Telehealth Market Growth, Trends, and Analysis by 2031

Coverage: By Product (Integrated and Standalone), Type (Hardware, Services, and Software), Mode of Delivery (On-Premise, Web-Based, and Cloud-Based), End User (Patients, Payers, and Healthcare Providers), and Geography

- Status : Data Released

- Report Code : TIPHE100000832

- Category : Technology, Media and Telecommunications

- No. of Pages : 150

- Available Report Formats :

- Last update date : May 16, 2024

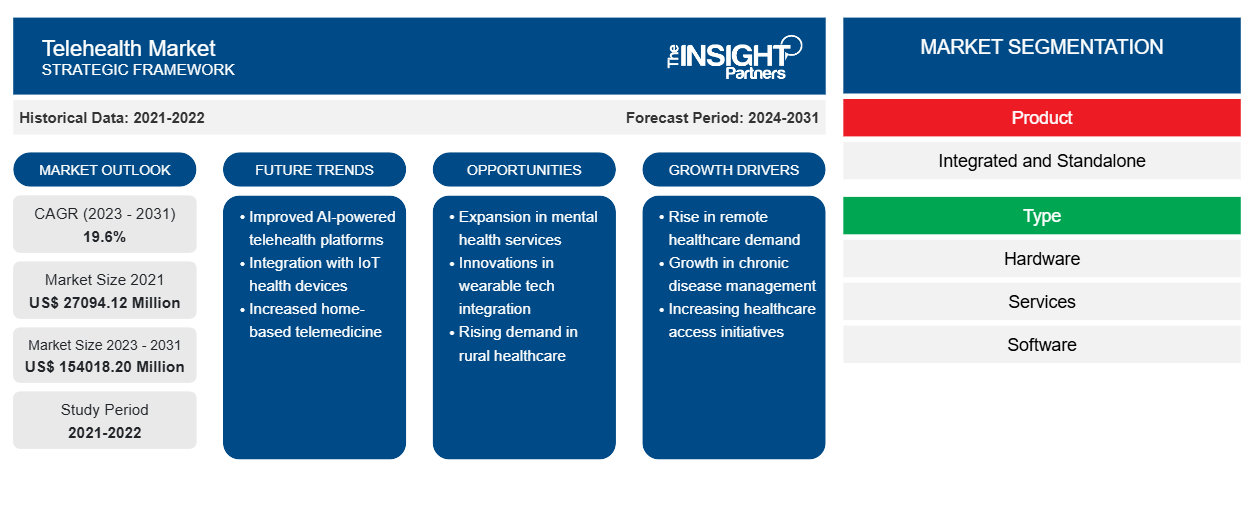

2021 Market Size

US$ 27094.12 Mn

Base year value

2031 Forecast

US$ 154018.20 Mn

Projected by 2031

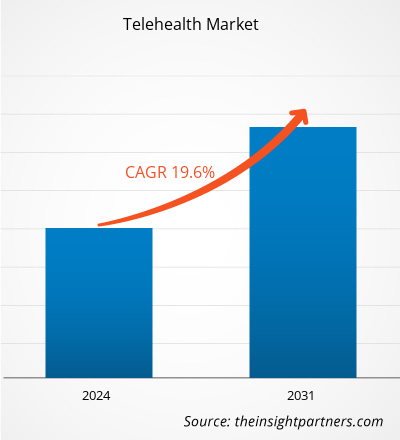

CAGR 2024-2031

19.6 %

Growth rate

Addressable Market

US$ 824,731.58 Mn

(2024-2031)

The Telehealth Market size was estimated to be US$ 27094.12 million in 2021 and US$ XX million in 2023 and is expected to reach US$ 154018.20 million by 2031; it is estimated to record a CAGR of 19.6% in till 2031. Telehealth plays a vital role in improving healthcare services with technology. With the widespread use of technology and its adoption in rural areas, telehealth has shown notable advantages. Moreover, it reduces costs to the patient and healthcare system, particularly for patients living in rural areas. The patients can be diagnosed remotely, and their data is shared with clinical experts either via store-and-forward technology or in the online session. The increasing prevalence of cardiovascular disease, home monitoring for the treatment, and reduced cost for chronic treatments is likely to remain key Telehealth Market trends.

Telehealth Market Analysis

Tele-homecare is an innovative way to provide care, monitor a patient, and provide information using the latest technology. Monitoring allows early identification of diseases and provides aid in emergencies. Hence, the use of tele home services is increasing. For instance, according to an article published by JMIR Publications, in January 2022, children and their families chose pediatric tele home care since it is 9% less expensive than traditional hospital care, freeing up hospital beds for more complicated situations in Spain.

Moreover, people prefer tele-home at home rather than visiting a hospital for treatment owing to greater convenience and reduction in overall cost. For instance, according to an article published by the Partnership for Quality Home Healthcare, in 2021, ~86% of adults preferred to receive "post-hospital, short-term healthcare" at home, while only 5% preferred nursing homes in the United States. Tele home services provide an opportunity for significant savings for patients and hospitals. Further, home monitoring programs are intended to help patients with re-hospitalization or frequent ER visits to receive treatment in the comfort at home. The home monitoring program aims to reduce hospital trips or readmissions to the physician and length of hospital stays. The monitoring programs comprise a wide range of patient health data from the point of care, including vital signs, weight, heart rates, blood sugar, blood oxygen levels, blood pressure, and electrocardiograms. The data can be transmitted to skilled health professionals in facilities such as hospitals & intensive care units, skilled nursing facilities, centralized off-site case management programs, and monitoring centers in primary care settings. The professionals monitor the patients remotely and provide a treatment plan based on the health data information. The home monitoring programs are designed to achieve the "triple aim" of health care by improving access to care, patient outcomes, and making health care systems more cost-effective. The above-mentioned factor is anticipated to have a positive impact on the growth of telehealth market.

Telehealth Market Overview

The growth of the telehealth market is attributed to some key driving factors such as the increasing prevalence of cardiovascular disease, home monitoring for the treatment, and reduced cost for chronic treatments. However, lack of regulations and limited access in rural areas are major factors hindering the market growth. Global telehealth market is segmented by region into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. In North America, the US is the largest market for telehealth. The growth of the region is attributed to large amount of investments done by local government for remote monitoring and virtual care. According to the Centers for Disease Control and Prevention, from 2019 to 2021, telemedicine use increased from 15.4% to 86.5% in the United States. In addition, digital health innovations are further expected to stimulate the growth of telehealth market in North America.

The Asia Pacific region is expected to account for the fastest growth in the telehealth market. The telehealth market in Asia Pacific is likely to witness rapid growth owing to rising convenience of telehealth services amongst the millennial and increasing numbers of smartphone users. Such a factor is expected to aid the growth of telehealth market during the forecast period.

Market Research Highlights

- Global market for Telehealth was valued at US$ 27,094.12 Million in 2709

- Annual market size is expected to reach US$ 154,018.20 Million by 2031

- Total addressable market (TAM) during 2024-2031 is projected to reach approximately US$ XX

- Market is anticipated to register a CAGR of 19.6% during the forecast period

- The United States represents a key market, supported by Rise in remote healthcare demand, Growth in chronic disease management, Increasing healthcare access initiatives, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion in mental health services, Innovations in wearable tech integration, Rising demand in rural healthcare are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Medtronic, Cerner Corporation, Tunstall Healthcare, AMD Global Medicine, Inc., Philips Healthcare, Cisco Systems, Inc., Aerotel Medical Systems Ltd., Honeywell Life Care Solutions, Medvivo Group Ltd., American Well, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Telehealth Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Telehealth Market Drivers and Opportunities

Use Cases of Telehealth in Healthcare Industry to Favor Market

The telemedicine in healthcare industry has grown significantly over the past few years. Telecommunications enable healthcare professionals to evaluate, diagnose and treat patients virtually. Technologies like telemonitoring devices, home messaging services, monitoring centers, and voice recognition are used to make remote healthcare more streamlined and efficient. With the increasing adoption of smartphones and easy availability of technologically advanced devices, innovators have started investing to make the most of the current situation of the industry, by focusing on delivering quality healthcare & comfort through various mobile platforms, which would help patients track their fitness regimes and obtain answers to medical inquiries over the phone, WhatsApp, or through several mobile applications. For instance, several apps, such as Teladoc Health, Doctor Anywhere, Doctor On Call, and ClicknCare, have been introduced to help patients book appointments, track their consultations & medical prescriptions, and store their healthcare information throughout the treatment. Remote care and telehealth ensure that medical professionals can provide services to patients who need care without the added risk of spreading disease.

Moreover, telemedicine has become the backbone of healthcare and will continue to evolve long into the future. Eventually, telemedicine will become the primary care delivery model, combined with better diagnostic tools, device integration and data interoperability. This need is likely to drive the telehealth market during the forecast period.

Technological developments – An Opportunity in Telehealth Market

Various launches of technologically advanced products for telehealth are expected to boost market growth. For instance, in January 2023, Teladoc Health, the global leader in whole-person virtual care, announced the launch of a fully integrated healthcare experience through a new comprehensive digital application enabling personalized whole-person care to individuals. Consumers can now seamlessly access Teladoc Health’s full range of services, including primary care, mental health, and chronic condition management, from one place and under a single portable account. Such technological advancements are estimated to generate attractive growth opportunity for the telehealth market.

Telehealth Market Report Segmentation Analysis

Key segments that contributed to the derivation of the Telehealth Market analysis are type and mode of delivery.

- Based on type, the telehealth market is segmented into hardware, services, and software. In 2023, the software segment held the largest share of the market. Moreover, the same segment is expected to register the highest CAGR during the forecast period. The software is secured, which provides free access for patients to deliver health care, health information or health education at a distance through online service on mobile phones. Telehealth software enables execution in various settings to abolish the need for special training and minimize downtime. Additionally, it helps in, epidemiology & public health, electronic health records, personal wellness & fitness applications, clinical reference, and patient decision support.

- Based on mode of delivery, the telehealth market is divided into on-premise, web-based, and cloud-based. In 2023, the web-based delivery mode held the largest market share by mode of delivery. However, the cloud-based segment is expected to register the highest CAGR in the market during the forecast period. The cloud-based delivery mode is the more safe and standardized information system used for online computing services and is essential for delivering on-demand computing resources. The cloud-based system allows the user to connect to the computer via the internet or web browser, enabling access to the data anytime, anywhere on any device. Cloud-based delivery mode system is an extremely manageable alternative that helps access real-time information.

Telehealth Market Share Analysis by Geography

The geographic scope of the Telehealth Market report is mainly divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South America/South & Central America.

In terms of revenue, North America dominated the telehealth market share. The North America telehealth market has been segmented into the US, Canada, and Mexico. The US holds the largest share of the North American telehealth market. The growth of telehealth market in the US is attributed to the various market players, and a dynamic scenario has been established. It has transformed the dynamics of telehealth in the region. The growth in North America is characterized by companies engaged in partnerships, collaborations, acquisitions, mergers, and product launches to innovate in the telemedicine market, driving growth in the forecast period. For instance, in April 2021, Inova Health System offered an FDA-approved telemedicine option for remote neuromodulation of deep brain stimulation (DBS) patients being treated for Parkinson’s disease and essential tremors. Thus, the growing prevalence of remote monitoring will likely contribute to the growth of the US telemedicine market size.

Telemedicine

Telehealth Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 27094.12 Million |

| Market Size by 2031 | US$ 154018.20 Million |

| Global CAGR (2023 - 2031) | 19.6% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Telehealth Market Players Density: Understanding Its Impact on Business Dynamics

The Telehealth Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Telehealth Market News and Recent Developments

The Telehealth Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. The following is a list of developments in the market for Telehealth and strategies:

- In November 2023, a bipartisan group of four senators reintroduced legislation that eliminated barriers to the virtual prescription of medication for opioid use disorder (OUD). (Source: mHealth Intelligence, 2023)

Telehealth Market Report Coverage and Deliverables

The “Telehealth Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market dynamics such as drivers, restraints, and key opportunities

- Key future trends

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Global and regional market analysis covering key market trends, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends