DNA Next Generation Sequencing Market Overview and Growth by 2025

DNA Next Generation Sequencing Market to 2025 - Industry Analysis and Forecasts By Product (Platforms, Services and Consumables); Application (Diagnostics, Drug Discovery, Precision Medicine, & Other Applications); & End User (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, Hospitals Clinics, & Other End Users) and Geography

- Status : Published

- Report Code : TIPRE00002934

- Category : Life Sciences

- No. of Pages : 246

- Available Report Formats :

- Last update date : June 13, 2024

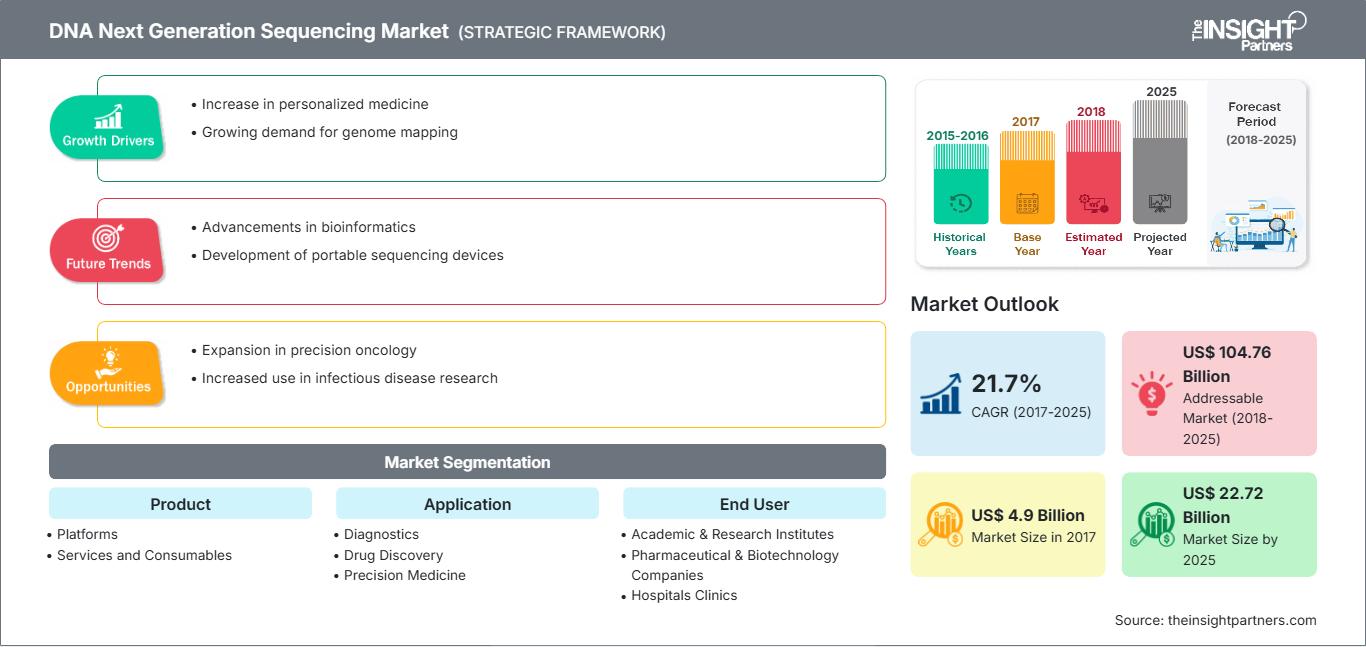

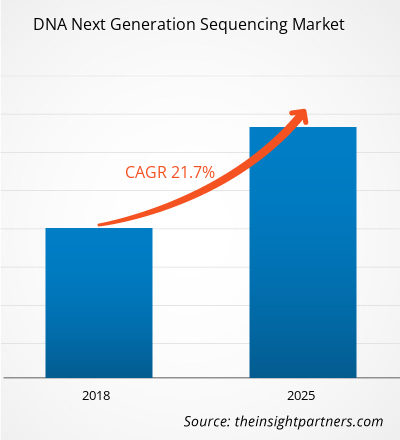

2017 Market Size

US$ 4.9 Bn

Base year value

2025 Forecast

US$ 22.72 Bn

Projected by 2025

CAGR 2018-2025

21.7 %

Growth rate

Addressable Market

US$ 104.76 Bn

(2018-2025)

[Research Report] The DNA next generation sequencing market size is estimated to reach US$ 22,716.9 million by 2025 from US$ 4,898.5 million in 2017; it is expected to grow at a CAGR of 21.7% during 2018-2025.

Next generation sequencing is also known as high-throughput sequencing. NGS enables rapid sequencing of the base pairs in DNA samples. NGS is driving the drug discovery application and enabling the future of personalized medicine, genetic diseases, and clinical diagnostics. Moreover, next-generation sequencing (NGS) is a massively parallel sequencing technology that can establish the order of nucleotides in a whole genome with scalability, ultra-high throughput, and fast speed. Since it includes preparing the sample for the subsequent sequencing reaction, DNA pre-sequencing is one of the most important processes in the total sequencing protocol. In the global healthcare sector, NGS is steadily being integrated into clinical laboratory analysis, testing, and disease diagnoses. In pharmacogenomics, NGS has been widely employed to speed up the drug discovery process.

The DNA next generation sequencing market growth is attributed owing to increasing number of cancer cases across the globe, rising research studies, increasing collaborations between research institutes and market players along with rising applications of DNA next generation sequencing and technological advancements in sequencing technologies. However, the dearth of skilled professionals is expected to critically impact the overall DNA next generation sequencing market growth.

Market Assessment and Insights

- Global market for DNA Next Generation Sequencing was valued at US$ 4.90 Billion in 2017

- Annual market size is expected to reach US$ 22.72 Billion by 2025

- Total addressable market (TAM) during 2018-2025 is projected to reach approximately US$ 104.76 Billion

- Market is anticipated to register a CAGR of 21.7% during the forecast period

- The United States represents a key market, supported by Increase in personalized medicine, Growing demand for genome mapping, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion in precision oncology, Increased use in infectious disease research are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Illumina, Inc., Thermo Fisher, Qiagen N.V., Beijing Genomics Institute, PerkinElmer, Inc., Hoffman-La Roche Ltd., Agilent Technologies, Eurofins Scientific, Oxford Nanopore Technologies Ltd., Macrogen Inc., while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

DNA Next Generation Sequencing Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Market Insights

Declining Price of Sequencing and Technological Advancements in Sequencing Methods Drives DNA Next Generation Sequencing Market

In the recent years, next generation sequencing prices have declined substantially. In 2000, the cost for sequencing human genome was US$ 3.7 billion and took 13 years for completion. However, the costs for the same in recent years reduced to US$ 10 million in 2006 and further declined in 2012, and the process requires fewer days. Major DNA next generation sequencing market players such as Illumina and Roche have introduced breakthrough technologies that are cost-efficient and require less time in sequencing processes.

Moreover, advancement in the field of molecular biology has equally enhanced sequencing procedures. Many industry players have come up with innovative NGS technology in the last few years. For instance, Pacific Biosciences with Sequel and Oxford Nanopore with PromethION. Additionally, three advanced NSG systems that dominate the market include Roche GS FLX (454), Illumina HiSeq 2000 (Solexa), and AB SOLiD (Agencourt).

Further modification and automation of this process continued to increase sequencing data and also resulted in managing time more efficiently, thereby allowing researchers to reach major milestones in the Human Genome Project. NGS makes sequence-based gene expression analysis a “digital” alternative to analog techniques. Advancement in genome sequencing has made sequencing easy and accurate. These technological advancements are likely to boost the DNA next generation sequencing market size in the near future.

Product-Based Insights

The global DNA next generation sequencing market, based on product, is segmented into platforms, services, and consumables. The platform segment is further sub-segmented into HiSeq Series, MiSeq Series, SOLiD, Ion Torrent, Pacbio Rs II and Sequel Systems, and others. Further, the services segment is sub-segmented into sequencing services and data management and analysis services. Moreover, the consumables segment is sub-segmented into sample consumable preparation and other NGS consumables. The consumables segment held a larger share among the product subsegments in the DNA next generation sequencing market in 2017 and is also anticipated to follow a similar trend over the forecast period. More recent NGS platforms have adopted a new sequencing method, called single-molecule sequencing (SMS), which does not require prior amplification of DNA, thus avoiding the PCR-related error reads or amplification bias toward repeat regions. During the past five years, next-generation sequencing (NGS) has transitioned from research to clinical use. At least 14 countries have created initiatives to sequence large populations, and it is projected that more than 60 million people worldwide will have their genome sequenced by 2025.

Application-Based Insights

The global DNA next generation sequencing market, based on application, is segmented into diagnostics, drug discovery, precision medicine, and other applications. The diagnostics segment held the largest share in 2017 and is expected to witness significant growth over the next five to six years. The use of next-generation sequencing (NGS) technology in diagnostic genome care needs precision and accuracy. The NGS technologies use cost-efficient sequencing to gain genomic information about the patients from the whole-genome sequencing to perform clinical actions. Next-generation sequencing is eventually substituting conventional technologies to diagnose various genetic disorders. Large sets of genes can now be addressed in a single test instead of a gene-by-gene approach.

End User-Based Insights

The global market, based on end user, is segmented into academic & research institutes, pharmaceutical & biotechnology companies, hospitals & clinics, and other end users. The academic and research institutes segment is expected to witness the highest growth over the forecast period. The sequence helps scientists in finding the kind of genetic information that is carried in a particular DNA segment. For example, scientists can use sequence information to determine which stretches of DNA contain genes and which stretches carry regulatory instructions, turning genes on or off. The automated-industrialized approach based on random or shotgun sequencing was introduced by The Institute for Genomic Research (TIGR) in Rockville, Maryland, and resulted in the publication of 337 new human genes and 48 homologous genes from other organisms

DNA Next Generation Sequencing Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2017 | US$ 4.9 Billion |

| Market Size by 2025 | US$ 22.72 Billion |

| Global CAGR (2017 - 2025) | 21.7% |

| Historical Data | 2015-2016 |

| Forecast period | 2018-2025 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

DNA Next Generation Sequencing Market Players Density: Understanding Its Impact on Business Dynamics

The DNA Next Generation Sequencing Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Product launches and approvals are commonly adopted strategies by companies to expand their global footprints and product portfolios. Moreover, the market players focus on the partnership strategy to enlarge their clientele, which, in turn, permits them to maintain their brand name across the world. The market share is anticipated to flourish with the development of new innovative products by market players. Some of the market participants present in the concerned market are THERMO FISHER SCIENTIFIC INC.; Illumina, Inc; Qiagen N.V.; Beijing Genomics Institute; PerkinElmer, Inc.; F.Hoffman-La Roche Ltd.; Agilent Technologies; Eurofins Scientific; Oxford Nanopore Technologies Ltd; and Macrogen Inc.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends