Viral Vector and Plasmid DNA Manufacturing Market Segments and Growth by 2027

Viral Vector and Plasmid DNA Manufacturing Market Forecast to 2027 - Analysis by Product (Viral Vectors and Non-viral Vectors) and Application (Cancer, Inherited Disorders, Viral Infections, and Others)

- Status : Published

- Report Code : TIPRE00003074

- Category : Life Sciences

- No. of Pages : 140

- Available Report Formats :

- Last update date : June 13, 2024

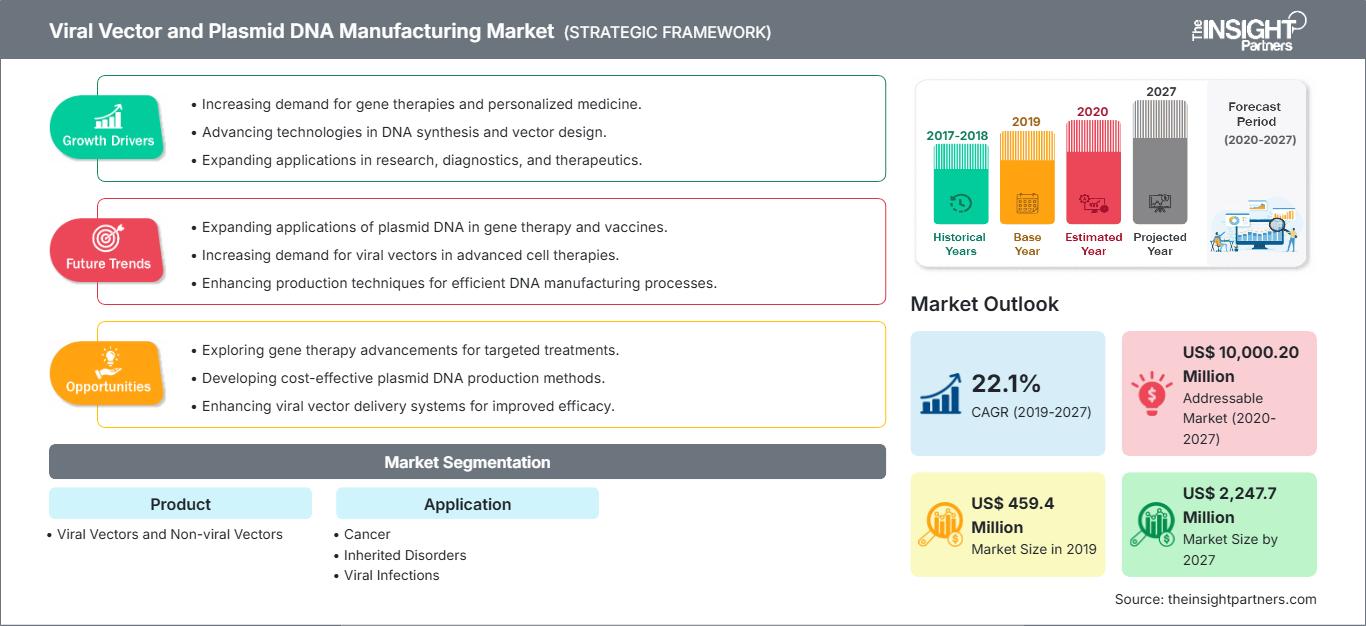

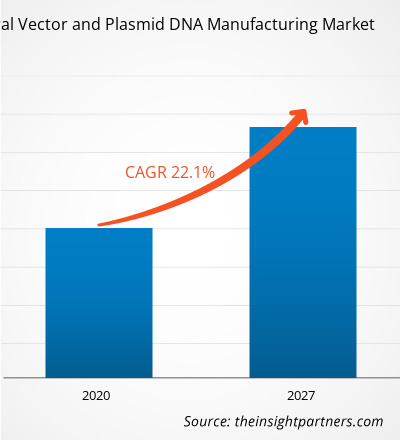

2019 Market Size

US$ 459.4 Mn

Base year value

2027 Forecast

US$ 2,247.7 Mn

Projected by 2027

CAGR 2020-2027

22.1 %

Growth rate

Addressable Market

US$ 10,000.20 Mn

(2020-2027)

[Research Report] The viral vector and plasmid DNA manufacturing market size was projected to grow from US$ 459.4 million in 2019 to US$ 2,247.7 million by 2027; it is further estimated to record a CAGR of 22.1% from 2020–2027.

Analyst Perspective:

The increasing demand for gene therapy and advancement in gene editing technologies for the development of treatment option for various chronic disorders, viral infection, and others are driving the viral vector and plasmid DNA manufacturing market growth. Additionally, increase in research activities and growing investments in pharmaceutical & biotechnology industries followed by the favorable regulatory scenario is expected to anticipate the market growth. Moreover, integration of advanced computing technologies is further expected to enhance the application area of viral vector and plasmid DNA manufacturing in near future which in turn propelling the market growth.

Market Overview:

A viral vector is a tool used in gene delivery and manipulation. It is modified virus that has been engineered to carry and deliver specific genes into cells. Viral vectors are commonly used in gene therapy for gene editing application, as they can efficiently deliver genetic material into target cells. Plasmid vector is a small circular piece of DNA that is separate from the chromosomal DNA in a cell. Plasmids can replicate independently and are commonly found in bacteria. In research, plasmids are often used as vectors to introduce genes into cells for various purposes, such as protein production or genetic engineering. Both viral vector and plasmid DNA are essential tools for gene delivery and manipulation in research, allowing researchers to understand potential applications.

Market Assessment and Insights

- North America dominated the market with 40.1% share in 2019.

- Asia Pacific is poised to grow at a CAGR of 23.9% over the forecast period.

- United States market is projected to grow at a CAGR of 22.3% over the forecast period.

- By Product, the Viral Vectors segment accounted for the largest market share of 67.3% in 2019.

- By Application, the Cancer segment is anticipated to witness the fastest growth, registering a CAGR of 22.6% over the forecast period

- The report profiles key industry players such as Sanofi SA, BRAMMER BIO, BRAMMER BIO, FUJIFILM Diosynth Biotechnologies Ltd, Cell and Gene Therapy Catapult, Cobra Biologics, FinVector, Kaneka Eurogentec S.A., MassBiologics, Spark Therapeutics Inc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Viral Vector and Plasmid DNA Manufacturing Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Market Trends:

I

ntegration of Advanced Computing TechnologiesEmergence of revolutionary technologies such as artificial intelligence, data science, natural language processing, and others are estimated to reshape the future of healthcare technologies during the forecast period. However, gene therapy offers innovative solutions for treatment of diseases, the execution of it faces some technical challenges. For instance, error in gene replacing may lead to harmful mutations in the DNA, resulting into severe health problems. To achieve high level of precision in procedures, intelligent algorithms can offer a significant way. Further, a majority of players are engaged in R&D of new technologies, which will deal with increasing demand for modern technologies. For instance, in March 2019, Oxford Biomedica entered into strategic collaboration with Microsoft to improve gene therapies. Moreover, in May 2020, Dyno Therapeutics announced its proposed financial investments of an estimated US$ 2.0 billion to design AI-based gene therapies. Such events represent a huge opportunity for the integrations of advanced computing technologies, which will eventually redefine the concept of gene therapies during years to come.

Segmental Analysis:

Based on application, the viral vector and plasmid DNA manufacturing market is segmented into cancer, inherited disorders, viral infections, and others. The cancer segment held the largest share of the market in 2019, and the same segment is anticipated to register the highest CAGR of 22.6% during the forecast period. Viral vectors and non-viral vectors have their application and are being studied for both preventive and therapeutic applications in cancer or oncology. Viral vector-based immunization with anticancer agents or delivery of anticancer genes is some critical areas of research that have shown steady progress. Moreover, the government approvals of lentiviral vector-based CAR-T cell therapies, which is used for the treatment of Acute Lymphoblastic Leukemia (ALL) and large B cell lymphoma, have attracted considerable attention from users. Viral vectors and non-viral vectors have resulted in a significant proliferation of the cancer-based pipeline projects on advanced therapies. For instance, around two-thirds of the research in gene therapy is focused on oncology. The above-mentioned factors have contributed to the dominance of cancer over other disease areas. Based on products, the global viral vector and plasmid DNA manufacturing market is bifurcated into viral and non-viral vectors. In 2019, the viral vectors segment held the largest market share, and the same segment is expected to grow at the fastest CAGR during the coming years.

Regional Analysis:

Based on geography, global viral vector and plasmid DNA manufacturing market is segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. North America held the largest viral vector and plasmid DNA manufacturing market share which is closely followed by Europe. The US held the largest share of the North American viral vector and plasmid DNA manufacturing market in 2019. The growth of the US market is primarily driven by the growing awareness regarding benefits of gene therapy, increasing research and development activities, and rising demand for advanced therapeutic solutions to treat chronic conditions and viral infections.

In addition, increasing demand for viral vectors due to growing adoption of gene therapies is also anticipated to drive the US viral vector and plasmid DNA manufacturing market growth during the forecast period. In addition, due to this growing demand, major players in the market are focusing on expansion of their viral vector manufacturing capacity. For instance, in May 2020, Thermo Fisher Scientific Inc. announced its plan to expand viral vector manufacturing capacity. According to company estimates, the new facility will be operational by 2022. Further, in April 2020, Merck announced its proposed plan to open a new US-based manufacturing facility for viral vectors. The company has invested around US$ 112.6 million for this proposed expansion.

In Canada, the viral vector and plasmid DNA manufacturing market growth is expected owing to the development of the healthcare systems and rapidly increasing adoption of modern cell related technologies. On the other hand, in Mexico, it is expected that the viral vector and plasmid DNA manufacturing market is likely to experience growth opportunities due increasing awareness of benefits offered by viral vectors and plasmid DNA.

Key Player Analysis:

The viral vector and plasmid DNA manufacturing market majorly consists of the players such as Brammer Bio, Sanofi, Cardinal Health Inc, FUJIFILM Diosynth Biotechnologies, Cell and Gene Therapy Catapult, Cobra Biologics, FinVector, Kaneka Eurogentec SA, MassBiologics, Spark Therapeutics, and Uniqure among others. Among the players in the viral vector and plasmid DNA manufacturing market, Sanofi and FUJIFILM Diosynth Biotechnologies are the top two players owing to their organic and inorganic activities.

Viral Vector and Plasmid DNA Manufacturing Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2019 | US$ 459.4 Million |

| Market Size by 2027 | US$ 2,247.7 Million |

| Global CAGR (2019 - 2027) | 22.1% |

| Historical Data | 2017-2018 |

| Forecast period | 2020-2027 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Viral Vector and Plasmid DNA Manufacturing Market Players Density: Understanding Its Impact on Business Dynamics

The Viral Vector and Plasmid DNA Manufacturing Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Recent Developments:

Inorganic and organic strategies such as mergers and acquisitions are highly adopted by companies in the viral vector and plasmid DNA manufacturing market. A few recent key market developments are listed below:

- In March 2023, Sartorius acquired French company Polyplus for 2.4 billion euros ($2.6 billion). The deal gives Sartorius additional know-how in nucleic acid delivery, including transfection reagents and plasmid DNA design, all of which are key elements in the production of viral vectors for building cell and gene therapies.

- In July 2021, Thermo Fisher Scientific Inc. opened a new cGMP plasmid DNA manufacturing facility in Carlsbad, Calif., enabling it to meet rapidly growing demand for plasmid DNA-based therapies and vital mRNA-based vaccines.

- In March 2021, WACKER acquired 100% of the shares in pharmaceutical contract manufacturer Genopis Inc. from Helixmith Co Ltd, Seoul (South Korea) and Medivate Partners LLC, Seoul (South Korea) in February. The signing of the related agreement was followed by the successful closing in late February and, now, the acquisition’s new name: Wacker Biotech US Inc.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends