区域供热市场趋势、需求及2034年增长情况

区域供热市场规模及预测(2021-2034 年)、全球及区域份额、趋势及增长机会分析报告涵盖范围:按热源(煤炭、天然气、石油及石油产品等)、电厂类型(锅炉、热电联产 (CHP) 等)、应用(住宅、商业和工业)以及地理区域(北美、欧洲、亚太、中东和非洲以及南美和中美洲)划分。

- 状态 : 已发布

- 报告代码 : TIPRE00007183

- 类别 : 能源和电力

- 页数 : 248

- 可用报告格式 :

- 最后更新日期 : April 27, 2026

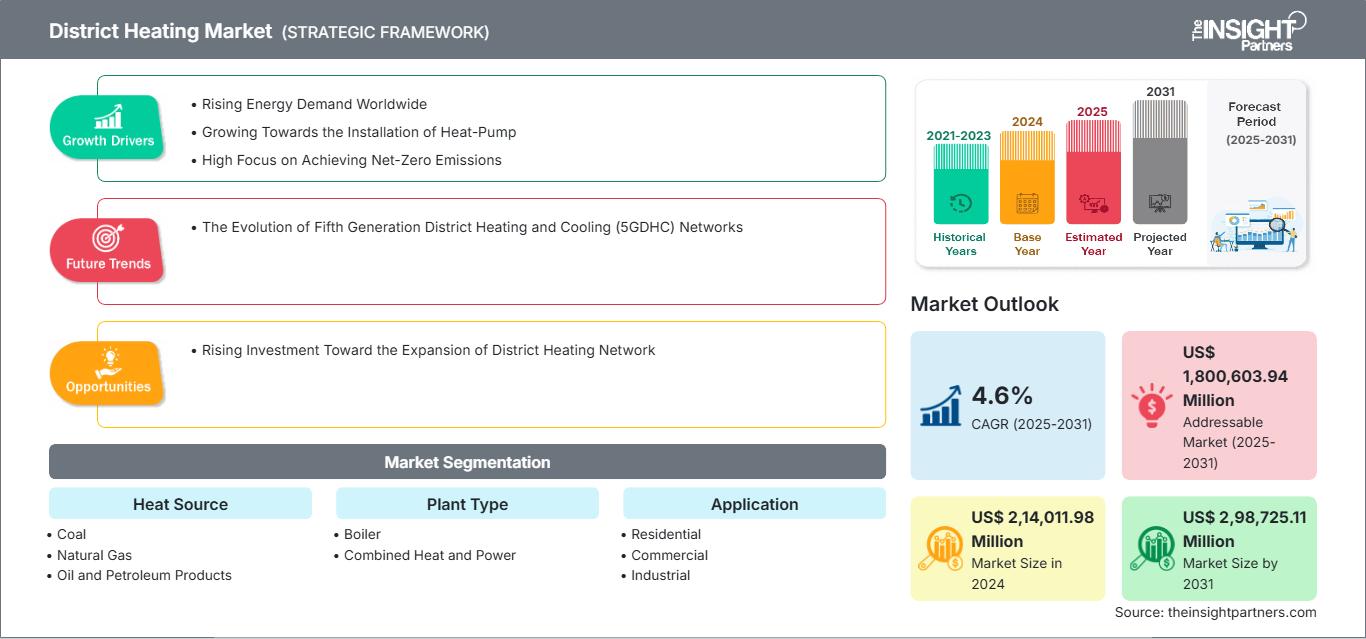

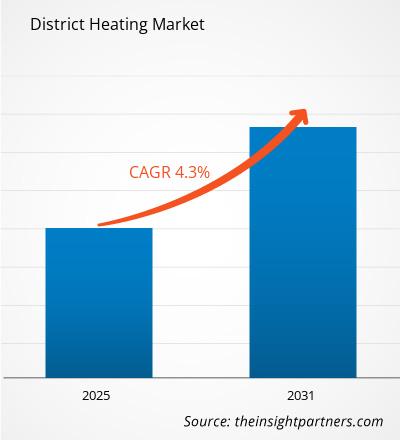

预计到2034年,区域供热市场规模将从2025年的2275.4亿美元增长至3343.3亿美元。预计2026年至2034年期间,该市场将以4.37%的复合年增长率增长。

区域供热市场分析

由于城市化进程加快、节能项目增多以及为提高可持续性和效率而利用生物能源、太阳能和地热能等可再生资源,区域供热市场正经历强劲扩张。智能电表在最大限度地提高区域供热系统的配热效率方面发挥着重要作用。

区域供热市场概览

市场对集中式、高效供暖解决方案的需求日益增长。环保能源的普及、技术的进步以及扶持政策的出台,都推动了住宅、商业和工业领域的这一需求。

市场调研亮点

- 2024年,欧洲以48.9%的市场份额占据主导地位。

- 亚太地区预计在预测期内将以 6.1% 的复合年增长率增长。

- 预计美国市场在预测期内将以 5.1% 的复合年增长率增长。

- 按热源划分,天然气细分市场在 2024 年占据了最大的市场份额,达到 51.8%。

- 按植物类型划分,预计“其他”类别将实现最快增长,在预测期内复合年增长率将达到 7.8%。

- 按应用领域划分,住宅领域在 2024 年占据了最大的市场份额,达到 51.2%。

- 该报告重点介绍了西门子股份公司、威立雅、ENGIE、丹佛斯、富腾公司、Statkraft AS、Vattenfall AB、LOGSTOR Denmark Holding ApS、Shinryo Corporation、Vital Energi Ltd 等主要行业参与者,同时分析了可能重塑未来市场的新理念、颠覆性产品和创新服务的关键发展,并揭示了整个行业的新兴主题。

根据您的需求定制此报告

获取免费定制服务区域供热市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

区域供热市场驱动因素和机遇

市场驱动因素:

- 城市化进程加快:城市人口快速增长,推动了集中供暖的需求,为多栋建筑提供能源分配,降低基础设施成本,提高服务可靠性。

- 对能源效率的需求日益增长:与独立系统相比,区域供热可最大限度地减少能源损失,优化燃料利用并降低运营成本。

- 可再生能源整合:将生物质能、地热能和太阳能纳入区域供热网络,可以促进可持续发展,减少碳排放,并支持政府的气候目标。

- 政府政策:支持性法规、补贴和碳减排指令激励区域供热的普及,鼓励在城市和工业区进行投资和扩张。

市场机遇:

- 智能计量:实施先进的传感器和智能电表可以实现精确的能源管理,减少浪费,并进行预测性维护。

- 工业应用:工厂、加工厂和商业综合体可以利用区域供热获得可靠、经济高效的能源,从而将市场扩展到住宅领域之外。

- 住宅扩张:公寓和住宅小区建设的增加为部署集中供暖系统创造了机会,从而提供持续的舒适性和节能效果。

- 脱碳目标:全球日益重视减少温室气体排放,这鼓励采用低碳区域供热,从而吸引投资和创新技术解决方案。

区域供热市场报告细分分析

为了解区域供热市场的结构、增长前景和新兴趋势,可将其划分为不同的细分市场。以下是行业报告中常用的标准细分方法:

按热源分类:

- 煤炭:燃煤系统提供稳定的热能供应,常用于煤炭资源丰富的地区,支持大规模集中供热网络。

- 天然气:天然气系统提供更清洁、高效、灵活的供热方式,由于排放量低、燃料易于获取,因此得到广泛应用。

- 石油和石油产品:石油和石油燃料发电厂在其他燃料稀缺的地方提供可靠的供暖,以稳定的输出支持工业和住宅应用。

- 其他:生物质能、太阳能和地热能等可再生和替代燃料有助于实现可持续的低碳区域供热解决方案。

按植物类型:

- 锅炉:传统锅炉设备通过燃烧燃料产生热量,从而产生蒸汽或热水,并通过区域供热网络进行分配。

- 热电联产(CHP):热电联产装置同时产生电力和热能,最大限度地提高能源效率并降低燃料消耗。

- 其他:包括电加热器、地热发电厂和混合配置在内的创新系统,提供了灵活且可持续的供热选择。

按申请方式:

- 住宅

- 商业的

- 工业的

按地理位置:

- 北美

- 欧洲

- 亚太地区

- 南美洲和中美洲

- 中东和非洲

区域供热市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2025年市场规模 | 2275.4亿美元 |

| 到2034年市场规模 | 3343.3亿美元 |

| 全球复合年增长率(2026-2034 年) | 4.37% |

| 史料 | 2021-2024 |

| 预测期 | 2026-2034 |

| 涵盖部分 |

按热源

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

区域供热市场参与者密度:了解其对业务动态的影响

区域供热市场正快速增长,这主要得益于终端用户需求的不断增长,而终端用户需求的增长又源于消费者偏好的转变、技术的进步以及消费者对产品优势认知的提高。随着需求的增长,企业不断拓展产品和服务,持续创新以满足消费者需求,并把握新兴趋势,这些都进一步推动了市场增长。

按地域划分的区域供热市场份额分析

亚太地区区域供热市场正经历快速增长,其主要驱动力包括城市化、工业化、政府激励措施、可再生能源的普及、节能举措以及对集中供热解决方案日益增长的需求。此外,智能计量技术的进步、住宅和商业基础设施的扩建、低碳和可再生热源的整合以及对可持续能源项目投资的增加,也进一步推动了市场增长。

由于城市化率、能源政策、燃料供应、基础设施建设、政府激励措施、气候条件以及可再生供热技术的应用等方面的差异,各地区的区域供热市场增长情况不尽相同。以下是各地区市场份额和发展趋势的概述:

1. 北美洲

- 市场份额:占据全球市场相当大的份额

-

关键驱动因素:

- 政府激励措施:联邦和州政府项目为低碳供热项目提供补贴和税收优惠,促进对区域供热基础设施的投资,并加速城市和工业部门采用可持续能源解决方案。

- 采用节能供暖

- 城市化进程加快

- 趋势:可再生能源的整合和智能计量。

2. 欧洲

- 市场份额:由于欧盟早期出台的严格法规,占据了相当大的份额。

-

关键驱动因素:

- 可再生能源整合:利用生物质能、太阳能和地热能可以减少排放、降低燃料成本,并促进可持续的区域供热解决方案。

- 政府政策

- 能源效率目标。

- 趋势:热电联产 (CHP) 电厂的扩张提高了能源效率,同时减少了对城市环境的影响。

3. 亚太地区

- 市场份额:增长最快的地区,占据主导市场份额

-

关键驱动因素:

- 快速城市化:城市人口不断增长,推动了对集中供暖系统的需求,以满足住宅区、商业区和工业区的需求。

- 工业增长

- 政府激励措施

- 趋势:智能供暖系统和可再生热源的采用率正在上升,提高了亚太地区的能源效率并减少了碳足迹。

4. 中东和非洲

- 市场份额:虽然规模较小,但增长迅速。

-

关键驱动因素:

- 可再生资源可用性:丰富的当地生物质、地热和太阳能资源能够以经济高效的方式为区域供热网络生产低碳热能。

- 技术进步

- 政府支持与政策

- 趋势:混合区域供热系统结合传统燃料和可再生能源。

5. 南美洲和中美洲

- 市场份额:市场稳步增长

-

关键驱动因素:

- 能源效率举措:政策和技术优化热能产生和分配,最大限度地减少能源损失,降低城市和工业环境中的运营成本。

- 基础设施开发

- 对可持续能源的投资

- 趋势:区域供热项目整合了生物质能和其他可再生能源,支持可持续发展目标,并降低城市地区的运营成本。

市场密度高,竞争激烈

由于丹佛斯公司、威立雅公司、富腾公司、ENGIE公司、LOGSTOR丹麦控股公司、西门子公司、Statkraft公司、Vattenfall公司、新凌株式会社和Vital Energi有限公司等全球主要企业的参与,竞争非常激烈。

激烈的竞争促使企业通过提供以下服务来脱颖而出:

- 创新技术解决方案

- 可持续能源一体化

- 定制服务

- 成本效益

- 性能可靠。

机遇与战略举措

- 拓展至新兴市场——瞄准城市化和工业化程度不断提高的地区,进行新的安装。

- 可再生能源整合——利用生物质能、太阳能和地热能提供可持续的供暖解决方案。

主要参与者名单

- 丹佛斯公司

- 威立雅

- 富腾公司

- ENGIE

- LOGSTOR 丹麦控股有限公司

- 西门子股份公司

- Statkraft AS

- Vattenfall AB

- 新菱株式会社

- 维塔尔能源有限公司

免责声明:以上列出的公司不分先后顺序。

研究过程中分析的其他公司包括:

- 阿法拉伐

- 达尔能源

- FVB能源公司

- 通用电气公司

- 海伦

- 兰博集团

- Uniper SE

- 莱茵集团

- NIBE Industrier AB

- 亿安集团

- Enwave能源公司。

区域供热市场新闻及最新动态

- 2025年3月,富腾集团同意支持芬兰技术的发展——富腾集团同意利用其模拟技术专长,支持芬兰技术公司Steady Energy的区域供热核反应堆的开发。目标是使用Apros软件为Steady Energy的LDR-50反应堆创建数字孪生模型。

- 威立雅集团于2024年10月宣布将在伦敦建设一个新的区域供热网络。作为欧洲领先的本地脱碳能源企业,威立雅宣布将与南华克区议会合作,在伦敦建设一个新的区域供热网络,该网络将利用集团旗下的SELCHP能源回收设施(ERF)提供的热能。该网络每年可利用处理不可回收垃圾的发电过程中产生的75吉瓦时低碳热能,为11个社会住房项目和学校的近5000户家庭供热。该项目旨在未来15年内满足新增2万套住房的供热需求,符合南华克区议会的区域行动计划。

区域供热市场报告涵盖范围及成果

《区域供热市场规模及预测(2021-2034)》报告对市场进行了详细分析,涵盖以下领域:

- 本报告涵盖全球、区域和国家层面的区域供热市场规模及预测,包括所有关键细分市场。

- 区域供热市场趋势,以及驱动因素、制约因素和关键机遇等动态因素。

- 详细的PEST和SWOT分析

- 区域供热市场分析,涵盖关键趋势、全球和区域框架、主要参与者、法规和最新发展

- 区域供热市场行业格局及竞争分析,涵盖市场集中度、热力图分析、主要参与者及最新发展动态

- 公司详细概况

Nivedita 是一位经验丰富的研究专业人士,在市场研究和商业咨询领域拥有超过 9 年的经验。她目前担任 The Insight Partners 的 ICT 领域项目经理,在管理和执行跨技术领域的联合研究、定制研究、订阅研究和咨询研究方面拥有深厚的专业知识。

Nivedita 在提供数据驱动的分析和切实可行的洞察方面拥有丰富的经验,并已成为多个关键项目的关键贡献者。她的工作涉及端到端的项目执行——从理解客户目标、分析市场趋势到制定战略建议。她与领先的 ICT 公司广泛合作,帮助他们识别市场机遇并引领行业变革。

Nivedita 拥有德拉敦 IMS 的管理学 MBA 学位。在加入 The Insight Partners 之前,她在浦那的 MarketsandMarkets 和 Future Market Insights 积累了宝贵的经验,担任过各种研究职位,并在行业分析和客户互动方面奠定了坚实的基础。

- 全面的市场规模与预测分析

- 详细的细分市场分析

- 深入的市场动态评估

- 区域及国家级洞察

- 竞争格局与企业对标分析

- 战略性商业情报

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势