sorveglianza e avvistamento optronici militari: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato per i sistemi di sorveglianza e di puntamento optronici militari

Crescente adozione di dispositivi leggeri per la visione notturna

Con la crescente innovazione e la crescente minaccia di attacchi terroristici notturni, l'adozione di dispositivi per la visione notturna è in aumento. In precedenza, i dispositivi per la visione notturna utilizzavano componenti relativamente più pesanti, aggiungendo peso a un soldato. Vari attori del mercato stanno ora introducendo prodotti per la visione notturna leggeri. Ad esempio, ACTinBlack ha sviluppato un dispositivo per la visione notturna binoculare leggero con elevate prestazioni ottiche e un design ergonomico. Nell'ottobre 2023, Thermoteknix Systems, un'azienda statunitense di termografia e realtà aumentata (AR), ha lanciato una soluzione per la visione notturna chiamata Fused Night Vision Goggle con realtà aumentata avanzata (FNVG-AR). Il sistema FNVG-AR è un visore notturno binoculare leggero (NVG) integrato con tubi per la visione notturna al fosforo bianco da 16 mm di nuova generazione basati su tecnologia avanzata e una termocamera ad alta risoluzione.

Aumento dell'impiego di UAV

I sistemi senza pilota sono diventati parte integrante delle forze militari in tutto il mondo, poiché riducono il rischio per le vite umane. Grazie ai vari vantaggi offerti dai veicoli aerei senza pilota (UAV), molti paesi, come gli Stati Uniti, l'India e la Cina, hanno stanziato budget sostanziali per distribuire più UAV nelle loro forze militari, principalmente per applicazioni di sorveglianza. L'implementazione di sistemi di sorveglianza e avvistamento optronici su piattaforme senza pilota facilita la trasmissione di dati di sorveglianza e immagini. L'integrazione di sistemi senza pilota con antenne di comunicazione e altre apparecchiature di sorveglianza aiuta in varie missioni critiche. Pertanto, il crescente impiego di UAV per missioni di sorveglianza e mappatura aeree e navali sta determinando una crescente necessità di sistemi di sorveglianza e avvistamento optronici che possano essere efficacemente integrati nella piattaforma UAV senza ostacolarne l'efficienza complessiva. Pertanto, diversi importanti attori del settore, tra cui Rafael Advanced Defense Systems Ltd. e Lockheed Martin, nel mercato dei sistemi di sorveglianza e avvistamento optronici militari sottolineano lo sviluppo e l'offerta di sistemi di sorveglianza e avvistamento optronici per piattaforme UAV.

Analisi della segmentazione del rapporto di mercato sui sistemi di sorveglianza e avvistamento optronici militari

I segmenti chiave che hanno contribuito alla derivazione dell'analisi del mercato dei sistemi di sorveglianza e di avvistamento optronici militari sonotipologia, componente e utenti finali.

- In base al tipo, il mercato dei sistemi di sorveglianza e avvistamento optronici militari è classificato in intensificazione dell'immagine, sistemi laser militari ed elettro-ottica/infrarossi. Il segmento elettro-ottica ha detenuto la quota maggiore del mercato nel 2023.

- Per componente, il mercato è categorizzato in dispositivi per la visione notturna, dispositivi di imaging termico portatili, apparecchiature di osservazione integrate, sensori a infrarossi, sismici e acustici autonomi e altri. Il segmento dei sensori sismici e acustici ha dominato il mercato nel 2023.

- In termini di utenti finali, il mercato dei sistemi di sorveglianza e avvistamento optronici militari è suddiviso in terrestre, aereo e navale. Il segmento terrestre ha detenuto la quota maggiore del mercato nel 2023.

Analisi della quota di mercato dei sistemi di sorveglianza e di puntamento optronici militari

L'ambito geografico del rapporto sul mercato dei sistemi di sorveglianza e avvistamento optronici militari offre un'analisi globale dettagliata. Nord America, Europa e Asia Pacifico sono le principali regioni che stanno assistendo a una crescita significativa nel mercato dei sistemi di sorveglianza e avvistamento optronici militari. Il mercato dei sistemi di sorveglianza e avvistamento optronici militari in Nord America è ulteriormente segmentato in Stati Uniti, Canada e Messico. Nel 2023, gli Stati Uniti hanno dominato il mercato dei sistemi di sorveglianza e avvistamento optronici militari in Nord America con una quota di mercato significativa nel 2023, seguiti da Canada e Messico. Queste economie sviluppate spendono una parte considerevole del loro PIL in spese militari. Secondo la raccolta di indicatori di sviluppo della Banca Mondiale, che sono compilati da fonti ufficialmente riconosciute, la spesa militare negli Stati Uniti è stata segnalata come circa il 3,5% del suo PIL nel 2023. Inoltre, nell'anno fiscale 2023, il governo degli Stati Uniti ha speso 820 miliardi di dollari nel settore della difesa nazionale, secondo il Dipartimento federale del bilancio degli Stati Uniti. L'importo è stato stimato essere il 13% della spesa federale degli Stati Uniti. I principali attori del mercato stanno sviluppando tecnologie avanzate basate su sistemi di sorveglianza optronica aerea, telecamere termiche digitali avanzate, sistemi di tracciamento e ricerca e altri. Ad esempio, la Obsidian Sensors Inc. con sede negli Stati Uniti ha lanciato una nuova tecnologia nel 2023 che elabora le immagini termiche utilizzando sensori ad alta risoluzione a prezzi accessibili.

Approfondimenti regionali sul mercato dei sistemi di sorveglianza e di avvistamento optronici militari

Le tendenze regionali e i fattori che influenzano il mercato dei sistemi di sorveglianza e avvistamento optronici militari durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato dei sistemi di sorveglianza e avvistamento optronici militari in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato dei sistemi di sorveglianza e avvistamento optronici militari

Ambito del rapporto di mercato sui sistemi di sorveglianza e avvistamento optronici militari

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 17.358,98 milioni di dollari USA |

| Dimensioni del mercato entro il 2031 | 26.852,12 milioni di dollari USA |

| CAGR globale (2023-2031) | 5,6% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per tipo

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Sistemi di sorveglianza e avvistamento optronici militari Densità dei player del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei sistemi di sorveglianza e puntamento optronici militari sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato dei sistemi di sorveglianza e puntamento optronici militari sono:

- Aereo

- Società per azioni Lockheed Martin

- Gruppo Talete

- Società di General Dynamics

- Società controllata da L3Harris Technologies Inc.

- Industrie aerospaziali israeliane

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato dei sistemi di sorveglianza e di avvistamento optronici militari

Notizie di mercato e sviluppi recenti sui sistemi di sorveglianza e avvistamento optronici militari

Il mercato dei sistemi di sorveglianza e avvistamento optronici militari viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato dei sistemi di sorveglianza e avvistamento optronici militari:

- Lo specialista di sensori HENSOLDT sta fornendo un numero imprecisato di sistemi di visione ottica all'avanguardia per il veicolo da combattimento della fanteria PUMA. I clienti sono le case di sistema KNDS e Rheinmetall, che producono il veicolo da combattimento della fanteria PUMA e lo distribuiscono tramite la PSM GmbH fondata congiuntamente. Il valore dell'ordine è nell'ordine di milioni a due cifre. Oltre ai sistemi di visione per le torrette dei veicoli da combattimento della fanteria, l'ordine include l'equipaggiamento per dodici addestratori di torrette per l'addestramento degli equipaggi dei veicoli. Con questa consegna, HENSOLDT sta contribuendo a migliorare il PUMA sul K-Stand S1. (Fonte: HENSOLDT, comunicato stampa, giugno 2024)

- Le forze armate francesi hanno ricevuto i primi 300 visori notturni Thales ordinati dalla French Defence Procurement Agency (DGA) nel 2020 come parte del contratto Bi-NYX. I 300 visori consegnati alla DGA sono il primo lotto di un ordine di 2.000 set effettuato a dicembre 2023. I restanti 1.700 saranno spediti entro la fine dell'anno. (Fonte: Thales, comunicato stampa, ottobre 2024)

Copertura e risultati del rapporto di mercato sui sistemi di sorveglianza e avvistamento optronici militari

Il rapporto "Dimensioni e previsioni del mercato dei sistemi di sorveglianza e avvistamento optronici militari (2021-2031)" fornisce un'analisi dettagliata del mercato che copre:

- Dimensioni e previsioni del mercato dei sistemi di sorveglianza e avvistamento optronici militari a livello nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato dei sistemi di sorveglianza e di puntamento optronici militari, nonché dinamiche di mercato quali driver, sistemi di ritenuta e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato dei sistemi di sorveglianza e avvistamento optronici militari che copre le principali tendenze di mercato, il quadro nazionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato dei sistemi di sorveglianza e di puntamento optronici militari

- Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Sblocca sconti esclusivi sui report

Richiedi ora

Ottieni un campione gratuito per - Mercato dei sistemi di sorveglianza e avvistamento optoelettronici militari

Ottieni un campione gratuito per - Mercato dei sistemi di sorveglianza e avvistamento optoelettronici militari