Industrial Wood Adhesives Market Size, Growth & Trends by 2034

Industrial Wood Adhesives Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Resin Type (Natural and Synthetic) and Technology (Solvent-Based, Water-Based, Solventless, and Others)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00022059

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

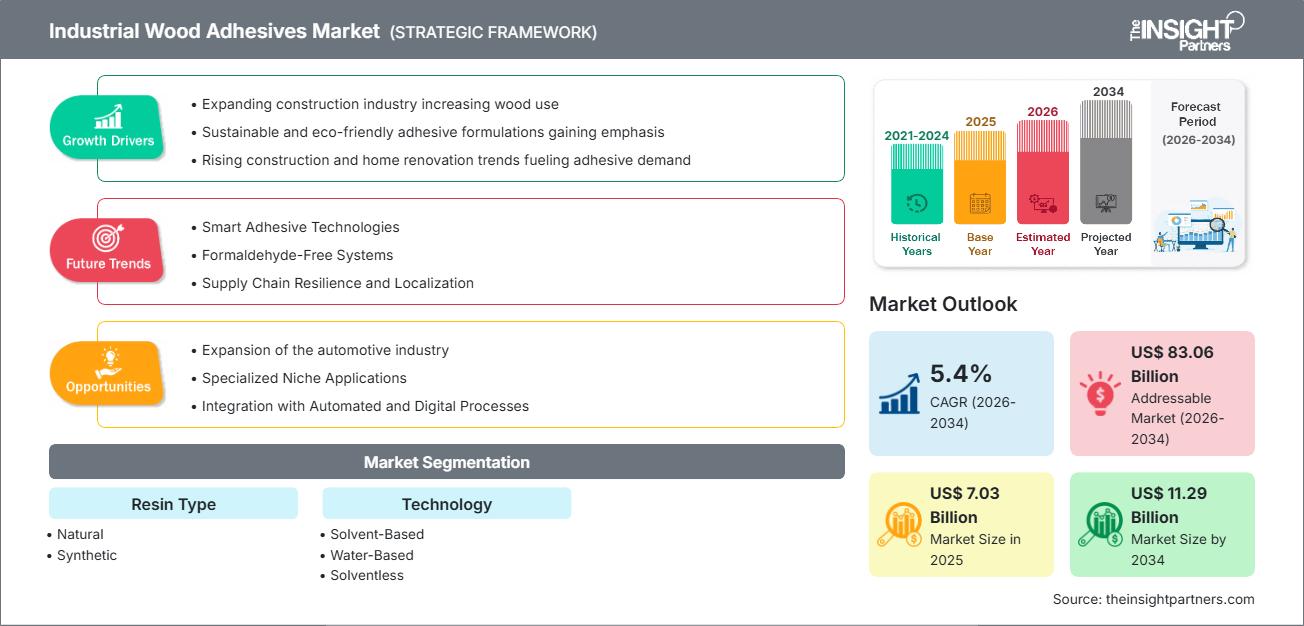

The global Industrial Wood Adhesives market size is projected to reach US$ 11.29 billion by 2034 from US$ 7.03 billion in 2025. The market is anticipated to register a CAGR of 5.4% during the forecast period 2026–2034. Key market dynamics include the rapid expansion of the global construction sector, a rising preference for engineered wood products like CLT and LVL, and an intensifying focus on sustainable, low-VOC (Volatile Organic Compound) bonding solutions. Additionally, the market is expected to benefit from the growth of the organized furniture retail sector, advancements in high-speed automated woodworking machinery, and the increasing replacement of traditional mechanical fasteners with high-performance chemical adhesives in modular housing applications.

Industrial Wood Adhesives Market Analysis

The industrial wood adhesives market analysis reveals a decisive pivot toward "green chemistry" as regulatory bodies tighten restrictions on formaldehyde emissions. To maintain market share, manufacturers must prioritize the development of bio-based resins and soy-derived bonding agents that satisfy stringent LEED and CARB II certifications. Strategic opportunities are emerging in the cross-laminated timber (CLT) segment, where the demand for structural integrity and moisture resistance offers a significant competitive edge to suppliers of polyurethane and emulsion polymer isocyanate (EPI) systems. The analysis further indicates that operational success depends on optimizing the open-time and press-cycle efficiency of adhesives to align with the high-throughput requirements of modern furniture factories. Producers should differentiate themselves by offering bespoke technical support and integrated application systems, transitioning from simple commodity suppliers to comprehensive bonding solution providers.

Industrial Wood Adhesives Market Overview

Industrial wood adhesives are evolving from a focus on basic bonding to the provision of specialized, high-performance structural interfaces. While historically dominated by urea-formaldehyde for cost-sensitive panel production, industrial wood adhesives are diversifying into advanced water-based and solventless technologies to meet evolving safety standards. Industrial wood adhesives serve a broad range of applications, including flooring, furniture, and structural timber, supported by both large-scale chemical conglomerates and specialized niche adhesive formulators. Increased urbanization and the "do-it-yourself" (DIY) trend in developed economies are fueling the demand for durable and easy-to-apply woodworking adhesives. While Europe and North America remain centers for technological innovation and high-standard compliance, the Asia-Pacific region has solidified its position as the global production hub for mass-market wood-based panels and furniture exports. For instance, the market in the US is characterized by a mature construction sector and a robust demand for sustainable building materials. Domestic manufacturers are increasingly adopting bio-based adhesives to align with strict environmental regulations. The rise in home renovation projects and the expansion of the prefabricated housing industry further stimulate the consumption of high-performance woodworking bonding solutions.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONIndustrial Wood Adhesives Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Industrial Wood Adhesives Market Drivers and Opportunities

Market Drivers:

- Growing Adoption of Engineered Wood in Sustainable Construction: The global construction industry is increasingly replacing traditional steel and concrete with engineered wood products like Cross-Laminated Timber (CLT) and Glulam to reduce carbon footprints. This shift acts as a primary driver because these structural wood components rely entirely on high-strength chemical bonding for stability, creating a massive and consistent demand for industrial-grade structural adhesives.

- Stricter Formaldehyde Emission Regulations: International regulatory bodies are enforcing much tighter limits on Volatile Organic Compound (VOC) emissions, particularly formaldehyde, to improve indoor air quality. This regulatory pressure is driving a market-wide transition from traditional urea-formaldehyde resins toward more advanced, "green" bonding solutions like water-based and soy-derived adhesives, forcing manufacturers to upgrade their product portfolios.

- Rapid Expansion of Organized Furniture Retail and Automation: The rise of large-scale, "ready-to-assemble" furniture manufacturing requires high-speed production lines to meet global consumer demand. This drives the market for fast-curing hot-melt and water-borne adhesives that can keep pace with automated machinery, allowing for immediate packaging and shipping without the long drying times associated with traditional glues.

Market Opportunities

- Development and Commercialization of Bio-Based Resins: There is a significant strategic opportunity to pioneer adhesives derived from natural sources like lignin, soy protein, and starch to meet the demand for carbon-neutral building materials. Companies that successfully scale these renewable bonding agents can capture the growing segment of eco-conscious developers and consumers who are willing to pay a premium for certified sustainable products.

- Advancement in Modular and Prefabricated Housing Technologies: As the construction industry moves toward off-site, modular manufacturing to save time and labor costs, there is a specialized opportunity for adhesives that offer rapid-set and high-vibration resistance. These adhesives are critical for ensuring that pre-built wood modules remain structurally sound during transport and assembly on-site.

- Expansion into High-Growth Emerging Economies: Markets across the Asia-Pacific and Middle East are undergoing massive infrastructure development and industrialization. Establishing local production facilities or strategic partnerships in these regions allows adhesive manufacturers to tap into high-volume manufacturing hubs where the demand for wood-based materials is surging due to new city-building initiatives.

Industrial Wood Adhesives Market Report Segmentation Analysis

The Industrial Wood Adhesives Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Resin Type:

- Natural: An emerging segment focused on sustainability, utilizing renewable sources to provide low-toxicity bonding solutions for eco-conscious markets.

- Synthetic: The primary volume contributor, encompassing a wide range of chemically formulated resins known for their high bonding strength, durability, and cost-effectiveness across industrial scales.

By Technology:

- Water-Based: The leading technology segment, favored for its low VOC profile, ease of cleaning, and compliance with modern safety and environmental standards.

- Solvent-Based: Utilized for specific heavy-duty applications requiring rapid drying and high resistance to extreme environmental conditions, despite increasing regulatory scrutiny.

- Solventless: A high-growth segment including hot-melts and 100% solids, offering efficiency gains in automated manufacturing processes and reduced environmental impact.

- Others: Includes specialized technologies such as radiation-cured and hybrid systems designed for niche high-performance woodworking applications.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Industrial Wood Adhesives Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 7.03 Billion |

| Market Size by 2034 | US$ 11.29 Billion |

| Global CAGR (2026 - 2034) | 5.4% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Resin Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Industrial Wood Adhesives Market Players Density: Understanding Its Impact on Business Dynamics

The Industrial Wood Adhesives Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industrial Wood Adhesives Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium adhesive producers and industrial woodworking manufacturers to expand.

The industrial wood adhesives market is undergoing a significant transformation, moving from traditional resin formulations to high-performance, sustainable bonding systems. Growth is driven by the global surge in engineered wood construction, a rising demand for low-emission furniture, and the expansion of automated woodworking industries. Below is a summary of market share and trends by region:

North America

- Market Share: Holds a significant share of the global market supported by a resurgence in residential construction and advanced manufacturing.

- Key Drivers:

- Strong demand for formaldehyde-free and soy-based adhesives to comply with strict indoor air quality standards.

- Increasing adoption of Mass Timber and Cross-Laminated Timber (CLT) in commercial building projects.

- Robust DIY and home renovation culture driving retail consumption of high-performance wood glues.

- Trends: Strategic shift toward bio-based polyurethane systems and the mainstreaming of "green" building certifications like LEED in the woodworking sector.

Europe

- Market Share: Represents a dominant portion of the global market, anchored by high-standard furniture clusters in Germany, Italy, and Scandinavia.

- Key Drivers:

- Stringent E0 and REACH regulations mandate the use of low-toxicity and sustainable bonding agents.

- Highly developed engineered wood industry specializing in structural Glulam and high-end cabinetry.

- Strong government backing for circular economy initiatives and bio-refinery-sourced raw materials.

- Trends: Consolidation of market players and a focus on "intelligent" adhesives that facilitate the easy disassembly and recycling of wooden components.

Asia-Pacific

- Market Share: The largest and fastest-growing region, acting as the global hub for plywood, panel, and furniture exports.

- Key Drivers:

- Massive infrastructure development and urban housing schemes in China, India, and Southeast Asia.

- Rapid industrialization and the presence of cost-effective manufacturing bases for global furniture brands.

- Government-supported shifts toward higher-value woodworking to meet international export safety standards.

- Trends: Heavy investment in automated production lines and an increasing transition from low-cost urea resins to premium water-based and hot-melt technologies.

South and Central America

- Market Share: An emerging market with a growing industrial woodworking sector in countries like Brazil, Argentina, and Chile.

- Key Drivers:

- Expansion of the regional forestry and pulp industries into value-added wood products.

- Rising middle-class disposable income is leading to a preference for modern, aesthetically pleasing interior furnishings.

- Modernization of small-to-medium woodworking enterprises into commercial-grade production facilities.

- Trends: Growth of boutique furniture brands and the gradual implementation of sustainable forest management certifications that influence adhesive selection.

Middle East and Africa

- Market Share: A developing market with significant potential, transitioning from traditional joinery to formalized industrial production.

- Key Drivers:

- High demand for durable and heat-resistant adhesives suited for the extreme climatic conditions of the region.

- Large-scale "Smart City" and luxury hospitality projects in the GCC countries (e.g., Saudi Arabia and the UAE).

- Strategic efforts to reduce import dependency by establishing local chemical and resin manufacturing units.

- Trends: Implementation of modern cooling and application technologies to manage adhesive performance in arid environments, coupled with a focus on high-strength bonds for heavy-duty structural applications.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as H.B.Fuller Company, Henkel AG & Company KGAA, Ashland, Arkema Group, Sika AG, Pidilite Industries Ltd, Jubilant Industries Ltd, Dow, Inc., and 3M also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Premiumization and Sustainable Branding: Positioning adhesives as essential for high-performance, eco-friendly construction by emphasizing low VOC emissions, bio-based resin origins, and compliance with stringent environmental certifications.

- Specialized Product Portfolios: Industrial wood adhesives now extend beyond basic resins to include moisture-activated systems for marine wood, micro-emission hot melts for interior edge banding, and high-strength fire-rated solutions for cross-laminated timber (CLT).

- Technological Integration and R&D: Companies are managing the entire innovation chain, from proprietary synthetic resin development to the creation of "smart" application tools. This ensures precision in industrial settings, reduces material waste, and meets ethical, clean-label production standards.

- Advanced Processing for Circularity: New formulation technologies, such as bio-filler blending and moisture-resistant polymer chemistry, help create durable wood products that support sustainable building practices and enable easier disassembly for recycling.

Opportunities and Strategic Moves

- Partner with High-Volume Furniture Hubs and Automation Providers: Tap into the surging demand for fast-curing, machine-ready adhesives by forming strategic alliances with large-scale furniture exporters and robotic assembly plants in the Asia-Pacific and North American markets.

- Incorporate Bio-Based Chemistry and Low-Emission Standards: Adopt renewable carbon-content certifications and lifecycle assessments to appeal to environmentally conscious builders and government-led infrastructure projects seeking green building credits.

Major Companies operating in the Industrial Wood Adhesives Market are:

- H.B.Fuller Company

- Henkel AG & Company KGAA

- Ashland

- Arkema Group

- Sika AG

- Pidilite Industries Ltd

- Jubilant Industries Ltd

- Dow, Inc.

- 3M

Disclaimer: The companies listed above are not ranked in any particular order.

Industrial Wood Adhesives Market News and Recent Developments

- In January 2025, Kiilto introduced a new line of Industrial Wood Adhesives, providing a comprehensive range of technical solutions specifically designed for the engineered wood industry. The Kiilto Pro SW line was engineered for high-performance applications that required exceptional strength and quality capable of withstanding decades of intensive use.

- In December 2024, Arkema finalized the acquisition of Dow's flexible packaging laminating adhesives business, a leading global producer that generated annual sales of approximately US$ 250 million. This strategic operation significantly expanded Arkema's portfolio of Industrial Wood Adhesives and specialty solutions, positioning the Group as a dominant player in the high-growth flexible packaging and industrial lamination markets.

Industrial Wood Adhesives Market Report Coverage and Deliverables

The "Industrial Wood Adhesives Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Industrial Wood Adhesives Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Industrial Wood Adhesives Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Industrial Wood Adhesives Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Industrial Wood Adhesives Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For