Rapporto sull’analisi delle dimensioni e delle quote del mercato Plastic to Fuel | Previsioni 2031

Dimensioni e previsioni del mercato della conversione della plastica in carburante (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tecnologia [pirolisi, gassificazione e depolimerizzazione] e prodotto finale [petrolio greggio, idrogeno e altri] e geografia.

- Stato : Dati rilasciati

- Codice del report : TIPRE00008127

- Categoria : Energia e potenza

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 15, 2025

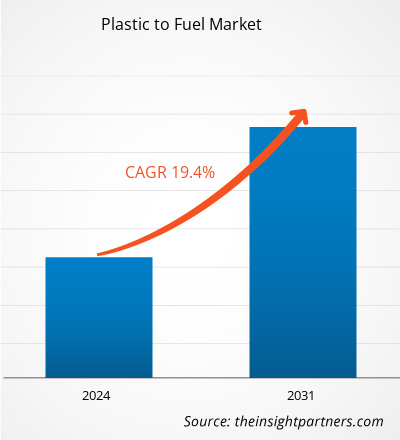

Si prevede che la dimensione del mercato della conversione della plastica in carburante raggiungerà 1.194,48 milioni di dollari entro il 2031, rispetto ai 289,55 milioni di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 19,4% nel 2023-2031. È probabile che il continuo sviluppo tecnico nel riciclaggio e nello smaltimento dei rifiuti rimanga una tendenza chiave del mercato della conversione della plastica in carburante.

Analisi del mercato della plastica al carburante

Si prevede che la crescente consapevolezza riguardo alle emissioni di gas serra guiderà la crescita della plastica nel mercato dei carburanti. I polimeri non riciclabili come il polietilene tereftalato (PET), il polistirene e il cloruro di polivinile (PVC) sono attualmente la preoccupazione principale. Oltre il ~90% della plastica non viene riciclata e viene scartata, messa in discarica o versata nell'oceano. Solo il 9-10% dei rifiuti di plastica è stato raccolto e riciclato, il che implica che solo il 9-10% dei rifiuti di plastica è stato raccolto e riciclato. Ciò apre un enorme potenziale di mercato per l'industria della plastica in carburante poiché il riciclaggio di questi rifiuti di plastica produrrà rifiuti di plastica non riciclabili che possono essere utilizzati in PFT in un futuro non troppo lontano.

Panoramica del mercato della plastica al carburante

Con la crescita della popolazione, il rapido sviluppo economico, la continua urbanizzazione e i cambiamenti nello stile di vita, la produzione e il consumo di rifiuti di plastica stanno aumentando a un ritmo elevato. I rifiuti di plastica sono diventati una preoccupazione crescente in tutto il mondo negli ultimi anni. Con una crescente dipendenza dalla plastica, la pratica di scartare la plastica in modo sconsiderato è diventata convenzionale. Numerose procedure di conversione dei rifiuti in ricchezza sono state create nel corso degli anni per riciclare e riutilizzare la plastica in modi innovativi. Convertire i rifiuti di plastica in carburante e renderli utilizzabili sia per esigenze industriali che residenziali è una delle innovazioni attuali. La conversione della plastica in carburante è stata precedentemente eseguita efficacemente in paesi come Germania, Stati Uniti e Giappone. Questi tre sono stati anche efficienti nel trasformare le procedure di conversione in modelli aziendali fattibili. Allo stesso modo, paesi come Canada e India stanno progressivamente adottando il processo di conversione della plastica in carburante.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della plastica al carburante: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato della plastica come carburante

L'aumento del fabbisogno energetico spinge la domanda di tecnologie per trasformare la plastica in carburante

L'elettricità svolge un ruolo cruciale e detiene una quota crescente di servizi energetici. Con l'aumento del reddito disponibile, la consapevolezza dei consumatori, l'elettrificazione dei trasporti e del riscaldamento e un aumento della domanda di gadget digitali e aria condizionata, si stima che la domanda di energia aumenterà ulteriormente. Le politiche governative e la tecnologia disponibile lavorano in linea con lo scenario delle politiche per spostare l'approvvigionamento energetico verso fonti a basse emissioni di carbonio, il che sta aumentando la domanda di tecnologia di plastica per alimentare a livello globale. L'accessibilità commerciale di una gamma di tecnologie di generazione a basse emissioni pone l'elettricità in prima linea negli sforzi per combattere il cambiamento climatico e l'inquinamento, il che sta aumentando la domanda di soluzioni alternative, determinando così l'espansione del mercato della plastica per alimentare.

Introduzione del processo Go Green: un'opportunità nel mercato della plastica per carburante

Le iniziative di conversione della plastica in carburante stanno iniziando a prendere piede nel settore energetico, poiché sempre più persone stanno diventando consapevoli del danno ambientale provocato dalla plastica monouso e dalle inadeguate pratiche di riciclaggio delle persone. Ciò sta spingendo i ricercatori a cercare modi innovativi per smaltire la crescente produzione di plastica. Si prevede che un aumento dei sussidi governativi per lo sviluppo di tecnologie verdi e i tentativi di incoraggiare tali tecnologie attraverso finanziamenti estesi offriranno notevoli opportunità di crescita del mercato. Inoltre, le rigide normative sulla sicurezza energetica del governo stanno spingendo le aziende a investire in ricerche ecosostenibili. La conversione della plastica in carburante è un'opzione promettente non solo per ridurre l'inquinamento, ma anche per apportare importanti benefici economici alle regioni.

Analisi della segmentazione del rapporto di mercato sulla trasformazione della plastica in carburante

I segmenti chiave che hanno contribuito all'analisi del mercato della trasformazione della plastica in carburante sono la tecnologia e il prodotto finale.

- In base alla tecnologia, il mercato della plastica per carburante è stato suddiviso in pirolisi, gassificazione e depolimerizzazione. Il segmento della pirolisi ha detenuto una quota di mercato maggiore nel 2023.

- In termini di prodotto finale, il mercato è stato segmentato in petrolio greggio, idrogeno e altri. Il segmento del petrolio greggio ha dominato il mercato nel 2023.

Analisi della quota di mercato della plastica per carburante per area geografica

L'ambito geografico del rapporto sul mercato della conversione della plastica in carburante è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa e Sud America/Sud e Centro America.

L'Asia Pacifica comprende molti paesi in via di sviluppo, tra cui Cina e India. Questi sono anche i due paesi più popolati al mondo. Questi rifiuti di plastica vengono scaricati nelle discariche o nell'oceano, popolando così l'ambiente e lasciando impatti negativi a lungo termine in tutto il mondo. Inoltre, l'Asia Pacifica detiene la quota maggiore di inquinamento marino da plastica con importanti contributori come Cina, Indonesia, Sri Lanka, Vietnam e Filippine. Infrastrutture di gestione dei rifiuti inefficienti e la mancanza di consapevolezza riguardo all'impatto negativo della plastica monouso sono le ragioni principali che contribuiscono all'aumento dei rifiuti di plastica nella regione. I crescenti investimenti da parte di governi e organizzazioni private per promuovere il riciclaggio della plastica in ulteriori materiali riutilizzabili stanno spingendo la crescita del mercato della plastica per carburante in tutta la regione. A causa dell'aumento degli investimenti nel riciclaggio dei rifiuti di plastica in tutta la regione, gli operatori del mercato della plastica per carburante stanno anche investendo nell'espansione della loro attività in tutta la regione, il che sta guidando la crescita del mercato della plastica per carburante nella regione Asia Pacifica.

Approfondimenti regionali sul mercato della plastica in carburante

Le tendenze regionali e i fattori che influenzano il mercato Plastic to Fuel durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato Plastic to Fuel in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato della plastica in carburante

Ambito del rapporto di mercato sulla conversione della plastica in carburante

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 289,55 milioni di dollari USA |

| Dimensioni del mercato entro il 2031 | 1.194,48 milioni di dollari USA |

| CAGR globale (2023-2031) | 19,4% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per tecnologia

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato Plastic to Fuel Market sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato della trasformazione della plastica in carburante sono:

- Agilyx, Inc

- Cassandra Oil AB

- Azienda

- Nexus Fuels LLC

- Tecnologie di riciclaggio Ltd.

- Agile Process Chemicals LLP

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato Plastic to Fuel

Notizie e sviluppi recenti sul mercato della plastica per carburante

Il mercato Plastic to Fuel viene valutato raccogliendo dati qualitativi e quantitativi post-ricerca primaria e secondaria, che includono importanti pubblicazioni aziendali, dati associativi e database. Di seguito è riportato un elenco di sviluppi nel mercato per innovazioni, espansione aziendale e strategie:

- Nel febbraio 2022, Agilyx e Virgin Group hanno collaborato per una partnership strategica volta alla ricerca e allo sviluppo di impianti di carburante a basse emissioni di carbonio per supportare la lotta all'inquinamento da plastica e sostenere l'agenda della transizione globale verso zero emissioni nette. (Fonte: Agilyx, Inc, comunicato stampa/sito Web aziendale/newsletter)

- Nel novembre 2022, Klean Industries ha collaborato con RGH Systems per sviluppare un impianto di conversione della plastica di scarto in energia nelle Filippine. (Fonte: Klean Industries Inc., comunicato stampa/sito Web aziendale/newsletter)

Copertura e risultati del rapporto sul mercato della plastica in carburante

Il rapporto “Dimensioni e previsioni del mercato della plastica per carburante (2021-2031)” fornisce un’analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni del mercato della plastica al carburante e previsioni a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Dinamiche di mercato come fattori trainanti, vincoli e opportunità chiave

- Tendenze del mercato della plastica come carburante

- Analisi PEST e SWOT dettagliate

- Analisi di mercato dalla plastica al carburante che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama e della concorrenza del settore della plastica per il carburante, che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti

- Profili aziendali dettagliati

Nivedita è una ricercatrice affermata con oltre 9 anni di esperienza in ricerche di mercato e consulenza aziendale. Attualmente Project Manager nel settore ICT presso The Insight Partners, vanta una profonda esperienza nella gestione e nell'esecuzione di incarichi di ricerca sindacati, personalizzati, in abbonamento e di consulenza in diversi settori tecnologici.

Con una comprovata esperienza nell'analisi basata sui dati e nella fornitura di insight fruibili, Nivedita ha contribuito in modo determinante a diversi progetti critici. Il suo lavoro include l'esecuzione end-to-end dei progetti, dalla comprensione degli obiettivi del cliente all'analisi delle tendenze di mercato, fino alla formulazione di raccomandazioni strategiche. Ha collaborato ampiamente con aziende leader nel settore ICT, aiutandole a identificare opportunità di mercato e a gestire i cambiamenti del settore.

Nivedita ha conseguito un MBA in Management presso IMS, Dehradun. Prima di entrare in The Insight Partners, ha maturato una preziosa esperienza presso MarketsandMarkets e Future Market Insights a Pune, dove ha ricoperto diversi ruoli di ricerca e ha costruito solide basi nell'analisi di settore e nel coinvolgimento dei clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative