In-vitro Diagnostics Market Share, Growth & Forecast by 2034

Coverage: By Product & Service (Reagents & Kits, Instruments, and Software & Services), Technology (Immunoassay/ Immunochemistry, Clinical Chemistry, Molecular Diagnostics, Microbiology, Blood Glucose Self-Monitoring, Coagulation and Hemostasis, Hematology, Urinalysis, and Others), Application (Infectious Diseases, Diabetes, Oncology, Cardiology, Autoimmune Diseases, Nephrology, and Others), End User (Hospitals, Laboratories, Home Care, and Others), and Geography (North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America)

- Status : Published

- Report Code : TIPBT00002657

- Category : Life Sciences

- No. of Pages : 753

- Available Report Formats :

- Last update date : April 08, 2026

2025 Market Size

US$ 112.04 Bn

Base year value

2034 Forecast

US$ 218.73 Bn

Projected by 2034

CAGR 2026-2034

7.8 %

Growth rate

Addressable Market

US$ 1,495.70 Bn

(2026-2034)

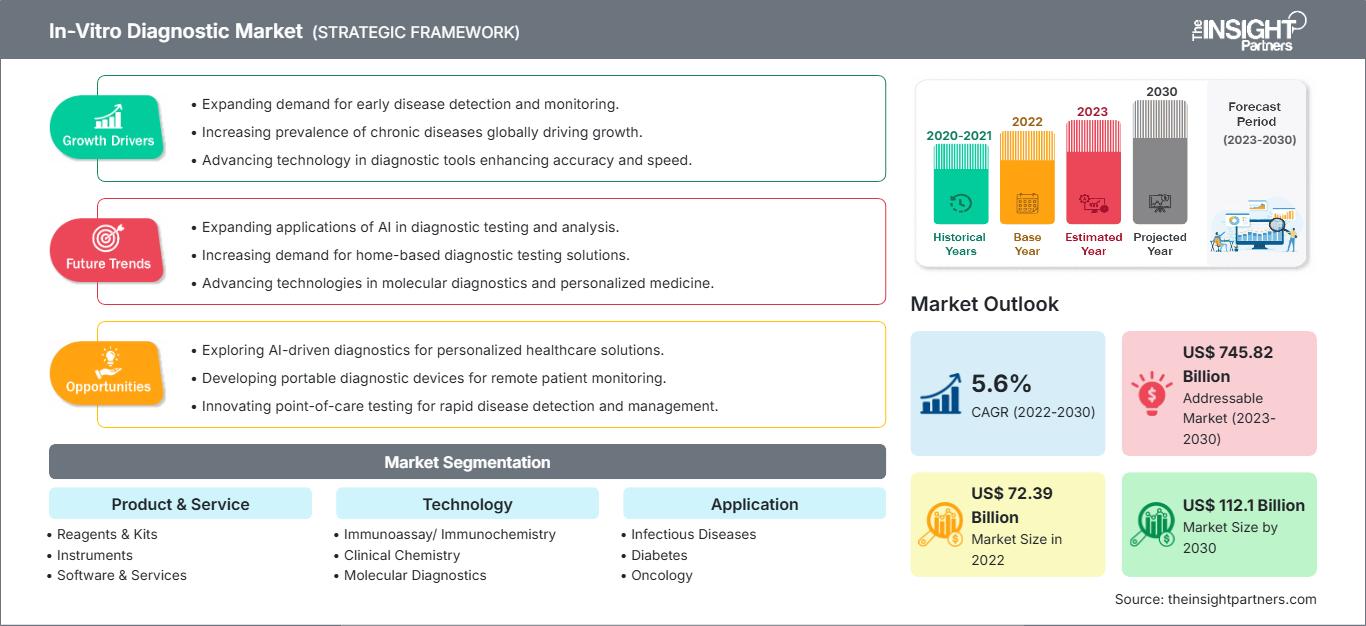

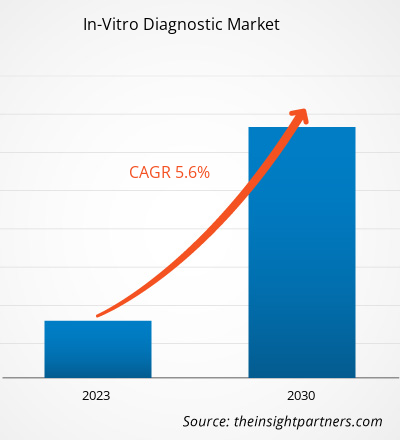

The In-vitro Diagnostics market size is projected to reach US$ 218.73 Billion by 2034 from US$ 112.04 Billion in 2025. The market is expected to register a CAGR of 7.8% during 2026–2034.

In-Vitro Diagnostics Market Analysis

More chronic diseases are being diagnosed, people are becoming more aware of healthcare, and there is a need to identify diseases at their initial stages. Molecular diagnostics and point-of-care testing, and automated systems show improved results through their combination with digital health technologies and artificial intelligence systems. The main product categories include reagents and kits, and instruments. North America leads in market share, but Asia Pacific shows the highest growth potential as its healthcare infrastructure continues to develop. The main obstacles that organizations face include regulatory challenges and high costs, and the need for data standardization.

In-Vitro Diagnostics Market Overview

Medical devices and tests analyze samples such as blood, urine, or tissues outside the human body to detect diseases, conditions, or infections. IVDs provide essential support for early diagnosis and personalized medicine, and treatment monitoring. The main parts of the system include clinical chemistry and molecular diagnostics and immunoassays, and point-of-care testing. The introduction of rapid diagnostic tests and next-generation sequencing, and AI-integrated diagnostic platforms has created new testing capabilities that achieve better testing results. The marketplace operates under three main factors, which include regulatory standards and the rising demand for home testing, and the increasing investments in biotechnology. The IVD market is moving toward diagnostic solutions that provide better accessibility and faster results, and more accurate testing because these solutions create essential testing methods for contemporary medical practice.

Market Assessment and Insights

- North America dominated the market with 42.1% share in 2025.

- Asia Pacific is poised to grow at a CAGR of 8.3% over the forecast period.

- United States market is projected to grow at a CAGR of 7.6% over the forecast period.

- By Product, the Reagents and Kits segment accounted for the largest market share of 69.2% in 2025.

- By Reagents And Kits, the Molecular Diagnostics segment is anticipated to witness the fastest growth, registering a CAGR of 9.3% over the forecast period

- By Instruments, the Immunoassay Instruments segment accounted for the largest market share of 24% in 2025.

- By Clinical Chemistry Analyzers, the Automated clinical chemistry analyzers segment is anticipated to witness the fastest growth, registering a CAGR of 8.5% over the forecast period

- By Immunoassay Instruments, the ELISA Systems segment accounted for the largest market share of 56.1% in 2025.

- By Urinalysis Instruments, the Fully Automated segment is anticipated to witness the fastest growth, registering a CAGR of 6.1% over the forecast period

- By Technology, the Immunoassay or Immunochemistry segment accounted for the largest market share of 27.2% in 2025.

- By Immunoassay Or Immunochemistry, the Chemiluminescent Immunoassay (CLIA or ECLIA or Flash CLIA or Glow CLIA) segment is anticipated to witness the fastest growth, registering a CAGR of 9.3% over the forecast period

- By Immunochromatography, the HIV and HIV 4 Gen segment accounted for the largest market share of 26% in 2025.

- By Cellular Analysis, the Digital cell morphology analysis segment is anticipated to witness the fastest growth, registering a CAGR of 8.5% over the forecast period

- By Sensor Technology, the Biochemistry segment accounted for the largest market share of 69.1% in 2025.

- By Separation Technology, the 10 segment is anticipated to witness the fastest growth, registering a CAGR of 5.7% over the forecast period

- By Molecular Diagnosis, the Digital PCR (dPCR) segment accounted for the largest market share of 36.8% in 2025.

- By Molecular Genomics, the Next-Generation Sequencing (NGS) segment is anticipated to witness the fastest growth, registering a CAGR of 8% over the forecast period

- By Application, the Infectious Diseases segment accounted for the largest market share of 48% in 2025.

- By Usability, the Disposable Devices segment is anticipated to witness the fastest growth, registering a CAGR of 8.4% over the forecast period

- By Site Of Testing, the Laboratory Tests segment accounted for the largest market share of 81.7% in 2025.

- By Specimen, the Blood Serum and Plasma segment is anticipated to witness the fastest growth, registering a CAGR of 8.3% over the forecast period

- By End User, the Hospitals segment accounted for the largest market share of 44.2% in 2025.

- The report profiles key industry players such as Siemens AG, F. Hoffmann-La Roche Ltd, Sysmex Corp, bioMerieux SA, Bio-Rad Laboratories Inc, DiaSorin SpA, Becton Dickinson and Co, Danaher Corp, Thermo Fisher Scientific Inc., Abbott, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

In-Vitro Diagnostic Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

In-Vitro Diagnostics Market Drivers and Opportunities

Market Drivers:

- Rising Prevalence of Chronic Diseases: The increasing prevalence of diabetes, cardiovascular diseases, and cancer drives demand for early detection and regular monitoring through IVD tests, boosting market growth globally.

- Technological Advancements: Innovations such as molecular diagnostics, AI-assisted analysis, and point-of-care devices improve accuracy and speed, making IVD tests more accessible, expanding their adoption in healthcare.

Market Opportunities:

- Emerging Markets Expansion: Growing healthcare infrastructure and awareness in developing countries present untapped markets for IVD products, enabling companies to reach a broader patient base and increase revenue.

- Home-Based Testing: Rising consumer interest in self-testing and remote diagnostics, accelerated by telemedicine, offers potential for at-home IVD solutions, enhancing convenience and early disease detection.

In-Vitro Diagnostics Market Report Segmentation Analysis

The In-vitro Diagnostics market is divided into different segments to give a clearer view of how it works, its growth potential, and the latest trends. Below is the standard segmentation approach used in industry reports:

By Product:

- Reagents and Kits – The essential components of IVD tests include chemicals and antibodies, and prepared testing kits, which serve to detect diseases and track patient health. The core consumables of diagnostics need these materials because they ensure testing accuracy

- Instruments and Software and Services - The system includes analytical devices and diagnostic instruments along with software that enables sample processing and result analysis. The laboratory services provide equipment maintenance and calibration services, together with training programs, to ensure their laboratories operate at optimal performance

By Usability:

- Disposable Devices – Diagnostic equipment includes test strips and cartridges, and point-of-care kits, only for one-time use. The system helps to decrease contamination risks while making testing procedures easier to use. It has become a standard method for quick tests and at-home medical testing

- Reusable Equipment – Researchers need laboratory instruments and analyzers for their work because these tools enable researchers to conduct multiple testing sessions. The equipment needs maintenance work and calibration work because it delivers cost savings over extended periods while supporting high-volume sample testing in clinical laboratories

By Technology:

- Immunoassay/Immunochemistry

- Clinical Chemistry

- Molecular Diagnostics

- Microbiology

- Blood Gas Analyzers

- Coagulation and Hemostasis

- Hematology

- Urinalysis

- Glucose Monitoring

- Others

By Application:

- Infectious Disease

- Diabetes

- Oncology

- Cardiology

- Genetic Diseases

- Nephrology

- Blood Grouping and Testing

- Allergy Diagnostics

- Gastrointestinal Diseases

- Immune System Disorders

- Others

By Site of Testing:

- Laboratory Tests

- Point of Care Tests

By Specimen:

- Blood

- Serum and Plasma

- Saliva Specimens

- Urine Specimens

- Others

By End User:

- Hospitals

- Clinical Laboratories

- Pharmaceutical and Biopharmaceutical Companies

- Home Care

- Others

By Geography:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

In-Vitro Diagnostic Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 112.04 Billion |

| Market Size by 2034 | US$ 218.73 Billion |

| Global CAGR (2026 - 2034) | 7.8% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

In-Vitro Diagnostic Market Players Density: Understanding Its Impact on Business Dynamics

The In-Vitro Diagnostic Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

In-Vitro Diagnostics Market Share Analysis by Geography

The market demonstrates distinct differences across regions, which result from variations in healthcare systems, regulatory systems, and disease distribution across areas. The US, as part of North America, controls the largest market share because its advanced healthcare system enables high usage of new diagnostic methods, while the country maintains strong research and development activities. The demand for IVD tests increases because people have widespread insurance coverage and understand the importance of early disease detection. Europe represents the second-largest share, with Germany, France, and the UK dominating the region. The market expansion results from the establishment of a laboratory network, the implementation of strict regulatory requirements, and the rising adoption of molecular testing methods.

APAC experiences its fastest growth because healthcare expenditures increase and diagnostic facilities expand, and chronic disease rates rise. Government programs that support early disease detection and local production of affordable IVD products serve as the main driving forces behind China, India, and Japan's role as vital market participants. The Middle East and Africa, together with Latin America, present smaller market shares, which still create potential growth because healthcare facilities improve, and people learn about preventive health measures.

Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a significant portion of the global market

- Key Drivers:

- Advanced healthcare infrastructure and widespread adoption of automated, high‑throughput diagnostics

- Strong research and development investment and rapid integration of molecular and point‑of‑care technologies

- Trends: Growth of AI‑enhanced diagnostics, increased home‑based testing, and precision medicine focus

2. Europe

- Market Share: Substantial market share

- Key Drivers:

- Established public healthcare systems with strong screening and preventive care programs

- Aging population increasing routine chronic disease testing demand

- Trends: Emphasis on regulatory harmonization (IVDR), digital pathology, and decentralized diagnostics

3. Asia Pacific

- Market Share: Fastest-growing region with a rising market share every year

- Key Drivers:

- Rapid healthcare spending growth, expanding lab infrastructure, and rising disease burden

- Large populations fueling demand for affordable point‑of‑care and molecular diagnostics

- Trends: Increasing local manufacturing, government screening initiatives, and broader testing access.

4. South and Central America

- Market Share: Growing market with steady progress

- Key Drivers:

- Rising healthcare investment and expansion of public healthcare access

- Increasing awareness of early disease detection and preventive care

- Trends: Centralized lab networks in urban centers and growing point‑of‑care adoption.

5. Middle East and Africa

- Market Share: Although small, but growing quickly

- Key Drivers:

- Government‑led healthcare modernization and lab infrastructure improvement

- Rising awareness and demand for infectious and chronic disease diagnostics

- Trends: Increased adoption of mobile diagnostics, partnerships with international firms, and expansion of affordable testing solutions

Opportunities and Strategic Moves

- In February 2025, Revvity, Inc. announced the launch of three Mimix reference standards for IVD use. It is designed for monitoring of next-generation sequencing (NGS) or droplet digital polymerase chain reacting (ddPCR) assays designed to detect somatic mutations in genomic DNA (gDNA) from human samples for IVD use.

- In May 2024, Polaris announced the launch of its premium line of molecular diagnostics kits, certified as In Vitro Diagnostic (IVD) reagents.

- In December 2025, KVP International announced the acquisition of SafePath-IVD, a diagnostics manufacturer and CDMO provider with FDA, ISO 13485, and USDA licenses based in Carlsbad, California. The acquisition strengthens KVP’s position as a fast-growing provider of veterinary diagnostics and expands SafePath-IVD’s ability to scale across veterinary and human health markets. The acquisition marks a significant milestone in KVP’s strategic expansion into point-of-care and rapid diagnostic solutions.

Major Companies operating in the In-Vitro Diagnostics Market are:

- Abbott

- F. Hoffmann-La Roche Ltd

- Danaher Corp

- Siemens AG

- Becton Dickinson and Co

- Thermo Fisher Scientific Inc.

- MiLab Scientific

- ANGEL BIOTECH

- Microhaem Scientifics

- Sysmex Corp

Disclaimer: The companies listed above are not ranked in any particular order.

Other companies analyzed during the course of research:

- Illumina, Inc.

- Hologic, Inc.

- Bio Rad Laboratories, Inc.

- bioMérieux

- Revvity Inc

- Becton, Dickinson and Company

- Agilent Technologies, Inc.

- Qiagen

- DiaSorin S.p.A.

- Grifols, S.A.

- Werfen

- QuidelOrtho Corporation

In-Vitro Diagnostics Market News and Recent Developments

- In January 2025, Argonaut Manufacturing Services, a contract development and manufacturing organization serving the biopharma and life sciences industries, was selected as the manufacturing partner for Akoya Biosciences Inc.’s IVD assays currently in development.

In-Vitro Diagnostics Market Report Coverage and Deliverables

The "In-vitro Diagnostics Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- In-vitro Diagnostics market size and forecast at global, regional, and country levels for all the segments covered under the scope

- In-vitro Diagnostics market trends, as well as dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- In-vitro Diagnostic markets analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the in-vitro diagnostics market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends