Medical Scheduling Software Market Overview and Growth by 2028

Medical Scheduling Software Market Forecast to 2028 - Analysis by Software (Installed Software and Web-Based Software), End User (Hospitals, Clinics, and End User)

- Status : Published

- Report Code : TIPHE100001414

- Category : Technology, Media and Telecommunications

- No. of Pages : 147

- Available Report Formats :

- Last update date : June 13, 2024

2022 Market Size

US$ 435.24 Mn

Base year value

2028 Forecast

US$ 927.09 Mn

Projected by 2028

CAGR 2023-2028

13.4 %

Growth rate

Addressable Market

US$ 4,149.47 Mn

(2023-2028)

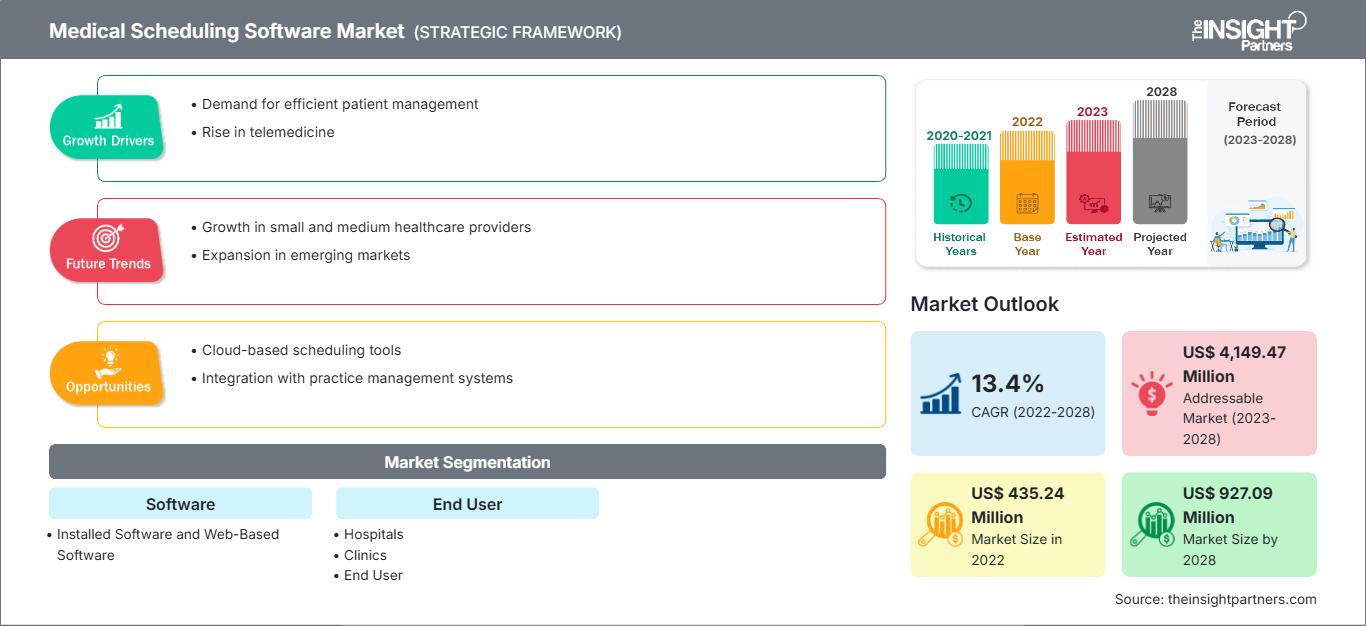

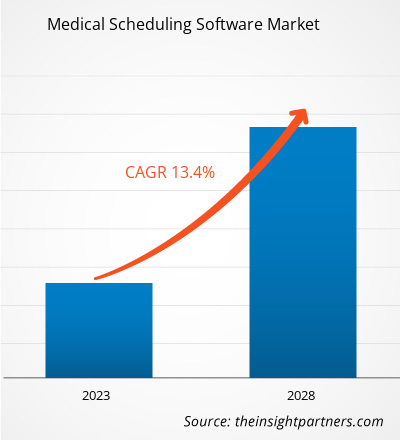

The medical scheduling software market is expected to reach US$ 927.09 million by 2028 from US$ 435.24 million in 2022; it is estimated to grow at a CAGR of 13.4% from 2022 to 2028.

Medical scheduling software allows patients to schedule their appointments through online when they are away from the hospitals or clinics. The practice employs the comprehensive system with an integrated patient portal and scheduling software. Common features of a medical scheduling software include, patient registration, appointment reminder services, customizable settings, and patient tracking. The economic and efficient handling of the software has led to increased preference of the software.

The medical scheduling software market is segmented based on software, end user, and geography. By geography, the market is broadly segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. The report offers insights and in-depth analysis of the medical scheduling software market, emphasizing on parameters such as market trends, technological advancements, and market dynamics, along with the analysis of the competitive landscape of the world's leading market players.

Market Insights

Rising adoption of patient-centric approach by healthcare providers

A patient-centric approach is an idea in healthcare systems that can establish a partnership among patients & their families and healthcare practitioners to align decisions with patients’ needs, preferences, and wants. It also includes the delivery of specific education and support patients require to make certain decisions and participate in their care.

Market Assessment and Insights

- North America dominated the market with 42.4% share in 2021.

- Asia Pacific is poised to grow at a CAGR of 14.1% over the forecast period.

- United States market is projected to grow at a CAGR of 13.9% over the forecast period.

- By Software, the Web-Based Software segment accounted for the largest market share of 67.6% in 2021.

- By End User, the Clinics segment is anticipated to witness the fastest growth, registering a CAGR of 14% over the forecast period

- The report profiles key industry players such as Q-nomy Inc, AdvancedMD Inc, TimeTrade, Yocale Network Corporation, Voicent Communications Inc., WellSky, Daw Systems, Inc., ByteBloc Software, Workpath, Delta Health Technologies, Inc., while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Medical Scheduling Software Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Increased engagement with all stakeholders (providers, patients, and others), leading to reduced overall expenses. Improved knowledge and understanding among patients of their health, well-being, and healthcare choices leading to enhanced care and reduced levels of illness. This improved knowledge can also improve care after discharge, hospital visits, reduced readmissions, and secondary consults. By engaging and collaborating with patients in decision-making, health providers can make more suitable decisions regarding a patient’s health. Increased competitive advantage as more hospitals compete for patients based on both qualities of care and cost. Better quality of life for patients leads to an increase in the satisfaction of both doctor and patient.

In recent years the patient-centric approach has been predominant in the healthcare industry. Technological innovations and software development are crucial to this healthcare industry revolution. These technological developments support medical and administrative services that dramatically enhance and ease healthcare processes, communications, and workflow. Patient-centric healthcare raises patient satisfaction levels, which creates benefits for healthcare providers and practices. Thus, the rising adoption of a patient-centric approach by healthcare providers driving the growth of the medical scheduling software market.

Increasing Knowledge about the Internet of Things

During 2011–2020, a significantly large number of devices were connected to the internet than ever before, and this trend would continue steadily in the coming decades as well. The emergence of the Internet of Things (IoT) has propelled the development of various health practices aimed at improving population health. Many services and applications of IoT in healthcare—eHealth, mobile health (mHealth), ambient assisted living, semantic devices, wearable devices and smartphones, and community-based healthcare—have been examined in several recent studies. These services have been extensively informative and can be used for a variety of purposes across single condition and cluster condition management, including allowing healthcare professionals to track and monitor patient progress remotely, improving self-management of chronic conditions, assisting in the early detection of abnormalities, and accelerating symptom identification and clinical diagnoses. Further, IoT-powered apps have the potential to make better use of healthcare resources while providing high-quality, low-cost medical treatment.

Further artificial intelligence (AI) has boosted the availability of point-of-care health information; for example, chatbots (also known as AI physicians) can provide lifestyle and medical advice. Woebot, Your. Md, Babylon, and HealthTap are among other examples of well-known AI bots that provide immediate recommendations to patients, based on details/symptoms entered by them.

Opportunities for IoT innovation in the healthcare industry are continuously emerging and evolving. Medical facilities have special challenges, and vendors of IoT are developing new approaches to address those challenges.

Increasing Acceptance of Mobile Health Technology

Advancements in mobile technology, coupled with growing health concerns, are fueling the growth of mHealth services (MHS) across the world. Mobile and wireless technologies hold the potential to change the way healthcare is delivered. Rapid advancements in mobile technologies and applications, an increase in new opportunities for integrating mobile health into existing eHealth services, and ongoing expansion of mobile cellular network coverage are among the major factors supporting the proliferation of mHealth solutions. As per the International Telecommunication Union (ITU) estimates, there are more than 5 billion wireless subscribers, with over 70% of them living in low- and middle-income countries in 2020. According to the GSM Association, commercial wireless transmissions have reached ~85% of the world's population, i.e., far beyond the reach of the electric grid. The proliferation of wireless communication would not only help enhance the quality of care and the health of patients but also save huge unnecessary healthcare costs every year by simply assisting in addressing the issue of poor prescription drugs. The applications of mHealth are likely to expand in the coming years. As diabetes grows more prevalent in the US, the potential of mHealth apps to help in diabetes care and prevention will be one of the most important domains for mHealth app producers. For instance, Britain’s National Health Service launched their Test Bed Programme, in which Type 1 or Type 2 diabetic patients were to be experimented with health technology, allowing them to self-manage their conditions by staying at home. This helps patients in cutting down additional costs incurred in the form of hospital stays. Also, in addition to the improved internet connectivity, decreasing internet costs, particularly in developing countries, are the major factors boosting the adoption of mHealth applications.

Various other next-generation health apps are mentioned below:

- The Mobile MIM app was the first medical app in Apple's App Store. It is used to view, register, fuse, and show medical images from SPECT, PET, CT, MRI, X-ray, and Ultrasound examinations for diagnosis purposes. Mobile MIM enhances physicians' access to pictures and allows them to consult with peers by providing wireless and portable access to medical images.

- WellDoc Inc. developed BlueStar Diabetes App that works by recording blood glucose data; it also provides real-time coaching. With more than 20,000 automated coaching messages, WellDoc's system analyzes the data and provides a tailored coach to help patients manage their medication and treatment.

The new Welch Allyn iExaminer app transforms the PanOptic Ophthalmoscope into a mobile digital imaging device that allows users to observe the eyes. The products were invented to simplify the detection of retinal detachment and glaucoma, among others. The adapter allows the optical access of the PanOptic Ophthalmoscope to the visual axis of an iPhone camera, allowing it to capture high-resolution images of the fundus and retinal nerve.

Medical Scheduling Software Market - End user Insights

Based on end user, the global medical scheduling software market is divided into hospitals, clinics, and others. The hospitals segment held the largest share of the market in 2021 and is expected to grow at the highest CAGR during the forecast period. Patients mainly prefer hospitals to seek treatment from various medical specialties such as cardiology, pediatric, pulmonary, psychiatric, and internal medicine. Hospitals are the primary points for patients for diagnostics, treatment, and other health care services. Many patients are admitted for surgical procedures, while several walks in for diagnostics. Most hospital patients are already suffering from various infectious and chronic diseases. Hospitals are primary healthcare centers for the people, which is likely to propel the medical scheduling software market growth for the segment.

Additionally, the increasing prevalence of chronic diseases such as cardiovascular disease, cancers, and chronic diseases fuels the demand for medical scheduling software to manage hospital patient visits. According to the World Health Organization, cardiovascular diseases (CVDs) are the leading cause of death globally, responsible for 17.9 million deaths yearly. Further, according to the WHO, cancer is one of the common causes of death globally, and it is predicted that the number of new cases will significantly increase by 2030. Approximately 400,000 children develop cancer annually. Thus, the rise in cancer, increase in the number of hospitals, and rise in surgical procedures for various CVDs across the globe increases the need for technology for efficient management of patient flow, which is anticipated to drive the demand for the hospitals segment in the medical scheduling software market during the forecast period.

Product launches and mergers and acquisitions are the highly adopted strategies by the players operating in the global medical scheduling software market. A few of the recent key product developments are listed below:

- In February 2022, Daw Systems, Inc. announced that it is a recipient of the 2021 Surescripts White Coat Award for Highest Accuracy. Daw Systems, Inc.'s core product, ScriptSure Cloud ERX v2.0, incorporates extensive functionality from the Surescripts network, allowing medical professionals to send prescriptions to pharmacies electronically.

- In September 2022, Upland Software and HP Inc. plan to bring Upland’s Document Workflow Cloud solutions onto HP Workpath as part of their continued efforts to modernize the flow of information between paper and digital. The new offering, expected to be released at the end of 2020, is a full end-to-end unified cloud-based workflow platform for document capture, image processing, and data extraction.

The COVID-19 pandemic brought worldwide shutdown of supply and demand chains which resulted in decline in the sales in the healthcare industry during the initial stage of lockdown. However, due to restriction such as social distancing and emergency appointment at hospitals the medical scheduling software market witnessed a growth during pandemic. Due to the growing demand for better administrative systems in healthcare settings and the growing shift towards internet-based platforms, the COVID-19 pandemic has positively impacted the medical scheduling software market. As a result of the increasing demand, the healthcare IT market is expected to grow healthy in the post-COVID-19 era.

Medical Scheduling Software Market - Segmentation

Based on software, the market is bifurcated into web-based and installed software. Based on end user the market is segmented into hospitals, clinics, and end users. Based on geography, the market is divided into North America (US, Canada, Mexico), Europe (France, Germany, UK, Italy, Spain, and Rest of Europe), Asia Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia Pacific), Middle East & Africa (Saudi Arabia, South Africa, UAE, and Rest of Middle East & Africa), South and Central America (Brazil, Argentina, and Rest of South and Central America)

Medical Scheduling Software Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 435.24 Million |

| Market Size by 2028 | US$ 927.09 Million |

| Global CAGR (2022 - 2028) | 13.4% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2028 |

| Segments Covered |

By Software

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Medical Scheduling Software Market Players Density: Understanding Its Impact on Business Dynamics

The Medical Scheduling Software Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Medical Scheduling Software Market - Company Profiles

- TimeTrade, AdvanceMD, Inc.

- Yocale Network Corporation

- Voicent Communications Inc.

- WellSky

- Daw Systems, Inc.

- ByteBloc Software

- Workpath

- Delta Health Technologies, Inc.

- DHS Worldwide

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends