Bio-Based Ethylene Market Size, Share & Demand by 2034

Bio-Based Ethylene Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Raw Material (Sugars, Starch, and Lignocellulosic Biomass) and End-User Industry (Packaging, Detergents, Lubricant, and Additives)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00015881

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

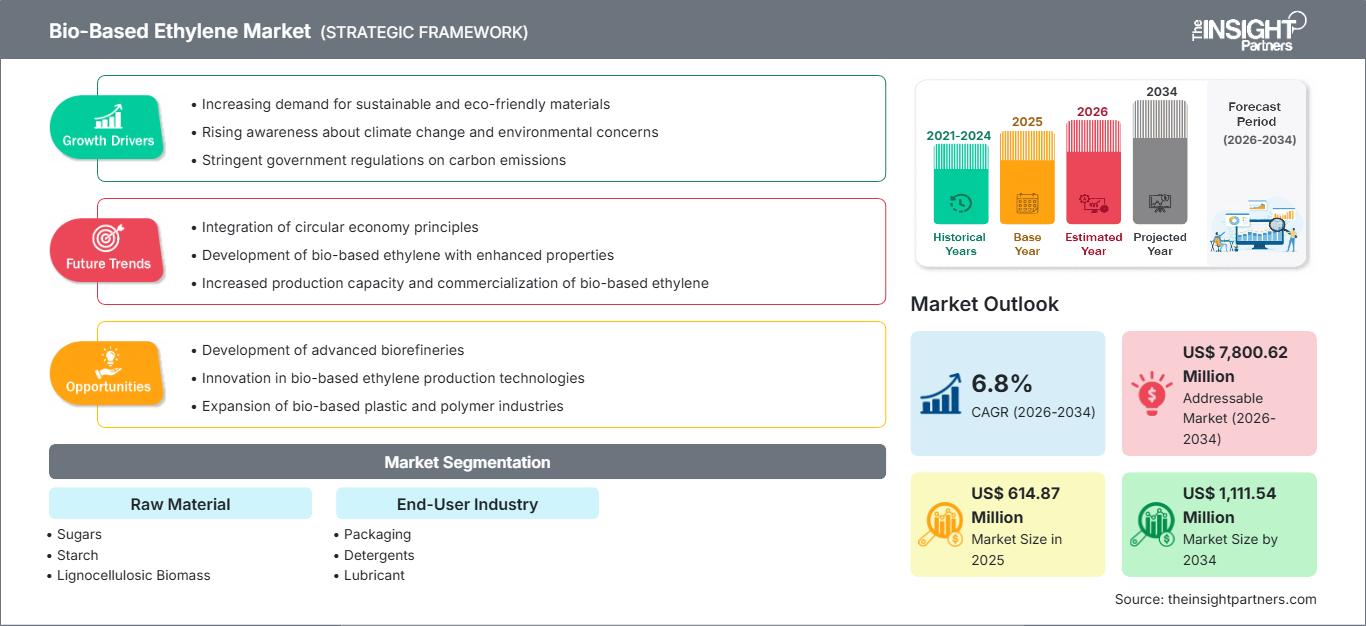

The global Bio-Based Ethylene market size is projected to reach US$ 1,111.54 million by 2034 from US$ 614.87 million in 2025. The market is anticipated to register a CAGR of 6.8% during the forecast period 2026–2034. Key dynamics include an aggressive global pivot toward decarbonizing the plastics value chain, increased regulatory pressure on single-use plastics, and the rapid scale-up of "drop-in" renewable chemical solutions. Furthermore, the market is set to benefit from the rise of sustainable aviation fuel (SAF) production, which generates bio-naphtha as a byproduct, and the growing commitment of global consumer brands to achieve net-zero Scope 3 emissions by 2040.

Bio-Based Ethylene Market Analysis

The Bio-Based Ethylene market analysis reveals a critical transition from pilot-scale experimental production to industrial-scale commercialization. To succeed, businesses must navigate the "green premium"—the cost gap between bio-ethylene and fossil-based equivalents, which remains approximately 20-40% higher depending on feedstock volatility. Strategic opportunities lie in the integration of Mass Balance accounting, allowing manufacturers to co-process bio-feedstocks in existing steam crackers without massive capital expenditure. This "drop-in" capability is essential for rapid market entry into the high-volume polyethylene (PE) sector.

Decision-makers should focus on securing long-term offtake agreements with brand owners in the packaging and automotive industries, who are willing to absorb price premiums to meet environmental ESG targets. Competitive differentiation is increasingly tied to ISCC PLUS certification, which ensures traceability across the supply chain. Furthermore, the analysis indicates that the market is shifting toward lignocellulosic biomass to avoid the "food vs. fuel" debate associated with first-generation sugars. Successful market participation now requires a dual focus on feedstock security and the utilization of government tax credits, such as the US Inflation Reduction Act, to offset high operational expenses.

Bio-Based Ethylene Market Overview

Bio-based ethylene is undergoing a structural transformation, evolving from a niche chemical curiosity into a fundamental pillar of the global circular economy. Historically dependent on sugar-to-ethanol dehydration in regions like Brazil, bio-based ethylene is now diversifying into a multi-feedstock ecosystem. Significant breakthroughs in catalytic conversion and fermentation technologies propel this transition. As the largest bulk chemical by volume, ethylene's shift to renewable sources is viewed as the "holy grail" for decarbonizing the polymer industry.

Large-scale chemical giants are increasingly adopting "drop-in" solutions, where bio-based ethylene is chemically identical to its petroleum counterpart, requiring no downstream equipment modifications. However, the market faces a complex landscape where growth is balanced against high CAPEX requirements and the logistical challenge of biomass collection. Current trends show a massive surge in B2B partnerships between agricultural processors and petrochemical firms, creating integrated value chains that mitigate feedstock price volatility. The US bio-based ethylene market is rapidly evolving, driven by abundant agricultural feedstocks and federal incentives like the Inflation Reduction Act (45Z credits). While traditional ethane cracking dominates, Gulf Coast facilities are increasingly integrating bio-naphtha. Key players are leveraging advanced ethanol-to-jet and dehydration technologies to supply the growing demand for sustainable packaging and automotive components.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONBio-Based Ethylene Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Bio-Based Ethylene Market Drivers and Opportunities

Market Drivers:

- Stringent Carbon Emission Regulations: Global mandates, such as the EU Green Deal and the US EPA's renewable fuel standards, are forcing chemical manufacturers to lower their carbon intensity. Bio-based ethylene offers a carbon-neutral or even carbon-negative profile (when combined with CCUS), making it a primary tool for regulatory compliance.

- Corporate Sustainability Commitments: Major consumer-facing giants (e.g., Coca-Cola, IKEA, and Unilever) have pledged to transition to 100% renewable or recycled plastics. This massive "pull" demand from the end-user level provides a guaranteed market for bio-ethylene derivatives like Bio-PE and Bio-PET.

- Advancements in Ethanol Dehydration Technology: Modern catalytic processes for converting bio-ethanol into ethylene have achieved yields exceeding 99%. These technological refinements, pioneered by companies like Lummus Technology and Braskem, have significantly improved the energy efficiency and economic viability of the dehydration route.

Market Opportunities:

- Utilization of Second-Generation (2G) Feedstocks: Moving beyond food-based sugars to lignocellulosic biomass (agricultural residues, forestry waste) presents a major opportunity to reduce feedstock costs and improve the environmental profile, appealing to eco-conscious consumers and avoiding land-use conflicts.

- Expansion into Bio-Based Ethylene Oxide (EO) and Glycols: While polyethylene is the primary outlet, there is an underserved opportunity in the detergents and lubricants sector. Bio-based EO serves as a precursor for renewable surfactants, allowing "green" cleaning brands to claim 100% bio-based formulations.

- Strategic Integration with SAF Production: As the aviation industry scales Sustainable Aviation Fuel (SAF), the resulting bio-naphtha byproduct can be fed into existing crackers. This synergy allows petrochemical companies to diversify their feedstock mix with minimal infrastructure changes, creating a stable supply of bio-attributed ethylene.

Bio-Based Ethylene Market Report Segmentation Analysis

The Bio-Based Ethylene Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Raw Material:

- Sugars: Currently the dominant segment, primarily utilizing sugarcane and sugar beet. It benefits from well-established fermentation-to-ethanol pathways, particularly in Brazil and India, offering the highest yield and commercial maturity.

- Starch: Derived mainly from corn and wheat. This segment is prominent in North America; however, it faces scrutiny regarding food security, leading to a shift toward industrial-grade starch sources.

- Lignocellulosic Biomass: The fastest-growing niche, utilizing non-food residues like corn stover and wood chips. It is highly favored for its superior sustainability profile and is the focus of intense R&D for commercial scaling.

By End-User Industry:

- Packaging: The largest consumer segment. It utilizes bio-polyethylene for bottles, films, and containers, driven by the global retail shift away from fossil-based single-use plastics.

- Detergents: Bio-ethylene is converted into bio-based surfactants. This segment is expanding as home care brands look to replace petrochemical ingredients in liquid soaps and laundry pods.

- Lubricant and Additives: A specialized high-value segment. Bio-based ethylene is used to produce synthetic esters and polyalphaolefins (PAOs), offering superior biodegradability and performance for industrial and automotive lubricants.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Bio-Based Ethylene Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 614.87 Million |

| Market Size by 2034 | US$ 1,111.54 Million |

| Global CAGR (2026 - 2034) | 6.8% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Raw Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Bio-Based Ethylene Market Players Density: Understanding Its Impact on Business Dynamics

The Bio-Based Ethylene Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Bio-Based Ethylene Market Share Analysis by Geography

The bio-based ethylene market is undergoing a significant transformation, moving from a niche renewable alternative to a global high-value industrial chemical. Growth is driven by the rising regulatory pressure on carbon footprints, a surge in "net-zero" corporate commitments, and the expansion of the sustainable packaging sector. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a leading position globally, serving as a primary hub for technological innovation and commercial-scale production.

- Key Drivers: Significant federal support and tax incentives focused on decarbonizing the industrial chemical sector.

- Wide availability of agricultural feedstocks and a highly integrated petrochemical infrastructure that facilitates bio-blending.

- Strong domestic demand from consumer-facing brands seeking to reduce the carbon intensity of their plastic supply chains.

- Trends: Rapid adoption of mass balance accounting models and a transition toward utilizing agricultural waste and residues to produce second-generation renewable chemicals.

2. Europe

- Market Share: Accounted for a substantial portion of the global market, led by advanced sustainability policies and legislative frameworks.

- Key Drivers: Stringent environmental mandates and circular economy initiatives that prioritize renewable carbon sources over fossil-based inputs.

- High carbon costs and emissions trading systems that encourage chemical manufacturers to adopt bio-attributed feedstocks.

- Government-backed research and development aimed at establishing sustainable chemical clusters.

- Trends: A strategic focus on waste-to-ethylene technologies and a heavy reliance on rigorous third-party certifications to ensure supply chain transparency and carbon traceability.

3. Asia-Pacific

- Market Share: Recognized as the fastest-growing region, driven by massive capacity expansions and the rapid industrialization of emerging economies.

- Key Drivers: Strategic government initiatives aimed at reducing dependence on imported fossil fuels through the development of a local bio-economy.

- Growing middle-class demand for eco-friendly consumer goods and sustainable packaging in high-volume retail sectors.

- Favorable partnerships between regional agricultural producers and international chemical firms to secure stable feedstock supplies.

- Trends: Intensive investment in large-scale ethanol dehydration facilities and the integration of renewable energy sources to power bio-refinery operations.

4. Central and South America

- Market Share: Holds a specialized and significant share, particularly as a global exporter of low-carbon building blocks.

- Key Drivers: Natural competitive advantage due to the world's most efficient production of high-yield sugar crops used for fermentation.

- Established vertical integration where companies manage the entire lifecycle from biomass cultivation to polymer manufacturing.

- Strong orientation toward international markets that require premium-grade renewable resins.

- Trends: Expansion of dedicated production facilities and the development of "carbon-negative" materials that leverage sustainable land-use practices.

5. Middle East and Africa

- Market Share: An emerging market currently focusing on long-term economic diversification and strategic pilot projects.

- Key Drivers: Regional visions targeting a shift away from oil dependency and toward advanced, sustainable manufacturing.

- Strategic investments in agriculture and chemical technologies suited for arid climates.

- Increasing interest in the production of high-value specialty chemicals and renewable additives for urban infrastructure.

- Trends: Implementation of pilot programs for carbon-capture-to-chemical conversion and the upgrading of existing industrial facilities to process bio-based naphtha.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Braskem S.A., The Dow Chemical Company, LyondellBasell Industries Holdings B.V., SABIC, Enerkem, Linde, Shell Global, TotalEnergies, and Axens, which also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Premiumization and Sustainability Branding: Positioning bio-based ethylene as a superior, low-carbon alternative to fossil-derived equivalents. Companies leverage ISCC PLUS certification to offer "I'm green™" polymers, emphasizing carbon sequestration and fossil-free credentials to appeal to global FMCG brands.

- Diverse Derivative Portfolios: Bio-based ethylene products now include more than just polyethylene (PE). Companies offer renewable precursors for bio-based surfactants (detergents), specialty glycols, and high-end renewable elastomers used in the automotive and medical sectors.

- Vertical Integration and Feedstock Security: Producers manage the entire supply chain, from sourcing sugarcane and agricultural residues (corn stover) to local chemical conversion. This approach ensures supply chain transparency and meets the ethical, clean-label standards demanded by sustainable finance regulators.

- Advanced Processing Technologies: New processing technologies, like catalytic ethanol-to-ethylene (E2E) dehydration and direct CO2-to-ethylene photosynthesis, help create high-purity bio-ethylene used in high-performance polymers and cosmetic ingredients worldwide.

Opportunities and Strategic Moves

- Partner with High-End Retail and Consumer Brands: Tap into the surging demand for sustainable, plant-based packaging in the Asia-Pacific and North American markets by forming strategic offtake agreements with leaders in the food, beverage, and personal care sectors.

- Incorporate Sustainable Farming and Regenerative Practices: Implement agricultural sourcing and waste-valorization certifications (e.g., RSB, Bonsucro) to appeal to environmentally conscious stakeholders seeking ethical alternatives to traditional petrochemicals.

Major Companies operating in the Bio-Based Ethylene Market are:

- Braskem S.A.

- The Dow Chemical Company

- LyondellBasell Industries Holdings B.V.

- SABIC

- Enerkem

- Linde

- Shell Global

- TotalEnergies

- Axens

Disclaimer: The companies listed above are not ranked in any particular order.

Bio-Based Ethylene Market News and Recent Developments

- In November 2025, LanzaTech Global, Inc., a leader in industrial carbon recycling, was awarded a €40 million grant from the European Union's Innovation Fund. The project featured the first commercial deployment of the company's second-generation bioreactor, which aimed to produce 23.5 kt of ethanol per year by consuming smelter furnace greenhouse gases from the Porsgrunn Manganese Smelter. This renewable ethanol was intended to serve as a critical precursor for the production of Bio-Based Ethylene, providing a sustainable alternative for the European plastics and chemical industries.

- In July 2024, Dow announced at the German Rubber Conference (DKT) the launch of NORDEL™ REN Ethylene Propylene Diene Terpolymers (EPDM), which functioned as a renewable version of their established rubber material. This innovation utilized Bio-Based Ethylene as a primary feedstock to create a high-performance material suitable for automotive, infrastructure, and consumer applications.

Bio-Based Ethylene Market Report Coverage and Deliverables

The "Bio-Based Ethylene Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Bio-Based Ethylene Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Bio-Based Ethylene Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Bio-Based Ethylene Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Bio-Based Ethylene Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For