Descripción general del mercado de software académico, crecimiento, tendencias, análisis, informe de investigación (2021-2027)

Pronóstico del mercado de software académico hasta 2027: impacto de la COVID-19 y análisis global por implementación (en la nube y local) y aplicación (universidades, servicios educativos, etc.)

- Estado : Publicada

- Código de informe : TIPRE00013179

- Categoría : Tecnología, medios y telecomunicaciones

- Número de páginas : 141

- Formatos de informe disponibles :

- Fecha de última actualización : June 19, 2024

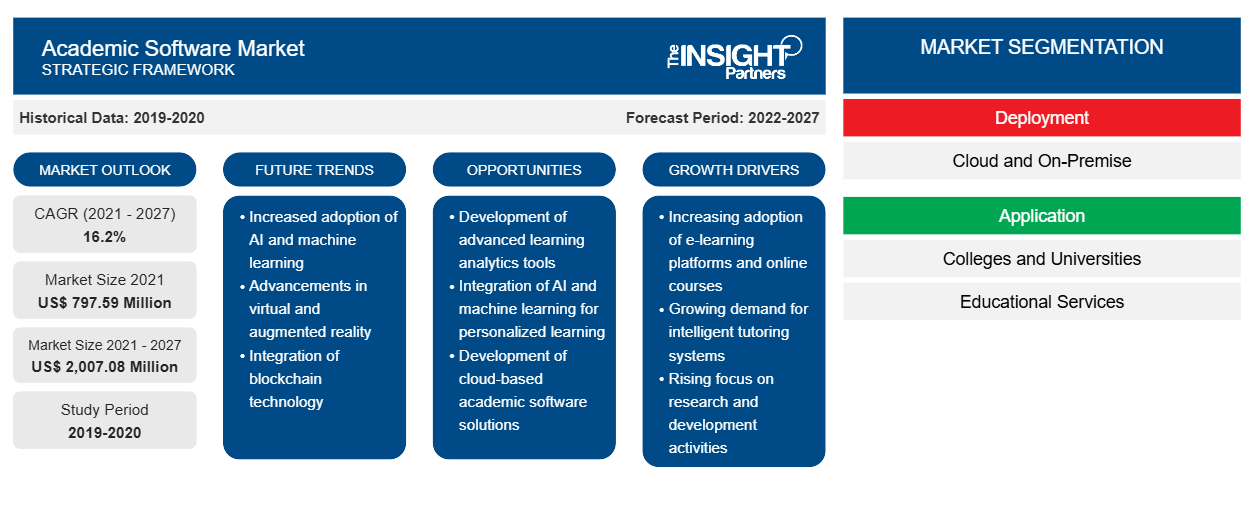

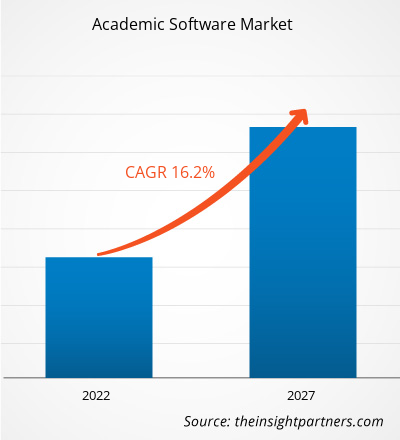

Se espera que el mercado de software académico crezca de US$ 797,59 millones en 2021 a US$ 2.007,08 millones en 2027. Se espera que el mercado de software académico crezca a una CAGR del 16,2% durante el período de pronóstico de 2021 a 2027.

La creciente adopción del aprendizaje electrónico en las instituciones es el factor clave que impulsa el crecimiento del mercado de software académico. En el aprendizaje electrónico, leer o ver contenido está cambiando la forma en que se imparte la educación. Varios cursos de aprendizaje electrónico, como animaciones, podcasts y videos, crean un entorno de aprendizaje multimodal y realista. El aprendizaje electrónico y el contenido educativo abren varias oportunidades de aprendizaje inmersivo para los estudiantes a través de computadoras, portátiles, tabletas o teléfonos inteligentes. En lugar de estar en un entorno pasivo, los estudiantes pueden elegir lo que necesitan aprender de manera fácil y rápida. Estos beneficios están aumentando la demanda de software académico en todo el mundo.

La pandemia de COVID-19 ha afectado gravemente al sector educativo en todo el mundo. Esto también ha promovido la adopción de sistemas de educación en línea en las principales economías del mundo, lo que ha influido en la adopción de software para diversas aplicaciones, como impartir conferencias, gestionar estudiantes y otras actividades operativas desde ubicaciones remotas. Por lo tanto, se espera que la creciente adopción de soluciones tecnológicamente avanzadas en todo el sector tenga un impacto positivo en el crecimiento del mercado de software académico durante la pandemia.

Según la implementación, el mercado de software académico se segmenta en la nube y en las instalaciones. En 2019, el segmento de la nube representó una mayor participación en el mercado. En los últimos años, la industria tecnológica ha experimentado un aumento constante en la adopción de la computación basada en la nube. Esto se debe al hecho de que la computación basada en la nube simplifica el tiempo de implementación y reduce sustancialmente los costos de implementación. Esta ventaja ha atraído a una gran cantidad de usuarios finales; por lo tanto, la mayoría de los actores del mercado de software académico ofrecen productos basados en la nube junto con la creciente demanda de software basado en la nube. Además, la infraestructura de Internet en los países desarrollados ha evolucionado y está floreciendo en muchos países en desarrollo, lo que permite a los usuarios finales acceder a las soluciones basadas en la nube tanto en países desarrollados como en desarrollo.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de software académico: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Perspectivas del mercado del software académico

Integración de Tecnologías como Inteligencia Artificial con Soluciones de Software Académico

La inteligencia artificial (IA) es una tecnología que otorga a las computadoras la capacidad, de la misma manera que los humanos, de comunicarse con las personas, comprender eventos, aprender y reaccionar ante ellos. A lo largo de los años, la inteligencia artificial no solo tuvo enormes aplicaciones en diferentes industrias (como la seguridad, la vigilancia y la tecnología de la información), sino que también experimentó un aumento en la adopción de las tecnologías en el sector educativo. La IA se está adoptando en escuelas, colegios y universidades para automatizar tareas repetitivas, como la calificación, el análisis financiero y los procesos de admisión. Por ejemplo, la IA se puede calibrar para aprender y modelar las acciones de los maestros mientras califican, a través de programas informáticos avanzados (como Automated Grading) para la asignación automática de calificaciones en el futuro. Con el tiempo, el programa aprendería las habilidades académicas de varios estudiantes y, en función de su desempeño, prepararía planes de capacitación personalizados.

Información del mercado basada en la implementación

Según el tipo de implementación, el mercado mundial de software académico se segmenta en la nube y en las instalaciones. El software académico basado en la nube está experimentando una gran demanda en comparación con el software académico en las instalaciones. El segmento de la nube genera la mayor parte de la demanda, ya que es comparativamente menos costoso debido a la sólida infraestructura de red en los países desarrollados. Además, los proveedores de software académico basado en la nube están muy centrados en desarrollar un parche de seguridad de alto nivel para eliminar el riesgo de ciberataques. Este factor también está creando una demanda significativa de los usuarios finales, lo que impulsa el mercado de software académico.

Información del mercado basada en aplicaciones

Según la aplicación, el mercado de software académico se segmenta en colegios y universidades, servicios educativos y otros. La creciente adopción de soluciones modernas en las instituciones educativas y universidades para ofrecer cursos tanto en línea como fuera de línea a los estudiantes, junto con la iniciativa de poner soluciones avanzadas a disposición de todo el personal y los estudiantes, está influyendo en la adopción de software académico. Esto está impulsando el crecimiento del mercado a lo largo de los años.

Los actores que operan en el mercado de software académico se centran en estrategias, como iniciativas de mercado, adquisiciones y lanzamientos de productos, para mantener sus posiciones en el mercado de software académico. Algunos desarrollos de los actores clave del mercado de software académico son:

En diciembre de 2020, la plataforma del sistema de información para estudiantes Alma introdujo la función de promedios de calificaciones (GPA), que se agregó a la herramienta del libro de calificaciones. La calificación basada en estándares (SBG) se basa en alinear la retroalimentación y la medición del progreso de los estudiantes con las habilidades particulares que se enseñan y evalúan, en lugar de usar una sola puntuación para cubrir múltiples temas o estándares.

En julio de 2020, ConexED actualizó su aplicación iOS 2.2.3 para ofrecer una experiencia más sencilla de usar. Esta aplicación permite a los estudiantes, el personal y el cuerpo docente participar en reuniones virtuales y videoconferencias desde sus dispositivos móviles.

Perspectivas regionales del mercado de software académico

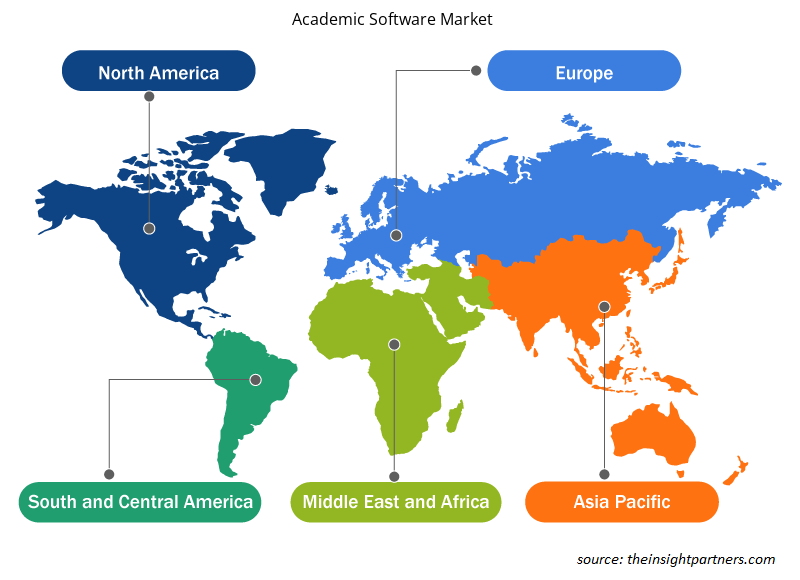

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de software académico durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de software académico en América del Norte, Europa, Asia Pacífico, Medio Oriente y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de software académico

Alcance del informe sobre el mercado de software académico

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2021 | US$ 797,59 millones |

| Tamaño del mercado en 2027 | US$ 2.007,08 millones |

| CAGR global (2021-2027) | 16,2% |

| Datos históricos | 2019-2020 |

| Período de pronóstico | 2022-2027 |

| Segmentos cubiertos |

Por implementación

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de software académico: comprensión de su impacto en la dinámica empresarial

El mercado de software académico está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de software académico son:

- Alma

- SOFTWARE DEL CAFÉ DEL CAMPUS

- ConexED

- Soluciones Envisio Inc.

- TELA COMPLETA

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de software académico

Mercado de software académico: por implementación

- Nube

- En las instalaciones

Mercado de software académico por aplicación

- Colegios y universidades

- Servicios Educativos

- Otros

Mercado de software académico por geografía

-

América del norte

- A NOSOTROS

- Canadá

- México

-

Europa

- Francia

- Alemania

- Rusia

- Reino Unido

- Italia

- Resto de Europa

-

Asia Pacífico (APAC)

- Porcelana

- India

- Japón

- Australia

- Corea del Sur

- Resto de APAC

-

Ministerio de Asuntos Exteriores

- Arabia Saudita

- Emiratos Árabes Unidos

- Sudáfrica

- Resto de MEA

-

SAM

- Brasil

- Argentina

- Resto de SAM

Mercado de software académico: perfiles de empresas

- Alma

- SOFTWARE DEL CAFÉ DEL CAMPUS

- ConexED

- Soluciones Envisio Inc.

- TELA COMPLETA

- Software de PowerVista, Inc.

- Qualtrics LLC

- Corporación Tophatmonocle

- Diálogo verdadero

- Colmena Wize

Ankita es una profesional dinámica en investigación de mercados y consultoría con más de 8 años de experiencia en los sectores de tecnología, medios de comunicación, TIC, electrónica y semiconductores. Ha liderado y ejecutado con éxito más de 100 proyectos de consultoría e investigación para clientes globales como Microsoft, Oracle, NEC Corporation, SAP, KPMG y Expeditors International. Sus principales competencias incluyen la evaluación de mercado, el análisis de datos, la previsión, la formulación de estrategias, la inteligencia competitiva y la redacción de informes.

Ankita es experta en la gestión de ciclos completos de proyecto, desde el diseño de propuestas de preventa y las conversaciones con los clientes hasta la entrega de información práctica posventa. Es experta en la gestión de equipos multifuncionales, la estructuración de módulos de investigación complejos y la alineación de soluciones con los objetivos de negocio específicos del cliente. Sus excelentes habilidades de comunicación, liderazgo y presentación le han permitido obtener constantemente resultados orientados al valor en entornos de mercado dinámicos y en constante evolución.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias