3D Mobile Market Growth, Size & Forecast by 2034

Coverage: By Type (3D Smartphones, 3D Tablets, 3D Notebooks, 3D E-Book Readers, Others); Components (Processor, Software, 3D Display, Image Sensor); Application (3D Mobile Gaming, 3D Mobile Advertisement, 3D Mobile Maps Navigation, 3D Mobile Device Protection, 3D Mobile Digital Content, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPTE100000775

- Category : Electronics and Semiconductor

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 16, 2026

2025 Market Size

US$ 13.89 Bn

Base year value

2034 Forecast

US$ 34.86 Bn

Projected by 2034

CAGR 2026-2034

10.76 %

Growth rate

Addressable Market

US$ 215.71 Bn

(2026-2034)

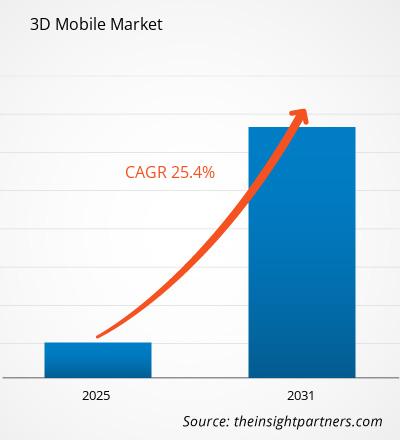

The 3D Mobile Market is expanding as mobile devices, spatial imaging, immersive displays, and depth-enabled interfaces converge across consumer and enterprise environments. The 3D Mobile market was valued at US$ 13.89 Billion in 2025 and is projected to reach US$ 34.86 Billion by 2034, advancing at a CAGR of 10.76% from 2026 to 2034. Growth is supported by stronger visual computing, AI-assisted cameras, and rising demand for interactive mobile experiences.

North America remains a high-value region for the 3D Mobile Market, with an estimated CAGR of 9.8%–10.6% through 2034. Regional momentum is shaped by premium smartphone replacement, strong mobile content creation, and early enterprise use of spatial computing. Telecom upgrades, medical visualization tools, and professional applications using depth perception and augmented interaction further support adoption across connected devices.

3D Mobile Market Assessment and Insights

- North America held a 27%–31% share of the 3D mobile market in 2025 and is growing at a CAGR between 2026 – 2034 of 9.8%–10.6%, supported by premium devices, 5G availability, spatial content creation, and enterprise visualization.

- The U.S. represented a 72%–78% North America 3D mobile market size in 2025 and is expanding at a CAGR between 2026 – 2034 of 9.6%–10.4%, led by device ecosystems and mobile imaging.

- Europe accounted for a 20%–24% of the 3D mobile market share in 2025 and is advancing at a CAGR between 2026 – 2034 of 8.8%–9.6%, with Germany, the UK, France, Italy, and Spain leading practical adoption.

- Asia Pacific held a 38%–43% of the 3D mobile market share in 2025 and is growing at a CAGR between 2026 – 2034 of 11.5%–12.4%, driven by China, Japan, South Korea, India, and large-scale electronics manufacturing.

- Largest Segment: 3D Smartphones held 46%–51% of the 3D mobile market share in 2025, growing at a CAGR between 2026 – 2034 of 10.4%–11.2%, supported by cameras, displays, and gaming.

- High Growth Segment: 3D Mobile Digital Content held 18%–22% of the 3D mobile market share in 2025, growing at a CAGR between 2026 – 2034 of 12.1%–13.0%, supported by AI media conversion.

- Key companies analyzed in detail: Apple Inc., LG Electronics Inc., ROKiT Phones, HTC Corporation, Samsung Electronics Co., Ltd., Sony Group Corporation, Nokia Corporation, OPPO, Sharp Corporation, Qualcomm Technologies, Inc., ZTE Corporation.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The 3D Mobile Market report has shifted from niche stereoscopic handsets toward depth-enabled devices, spatial media, and immersive user interfaces. Earlier adoption was constrained by limited content and viewing comfort, but current production dynamics are stronger because OLED displays, multi-camera modules, AI rendering, and mobile processors now support better depth capture and smoother visualization. This transition is broadening the 3D Mobile scope from entertainment into healthcare, maps, advertising, and field-service workflows.

Forward momentum will depend on ecosystem investment, regional manufacturing scale, and regulatory support for digital infrastructure. Emerging geographies are gaining relevance as 5G coverage, electronics manufacturing incentives, and mobile gaming adoption strengthen. The 3D Mobile trends most likely to influence long-term adoption include AI-assisted 2D-to-3D conversion, glasses-free display progress, and enterprise-grade mobile visualization that turns depth capability into measurable operational value.

3D Mobile Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 13.89 Billion |

| Market Size by 2034 | US$ 34.86 Billion |

| Global CAGR (2026 - 2034) | 10.76% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

3D Mobile Market Analysis

The 3d mobile Market is influenced by the rising need for richer mobile visualization across communication, entertainment, healthcare, and equipment control. Demand is not limited to standalone 3D phones; it includes mobile devices that capture, process, display, or transmit depth-based content. Improvements in OLED panels, computational photography, and edge AI are helping reduce earlier barriers around eye strain, latency, and content quality.

The value chain combines display suppliers, mobile chipset providers, camera module developers, handset OEMs, application developers, and telecom infrastructure partners. Qualcomm Technologies, Inc. contributes enabling silicon for graphics and spatial workloads, while Apple, Inc., Samsung, Sony, LG Electronics Inc., Nokia, HTC, Oppo, Sharp Corporation, and ROKiT Phones represent different positions across devices, immersive media, and mobile experience design.

Competition is shaped by the ability to combine hardware differentiation with content ecosystems. Premium brands are emphasizing spatial video, advanced displays, and camera intelligence, while specialized players focus on affordability or distinctive viewing formats. Strategic positioning increasingly depends on whether 3D functionality improves daily utility rather than remaining a novelty feature.

Investment trends are shifting toward AI-assisted depth reconstruction, lightweight optics, immersive collaboration, and low-power visual processing. Companies are allocating resources to software layers that convert ordinary media into spatial formats and make 3D interaction more seamless. This creates opportunities for device makers, app developers, telecom operators, and enterprise solution providers to participate in a more integrated 3D mobile ecosystem.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

3D Mobile Market: Strategic Insights

Regional Insights

North America 3D Mobile Market

North America is expected to post a CAGR of about 9.8%–10.6%, supported by premium device replacement cycles, strong mobile content creation, and enterprise interest in spatial communication. The region benefits from advanced 5G networks, high consumer spending, and a developer ecosystem that can translate 3D capability into gaming, training, healthcare, and productivity applications.

Structural growth is also tied to cloud services, AI imaging, and cross-device ecosystems. Apple, Inc., Qualcomm Technologies, Inc., and Samsung influence adoption through hardware, software, and chipset innovation. Demand is strongest where 3D mobile functions support media production, professional visualization, telemedicine, industrial inspection, and immersive learning rather than simple entertainment-led differentiation.

U.S. 3D Mobile Market

The U.S. accounts for an estimated 72%–78% share of North America’s 3d mobile Market and is projected to grow at nearly 10% CAGR. Demand is led by premium smartphones, XR-adjacent devices, mobile gaming, medical visualization, and enterprise collaboration tools that require accurate depth sensing and high-quality visual processing.

Company presence is strong across the U.S. mobile and semiconductor ecosystem. Apple, Inc. strengthens spatial content capture, while Qualcomm Technologies, Inc. supports graphics, AI, and connectivity performance for immersive devices. Application trends are expanding from consumer electronics into medical equipment, telecommunication equipment, and industrial automation, where 3D visualization improves remote decisions.

Europe 3D Mobile Market

Europe holds an estimated 20%–24% share of the global 3d mobile Market, with a CAGR of around 8.8%–9.6%. Germany is the leading country due to its industrial automation base, precision engineering culture, and demand for advanced visualization in manufacturing, healthcare, and connected equipment environments.

The UK 3D mobile market is influenced by games, creative media, telecommunications upgrades, and healthcare digitization. The implementation is most effective when 3D mobile technologies improve content creation, distance learning, and professional communication. Both operators and device suppliers concentrate on improving user experience, data effectiveness, and compatibility within a broad mobile ecosystem.

Germany is ahead of other European countries in using mobile visualization for engineering reviews, maintenance, and manufacturing control. At the same time, France, Italy, and Spain are contributing through their adoption of consumer electronics, the development of 5G services, and the digitalization of health care. Regional progress depends on practical enterprise use cases and the availability of premium devices rather than mass-market stereoscopic phones alone.

APAC 3D Mobile Market

Asia Pacific leads the 3d mobile Market with an estimated 38%–43% global share and a CAGR of roughly 11.5%–12.4%. China is the leading country, supported by large-scale smartphone manufacturing, display panel capacity, mobile gaming demand, and policy support for advanced electronics, digital infrastructure, and industrial upgrading.

The ecosystem in China is defined by the size of its components, innovations in devices, and the rapid adoption of mobile technology with AI. Japan and South Korea bring value in displays and cameras, gaming, and premium consumer electronics. Samsung, Sony, Sharp Corporation, LG Electronics Inc., and Oppo remain relevant via their devices, panels, imaging, and experience design.

India and Australia grow through 5G adoption, content consumption, edtech, and enterprise digitization. The industrial and policy factors driving growth include electronics manufacturing incentives, smart factories, medical technology upgrades, and digital services offered by telecommunications companies. Growth opportunities in APAC result from supply-side scale and diversification of use cases.

Middle East & Africa 3D Mobile Market

The Middle East & Africa 3d mobile Market is developing at an estimated CAGR of 8.2%–9.2%. The UAE is the leading country, supported by smart city programs, advanced telecom networks, digital tourism, and enterprise modernization. Saudi Arabia is also gaining relevance through infrastructure expansion and technology-led economic diversification.

Energy and infrastructure projects require the practical use of 3D mobile visualizations for field inspections, maintenance, engineering reviews, and training. Improvements in the telecom network enable greater data exchange, and office equipment and collaboration tools enable more immersive communication among distributed teams. This technology is predominantly used in urban, high-income markets and major institutional projects.

While South Africa and the rest of MEA have seen a gradual uptake in this area, it is mostly used in educational, healthcare, mining, and utility applications. The cost considerations continue to limit adoption in this region, but the use of durable hardware, cloud-based rendering, and telecom partners can help overcome this barrier. Long-term opportunities are strongest where 3D mobile tools reduce travel, improve safety, or support technical decision-making.

Segmentation Analysis

Type

The Type segment is expected to grow at a CAGR of 10.1%–10.9% from 2026–2034. Demand is shaped by how effectively device formats balance screen size, portability, battery performance, and content compatibility. Smartphones dominate because they combine capture, processing, and sharing, while tablets and notebooks are becoming important for education, design, gaming, and professional visualization.

- 3D Smartphones: The largest device category, supported by mobile gaming, depth-enabled cameras, premium displays, and demand for richer digital content experiences in compact, always-connected devices.

- 3D Tablets: Adoption is strongest in education, design review, media consumption, and enterprise visualization where larger screens improve depth perception and collaborative presentation value.

- 3D Notebooks: Growth is linked to gaming, creator workflows, engineering visualization, and portable workstation use cases that require stronger processors and graphics capability.

- 3D E-Book Readers: A niche segment where opportunity depends on interactive learning, illustrated publishing, children’s content, and low-power display innovation rather than mass consumer replacement cycles.

Components

The Components segment is projected to grow at a CAGR of 10.6%–11.4% from 2026–2034. Processors, software, 3D displays, and image sensors increasingly operate as an integrated stack. The 3D Mobile analysis indicates that differentiation depends less on one component and more on optimized power use, rendering speed, sensor accuracy, and developer support across devices.

- Processor: Processors determine rendering speed, AI acceleration, graphics quality, and battery efficiency, making them central to smooth 3D gaming, mapping, and content interaction.

- Software: Software enables depth rendering, content optimization, sensor fusion, developer tools, and application compatibility, reducing friction between hardware capability and user adoption.

- 3D Display: 3D displays define the visible experience, with glasses-free viewing, brightness, resolution, and viewing-angle performance influencing consumer acceptance and premium-device differentiation.

- Image Sensor: Image sensors support depth capture, gesture recognition, biometric functions, spatial mapping, and content creation, expanding the market beyond passive viewing into interactive use cases.

Application

The Application segment is forecast to grow at a CAGR of 11.0%–11.8% from 2026–2034. Mobile gaming leads current monetization, but advertising, navigation, device protection, and digital content are creating broader commercial relevance. As AI improves content conversion and spatial interaction, applications are expected to influence 3D Mobile growth more strongly than hardware novelty alone.

- 3D Mobile Gaming: The leading application, driven by immersive gameplay, premium graphics, competitive engagement, and device upgrades among users seeking more realistic mobile entertainment.

- 3D Mobile Advertisement: Brands use 3D formats to improve product visualization, interaction time, and campaign differentiation, particularly in retail, automotive, fashion, and entertainment categories.

- 3D Mobile Maps Navigation: Depth-based navigation improves spatial awareness for urban mobility, tourism, indoor mapping, and field operations where flat maps can limit situational understanding.

- 3D Mobile Device Protection: This segment supports visual diagnostics, biometric access, protective visualization overlays, and device-security interfaces that use depth data to enhance user confidence.

- 3D Mobile Digital Content: Digital content includes streaming, education, creator media, and social interaction, with adoption shaped by content availability and easier capture-to-share workflows.

Opportunity Snapshot

| Application | Revenue Contribution | Trend Tag | Adoption Stage |

| 3D Mobile Gaming | High | Immersive Play | Mature |

| 3D Mobile Advertisement | Medium | Product Views | Scaling |

| 3D Mobile Maps Navigation | Medium | Spatial Routes | Scaling |

| 3D Mobile Device Protection | Low | Depth Security | Emerging |

| 3D Mobile Digital Content | High | Spatial Media | Scaling |

3D Mobile Market Growth Drivers and Impact Analysis

Rising Demand for Spatial Media and Immersive Mobile Experiences

Consumer behavior is shifting from flat content consumption toward more interactive and depth-rich experiences, creating a strong foundation for the 3d mobile Market. Mobile users increasingly expect cameras, displays, games, and communication tools to deliver realism, personalization, and visual engagement. Spatial video capture, AI-based image enhancement, and glasses-free viewing concepts are helping manufacturers reposition 3D capability as a practical content feature rather than a short-lived device gimmick.

This driver is evident in premium phone differentiation, gaming capabilities on phones, and creator-centric features from companies like Apple, Inc., Samsung, Sony, and Oppo. As more people create spatial media with smartphones, there will be an increasing need for display devices, processors, and storage systems to support the creation of 3D media. This will affect application developers, telecom companies, and accessory makers, widening the commercial ecosystem around 3D mobile experiences.

Advances in Mobile Chipsets, Cameras, and Display Technologies

Technology improvements are lowering the practical barriers that previously limited 3D mobile adoption. Faster chipsets, dedicated graphics engines, neural processors, multi-camera systems, and high-refresh displays enable smoother depth rendering and more comfortable viewing. Qualcomm Technologies, Inc. plays an important role in enabling mobile visual computing, while display expertise from Samsung, LG Electronics Inc., Sony, and Sharp Corporation supports higher brightness, higher resolution, and greater form-factor flexibility.

Real-world implications would include an expanded target market for products across consumer electronics, telecommunications equipment, medical equipment, and industrial automation. Advanced hardware enables 3D capabilities without unnecessary battery depletion or thermal issues. This enhances the usability of devices, makes them suitable for business applications, and motivates OEMs to offer depth capabilities at various price points.

Enterprise Adoption of Mobile Visualization and Remote Assistance

Enterprise use cases are becoming a meaningful driver of demand as organizations seek mobile tools to improve remote guidance, training, inspection, and decision-making. Demanders seek mobile solutions that enable remote guidance, training, inspection, and decision-making capabilities. The use of a 3D mobile interface in industrial automation enables technicians to learn about equipment configuration, detect problems, and execute instructions in a digital environment. Depth-enabled mobile visualization may be used in the healthcare sector for diagnostics, education, and discussions of surgical planning without the need for fixed imaging stations.

The business value becomes apparent when 3D mobile capabilities minimize travel, shorten training cycles, or ensure greater operational precision. Telecom operators win because such use case scenarios imply high-bandwidth connectivity requirements. Mobile device vendors have an opportunity to create special enterprise versions of mobile devices that are more durable and secure.

3D Mobile Market Future Trends

AI-Driven Conversion of 2D Content into Spatial Mobile Media

One of the most important future trends in the 3d mobile Market is the use of AI to convert ordinary photos, videos, and interface elements into depth-enhanced experiences. These 3D mobile market trends address the historic shortage of native 3D content, which previously weakened consumer interest. AI depth estimation, scene segmentation, and generative rendering can make spatial media more accessible without requiring specialized capture equipment for every use case.

Future demand will be determined by how effortlessly these conversions are performed on smartphones, tablets, XR devices, and cloud computing platforms. The more effortlessly consumers can view their memories, products, training content, and entertainment in three dimensions, the more adoption rates are expected to grow. Those firms that have strong AI software and powerful processor and screen ecosystems are bound to gain an edge over their competitors.

Convergence of 3D Mobile Devices with XR and Wearable Ecosystems

The boundaries between smartphones, XR headsets, smart glasses, and mobile 3D displays are becoming less distinct. Users increasingly expect content captured on one device to be viewed or manipulated across another. This convergence encourages device manufacturers to design mobile products that support spatial capture, depth-aware interfaces, and compatibility with immersive viewing environments.

Future growth will come through ecosystems, not just isolated 3D phones. Companies like Apple, Inc., Samsung, HTC, Sony, and Qualcomm Technologies, Inc. will play a part in this because their software and hardware choices determine the experience across devices. Users can switch between handheld and wearable screens, and as a result, mobile devices can become hubs of the spatial computing ecosystem.

3D Mobile Market Opportunities

Specialized 3D Mobile Solutions for Healthcare and Training

Healthcare and training applications offer attractive opportunities because 3D visualization can deliver measurable value beyond consumer entertainment. Medical equipment users may benefit from mobile access to anatomical models, diagnostic images, procedure guidance, and remote consultation tools. The 3D mobile Market forecast highlights how training organizations can use mobile interfaces to simulate equipment operation, safety procedures, and environments.

The investment needs to be made in secure software, clinical visualizations, hardware compatibility, and collaborations with healthcare institutions or educational platforms. Companies that develop products for the regulated environment can earn higher margins than those for mass-market products. It is particularly lucrative for firms that can integrate depth capture, rendering, privacy, and mobility into their solutions.

Industrial Automation and Field-Service Visualization Platforms

The field of industrial automation is a real opportunity for the 3D mobile market because plants, utilities, and other infrastructural organizations require enhanced mobile visualization at the site level. Applications such as visual inspection of equipment, comparison of digital models with real equipment, remote support, and documentation of maintenance results will benefit from depth technology.

Investment should focus on toughened devices, software development, connectivity, and integration with enterprise systems. Organizations that offer 3D mobile services alongside analysis, asset management, and technical support could go beyond merely selling hardware. Industrial organizations would value reliability, proven time-saving, and compatibility with existing automation technologies.

Recent Developments

- June 2026: OPPO — introduced the Reno16 Series with HoloVerse 3D Technology, a 3D Pop Planet Design, and AI-powered creative features. The company stated that millions of microlenses create a floating depth effect, while the lineup also includes AI imaging tools and compact AMOLED displays for mobile content creation.

- April 2026: Samsung Electronics Co., Ltd. — with POSTECH- published research in Nature on a switchable 2D–3D display using a metasurface lenticular lens. The work demonstrated voltage-controlled switching between high-resolution 2D and glasses-free 3D modes, with an ultra-thin optical layer and wide viewing-angle potential for smartphones and tablets.

- February 2024: ZTE Corporation — launched the nubia Pad 3D II at MWC 2024, positioning it as a 5G and AI eyewear-free 3D tablet. The device included real-time 2D-to-3D conversion, AI eye tracking, improved 3D brightness and resolution, and an 86-degree viewing angle for entertainment, education, healthcare, and industrial uses.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends