Marktgröße, Marktanteil und Prognose für Cloud-Sicherheit bis 2034

Marktgröße und Prognose für Cloud-Sicherheit (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Servicemodell [Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS) und Infrastructure-as-a-Service (IaaS)], Bereitstellungsmodell (öffentliche Cloud, private Cloud und Hybrid-Cloud), Unternehmensgröße (Großunternehmen und kleine und mittlere Unternehmen), Lösungstyp (E-Mail- und Websicherheit, Cloud-Identitäts- und Zugriffsmanagement, Verhinderung von Datenverlust, Intrusion Detection System/Intrusion Prevention System, Security Information & Event Management und Sonstige) und Branchen [Banken, Finanzdienstleistungen und Versicherungen (BFSI); IT und Telekommunikation; Energie und Versorgung; Regierung und öffentlicher Sektor; Gesundheitswesen; Fertigung; und Sonstige].

- Status : Veröffentlichte Daten

- Berichtscode : TIPTE100000306

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : March 17, 2026

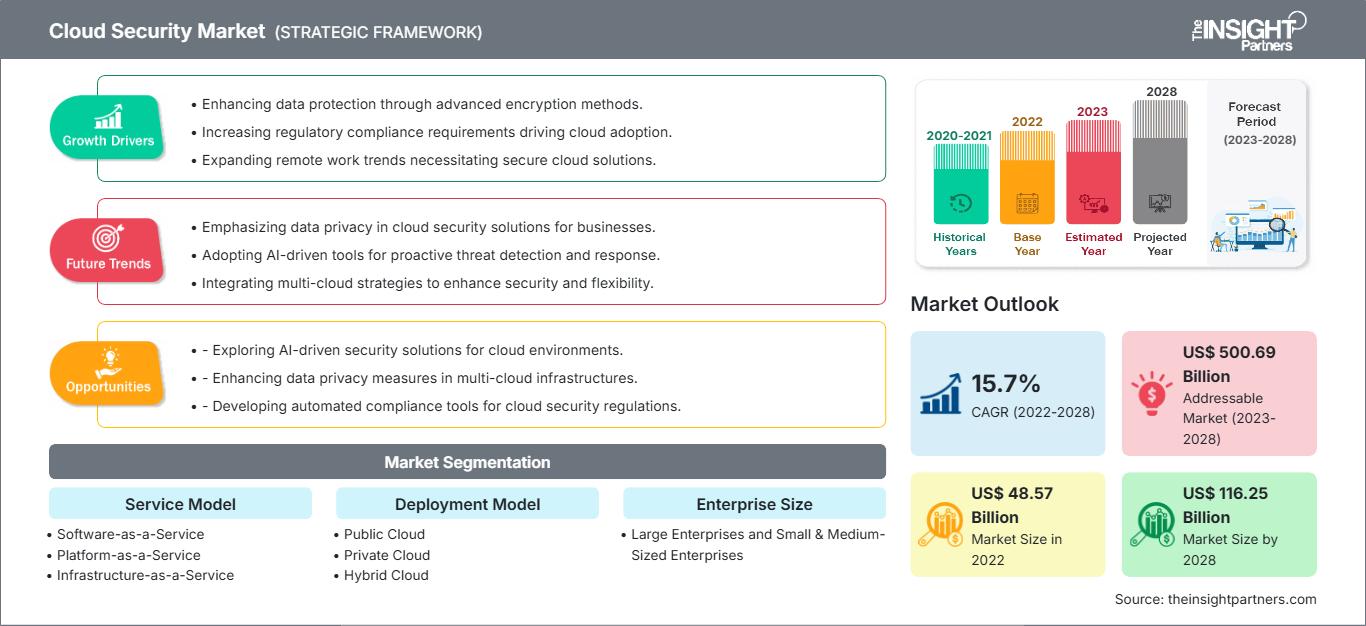

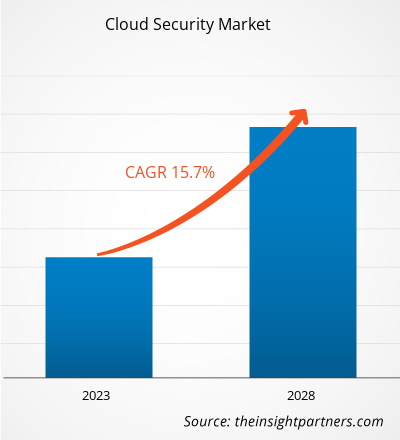

Der globale Markt für Cloud-Sicherheit wird bis 2034 voraussichtlich ein Volumen von 156,18 Milliarden US-Dollar erreichen, gegenüber 40,7 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 15,34 % verzeichnen wird.

Zu den wichtigsten Marktdynamiken zählen der exponentielle Anstieg komplexer Cyberangriffe, die rasche Migration geschäftskritischer Workloads in Multi-Cloud-Umgebungen und die zunehmende Strenge globaler Datenschutzbestimmungen wie DSGVO und CCPA. Darüber hinaus dürfte der Markt von der Integration von Künstlicher Intelligenz (KI) und Maschinellem Lernen (ML) in die Bedrohungserkennung, der Verbreitung von Remote-Arbeitskulturen mit dem damit verbundenen Bedarf an sicherem Zugriff sowie der steigenden Akzeptanz von Zero-Trust-Architekturen in verschiedenen Branchen profitieren.

Marktanalyse für Cloud-Sicherheit

Die Marktanalyse für Cloud-Sicherheit zeigt einen grundlegenden Wandel von reaktiver, perimeterbasierter Verteidigung hin zu proaktiven, datenzentrierten Sicherheitsmodellen. Im Zuge der Migration von Unternehmen zu Cloud-nativen Infrastrukturen weisen Beschaffungstrends eine deutliche Verlagerung hin zu integrierten Plattformen auf, die einheitliche Transparenz über fragmentierte Umgebungen hinweg bieten. Strategische Chancen eröffnen sich in den Bereichen Security-as-Code und DevSecOps, wo die direkte Integration von Sicherheit in den Softwareentwicklungszyklus einen klaren Wettbewerbsvorteil hinsichtlich Geschwindigkeit und Ausfallsicherheit bietet. Die Analyse hebt zudem hervor, dass der Markterfolg zunehmend von der Fähigkeit abhängt, Fehlkonfigurationsrisiken – der Hauptursache für Cloud-Sicherheitsvorfälle – zu managen und automatisierte Behebungstools einzusetzen. Die Wettbewerbsdifferenzierung basiert nun darauf, nahtlosen Schutz mit geringer Latenz zu bieten, der die Agilität und die Leistungsvorteile, für die Cloud-Dienste ursprünglich eingeführt wurden, nicht beeinträchtigt.

Marktübersicht zur Cloud-Sicherheit

Cloud-Sicherheit entwickelt sich von einer ergänzenden IT-Anforderung zu einer tragenden Säule moderner digitaler Unternehmensstrategien. Ursprünglich auf einfache Firewalls und Verschlüsselung fokussiert, umfasst der Markt heute ein breites Ökosystem aus Cloud Access Security Brokern (CASB), Cloud Workload Protection Platforms (CWPP) und Posture Management (CSPM). Während große Unternehmen aufgrund ihrer wertvollen Datenbestände zu den ersten Anwendern gehörten, expandiert der Markt dank skalierbarer, abonnementbasierter Sicherheitsmodelle rasant in den KMU-Bereich. Sowohl etablierte Cybersicherheitskonzerne als auch agile, Cloud-native Startups konkurrieren um die Marktführerschaft, indem sie die Komplexität hybrider und Multi-Cloud-Ökosysteme bewältigen. Der US-Markt beispielsweise ist der größte und ausgereifteste Cloud-Sicherheitsmarkt weltweit. Angetrieben von einer hohen Dichte an Technologieinnovatoren und strengen bundesstaatlichen Compliance-Standards, priorisiert der US-Markt fortschrittliche Bedrohungsanalysen und Zero-Trust-Frameworks. Massive Investitionen in die digitale Transformation im öffentlichen und privaten Sektor stärken weiterhin die Nachfrage nach inländischer Sicherheitsinfrastruktur.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Cloud-Sicherheit: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen im Bereich Cloud-Sicherheit

Markttreiber:

- Zunehmende Komplexität von Cyberbedrohungen: Die steigende Häufigkeit von Ransomware-Angriffen, Datenlecks und Advanced Persistent Threats (APTs), die auf in der Cloud gespeicherte Daten abzielen, ist ein Hauptgrund. Da Angreifer KI nutzen, um Schwachstellen aufzuspüren, sind Unternehmen gezwungen, in fortschrittliche Cloud-Sicherheitslösungen zu investieren, um sensible Unternehmens- und Kundendaten zu schützen.

- Rasante Einführung von Multi-Cloud- und Hybridstrategien: Unternehmen nutzen zunehmend mehrere Cloud-Service-Anbieter, um eine Abhängigkeit von einem einzelnen Anbieter zu vermeiden und die Zuverlässigkeit zu erhöhen. Diese Komplexität führt zu einem Bedarf an einheitlichen Sicherheitsplattformen, die eine konsistente Richtliniendurchsetzung und Transparenz über verschiedene Cloud-Umgebungen hinweg gewährleisten können.

- Strenge regulatorische und Compliance-Anforderungen: Weltweit führen Regierungen strengere Datenschutzgesetze ein. Die Einhaltung von Vorschriften wie HIPAA im Gesundheitswesen oder PCI DSS im Finanzwesen erfordert robuste Cloud-Sicherheitsmaßnahmen und treibt damit kontinuierliche Investitionen in Audit-, Verschlüsselungs- und Zugriffskontrolltools voran.

Marktchancen:

- Integration von KI und Automatisierung in der Bedrohungsanalyse: Sicherheitsanbieter haben die große Chance, KI-gestützte Tools zu entwickeln, die Bedrohungen in Echtzeit und ohne menschliches Eingreifen vorhersagen und beheben können. Die automatisierte Reaktion auf Sicherheitsvorfälle verkürzt die Verweildauer und minimiert den potenziellen Schaden eines Sicherheitsvorfalls.

- Expansion in den Bereich Cloud-Sicherheitsdienste für KMU: Kleine und mittlere Unternehmen (KMU) migrieren zunehmend in die Cloud, verfügen aber oft nicht über das interne Know-how, um diese abzusichern. Vereinfachte, gemanagte Cloud-Sicherheitspakete, die auf die budgetären und technischen Rahmenbedingungen von KMU zugeschnitten sind, stellen ein enormes, bisher unerschlossenes Wachstumspotenzial dar.

- Fokus auf Edge-Computing-Sicherheit: Mit zunehmender Verbreitung dezentraler Datenverarbeitung und des Internets der Dinge (IoT) wird die Absicherung des Cloud-Randes unerlässlich. Die Entwicklung spezialisierter Sicherheitslösungen für Edge-Rechenzentren und vernetzte Geräte bietet Marktteilnehmern ein strategisches Betätigungsfeld.

Marktbericht Cloud-Sicherheit: Segmentierungsanalyse

Der Marktanteil von Cloud-Sicherheit wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standard-Segmentierungsansatz dargestellt:

Nach Servicemodell:

- Software-as-a-Service (SaaS): Ein dominantes und leicht zugängliches Segment, in dem Sicherheit über die Cloud bereitgestellt wird und das sich an Organisationen richtet, die einen wartungsarmen, skalierbaren Schutz für ihre webbasierten Anwendungen suchen.

- Platform-as-a-Service (PaaS): Der Fokus liegt auf der Sicherung der Entwicklungs- und Bereitstellungsumgebung. Es wird sichergestellt, dass die von den Entwicklern verwendete Middleware und die Tools vor externen und internen Schwachstellen geschützt sind.

- Infrastructure-as-a-Service (IaaS): Konzentriert sich auf die Sicherung der grundlegenden Bausteine der Cloud, wie virtuelle Server, Speicher und Netzwerke, und gibt Unternehmen eine detaillierte Kontrolle über ihre Sicherheitskonfigurationen.

Nach Bereitstellungsmodell:

- Öffentliche Cloud: Das am weitesten verbreitete Modell aufgrund seiner Kosteneffizienz, das robuste Sicherheitsmaßnahmen mit geteilter Verantwortung zum Schutz der Daten in Multi-Tenant-Umgebungen erfordert.

- Private Cloud: Dieses Segment, das vor allem von stark regulierten Branchen wie dem Bankwesen und der öffentlichen Verwaltung bevorzugt wird, legt Wert auf maßgeschneiderte, hochsichere Konfigurationen, die einer einzelnen Organisation gewidmet sind.

- Hybrid Cloud: Das am schnellsten wachsende Bereitstellungsmodell, das eine nahtlose Sicherheitsintegration zwischen lokaler Hardware und öffentlichen Cloud-Ressourcen erfordert.

Nach Unternehmensgröße:

- Großunternehmen: Derzeit die Hauptumsatzträger, die umfassende, mehrschichtige Sicherheitslösungen zum Schutz ihrer riesigen globalen Datenbestände einsetzen.

- Kleine und mittlere Unternehmen: Ein wachstumsstarkes Segment, das zunehmend Cloud-native Sicherheit als kostengünstige Alternative zum Aufbau teurer Sicherheitszentren vor Ort einsetzt.

Nach Lösungstyp:

- E-Mail- und Websicherheit: Unverzichtbar, um Phishing und das Eindringen von Malware am häufigsten anzugreifen, nämlich über die Benutzeroberfläche.

- Cloud Identity & Access Management (IAM): Ein grundlegendes Segment, das sicherstellt, dass nur autorisierte Benutzer Zugriff auf bestimmte Cloud-Ressourcen haben, häufig unter Verwendung von Multi-Faktor-Authentifizierung.

- Data Loss Prevention (DLP): Spezialisierte Tools, die entwickelt wurden, um die unautorisierte Übertragung sensibler Informationen außerhalb der Unternehmens-Cloud zu überwachen und zu blockieren.

- Intrusion Detection/Prevention System (IDS/IPS): Aktive Überwachungslösungen, die schädlichen Datenverkehr in Echtzeit erkennen und neutralisieren.

- Security Information & Event Management (SIEM): Bietet eine zentrale Protokollierung und Analyse von Sicherheitswarnungen, um Muster von Kompromittierungen zu identifizieren.

- Sonstige: Dazu gehören Cloud Security Posture Management (CSPM) und Cloud Workload Protection Platforms (CWPP).

Nach Branchen:

- Banken, Finanzdienstleistungen und Versicherungen (BFSI): Führend im Bereich der Sicherheitsausgaben aufgrund der extremen Sensibilität der Finanzdaten und der strengen regulatorischen Aufsicht.

- IT & Telekommunikation: Vorreiter, die Cloud-Sicherheit integrieren, um ihre eigene Infrastruktur zu schützen und ihren Kunden sichere Dienste anzubieten.

- Energie & Versorgung: Schwerpunkt ist der Schutz kritischer Infrastrukturen und intelligenter Stromnetze vor Cybersabotage.

- Regierung und öffentlicher Sektor: Priorisiert Datensouveränität und nationale Sicherheit durch hochsichere, oft private Cloud-Implementierungen.

- Gesundheitswesen: Angetrieben von der Notwendigkeit, Patientendaten zu schützen und Datenschutzgesetze im Zuge des Übergangs zur Telemedizin einzuhalten.

- Fertigung: Immer mehr Unternehmen setzen auf Cloud-Sicherheit, um geistiges Eigentum und industrielle IoT-Systeme (IIoT) zu schützen.

- Sonstige: Dazu gehören Einzelhandel, Bildung und Medien.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Umfang des Marktberichts zur Cloud-Sicherheit

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 40,7 Milliarden US-Dollar |

| Marktgröße bis 2034 | 156,18 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 15,34 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Servicemodell

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich Cloud-Sicherheit: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Cloud-Sicherheit wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für Cloud-Sicherheit nach Regionen

Der asiatisch-pazifische Raum dürfte in den kommenden Jahren das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Süd- und Mittelamerika, dem Nahen Osten und Afrika bieten Premium-Sicherheitsanbietern und Managed-Service-Unternehmen zahlreiche ungenutzte Expansionsmöglichkeiten.

Der Markt für Cloud-Sicherheit befindet sich in einem tiefgreifenden Wandel und entwickelt sich von einem sekundären IT-Ausgabenposten zu einem zentralen Geschäftstreiber. Die weltweite Digitalisierung treibt das Wachstum, die Professionalisierung der Cyberkriminalität und die Einführung hybrider Arbeitsmodelle voran. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

Nordamerika

- Marktanteil: Besitzt weltweit den größten Marktanteil, was auf die Präsenz großer Hyperscaler wie AWS, Microsoft und Google zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Weitverbreitete Übernahme von Cloud-First-Strategien durch Fortune-500-Unternehmen.

- Die hohe Häufigkeit ausgeklügelter Cyberangriffe erfordert eine hochmoderne Verteidigung.

- Strikte Durchsetzung der Datenschutzbestimmungen auf Bundes- und Landesebene.

- Trends: Rasche Verbreitung von Zero-Trust-Architekturen und Konsolidierung von Sicherheitstools in einheitliche, KMU-freundliche Plattformen.

Europa

- Marktanteil: Ein bedeutender Markt, der sich durch einen starken Fokus auf Datensouveränität und Datenschutz auszeichnet und von Großbritannien, Deutschland und Frankreich angeführt wird.

-

Wichtigste Einflussfaktoren:

- Die Einhaltung der Datenschutz-Grundverordnung (DSGVO) treibt Investitionen in Verschlüsselung und Identitäts- und Zugriffsmanagement (IAM) voran.

- Starke staatliche Unterstützung für die Modernisierung der digitalen Infrastruktur und Sovereign-Cloud-Initiativen.

- Zunehmende Verbreitung von Hybrid-Cloud-Modellen in der Industrie und im verarbeitenden Gewerbe.

- Trends: Ein strategischer Wandel hin zur lokalen Datenverarbeitung und die steigende Nachfrage nach grünen Cloud-Sicherheitslösungen, die die Energieeffizienz in Rechenzentren optimieren.

Asien-Pazifik

- Marktanteil: Die am schnellsten wachsende Region, wobei China, Indien und Japan die Hauptmotoren für Ausgaben für Cloud-Infrastruktur und -Sicherheit darstellen.

-

Wichtigste Einflussfaktoren:

- Explosives Wachstum in den regionalen E-Commerce- und Fintech-Märkten.

- Staatlich initiierte Smart-City- und digitale Identitätsprojekte benötigen einen robusten Schutz.

- Rasante Urbanisierung und die Zunahme von Unternehmen, die mobile Lösungen in den Vordergrund stellen.

- Trends: Starke Abhängigkeit von Managed Security Service Providern (MSSPs) aufgrund eines lokalen Mangels an Cybersicherheitsexperten und eines Anstiegs der Aktivitäten von Cloud-nativen Startups.

Süd- und Mittelamerika

- Marktanteil: Ein aufstrebender Markt mit wachsenden Finanzdienstleistungen in Ländern wie Brasilien und Argentinien.

-

Wichtigste Einflussfaktoren:

- Modernisierung der Bankensysteme und der Aufstieg rein digitaler Banken.

- Zunehmende Internetverbreitung und der Wandel von herkömmlichen, lokal installierten IT-Systemen hin zur Cloud.

- Zunehmendes Bewusstsein für Cybersicherheitsrisiken nach mehreren aufsehenerregenden regionalen Sicherheitsvorfällen.

- Trends: Wachstum von spezialisierten Sicherheitsberatungsunternehmen und Einführung lokalisierter Cloud-Knoten durch globale Anbieter zur Reduzierung der Latenz und Verbesserung der Sicherheit.

Naher Osten und Afrika

- Marktanteil: Entwicklungsländer, die sich in Richtung formalisierter digitaler Wirtschaften bewegen, insbesondere in der GCC-Region.

-

Wichtigste Einflussfaktoren:

- Nationale Visionsprogramme (z. B. Saudi Vision 2030) treiben massive Investitionen in die digitale Infrastruktur voran.

- Strategischer Fokus auf den Schutz kritischer Öl- und Gasressourcen vor Cyberangriffen.

- Hohe Nachfrage nach sicheren, skalierbaren Cloud-Diensten zur Unterstützung einer jungen, technikaffinen Bevölkerung.

- Trends: Implementierung nationaler Cybersicherheitsrahmen und Fokus auf den Aufbau inländischer Cloud-Kapazitäten, um die Abhängigkeit von externen Anbietern zu verringern.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb verschärft sich aufgrund der Präsenz etablierter Marktführer wie Microsoft Corporation, Amazon Web Services (AWS), Palo Alto Networks, Check Point Software Technologies und Cisco Systems. Regionale Experten und spezialisierte Cloud-Anbieter wie Zscaler, CrowdStrike und Cloudflare tragen ebenfalls zu einer vielfältigen und schnell wachsenden Marktlandschaft bei.

Dieses wettbewerbsintensive Umfeld zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Plattformkonsolidierung: Weg von Insellösungen hin zu integrierten Plattformen (z. B. SASE und CNAPP), die den gesamten Sicherheitslebenszyklus über ein einziges Dashboard verwalten.

- KI-Integration: Nutzung generativer KI zur Automatisierung komplexer Sicherheitsaufgaben, wie z. B. das Schreiben von Firewall-Regeln oder die Analyse umfangreicher Protokolle auf subtile Anzeichen einer Sicherheitsverletzung.

- Zero-Trust-Frameworks: Über die herkömmlichen VPNs hinausgehend, um jeden Benutzer und jedes Gerät zu verifizieren, unabhängig davon, ob sie sich innerhalb oder außerhalb des Netzwerkperimeters befinden.

- End-to-End-Transparenz: Bereitstellung von Deep-Packet-Inspection und Verhaltensanalysen über IaaS-, PaaS- und SaaS-Schichten hinweg, um blinde Flecken in der Cloud zu beseitigen.

Chancen und strategische Schritte

- Partnerschaften mit Hyperscalern: Cybersicherheitsunternehmen gehen zunehmend strategische Allianzen mit AWS und Azure ein, um ihre Sicherheitstools nativ in die Cloud-Konsolen zu integrieren.

- Fokus auf branchenspezifische Sicherheit: Entwicklung spezialisierter Compliance-Konzepte für das Gesundheitswesen, den Finanzsektor und den öffentlichen Dienst, um den regulatorischen Aufwand für die Kunden zu vereinfachen.

Die wichtigsten Unternehmen, die auf dem Markt für Cloud-Sicherheit tätig sind, sind:

- Amazon Web Services, Inc.

- Microsoft

- Google LLC

- Orakel

- IBM Corporation

- Cisco Systems, Inc.

- Trend Micro Incorporated

- Palo Alto Networks, Inc.

- Checkpoint Software Technologies

- VMware, Inc.

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen im Markt für Cloud-Sicherheit

- Im September 2024 gab Check Point Software Technologies Ltd. die geplante Übernahme von Lakera bekannt, einem führenden Anbieter von KI-nativem Schutz für Agentic-KI-Anwendungen. Mit dieser Akquisition setzte Check Point einen neuen Standard für Cloud-Sicherheit, indem das Unternehmen einen umfassenden KI-Sicherheitsstack bereitstellte, der speziell für den Schutz von Unternehmen bei der beschleunigten Einführung cloudbasierter KI-Technologien entwickelt wurde.

- Im März 2025 gab Google Cloud die Unterzeichnung einer endgültigen Vereinbarung zur Übernahme von Wiz bekannt, um Unternehmen und Behörden mehr Auswahlmöglichkeiten beim Schutz ihrer IT-Systeme zu bieten. Durch die Integration der Wiz-Funktionen wollte das Unternehmen eine umfassende Cloud-Sicherheitsplattform bereitstellen, die moderne IT-Umgebungen in Multi-Cloud-Infrastrukturen schützt.

Marktbericht Cloud-Sicherheit: Abdeckung und Ergebnisse

Der Bericht „Cloud-Sicherheitsmarkt: Größe und Prognose (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für Cloud-Sicherheit auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Geltungsbereich abgedeckt werden

- Trends im Markt für Cloud-Sicherheit sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Cloud-Sicherheit mit Fokus auf wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen im Markt für Cloud-Sicherheit.

- Detaillierte Unternehmensprofile

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends