Markt für Kraftstoffe aus Kunststoff – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Marktgröße und -prognose für die Umwandlung von Kunststoff in Kraftstoff (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach Technologie [Pyrolyse, Vergasung und Depolymerisation] und Endprodukt [Rohöl, Wasserstoff und andere] sowie Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00008127

- Kategorie : Energie und Leistung

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 15, 2025

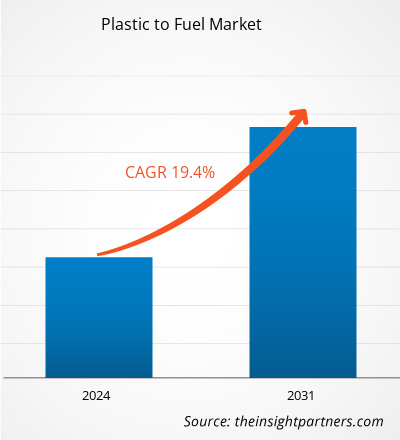

Der Markt für die Umwandlung von Kunststoff in Kraftstoffe soll von 289,55 Millionen US-Dollar im Jahr 2023 auf 1.194,48 Millionen US-Dollar im Jahr 2031 anwachsen. Der Markt soll zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 19,4 % verzeichnen. Die kontinuierliche technische Entwicklung im Bereich Recycling und Abfallentsorgung dürfte ein wichtiger Markttrend für die Umwandlung von Kunststoff in Kraftstoffe bleiben.

Marktanalyse für die Umwandlung von Kunststoff in Kraftstoff

Das wachsende Bewusstsein für Treibhausgasemissionen dürfte das Wachstum von Kunststoffen auf dem Kraftstoffmarkt vorantreiben. Nicht recycelbare Polymere wie Polyethylenterephthalat (PET), Polystyrol und Polyvinylchlorid (PVC) sind derzeit das größte Problem. Mehr als 90 % des Kunststoffs werden nicht recycelt und stattdessen weggeworfen, auf Deponien gelagert oder ins Meer geschüttet. Nur 9–10 % des Kunststoffabfalls wurden gesammelt und recycelt, was bedeutet, dass nur 9–10 % des Kunststoffabfalls gesammelt und recycelt wurden. Dies eröffnet ein enormes Marktpotenzial für die Kunststoff-zu-Kraftstoff-Industrie, da durch das Recycling dieser Kunststoffabfälle nicht recycelbare Kunststoffabfälle entstehen, die in nicht allzu ferner Zukunft in PFT verwendet werden können.

Überblick über den Markt für Kunststoff zu Kraftstoff

Angesichts der wachsenden Bevölkerung, der raschen wirtschaftlichen Entwicklung, der fortschreitenden Urbanisierung und der Veränderungen im Lebensstil nehmen die Erzeugung und der Verbrauch von Plastikmüll stark zu. Plastikmüll ist in den letzten Jahren weltweit zu einem zunehmenden Problem geworden. Mit der zunehmenden Abhängigkeit von Plastik ist die Praxis, Plastik achtlos wegzuwerfen, zur gängigen Praxis geworden. Im Laufe der Jahre wurden zahlreiche Verfahren entwickelt, um aus Abfall Wertstoffe zu gewinnen und Plastik auf innovative Weise zu recyceln und wiederzuverwenden. Die Umwandlung von Plastikmüll in Kraftstoff und seine Nutzbarmachung für industrielle und private Zwecke ist eine der aktuellen Innovationen. Die Umwandlung von Plastik in Kraftstoff wurde bereits in Ländern wie Deutschland, den USA und Japan erfolgreich durchgeführt. Diese drei Länder haben es auch geschafft, Umwandlungsverfahren in praktikable Geschäftsmodelle umzusetzen. Ebenso übernehmen Länder wie Kanada und Indien nach und nach den Prozess der Umwandlung von Plastik in Kraftstoff.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Der Markt für Kunststoff zu Kraftstoff: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen für den Markt „Kunststoff als Kraftstoff“

Steigender Energiebedarf treibt Nachfrage nach Technologien zur Umwandlung von Kunststoff in Kraftstoffe

Elektrizität spielt eine entscheidende Rolle und macht einen zunehmenden Anteil der Energiedienstleistungen aus. Angesichts des steigenden verfügbaren Einkommens, des Verbraucherbewusstseins, der Elektrifizierung von Transport und Wärme sowie einer steigenden Nachfrage nach digitalen Geräten und Klimaanlagen wird der Energiebedarf voraussichtlich weiter steigen. Regierungspolitik und verfügbare Technologie arbeiten im Einklang mit dem politischen Szenario, um die Energieversorgung auf kohlenstoffarme Quellen umzustellen, was die Nachfrage nach Technologien zur Umwandlung von Kunststoff in Kraftstoffe weltweit steigert. Die kommerzielle Verfügbarkeit einer Reihe emissionsarmer Erzeugungstechnologien stellt Elektrizität in den Mittelpunkt der Bemühungen zur Bekämpfung von Klimawandel und Umweltverschmutzung, was die Nachfrage nach alternativen Lösungen erhöht und somit zu einer Expansion des Marktes für die Umwandlung von Kunststoff in Kraftstoffe führt.

Einführung des Go Green-Prozesses – eine Chance auf dem Markt für die Umwandlung von Kunststoff in Kraftstoff

Initiativen zur Umwandlung von Plastik in Kraftstoff gewinnen in der Energiebranche zunehmend an Bedeutung, da sich immer mehr Menschen der Umweltschäden bewusst werden, die durch Einwegplastik und unzureichende Recyclingpraktiken verursacht werden. Dies veranlasst Forscher, nach innovativen Wegen zu suchen, um den wachsenden Plastikausstoß zu beseitigen. Eine Erhöhung der staatlichen Subventionen für die Entwicklung umweltfreundlicher Technologien und Versuche, solche Technologien durch erweiterte Finanzierung zu fördern, dürften erhebliche Marktwachstumschancen bieten. Darüber hinaus üben die strengen Energiesicherheitsvorschriften der Regierung Druck auf Unternehmen aus, in umweltfreundliche Forschung zu investieren. Die Umwandlung von Plastik in Kraftstoff ist eine vielversprechende Option, um nicht nur die Umweltverschmutzung zu reduzieren, sondern auch den Regionen große wirtschaftliche Vorteile zu bringen.

Segmentierungsanalyse des Marktberichts „Kunststoff zu Kraftstoff“

Schlüsselsegmente, die zur Ableitung der Marktanalyse zur Umwandlung von Kunststoff in Kraftstoff beigetragen haben, sind Technologie und Endprodukt.

- Basierend auf der Technologie wurde der Markt für die Umwandlung von Kunststoff in Kraftstoff in Pyrolyse, Vergasung und Depolymerisation unterteilt. Das Pyrolysesegment hatte im Jahr 2023 einen größeren Marktanteil.

- In Bezug auf das Endprodukt wurde der Markt in Rohöl, Wasserstoff und andere segmentiert. Das Rohölsegment dominierte den Markt im Jahr 2023.

Marktanteilsanalyse für Kunststoff zu Kraftstoff nach geografischer Lage

Der geografische Umfang des Marktberichts zur Umwandlung von Kunststoff in Kraftstoff ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

Der asiatisch-pazifische Raum umfasst viele Entwicklungsländer, darunter China und Indien. Dies sind auch die beiden bevölkerungsreichsten Länder der Welt. Diese Plastikabfälle werden entweder auf Mülldeponien oder ins Meer geworfen, wodurch die Umwelt belastet wird und weltweit langfristige negative Auswirkungen entstehen. Darüber hinaus ist der asiatisch-pazifische Raum mit Hauptverursachern wie China, Indonesien, Sri Lanka, Vietnam und den Philippinen der größte Anteil der Meeresverschmutzung durch Plastik. Eine ineffiziente Abfallwirtschaftsinfrastruktur und das mangelnde Bewusstsein für die negativen Auswirkungen von Einwegplastik sind die Hauptgründe für den Anstieg des Plastikmülls in der gesamten Region. Die steigenden Investitionen sowohl staatlicher als auch privater Organisationen zur Förderung des Recyclings von Plastik zu weiteren wiederverwendbaren Materialien treiben das Wachstum des Marktes für die Umwandlung von Plastik in Kraftstoffe in der gesamten Region voran. Aufgrund der steigenden Investitionen in das Recycling von Plastikabfällen in der gesamten Region investieren auch die Akteure auf dem Markt für die Umwandlung von Plastik in Kraftstoffe in die Ausweitung ihrer Geschäfte in der gesamten Region, was das Wachstum des Marktes für die Umwandlung von Plastik in Kraftstoffe in der Region Asien-Pazifik vorantreibt.

Regionale Einblicke in den Markt für Kunststoff als Kraftstoff

Die regionalen Trends und Faktoren, die den Markt für die Umwandlung von Kunststoff in Kraftstoff während des gesamten Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie der Umwandlung von Kunststoff in Kraftstoff in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für die Umwandlung von Kunststoff in Kraftstoff

Umfang des Marktberichts zur Umwandlung von Kunststoff in Kraftstoff

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 289,55 Millionen US-Dollar |

| Marktgröße bis 2031 | 1.194,48 Millionen US-Dollar |

| Globale CAGR (2023 - 2031) | 19,4 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Technologie

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für die Umwandlung von Kunststoff in Kraftstoff wächst rasant. Dies wird durch die steigende Nachfrage der Endverbraucher aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für die Umwandlung von Kunststoff in Kraftstoff sind:

- Agilyx, Inc

- Cassandra Oil AB

- Klean Industries Inc.

- Nexus Fuels LLC

- Recycling Technologies Ltd.

- Agile Process Chemicals LLP

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Kraftstoffe aus Kunststoff

Neuigkeiten und aktuelle Entwicklungen zum Markt für Kraftstoffe aus Kunststoff

Der Markt für die Umwandlung von Kunststoff in Kraftstoff wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für Innovationen, Geschäftserweiterungen und Strategien:

- Im Februar 2022 haben Agilyx und Virgin Group eine strategische Partnerschaft zur Erforschung und Entwicklung kohlenstoffärmerer Brennstoffanlagen geschlossen, um die Plastikverschmutzung zu bekämpfen und die Agenda des globalen Übergangs zu Netto-Null zu unterstützen. (Quelle: Agilyx, Inc, Pressemitteilung/Unternehmenswebsite/Newsletter)

- Im November 2022 arbeitete Klean Industries mit RGH Systems zusammen, um auf den Philippinen eine Anlage zur Energiegewinnung aus Kunststoffabfällen zu entwickeln. (Quelle: Klean Industries Inc., Pressemitteilung/Unternehmenswebsite/Newsletter)

Marktbericht zur Umwandlung von Kunststoff in Kraftstoffe – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für die Umwandlung von Kunststoff in Kraftstoff (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Kunststoff-Kraftstoff-Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Markttrends zu „Kunststoff als Kraftstoff“

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Kraftstoffe aus Kunststoff mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Kunststoff-Kraftstoff-Industrie, Landschafts- und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und jüngsten Entwicklungen

- Detaillierte Firmenprofile

Nivedita ist eine versierte Forschungsexpertin mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Sie ist derzeit als Projektmanagerin im IKT-Bereich bei The Insight Partners tätig und verfügt über umfassende Fachkenntnisse in der Leitung und Durchführung von syndizierten, kundenspezifischen, abonnementbasierten und beratenden Forschungsaufträgen in unterschiedlichen Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen und umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Sie hat umfassend mit führenden IKT-Unternehmen zusammengearbeitet und ihnen geholfen, Marktchancen zu erkennen und Branchenveränderungen zu meistern.

Nivedita hat einen MBA in Management vom IMS, Dehradun. Vor ihrem Eintritt bei The Insight Partners sammelte sie wertvolle Erfahrungen bei MarketsandMarkets und Future Market Insights in Pune, wo sie verschiedene Forschungspositionen innehatte und sich ein solides Fundament in Branchenanalyse und Kundenbindung erarbeitete.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends