Simulation Software Market Size, Demand & Growth by 2034

Coverage: By Component (Software, Services); Deployment Type (On-premise, Cloud); End-user (Automotive, Aerospace and Defense, Electrical and Electronics, Industrial Manufacturing, Healthcare, Education, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00002820

- Category : Technology, Media and Telecommunications

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 25, 2026

2025 Market Size

US$ 10.52 Bn

Base year value

2034 Forecast

US$ 23.37 Bn

Projected by 2034

CAGR 2026-2034

11.7 %

Growth rate

Addressable Market

US$ 171.44 Bn

(2026-2034)

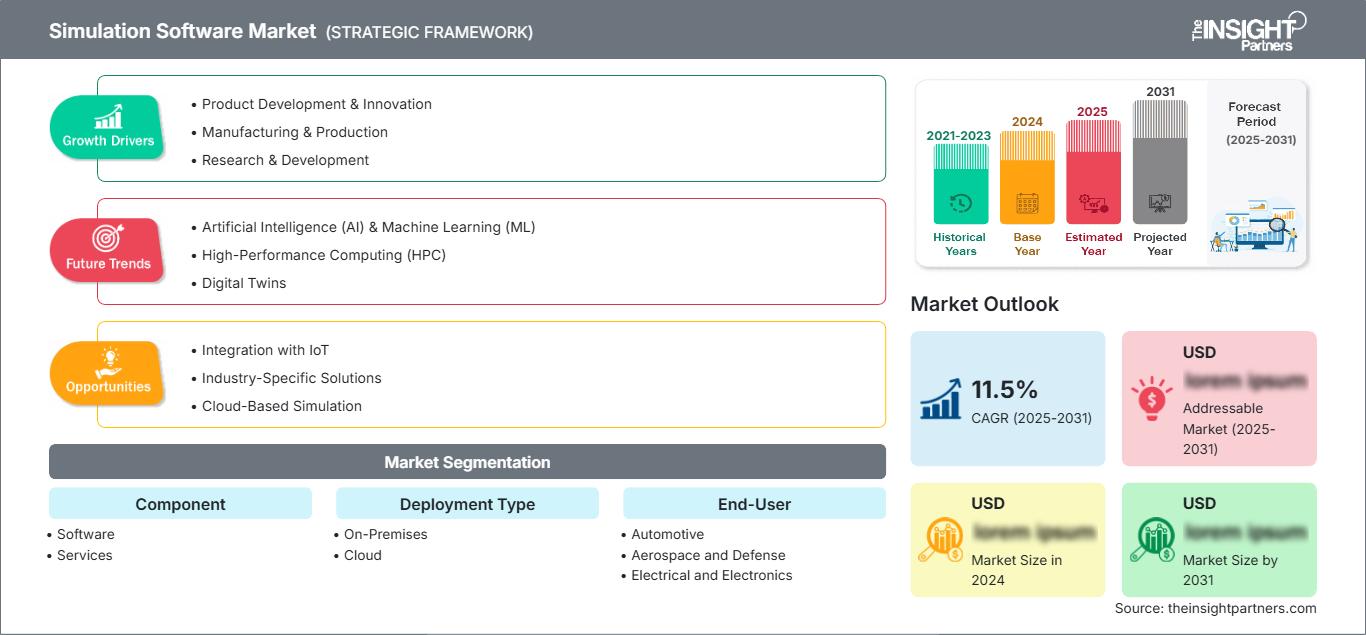

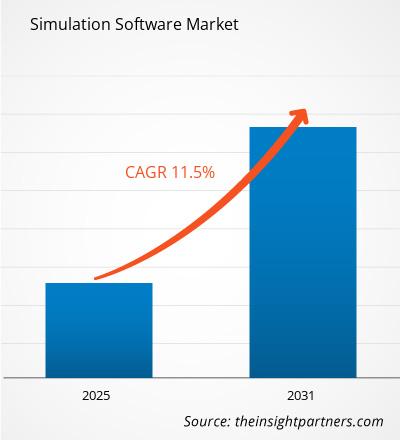

The global Simulation Software Market size is projected to reach US$ 23.37 billion by 2034 from US$ 10.52 billion in 2025. The market is anticipated to register a CAGR of 11.70% during the forecast period 2026–2034.

Key market dynamics include a heightening global focus on digital twins and Industry 4.0, rising adoption of virtual prototyping to reduce R&D costs, and a significant shift toward AI-integrated predictive modeling. Additionally, the market is expected to benefit from the growing complexity of electronic systems, expansion in cloud-native simulation platforms, and the increasing use of simulation in critical areas like autonomous driving and personalized healthcare.

Simulation Software Market Analysis

The simulation software market analysis shows high-fidelity virtual environments as industries prioritize operational efficiency and risk mitigation. The market is moving from traditional on-premises high-performance computing for defense and aerospace, and high-growth cloud-subscription models for agile manufacturing and startups. Strategic opportunities are emerging in medical training and surgical simulation, where high-definition virtual models offer a clear competitive advantage in patient safety. The analysis also notes that market expansion depends on seamless data interoperability and real-time synchronization between physical and digital assets. Competitive differentiation now stands out depending on the ability to provide multi-physics solvers that can handle complex structural, thermal, and fluid dynamics simultaneously, helping major developers charge premium prices in an increasingly technical landscape.

Simulation Software Market Overview

Simulation software has evolved from niche engineering applications to mainstream enterprise solutions. The simulation software includes finite element analysis, computational fluid dynamics, and electronic design automation tools. Both global technology corporations and specialized software firms compete in this market, using delivery models such as on-premises and cloud-based SaaS. Growing demand for faster product development cycles among automotive and electronics manufacturers in North America and Asia Pacific has increased the popularity of virtual testing as a cost-effective alternative to physical prototyping. North America leads in revenue due to its advanced aerospace and defense, while Asia Pacific is advancing in industrial automation and semiconductor manufacturing. The US market is the most developed, driven by high R&D spending and the broad availability of advanced engineering talent. Competition among brands is fueling greater automation and the inclusion of generative design features to optimize products automatically based on performance constraints.

Market Assessment and Insights

- Global market for Simulation Software was valued at US$ 10.52 Billion in 2025

- Annual market size is expected to reach US$ 23.37 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 171.44 Billion

- Market is anticipated to register a CAGR of 11.7% during the forecast period

- The United States represents a key market, supported by Product Development & Innovation, Manufacturing & Production, Research & Development, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Integration with IoT, Industry-Specific Solutions, Cloud-Based Simulation are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Altair Engineering, Inc., ANSYS, Inc., Autodesk Inc., BENTLEY SYSTEMS, INCORPORATED, Dassault Syst, Hexagon AB, PTC, Siemens, Synopsys, Inc., The MathWorks, Inc., while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Simulation Software Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Simulation Software Market Drivers and Opportunities

Market Drivers:

- Reduction in Product Development Time and Cost: Simulation allows engineers to identify design flaws virtually, significantly reducing the number of physical prototypes required. This nutritional efficiency for the R&D process is a primary driver for market adoption.

- Rapid Expansion of Digital Twin Technology: The integration of IoT sensors with virtual models has sustained high demand for real-time simulation capabilities. As industrial facilities trade up to smart factories, digital twin solutions continue to see stable volume gains.

- Advancements in Autonomous and Electric Vehicles: The shift toward EVs requires extensive battery and thermal management simulation, while autonomous driving relies on millions of virtual miles of sensor testing. This is particularly evident in the rapid adoption of simulation tools by automotive OEMs.

Market Opportunities:

- Expansion into In-Silico Clinical Trials: Beyond traditional engineering, simulation offers significant opportunities in healthcare for drug discovery and testing medical devices in virtual environments.

- Growth in 5G and Semiconductor Design: Forming strategic partnerships with electronics manufacturers may facilitate access to high-margin market segments in the APAC region, where demand for complex chip and network simulation is increasing.

- Diversification into Sustainable Engineering: There is a growing opportunity for software providers to target the renewable energy segment through simulations for wind turbine placement and solar grid optimization.

Simulation Software Market Report Segmentation Analysis

The Simulation Software Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Component:

- Software: The dominant volume driver, representing approximately 70% of the market. It includes core simulation engines and specialized modeling tools used across engineering disciplines.

- Services: A fast-growing segment focusing on consulting, training, and maintenance, as companies require specialized expertise to manage complex simulation workflows.

By Deployment Type:

- On-Premises: Holds a significant share, particularly in defense and aerospace, where data security and local high-performance computing are prioritized.

- Cloud: The fastest-rising deployment model, enabling remote collaboration, scalability, and lower upfront capital expenditure for small and medium-sized enterprises.

By End-User:

- Automotive: The largest end-user segment, utilizing simulation for crash testing, aerodynamics, and advanced driver-assistance systems.

- Aerospace and Defense: A primary consumer for mission-critical training, flight physics, and weapons system development.

- Electrical and Electronics: Relies on simulation for thermal management, circuit design, and semiconductor optimization.

- Industrial Manufacturing: Uses simulation to optimize factory floor layouts, production processes, and predictive maintenance.

- Healthcare: An emerging segment for surgical planning, patient-specific modeling, and medical device validation.

- Education: Increasing adoption of engineering pedagogy and research-driven virtual labs in higher education institutions.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Simulation Software Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 10.52 Billion |

| Market Size by 2034 | US$ 23.37 Billion |

| Global CAGR (2026 - 2034) | 11.7% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Component

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Simulation Software Market Players Density: Understanding Its Impact on Business Dynamics

The Simulation Software Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Simulation Software Market Share Analysis by Geography

Asia Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for industrial software providers and academic research institutions to expand.

The simulation software market is undergoing a significant transformation, moving from traditional desktop tools to integrated digital thread environments. Growth is driven by the rise of smart manufacturing, a surge in demand for green technologies, and the expansion of virtual training. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds the largest share globally, driven by heavy investment in defense and the presence of industry leaders like Ansys and Autodesk.

- Key Drivers:

- High R&D expenditure in the aerospace and defense sectors.

- Early adoption of AI-enhanced simulation and Digital Twin initiatives.

- Strong presence of tech hubs and advanced engineering research centers.

- Trends: Scaling of cloud-based collaborative engineering and the integration of simulation into the early conceptual design phase to reduce long-term costs.

2. Europe

- Market Share: A robust market anchored by the automotive and mechanical engineering sectors in Germany, France, and the UK.

- Key Drivers:

- Deep-seated automotive manufacturing base focusing on next-gen e-mobility.

- Strong government support for Industry 4.0 and sustainable manufacturing.

- Strict safety and environmental regulations requiring extensive virtual validation.

- Trends: A strategic shift toward sustainability-focused simulations and the growth of digital twins in manufacturing plants to meet ESG mandates.

3. Asia-Pacific

- Market Share: The fastest-growing region, with China and India acting as primary for manufacturing and electronics simulation.

- Key Drivers:

- Rapid industrialization and government-supported digital transformation initiatives.

- A massive electronics and semiconductor company seeking optimized design tools.

- Growing adoption of simulation in healthcare for medical training and surgical planning.

- Trends: Heavy reliance on e-commerce for software delivery and increasing B2B contracts for high-end automotive and infrastructure modeling.

4. South and Central America

- Market Share: Emerging market with a growing industry in countries like Brazil and Chile.

- Key Drivers:

- Modernization of the oil and gas industry through reservoir and drilling simulation.

- Rising interest in virtual training for the mining and manufacturing sectors.

- Trends: Growth of boutique engineering firms utilizing simulation for regional infrastructure projects and local manufacturing optimization.

5. Middle East and Africa

- Market Share: Developing market transitioning toward formalized industrial simulation in energy and urban planning.

- Key Drivers:

- Strategic investments in smart city projects (e.g., NEOM) and digital infrastructure.

- High demand for reservoir simulation to improve oil recovery rates.

- Trends: Implementation of virtual reality (VR) training for high-risk industrial environments and a focus on localized smart modeling.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Ansys, Inc., Dassault Systèmes, and Siemens Digital Industries Software. Specialist firms like The MathWorks, Inc., and Altair Engineering, Inc., alongside regional innovators such as Autodesk Inc. and PTC Inc., also contribute to a diverse market landscape.

This competitive environment pushes vendors to differentiate through:

- AI and Machine Learning Integration: Positioning simulation software as an intelligent assistant that can predict outcomes faster than traditional solvers.

- Multi-Physics Capabilities: Offering tools that can simulate heat, fluid, and structural stress in a single unified environment.

- SaaS and Subscription Models: Lowering the entry barrier for smaller firms by offering scalable, pay-as-you-go cloud services.

- Industry-Specific Solutions: Developing specialized modules for sectors like healthcare (biosimulation) or telecommunications (5G network modeling).

Opportunities and Strategic Moves

- Partner with cloud providers: To offer high-performance computing capabilities that reduce the local hardware burden for customers.

- Acquire niche AI startups: To integrate generative design and automated optimization into existing simulation workflows.

Major Companies operating in the Simulation Software Market are:

- Altair Engineering, Inc.

- ANSYS, Inc.

- Autodesk Inc.

- BENTLEY SYSTEMS, INCORPORATED

- Dassault Syst

- Hexagon AB

- PTC

- Siemens

- Synopsys, Inc.

- The MathWorks, Inc.

Disclaimer: The companies listed above are not ranked in any particular order.

Simulation Software Market News and Recent Developments

- In December 2025, Altair, a global leader in computational intelligence and now part of the leading technology company, Siemens, announced the latest updates to HyperWorks® 2026 software. With significant advances in AI, high-performance computing (HPC), and multiphysics integration, HyperWorks 2026 enables engineering teams to accelerate innovation and improve product performance across industries using comprehensive computer-aided engineering (CAE) design and simulation.

- In August 2025, Ansys, part of Synopsys and NVIDIA, signed an agreement to license, sell, and support Omniverse technology embedded in Ansys simulation solutions. Through its integration of NVIDIA Omniverse™, Ansys will deliver easy access to Omniverse technologies and libraries to customers, starting with its CFD and autonomous solutions. From deepening insights into aerodynamics to advancing autonomous vehicle safety and 6G connectivity, this collaboration fuels progress that empowers transformative solutions.

Simulation Software Market Report Coverage and Deliverables

The Simulation Software Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Simulation Software Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Simulation Software Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Simulation Software Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Simulation Software Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends