تقرير سوق الدفع الرقمي 2028 حسب القطاعات والجغرافيا والديناميكيات والتطورات الأخيرة والرؤى الإستراتيجية

البيانات التاريخية : 2019-2020 | سنة الأساس : 2021 | فترة التنبؤ : 2022-2028توقعات سوق المدفوعات الرقمية حتى عام 2028 - تأثير جائحة كوفيد-19 والتحليل العالمي حسب المكونات (الحلول والخدمات)، والنشر (محليًا وسحابيًا)، وحجم المؤسسة (الشركات الصغيرة والمتوسطة والكبيرة)، والقطاعات (الخدمات المصرفية والمالية والتأمين، وتجارة التجزئة والتجارة الإلكترونية، والرعاية الصحية، والسفر والضيافة، والإعلام والترفيه، وتكنولوجيا المعلومات والاتصالات، وغيرها)

- تاريخ التقرير : Jan 2022

- رمز التقرير : TIPRE00007577

- الفئة : الخدمات المصرفية والخدمات المالية والتأمين

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 225

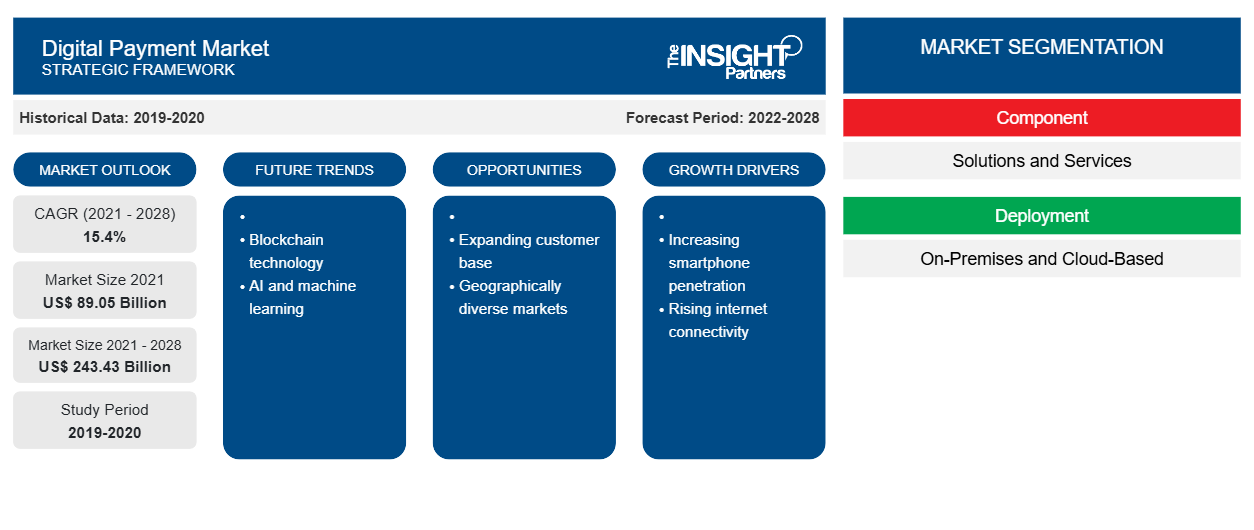

من المتوقع أن ينمو سوق الدفع الرقمي من 89,045.67 مليون دولار أمريكي في عام 2021 إلى 243,426.71 مليون دولار أمريكي بحلول عام 2028؛ ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 15.4٪ من عام 2021 إلى عام 2028.

من المتوقع أن ينمو سوق الدفع الرقمي العالمي خلال فترة التنبؤ بسبب الانتشار المتزايد للهواتف الذكية مما يتيح توسيع التجارة عبر الهاتف المحمول. إن الطريقة التي يصل بها الأشخاص إلى الإنترنت لها تأثير مباشر على نمو التجارة عبر الهاتف المحمول . يفضل المستخدمون الهواتف الذكية على أجهزة الكمبيوتر الشخصية لتصفح الإنترنت حيث أصبحت الهواتف الذكية أكثر بأسعار معقولة، ولم يعد الإنترنت عالي السرعة بنية تحتية متميزة في العديد من البلدان. يطور تجار التجزئة تطبيقات التسوق التي تحتوي على كتالوجات سهلة التصفح وتجربة دفع بسيطة. لا يغفل المصرفيون ومقدمو خدمات الدفع حقيقة أن العملاء مرتبطون جوهريًا بهواتفهم المحمولة. توفر البنوك تطبيقات مصرفية تسمح بإكمال المعاملات على شاشة الجهاز المحمول. كما غيرت التجارة عبر الهاتف المحمول طريقة عمل الشركات التقليدية، خاصة فيما يتعلق بقبول المدفوعات غير النقدية. علاوة على ذلك، يتلاشى الاختلاف بين التجارة المادية والرقمية، وتتقارب القنوات بشكل متزايد. تحولت تجربة الشراء داخل المتجر بشكل كبير إلى تجربة الشراء عبر الإنترنت بسبب التركيز القوي على المدفوعات غير التلامسية أثناء جائحة كوفيد-19. كما كانت المدفوعات غير التلامسية راسخة بالفعل في عدد قليل من المناطق قبل الجائحة. وتنتشر المدفوعات غير التلامسية و/أو التعريف البيومتري في تجربة الشراء عبر الإنترنت. وتُعَد البطاقة غير التلامسية النوع الأكثر انتشارًا للدفع غير التلامسي. ومن ناحية أخرى، تكتسب المدفوعات عبر الهاتف المحمول شعبية بسبب سهولة الاستخدام والشعبية المتزايدة لحلول الدفع من الشركات المصنعة للمعدات الأصلية (OEM) كطريقة دفع للبيع بالتجزئة. وفي عدد قليل من البلدان، تطلب تجار التجزئة والحكومات بشكل استباقي من العملاء زيادة المدفوعات غير التلامسية وتشجع تجار التجزئة على جعل ذلك ممكنًا. وقد زادت العديد من البنوك حدود الدفع غير التلامسية لتقليل الحاجة إلى لوحة اللمس أو النقود عند نقطة البيع. وكل هذه العوامل تدفع نمو سوق الدفع الرقمي.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الدفع الرقمي: رؤى استراتيجية

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تأثير جائحة كوفيد-19 على سوق الدفع الرقمي

لقد استفاد سوق الدفع الرقمي من جائحة كوفيد-19. تواجه الشركات تحديات جديدة بسبب الجائحة وتطوير بيئات العمل عن بعد. وفقًا لمسح أجراه البنك الدولي حول الاستجابات السياسية للجائحة، تبنت 58 حكومة على الأقل في البلدان النامية المدفوعات الرقمية لتقديم المساعدة في مواجهة كوفيد-19. تلقت 36 دولة على الأقل الأموال في حسابات تعمل بكامل طاقتها والتي يمكن استخدامها للادخار أو المعاملات بالإضافة إلى سحب النقود. يتطلب الشمول المالي مثل هذه القدرة الواسعة. علاوة على ذلك، أدى ظهور الوباء في عام 2020 إلى ظهور مجموعة من التحديات لعمليات السوق العالمية. انهارت البنى التحتية للرعاية الصحية في الاقتصادات المتقدمة بسبب العدد المتزايد من حالات كوفيد-19. ونتيجة لذلك، ستتطلب حالة الطوارئ الصحية العامة من الحكومات واللاعبين في السوق التدخل والمساعدة في إحياء عمليات السوق والإيرادات من خلال الجهود التعاونية لمبادرات البحث والتطوير لاسترداد الخسائر خلال فترة التنبؤ. بالإضافة إلى ذلك، تبشر الاستثمارات المتزايدة بالخير لسوق الدفع الرقمي في السنوات التالية.

رؤى سوق الدفع الرقمي

اعتماد متزايد على واجهات برمجة التطبيقات للخدمات المصرفية المفتوحة

تدرك شركات الخدمات المالية أهمية مبادرات الخدمات المصرفية المفتوحة وواجهات برمجة التطبيقات . تدرك البنوك التقليدية أنها يجب أن تعمل على تحسين قدراتها الرقمية للتنافس في القطاع وتجنب الاستبعاد من قبل الوافدين الجدد الذين يقدمون عروضًا وخدمات متفوقة. على سبيل المثال، تدعم العديد من شركات الخدمات المالية مثل PayPal وWells Fargo وVisa مشاريع الخدمات المصرفية المفتوحة. أيضًا، في أوروبا، أصبحت مبادرات الخدمات المصرفية المفتوحة هي القاعدة بشكل تدريجي لأن البنوك ملزمة قانونًا بإتاحة معلومات الحساب عبر واجهات برمجة التطبيقات بموجب توجيه خدمات الدفع المنقح (PSD2)، والذي دخل حيز التنفيذ اعتبارًا من عام 2018. تعمل واجهات برمجة تطبيقات الخدمات المصرفية المفتوحة على تعزيز جاذبية البنك وتمكنه من تلبية التوقعات المتغيرة للعملاء الحاليين وجذب عملاء جدد. يمكن أيضًا استخدام واجهات برمجة التطبيقات كحل فريد من نوعه لتعزيز تفاعل العملاء والاستجابة لمتطلبات المستهلكين بطريقة آمنة ورشيقة ومستقبلية. تُعد واجهات برمجة تطبيقات الخدمات المصرفية المفتوحة أصولًا مهمة لمؤسسات الخدمات المالية لأنها تسمح لها بتوسيع عروض الخدمة وتعزيز التفاعل مع العملاء وإنشاء قنوات دخل رقمية جديدة، مما يوفر فرصة كبيرة لسوق الدفع الرقمي للتوسع خلال الفترة المتوقعة

رؤى حول قطاع النشر

بناءً على النشر، ينقسم سوق الدفع الرقمي إلى محلي ومستند إلى السحابة. قاد القطاع المستند إلى السحابة السوق في عام 2020. يوفر النشر المستند إلى السحابة أمانًا مدمجًا للبيانات وقابلية للتوسع عند الطلب والقدرة على أداء أنشطة حوسبة مكثفة بسرعة. تعد السحابة ممكّنًا مهمًا للمحافظ الرقمية. مع انتشار المحافظ الرقمية، قد تعمل هذه الفوائد على تحسين الوظائف الحالية بشكل كبير بل وتؤدي حتى إلى ابتكارات جديدة. يزيل استخدام التخزين الافتراضي عن بُعد الحاجة إلى الخوادم المادية، مما يقلل من خطر الانقطاع والكوارث. توفر السحابة أيضًا حماية قوية للأمن السيبراني ويمكنها تلبية المعايير التنظيمية الحاسمة، مثل معيار أمان بيانات صناعة بطاقات الدفع (PCI DSS)، وهو أمر مهم بشكل خاص في صناعة الخدمات المالية.

رؤى حول حجم قطاع المنظمة

بناءً على حجم المنظمة، ينقسم سوق الدفع الرقمي إلى شركات كبيرة وصغيرة الحجم. قاد قطاع الشركات الكبيرة السوق في عام 2020 ومن المتوقع أن يهيمن على السوق خلال فترة التوقعات. حتى عندما يتعلق الأمر بأنظمة الدفع، فإن التبني التكنولوجي أمر بالغ الأهمية للحد من التكرار. ومع ذلك، بالنسبة للمؤسسات الأكبر حجمًا، لن ينجح حل واحد يناسب الجميع. إن ظهور العملات الرقمية للبنوك المركزية (CBDCs) وزيادة التبني الواسع النطاق للعملات المشفرة في أنظمة الدفع التقليدية من شأنه أن يجبر العديد من الشركات الكبيرة على تضمين العملات الرقمية في تطبيقاتها في السنوات القادمة. ستستخدم هذه الشركات العملات الرقمية في المقام الأول للدفع، كمخزن للقيمة، والاستفادة من الاستثمارات ذات العائد المرتفع المقدمة في تطبيقات التمويل اللامركزي (DeFi). على سبيل المثال، توفر PayG حلول دفع مخصصة للشركات الكبرى وتساعدها في تحسين طرق التحصيل الخاصة بها. إنها تسمح للشركات الكبيرة بتتبع تدفقاتها النقدية الداخلة والخارجة وتمكنها من التوسع عندما تحتاج إلى ذلك، دون إدخال أي عمليات، وهو ما يدفع نمو سوق الدفع الرقمي

رؤى حول قطاعات أنواع المكونات

بناءً على التطبيق، ينقسم سوق الدفع الرقمي إلى حلول وخدمات. قاد قطاع الحلول السوق في عام 2020. يمكن للبنوك والمعالجات وشركات الاتصالات والتجار استخدام أنظمة الدفع الرقمية لإجراء مدفوعات رقمية بسلاسة ووفقًا لمعايير الدفع الدولية. يتضمن الحل منصة تتحكم في دورة حياة البطاقات الرقمية. تشرف على عملية التسجيل بأكملها، بالإضافة إلى توفير وإدارة بيانات الاعتماد. يمكن للمصدرين ومقدمي الخدمات استخدام المنصة لتقديم خدماتهم في محافظهم الخاصة أو محافظ الطرف الثالث، مما يغذي نمو السوق. ينقسم سوق الدفع الرقمي العالمي لقطاع الحلول إلى بوابة الدفع ومعالجة الدفع وأمان الدفع وإدارة الاحتيال وغيرها.

يركز لاعبو سوق الدفع الرقمي على ابتكارات وتطويرات المنتجات الجديدة من خلال دمج التقنيات والميزات المتقدمة للتنافس. على سبيل المثال، في يناير 2021، أعلنت Okay وFSS Technologies (البرمجيات والأنظمة المالية)، وهي شركة عالمية لتكنولوجيا المدفوعات، عن تحالفهما لتقديم أمان مصادقة مركّز لمدفوعات المستهلكين، وخاصة التحقق من صحة المعاملات والمصادقة على الهاتف المحمول. من خلال منتجاتها وتقنياتها وعروض الحلول من الجيل التالي، تعمل FSS بالفعل على توسيع إمكاناتها التجارية في أوروبا. في مايو 2020، اشترت Fiserv, Inc. شركة Inlet, LLC ("Inlet")، وهي مورد لحلول التسليم الرقمي الآمنة للفواتير والبيانات للمؤسسات والجهات المرخصة في السوق المتوسطة. يشمل قطاع المدفوعات شركة Inlet، التي تعمل على تعزيز استراتيجية دفع الفواتير الرقمية للشركة.

رؤى إقليمية حول سوق الدفع الرقمي

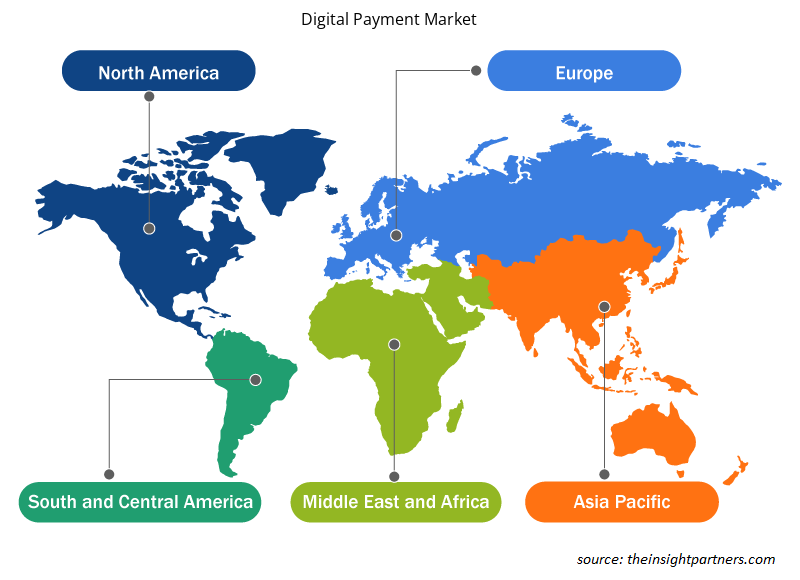

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الدفع الرقمي طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الدفع الرقمي والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الدفع الرقمي

نطاق تقرير سوق الدفع الرقمي

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2021 | 89.05 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 243.43 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2021 - 2028) | 15.4% |

| البيانات التاريخية | 2019-2020 |

| فترة التنبؤ | 2022-2028 |

| القطاعات المغطاة | حسب المكون

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

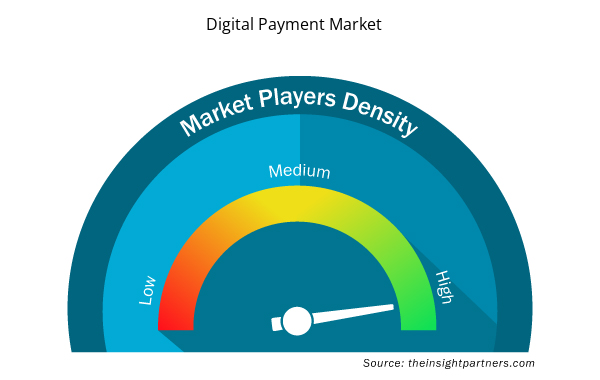

كثافة اللاعبين في سوق الدفع الرقمي: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الدفع الرقمي نموًا سريعًا، مدفوعًا بالطلب المتزايد من جانب المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الدفع الرقمي هي:

- ايه سي اي العالمية المحدودة

- أدين

- شركة البرمجيات والأنظمة المالية المحدودة

- شركة فيسيرف

- شركة المدفوعات العالمية المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الدفع الرقمي

سوق الدفع الرقمي – نبذة عن الشركة

- ايه سي اي العالمية المحدودة

- آدين

- شركة البرمجيات والأنظمة المالية المحدودة

- شركة فيسيرف

- شركة المدفوعات العالمية

- مجموعة نوفاتي المحدودة

- شركة باي بال القابضة

- شركة باي سيف المحدودة

- بلوك، المحدودة

- باي يو

أنكيتا خبيرة ديناميكية في أبحاث السوق والاستشارات، تتمتع بخبرة تزيد عن 8 سنوات في قطاعات التكنولوجيا والإعلام وتكنولوجيا المعلومات والاتصالات والإلكترونيات وأشباه الموصلات. وقد قادت ونفذت بنجاح أكثر من 100 مهمة استشارية وبحثية لعملاء عالميين مثل مايكروسوفت وأوراكل وشركة NEC وSAP وKPMG وExpeditors International. تشمل كفاءاتها الأساسية تقييم السوق، وتحليل البيانات، والتنبؤ، وصياغة الاستراتيجيات، والاستخبارات التنافسية، وكتابة التقارير.

أنكيتا بارعة في إدارة دورات المشاريع الكاملة، بدءًا من تصميم عروض ما قبل البيع ومناقشات العملاء، وصولًا إلى تقديم رؤى عملية بعد البيع. كما أنها ماهرة في إدارة فرق متعددة الوظائف، وهيكلة وحدات بحثية معقدة، ومواءمة الحلول مع أهداف العمل الخاصة بالعملاء. وقد مكنتها مهاراتها الممتازة في التواصل والقيادة والعرض التقديمي من تحقيق نتائج قيّمة باستمرار في بيئات سوقية سريعة التطور.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق الدفع الرقمي

احصل على عينة مجانية ل - سوق الدفع الرقمي