Marktwachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose für Hochgeschwindigkeitskabel bis 2031

Historische Daten : 2021-2023 | Basisjahr : 2024 | Prognosezeitraum : 2025-2031Marktgröße und Prognose für Hochgeschwindigkeitskabel (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Typ (Direct Attach Copper (DAC)-Kabel und Active Optical Cable (AOC), Active Copper Cable (ACC), PCIe-Kabel, Active Electrical Cable (AEC) und SAS-Kabel), Anwendung (Switch-to-Switch-Verbindung, Switch-to-Server und Server-to-Storage-Verbindung) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00025895

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 187

- Verfügbare Berichtsformate :

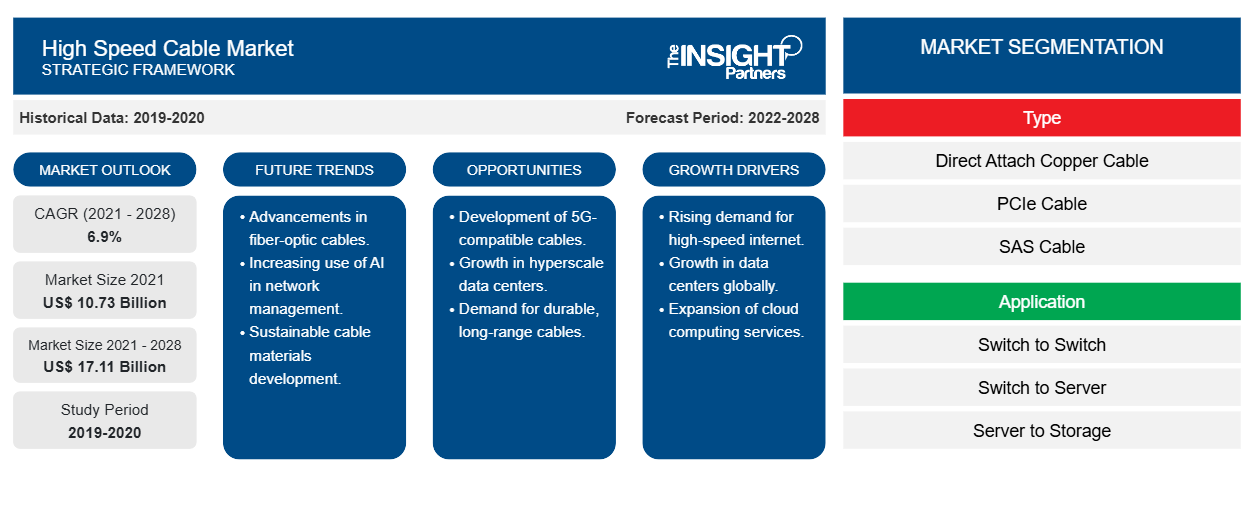

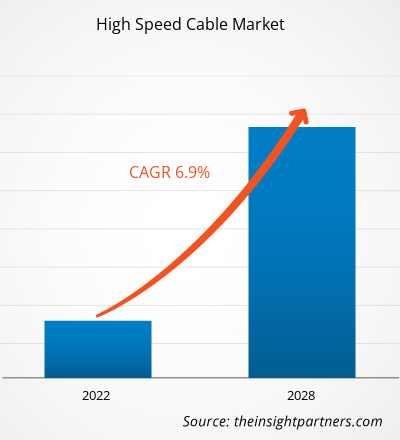

Der Markt für Hochgeschwindigkeitskabel wird voraussichtlich von 12,90 Milliarden US-Dollar im Jahr 2024 auf 24,99 Milliarden US-Dollar im Jahr 2031 anwachsen. Für den Zeitraum 2025–2031 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 10,2 % erwartet. Die Entstehung von Smart Cities dürfte in den kommenden Jahren neue Trends auf den Markt bringen.

Marktanalyse für Hochgeschwindigkeitskabel

Da Cloud-Dienste rasant expandieren, steigt die Nachfrage nach leistungsstarken und kostengünstigen Rechenzentrumsverbindungen rasant an. Dies hat zu einer zunehmenden Nutzung von Hochgeschwindigkeitskabeln geführt. Im Gegensatz zu optischen Verbindungen, die optische Module zur Signalumwandlung verwenden, ermöglichen Hochgeschwindigkeitskabel wie Direct Attach Copper (DAC) und Active Optical Cables (AOC) eine direkte Verbindung der Bitübertragungsschicht zwischen zwei Ports mithilfe von Twin-Axial-Kabeln. Dies gewährleistet die Signalintegrität über festgelegte Distanzen, ohne dass aktive optische Komponenten erforderlich sind. Branchen wie die Elektronik-, Automobil-, Kommunikations- und Netzwerkindustrie entwickeln sich weiter und führen Innovationen ein, die eine schnellere Datenübertragung ermöglichen. Der steigende Bedarf an effizienter Konnektivität treibt somit das Marktwachstum für Hochgeschwindigkeitskabel voran . Im Automobilsektor integrieren Hersteller zunehmend Elektronik- und Infotainmentsysteme in Fahrzeuge, um die Konnektivität zu verbessern, was die Nachfrage weiter ankurbelt.

Marktübersicht für Hochgeschwindigkeitskabel

Rechenzentren benötigen effiziente Verbindungen innerhalb und zwischen Racks. Hochgeschwindigkeitskabel eignen sich hierfür hervorragend. Sie bieten schnelle Verbindungen bei einem Stromverbrauch von weniger als 0,1 W und minimaler Wärmeentwicklung. Diese Energieeffizienz trägt dazu bei, den Kühlbedarf der Klimaanlagen im Rechenzentrum zu reduzieren. Darüber hinaus zeichnen sich Hochgeschwindigkeitskabel durch eine hohe Haltbarkeit aus und sind daher weniger anfällig für Schäden durch Biegen oder mechanische Beanspruchung. Diese Robustheit minimiert das Ausfallrisiko in Umgebungen mit hoher Dichte und bietet einen erheblichen Vorteil im Rechenzentrumsbetrieb.

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten

Markt für Hochgeschwindigkeitskabel: Strategische Einblicke

-

Informieren Sie sich über die wichtigsten Markttrends in diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, von Markttrends bis hin zu Schätzungen und Prognosen.

Markttreiber und Chancen für Hochgeschwindigkeitskabel

Entwicklungen bei 5G-Netzwerkdiensten

Passive DACs, im Grunde hochwertige Kupferdrähte ohne eingebettete Elektronik, sind aufgrund dieser Komponenten günstiger als Kabel. Fortschrittliche Chipsätze in AECS und VCSEL-Laser in AOCS erhöhen die Kosten jedoch um das Zwei- bis Fünffache. DACs werden häufig in 5G-Netzen für Verbindungen über kurze Distanzen im selben Gebiet eingesetzt, wie z. B. O-RAN-Mobilfunkstandorte und Edge-Rechenzentren. Diese Kabel ermöglichen Hochgeschwindigkeitsdatentransport mit geringer Latenz und geringem Stromverbrauch. Beispielsweise eignen sich passive QSFP28-DACs für direkte Verbindungen im Schaltschrank, da sie 100 Gbit/s unterstützen, während SFP28-DACs 25 Gbit/s unterstützen. Die dichten Zellen und das hohe Verkehrsaufkommen in 5G-Netzen erfordern Backhaul-Verbindungen, die Hunderte von Gigabit verarbeiten können. Dies erfordert schnellere Ethernet-Verbindungen, z. B. 400G oder mehr. DACs sind unerlässlich, um diese Hochgeschwindigkeits-Ethernet-Verbindungen über kurze Distanzen zu ermöglichen und einen effektiven Datentransfer zwischen Netzwerkgeräten zu gewährleisten. Den niedrigsten Stromverbrauch pro Port bieten passive DACs, die pro Port zwischen 91 % und 97 % weniger Strom verbrauchen als Glasfaserkabel mit unabhängigen Transceivern. Das Volumen der Server-Netzwerkzugriffsverbindungen mit kurzer Reichweite steigt schnell an.DACs, which are basically premium copper wires without any embedded electronics, are less expensive than the cables due to these components. Advanced chipsets in AECS and VCSEL lasers in AOCS add a premium that can increase the cost by at least two to five times. DACs are frequently utilized in 5G networks for short-range connections that occur in the same area, such as O-RAN cell sites and edge data centers. These cables support high-speed data transport with low latency and power consumption. For instance, passive QSFP28 DACs are appropriate for in-cabinet direct connections since they can support 100 Gb/s, while SFP28 DACs can support 25 Gb/s. The dense cells and high traffic of 5G networks necessitate backhaul connections capable of handling hundreds of gigabits. This necessitates greater speed Ethernet connections, such as 400G or greater. DACs are essential in order to facilitate these high-speed Ethernet connections across short distances and guarantee effective data transfer between network devices. The lowest power consumption per port is also provided by passive DACs, which use between 91% and 97% less power per port than fiber cabling with independent transceivers. The volume of short-reach server network access connections quickly mounts up.

Zunehmender Einsatz von Rechenzentren

Der Anstieg der Internetnutzung und die Entwicklung fortschrittlicher Softwarelösungen haben das weltweite Datenvolumen stark ansteigen lassen. Der Bedarf an der Verarbeitung und Speicherung riesiger Datenmengen hat Unternehmen dazu veranlasst, fortschrittliche Verarbeitungs- und Speicherlösungen einzusetzen und so den Aufbau von Rechenzentren voranzutreiben. Mit der zunehmenden Digitalisierung sind Rechenzentren zu einem zentralen Aspekt der modernen Industrie und Wirtschaft geworden. Rechenzentren spielen eine zentrale Rolle im Cloud Computing. Da die Branche aufgrund der Kosten- und Betriebsvorteile zunehmend auf Cloud-Technologie setzt, sind KMU bei der Einführung dieser Technologie führend. Darüber hinaus werden komplexe Cloud-Computing-Operationen von großen Technologieunternehmen und Forschungseinrichtungen durchgeführt. Aktive optische Kabel, direkt angeschlossene Kupferkabel und Glasfaserkabel gehören zu den am häufigsten in Rechenzentren verwendeten Hochgeschwindigkeitskabeln.

Segmentierungsanalyse des Marktberichts für Hochgeschwindigkeitskabel

Wichtige Segmente, die zur Ableitung der Marktanalyse für Hochgeschwindigkeitskabel beigetragen haben, sind Komponenten, Endbenutzer und Konnektivität.

- Je nach Typ ist der Markt in Direct Attach Copper (DAC)-Kabel, aktive optische Kabel (AOC), aktive Kupferkabel (ACC), PCIe-Kabel, aktive elektrische Kabel (AEC) und SAS-Kabel segmentiert. Das Segment der aktiven optischen Kabel (AOC) hatte im Jahr 2024 den größten Marktanteil.

- Je nach Anwendung ist der Markt in Switch-to-Switch-Interconnect, Switch-to-Server und Server-to-Storage-Interconnect segmentiert. Das Segment Switch-to-Switch-Interconnect hatte im Jahr 2024 den größten Marktanteil.

Marktanteilsanalyse für Hochgeschwindigkeitskabel nach geografischer Lage

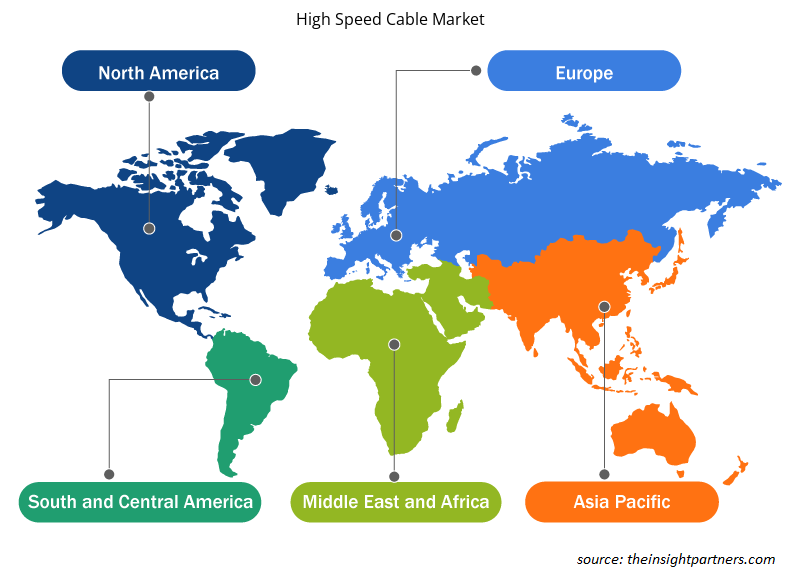

Der geografische Umfang des Marktberichts für Hochgeschwindigkeitskabel ist in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Süd- und Mittelamerika.

Der asiatisch-pazifische Raum hatte 2024 einen bedeutenden Marktanteil. Er ist die am schnellsten wachsende Region für die Nachfrage nach Hochgeschwindigkeitskabeln, was auf die rasante Urbanisierung, das exponentielle Wachstum der Internetnutzer und den technologischen Fortschritt in Ländern wie China, Japan, Südkorea und Indien zurückzuführen ist. Der Ausbau von 5G-Netzen, der Bau großer Rechenzentren und ein boomender Markt für Elektrofahrzeuge schaffen erhebliche Möglichkeiten für den Einsatz von Hochgeschwindigkeitskabeln in den Bereichen Telekommunikation, Transport und Energie.

Die Automobilindustrie im asiatisch-pazifischen Raum trägt ebenfalls maßgeblich zur steigenden Nachfrage nach Hochgeschwindigkeitskabeln bei. In China, Japan, Südkorea und anderen Ländern benötigen Automobilhersteller angesichts der zunehmenden Verbreitung von Elektrofahrzeugen Hochgeschwindigkeitskabel für die Übertragung von Bilddaten, Multifunktionsdisplays und Infotainmentsystemen für Rücksitzpassagiere sowie für andere Anwendungen. China, der weltweit größte Markt für Elektrofahrzeuge, setzt sich ehrgeizige Ziele für die Elektromobilität und treibt damit die Nachfrage nach Hochleistungskomponenten an. Laut der Internationalen Energieagentur (IEA) unterstreicht das signifikante Wachstum der Verbreitung von Elektrofahrzeugen in China – die Zahl der Neuzulassungen von Elektroautos wird im Jahr 2023 8,1 Millionen erreichen, ein Anstieg von 35 % gegenüber 2022 – die wachsende Nachfrage nach Hochgeschwindigkeitskabeln in der Automobilindustrie. Dieser Anstieg der Elektrofahrzeugproduktion hängt eng mit der zunehmenden Nachfrage nach Hochgeschwindigkeitskabeln zusammen, insbesondere im asiatisch-pazifischen Raum. Hochgeschwindigkeitskabel in Automobilanwendungen ermöglichen eine schnelle Datenübertragung für Funktionen wie fortschrittliche Fahrerassistenzsysteme (ADAS), Infotainmentsysteme und Kamerasysteme. Sie ermöglichen außerdem die Fahrzeug-zu-Fahrzeug-Kommunikation (V2V) und die Fahrzeug-zu-Infrastruktur-Kommunikation (V2X).

Regionale Einblicke in den Markt für Hochgeschwindigkeitskabel

Die Analysten von Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Hochgeschwindigkeitskabel im Prognosezeitraum beeinflussen, ausführlich erläutert. Dieser Abschnitt behandelt auch die Marktsegmente und die geografische Lage von Hochgeschwindigkeitskabeln in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

- Erhalten Sie regionale Daten zum Markt für Hochgeschwindigkeitskabel

Umfang des Marktberichts für Hochgeschwindigkeitskabel

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2024 | 12,90 Milliarden US-Dollar |

| Marktgröße bis 2031 | 24,99 Milliarden US-Dollar |

| Globale CAGR (2025 – 2031) | 10,2 % |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025–2031 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte von Hochgeschwindigkeitskabeln: Auswirkungen auf die Geschäftsdynamik

Der Markt für Hochgeschwindigkeitskabel wächst rasant. Die steigende Nachfrage der Endverbraucher wird durch Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile angetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte beschreibt die Verteilung der in einem bestimmten Markt oder einer bestimmten Branche tätigen Unternehmen. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu dessen Größe oder Gesamtmarktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für Hochgeschwindigkeitskabel sind:

- Amphenol Corporation

- Axon Cable SAS

- Molex LLC

- Volex PLC

- NVIDIA CORPORATION

- Samtec INC

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Hochgeschwindigkeitskabel

Marktnachrichten und aktuelle Entwicklungen zum Thema Hochgeschwindigkeitskabel

Der Markt für Hochgeschwindigkeitskabel wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet. Dazu zählen wichtige Unternehmenspublikationen, Verbandsdaten und Datenbanken. Nachfolgend sind einige Entwicklungen im Markt für Hochgeschwindigkeitskabel aufgeführt:

- Amphenol Communications Services (ACS), ein weltweit führender Anbieter von Hochleistungs-Verbindungslösungen, und Semtech Corporation (Nasdaq: SMTC), ein führender Anbieter von Hochleistungs-Halbleitern, IoT-Systemen (Internet of Things) und Cloud-Konnektivitätslösungen, haben ein hochmodernes 1,6T OSFP Active Copper Cable (ACC)-Produkt mit Semtechs CopperEdge 224G/Lane Linear Equalizer/Redriver ICs vorgestellt, das für den Einsatz in der nächsten Generation von KI/ML und Rechenzentrumsinfrastrukturen vorgesehen ist. (Quelle: Amphenol Communications, Pressemitteilung, April 2025)

- Samtec hat einen neuen Designleitfaden für Hochgeschwindigkeitskabel veröffentlicht, der zahlreiche neue Produkte, Technologien und Roadmap-Elemente enthält. Der Leitfaden präsentiert Samtecs Innovationen für Architekturen der nächsten Generation – Flyover-, HDR-, Optik- und HF-Lösungen kombiniert mit branchenführendem Support, eigener Fertigung und Anpassungsmöglichkeiten, um eine Lösung für jede Anwendung zu schaffen. (Quelle: Samtec, Pressemitteilung, Juni 2023)

Marktbericht zu Hochgeschwindigkeitskabeln – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Hochgeschwindigkeitskabel (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose für Hochgeschwindigkeitskabel auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Markttrends für Hochgeschwindigkeitskabel sowie Marktdynamiken wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Hochgeschwindigkeitskabel mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und jüngsten Entwicklungen für den Markt für Hochgeschwindigkeitskabel

- Detaillierte Firmenprofile

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für Hochgeschwindigkeitskabel

Kostenlose Probe anfordern für - Markt für Hochgeschwindigkeitskabel