Interventional Radiology Equipment Market Size, Share & Demand by 2034

Coverage: By Product (MRI Systems, Ultrasound Imaging Systems, CT Scanners, Angiography Systems, Fluoroscopy Systems, Biopsy Devices, Other Products); Application (Cardiology, Urology and Nephrology, Oncology, Gastroenterology, Other Applications), and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00021583

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : May 26, 2026

2025 Market Size

US$ 30.37 Bn

Base year value

2034 Forecast

US$ 47.99 Bn

Projected by 2034

CAGR 2026-2034

5.89 %

Growth rate

Addressable Market

US$ 367.87 Bn

(2026-2034)

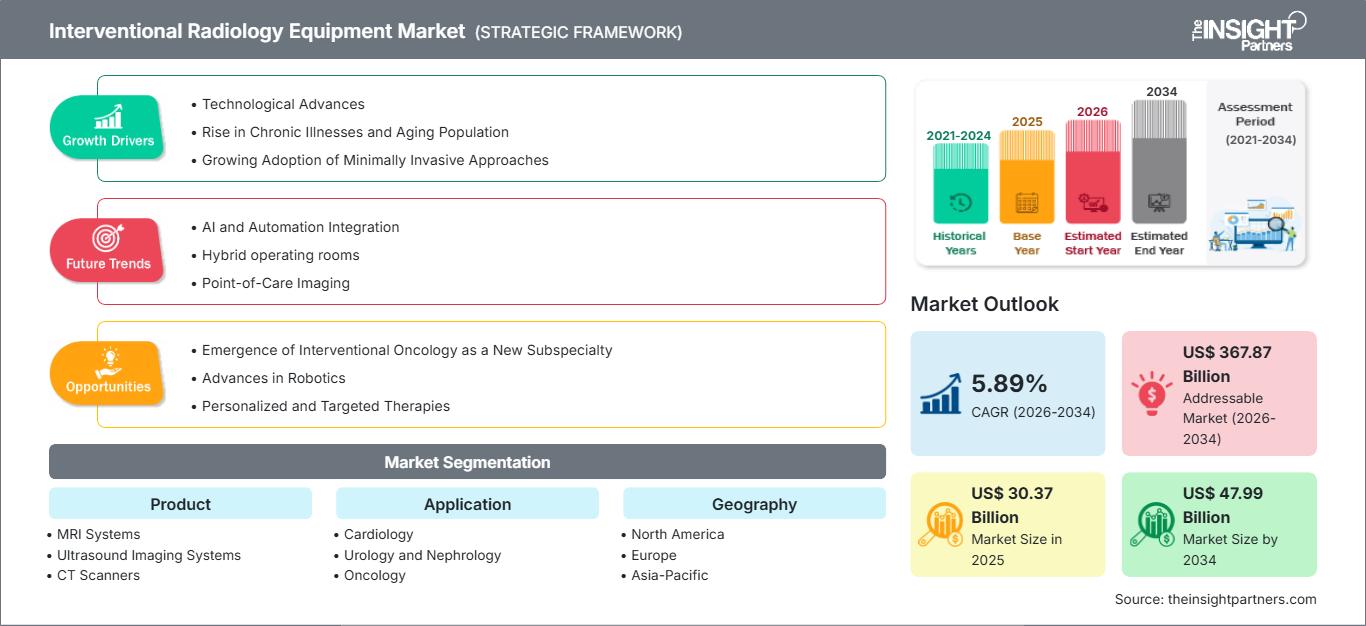

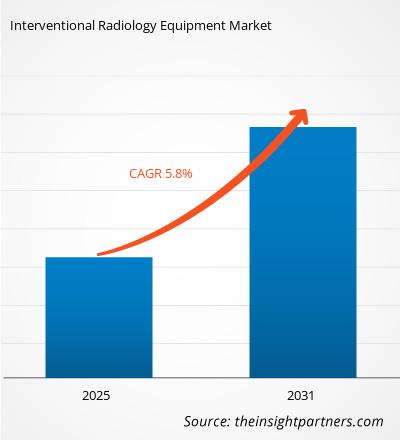

The Interventional Radiology Equipment Market size is expected to reach US$ 47.99 Billion by 2034 from US$ 30.37 Billion in 2025. The market is estimated to record a CAGR of 5.89% from 2026 to 2034.

The report is segmented by Product (MRI Systems, Ultrasound Imaging Systems, CT Scanners, Angiography Systems, Fluoroscopy Systems, Biopsy Devices, Other Products). The report further presents analysis based on the Application (Cardiology, Urology and Nephrology, Oncology, Gastroenterology, Other Applications). The global analysis is further broken-down at regional level and major countries. The Report Offers the Value in USD for the above analysis and segments.

Purpose of the Report

The report Interventional Radiology Equipment Market by The Insight Partners aims to describe the present landscape and future growth, top driving factors, challenges, and opportunities. This will provide insights to various business stakeholders, such as:

- Technology Providers/Manufacturers: To understand the evolving market dynamics and know the potential growth opportunities, enabling them to make informed strategic decisions.

- Investors: To conduct a comprehensive trend analysis regarding the market growth rate, market financial projections, and opportunities that exist across the value chain.

- Regulatory bodies: To regulate policies and police activities in the market with the aim of minimizing abuse, preserving investor trust and confidence, and upholding the integrity and stability of the market.

Interventional Radiology Equipment Market Segmentation Product

- MRI Systems

- Ultrasound Imaging Systems

- CT Scanners

- Angiography Systems

- Fluoroscopy Systems

- Biopsy Devices

- Other Products

Application

- Cardiology

- Urology and Nephrology

- Oncology

- Gastroenterology

- Other Applications

Market Research Highlights

- Global market for Interventional Radiology Equipment was valued at US$ 30.37 Billion in 2025

- Annual market size is expected to reach US$ 47.99 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 367.87 Billion

- Market is anticipated to register a CAGR of 5.89% during the forecast period

- The United States represents a key market, supported by Technological Advances, Rise in Chronic Illnesses and Aging Population, Growing Adoption of Minimally Invasive Approaches, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Emergence of Interventional Oncology as a New Subspecialty, Advances in Robotics, Personalized and Targeted Therapies are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Carestream Health, Esaote SPA, GE Healthcare, Hitachi Medical Corporation, Hologic Inc., Koninklijke Philips NV, Shimadzu Corporation, Siemens Healthineers AG, Canon Medical Systems Corporation, Samsung Medison (Samsung Electronics Co. Ltd), while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Interventional Radiology Equipment Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Interventional Radiology Equipment Market Growth Drivers

- Technological Advances: The interventional radiology equipment and technologies are two of the factors that are continuously improving. Furthermore, high-tech 3D ultrasound devices, MRI and CT scans have high resolution imaging technology which has improved the outcomes of most procedures done under IR. Other interventions such as robotic therapy and intra operative imaging have also increased the level of intervention accuracy thus reducing the rate of complications and improving the recovery period of the patients. Furthermore, the introduction of AI techniques within imaging devices and systems has fully begun assisting in procedure applications by enabling fast and accurate diagnosis with the use of treatment planning minimizing errors and also pinpointing the more accurate treatment options using predictive analytics.

- Rise in Chronic Illnesses and Aging Population: On a global scale, the rise in chronic disorders, inclusive of but not limited to cardiovascular diseases, cancer and diabetes, creates a higher demand for carrying out interventional radiology procedures. Most of these conditions however require diagnosis and treatment that allows for very low invasion which interventional radiology has been proven to be. Another factor contributing to the demand is the aging of the global population particularly in developed nations where there is also an increased incidence of geriatric-related diseases especially those that affect the blood vessels and the organs.

- Growing Adoption of Minimally Invasive Approaches: There is a growing concern among patients, as well as their healthcare givers, towards the use of invasive surgical approaches mainly because of the advantages presented by minimization of such procedures. These benefit include shorter recovery times, less pain, significantly reduced infection risks, and scars are smaller. Consequently, interventional radiology has had a significant growth over the traditional surgical methods mainly in fields such as oncology, neurology, and cardiology. The key factor in the ever-growing adoption of IR technologies is the ability to perform complex procedures with minimal invasion into the patient's body.

Interventional Radiology Equipment Market Future Trends

- AI and Automation Integration: Highly prevalent in the interventional radiology market is AI and ML integration into imaging and procedural guidance. With regards to image processing, these technologies allow a much faster and accurate approach to better assist in real-time decision-making during procedures. In areas such as image segmentation, abnormality detection, and even suggesting which interventional procedure should be taken next, AI tools can support in achieving improved results with streamlined workflows.

- Hybrid operating rooms: Hybrid ORs represent a growing trend; advanced imaging technology has been used to perform traditional and minimally invasive procedures by surgeons and interventional radiologists. Hybrid operating rooms provide such an advantage because they integrate the facilities of IR with conventional surgery, which can handle complex cases with flexibility. Hybrid ORs are very beneficial in neurosurgery, vascular interventions, and oncological procedures.

- Point-of-Care Imaging: The need for point-of-care imaging machines, including portable ultrasound and fluoroscopy machines, is on the rise because these devices provide instant imaging results-such as in cases of emergencies or outpatient procedures. These machines, however, are applied in different scenarios such as trauma care, outpatient diagnostic procedure, and are applied in remote places where large imaging machines may not be physically available. Such a trend is of high importance in developing countries and also in rural healthcare facilities, where access to high-end IR equipment is limited.

Interventional Radiology Equipment Market Opportunities

- Emergence of Interventional Oncology as a New Subspecialty: Interventional oncology is going through an enthusiastic growth period as a new substream of IR where opportunities exist for both the treatment providers as well as the equipment manufacturers. RFA, MWA, TACE and other interventions find their applications in the medical sector aimed at effective tumor ablation especially in liver cancer. As global cancer incidence rises, there is much market potential for IR equipment used in interventional oncology.

- Advances in Robotics: Robotic technologies are revolutionizing interventional radiology by enabling very precise and minimally invasive procedures. Complex procedures such as placement of catheter, insertion of stent, and biopsy are increasingly using robotic assistance; the evolution of these new technologies will reduce procedure time, increase accuracy, and lower complications and unlock significant growth opportunities for robotic: assisted interventional radiology.

- Personalized and Targeted Therapies: As the concept of personalized medicine evolves, so the demand for interventional radiology's role in treating individualized conditions is increasing. In that regard, targeted therapies like gene therapy that require precise delivery methods open new space for interventional radiology techniques, involving imaging: guided tools for administering targeted treatments. The IR market will thus face a growing demand for equipment that can facilitate such advanced interventions in oncology and neurology.

Interventional Radiology Equipment Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 30.37 Billion |

| Market Size by 2034 | US$ 47.99 Billion |

| Global CAGR (2026 - 2034) | 5.89% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Interventional Radiology Equipment Market Players Density: Understanding Its Impact on Business Dynamics

The Interventional Radiology Equipment Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Key Selling Points

- Comprehensive Coverage: The report comprehensively covers the analysis of products, services, types, and end users of the Interventional Radiology Equipment Market, providing a holistic landscape.

- Expert Analysis: The report is compiled based on the in-depth understanding of industry experts and analysts.

- Up-to-date Information: The report assures business relevance due to its coverage of recent information and data trends.

- Customization Options: This report can be customized to cater to specific client requirements and suit the business strategies aptly.

The research report on the Interventional Radiology Equipment Market can, therefore, help spearhead the trail of decoding and understanding the industry scenario and growth prospects. Although there can be a few valid concerns, the overall benefits of this report tend to outweigh the disadvantages.

Frequently Asked Questions

1. Rise in Chronic Illnesses and Aging Population

2. Growing Adoption of Minimally Invasive Approaches

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends