Digital Language Learning Market Key Players and Forecast by 2027

Historic Data: 2018-2019 | Base Year: 2020 | Forecast Period: 2021-2027Digital Language Learning Market Forecast to 2027 - COVID-19 Impact and Global Analysis By Language Type (English, German, Spanish, Mandarin, and Others); Deployment Type (On-Premise and Cloud); Business Type (Business-to-Business and Business-to-Customer); End-User (Academic and Non-Academic); and Geography

- Report Date : Dec 2020

- Report Code : TIPRE00006243

- Category : Technology, Media and Telecommunications

- Status : Published

- Available Report Formats :

- No. of Pages : 193

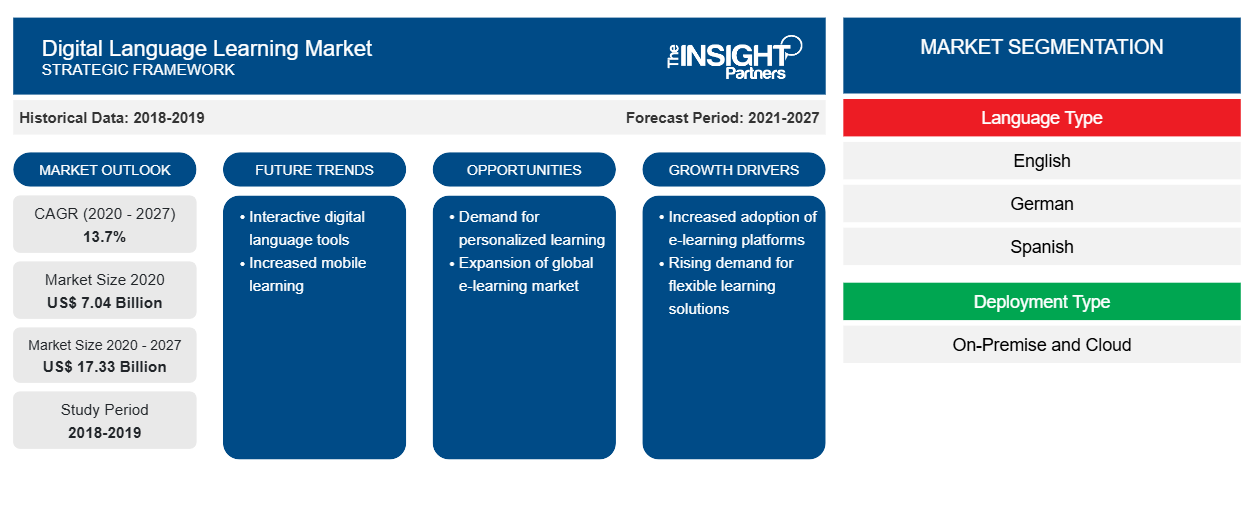

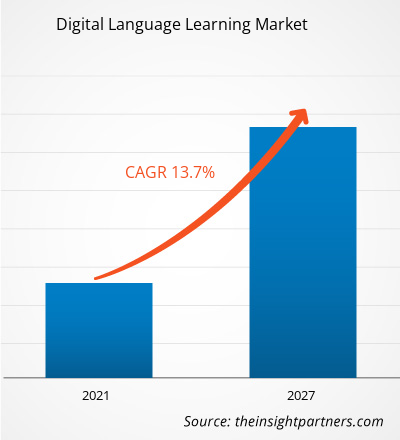

The digital language learning market expected to grow from US$ 7038.2 million in 2020 to US$ 17333.4 million by 2027; it is estimated to grow at a CAGR of 13.7% from 2020 to 2027.

Initiatives from Various Governments to Implement English Language Learning Programs is attributing to the growth of the market. The global education sector is transforming exponentially on the back of various initiatives undertaken by governments and private organizations to deliver digitally enhanced performance. Governments of various countries such as China, Australia, Brazil, and the UAE have initiated the digital education schemes in the past years, which has helped these countries to boost their English education systems. For instance, the Digital Education Revolution (DER) by the Australian government, which was initiated a decade ago, has enabled several schools and universities to leverage digital education. Similarly, the Chinese government has also initiated several policies to drive the digital education with a major focus on English language learning, which has propelled the rise in the number of companies offering the digital learning solutions to Chinese students. 51Talk is one of the most prominent digital English language learning institutions in China; 17Zuoye is another digital platform for Chinese students, teachers, and parents, which provides online assignments in the form of exercises and homework, allowing end users to enhance their capabilities. Currently, India is pacing up to create a substantial market space for digital education. Various initiative has been undertaken by the Indian government to popularize the digitalization technologies in the educational sector. SWAYAM is the most prominent digital learning platform and initiative undertaken by the Indian government, which helps the students to opt for online courses, covering all subjects of higher education. International universities are also allowed to offer their respective courses and examination through SWAYAM platform, which is facilitating the students to learn and opt for examinations from international universities. This factor enhances the English learning, speaking, and writing skills of students. National digital library is another initiative implemented by the Indian government with a vision of offering virtual source of learning resources, from a single-window facility. This initiative is gaining prominence gradually and is expected to boost the digital English language learning market in India to grow in the coming years, thereby contributing to the growth of the global digital language learning market

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Digital Language Learning Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Digital Language Learning Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Impact of COVID-19 Pandemic on Digital Language Learning Market

The recent outbreak of the pandemic has brought considerable positive disruption in the existing education sector globally during the past few months. Furthermore, the disruption in the conventional educational institutions and class-room based learning techniques witnessed a surge in adoption of robust and efficient online and digital learning solutions is projected to continue powering the market’s growth beyond the pandemic in the coming years. For instance, UNESCO along with several leading representatives from technology enterprise and ITU (International Telecommunication Union) collaborated to emphasis the economic significance of adoption of digital technologies in learning to enable swift learning capabilities among the larger audience without considerable investment into physical infrastructures among the emerging economies.

Whereas, in a separate survey conducted by the Cambridge University over 1,200 respondents identified an increased propensity to continue with digital learning technologies among their 60% of the survey candidates in the coming years. Hence, the recent outbreak has facilitated a surge in the adoption of the digital learning technologies and subsequently positively impacted the market growth in the past few months

Market Insights–Digital Language Learning Market

Leveraging Advanced and Simplified Technologies to Attract Students Toward Digital Education

In developed countries, such as the US and the UK, the digital education system has gained immense popularity as the students in schools, universities, and other institutions are completely aware of the technologies. However, in APAC and SAM countries, students lack the awareness of technology-driven learning. Several schools, universities, and coaching institutions are implementing digital technologies in their classes. As the digital educational platform developers are constantly upgrading their technologies to offer robust solutions, the adopters in APAC are continuously upgrading their technology infrastructure. The innovative cloud-based educational apps, websites, and other services are expected to create a significant market for digital education, including digital language learning solutions.

Language Type-Based Insights

Based on language type, the digital language learning market is segmented into English, Mandarin, Spanish, German, and others. The english segment held the largest market share in 2019.

Digital Language Learning Market Regional Insights

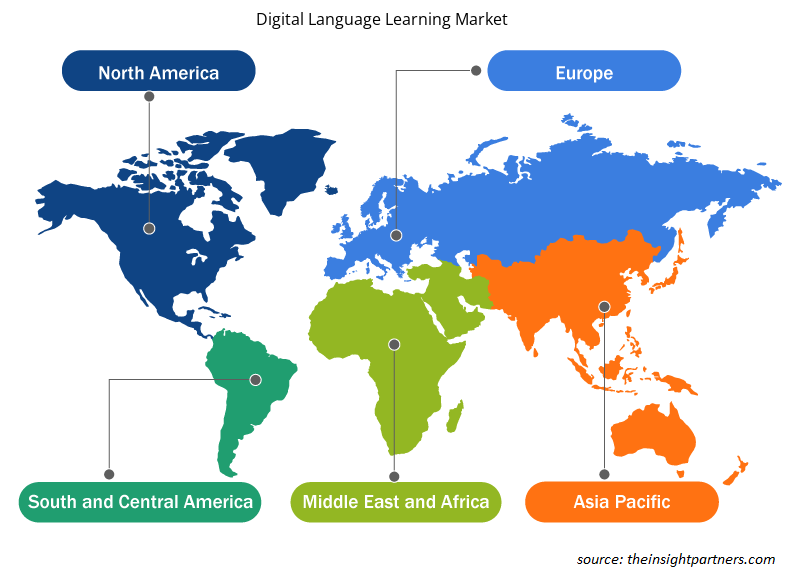

The regional trends and factors influencing the Digital Language Learning Market throughout the forecast period have been thoroughly explained by the analysts at The Insight Partners. This section also discusses Digital Language Learning Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for Digital Language Learning Market

Digital Language Learning Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2020 | US$ 7.04 Billion |

| Market Size by 2027 | US$ 17.33 Billion |

| Global CAGR (2020 - 2027) | 13.7% |

| Historical Data | 2018-2019 |

| Forecast period | 2021-2027 |

| Segments Covered |

By Language Type

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

Digital Language Learning Market Players Density: Understanding Its Impact on Business Dynamics

The Digital Language Learning Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the Digital Language Learning Market are:

- Babbel

- Busuu Ltd

- Fluenz

- Lingoda GmbH

- Living Language (Penguin Random House, LLC)

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the Digital Language Learning Market top key players overview

Players operating in the digital language learning market are mainly focused on the development of advanced and efficient products.

- In 2019, Fluenz announced the expansion of its Spanish Luxury Immersion Program to Barcelona, Spain in Spring of 2020.The users would be able to join the program for six days for language learning.

- In 2018, Preply, Inc. announced its plans to open new office in Barcelona in early 2019. The expansion was a result of $4 Mn funding in July. The company further plans to expand its presence in German, British, American and Latin American markets.

The digital language learning market has been segmented as follows:

Global Digital Language Learning Market - By Language Type

- English

- German

- Spanish

- Mandarin

- Others

Global Digital Language Learning Market - By Deployment Type

- On-Premises

- Cloud

Global Digital Language Learning Market - By Business Type

- Business-to-Business

- Business-to-Customer

Global Digital Language Learning Market - By End-User

- Academic

- Non-Academic

Global Digital Language Learning Market – by Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Russia

- U.K

- Rest of Europe

- Asia Pacific (APAC)

- Japan

- China

- Australia

- India

- South Korea

- Rest of APAC

- Middle East and Africa (MEA)

- Saudi Arabia

- UAE

- South Africa

- Rest of MEA

- South America (SAM)

- Brazil

- Argentina

- Rest of SAM

Digital Language Learning Market – Company Profiles

- Babbel

- Busuu, Ltd.

- Fluenz

- Lingoda GmbH

- Living Language (Penguin Random House, LLC)

- Pearson PLC

- Preply, Inc.

- Rosetta Stone, Inc.

- Verbling, Inc.

- Yabla, Inc.

Frequently Asked Questions

Which region led digital language learning market?

APAC region led digital language learning market. APAC comprises countries with developed educational sectors, including China, Australia, India, Singapore, and South Korea. These countries are leveraging every possible method and model to enhance English proficiency with an aim to increase the number of English speaking individuals. According to EF Education First English Proficiency Test, Asian countries hold the second position, after Europe, among the non-native English speaking countries. Over the years, countries in APAC have been investing significantly in promoting English language learning and also has lucrative opportunities for English learning.

Which factor is driving the digital language learning market?

Increasing number of Asian students migrating to western countries is the major factor driving the growth of the market. Digital English language learning is witnessing the major demand from the both academic and non-academic sectors in Asian countries. The currently increasing trend among Asian students to enroll themselves in universities in the western countries for higher education is creating a significant demand for language learning courses. Majority of the candidates from Asian countries, especially from India and China, enroll themselves for Test of English as a Foreign Language (TOEFL), International English Language Testing System (IELTS), Graduate Record Examination (GRE), Test of English for International Communication (TOEIC), and other language-based courses and certifications. TOEFL and IELTS are the tests conducted to assess a non-native candidate’s English fluency level, including proper English speaking and writing skills. This factor compels the enrolling candidates to opt for English Language Training (ELT) institutes. The burgeoning demand for these competitive exams has led to the establishment of various ELT institutions across these countries, which in turn has opened up avenues for different English learning methods.

Which Language type led the digital language learning market?

English is the most preferred language in terms of business perspectives across the globe, and close to 30 nations worldwide have it as their primary language of communication. More than 20% of the global population speaks this language. As a result, various sectors around the world have given importance to English as a common language for communications. Further, on the back of the trending globalization, many businesses have been set in different parts of the world where English is a mandatory language for communication. Digital English language learning encompasses digital content and products that facilitate easy learning through the use of various ICT-enabled interactive tools. These tools include mobile applications, e-books, audio clips, videos, games, digital software, and online tutoring, among others. A few of the key companies operating in the digital English language learning market are Cambridge University Press, Cengage/ National Geographic Learning, and EF Education First

Market Research & Consulting

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

- Parking Meter Apps Market

- eSIM Market

- Advanced Distributed Management System Market

- Online Exam Proctoring Market

- Electronic Data Interchange Market

- Barcode Software Market

- Maritime Analytics Market

- Cloud Manufacturing Execution System (MES) Market

- Robotic Process Automation Market

- Digital Signature Market

Testimonials

I wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.The Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.We worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, Market ResearchThe research report delivered details on drivers and restraints, trends, and opportunities, along with strategic activities in the market. Previously, we were struggling to get reliable information.

Manager Medical Devices ManufacturingReason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Yes! We provide a free sample of the report, which includes Report Scope (Table of Contents), report structure, and selected insights to help you assess the value of the full report. Please click on the "Download Sample" button or contact us to receive your copy.

Absolutely — analyst assistance is part of the package. You can connect with our analyst post-purchase to clarify report insights, methodology or discuss how the findings apply to your business needs.

Once your order is successfully placed, you will receive a confirmation email along with your invoice.

• For published reports: You’ll receive access to the report within 4–6 working hours via a secured email sent to your email.

• For upcoming reports: Your order will be recorded as a pre-booking. Our team will share the estimated release date and keep you informed of any updates. As soon as the report is published, it will be delivered to your registered email.

We offer customization options to align the report with your specific objectives. Whether you need deeper insights into a particular region, industry segment, competitor analysis, or data cut, our research team can tailor the report accordingly. Please share your requirements with us, and we’ll be happy to provide a customized proposal or scope.

The report is available in either PDF format or as an Excel dataset, depending on the license you choose.

The PDF version provides the full analysis and visuals in a ready-to-read format. The Excel dataset includes all underlying data tables for easy manipulation and further analysis.

Please review the license options at checkout or contact us to confirm which formats are included with your purchase.

Our payment process is fully secure and PCI-DSS compliant.

We use trusted and encrypted payment gateways to ensure that all transactions are protected with industry-standard SSL encryption. Your payment details are never stored on our servers and are handled securely by certified third-party processors.

You can make your purchase with confidence, knowing your personal and financial information is safe with us.

Yes, we do offer special pricing for bulk purchases.

If you're interested in purchasing multiple reports, we’re happy to provide a customized bundle offer or volume-based discount tailored to your needs. Please contact our sales team with the list of reports you’re considering, and we’ll share a personalized quote.

Yes, absolutely.

Our team is available to help you make an informed decision. Whether you have questions about the report’s scope, methodology, customization options, or which license suits you best, we’re here to assist. Please reach out to us at sales@theinsightpartners.com, and one of our representatives will get in touch promptly.

Yes, a billing invoice will be automatically generated and sent to your registered email upon successful completion of your purchase.

If you need the invoice in a specific format or require additional details (such as company name, GST, or VAT information), feel free to contact us, and we’ll be happy to assist.

Yes, certainly.

If you encounter any difficulties accessing or receiving your report, our support team is ready to assist you. Simply reach out to us via email or live chat with your order information, and we’ll ensure the issue is resolved quickly so you can access your report without interruption.

The List of Companies - Digital Language Learning Market

- Babbel

- Busuu Ltd

- Fluenz

- Lingoda GmbH

- Living Language (Penguin Random House, LLC)

- Pearson PLC

- Preply, Inc

- Rosetta Stone, Inc.

- Verbling, Inc

- Vabla, Inc

Get Free Sample For

Get Free Sample For