オーガニックペットフード市場の分析と予測 - 規模、シェア、成長、トレンド 2028 年

2028年までのオーガニックペットフード市場予測 - COVID-19の影響と世界分析:動物種別(犬、猫、その他)、流通チャネル(ハイパーマーケット、スーパーマーケット、専門ペットショップ、オンライン、その他)、地域別

- ステータス : 出版

- レポートコード : TIPRE00013941

- カテゴリー : 食品と飲料

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : June 19, 2024

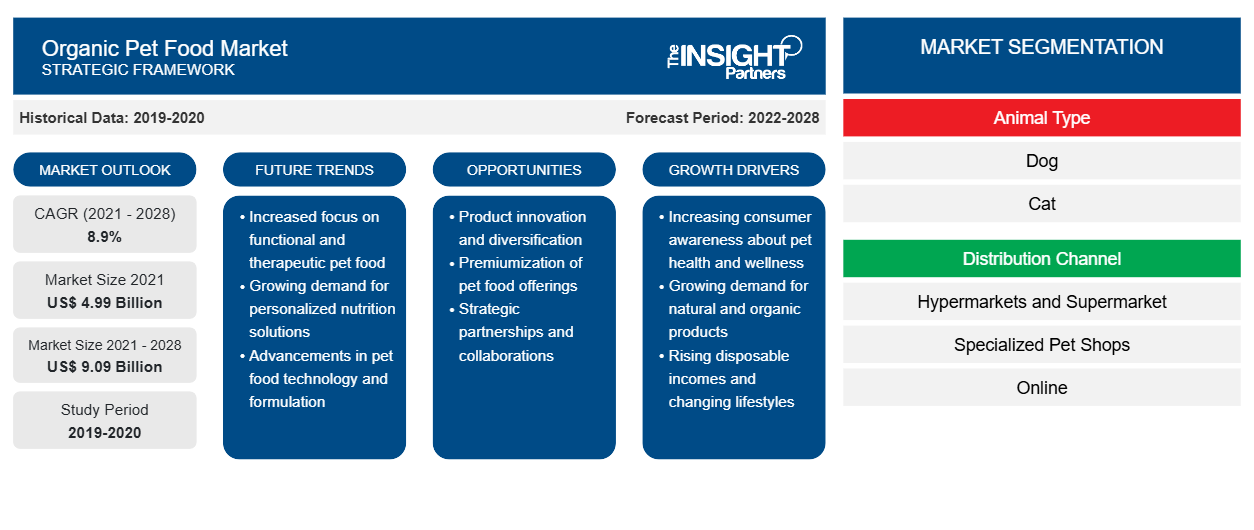

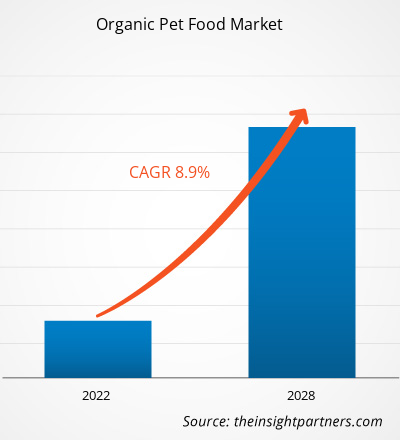

オーガニックペットフード市場は2021年に49億9,154万米ドルと評価され、2028年までに90億9,020万米ドルに達すると予測されており、2021年から2028年にかけて8.9%のCAGRで成長すると予想されています。

ペットの人間化が進み、ペット製品への支出が増えたことにより、オーガニック ペットフードの人気が高まっています。オーガニック製品を購入する消費者は、ペットに対しても同じ購入行動を取っています。消費者は、従来のペットフードに含まれる合成添加物や化学添加物の有害な副作用を防ぐために、クリーン ラベルのオーガニック ペットフードを求めています。

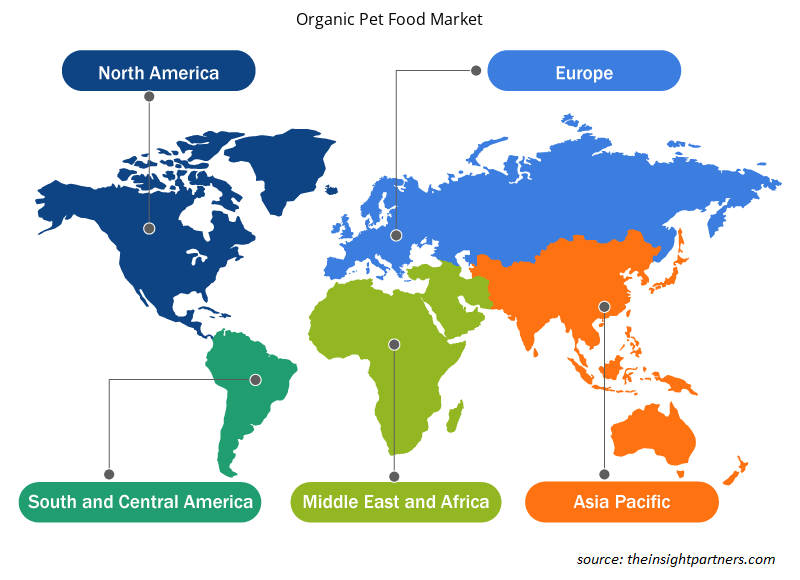

2020年、北米は世界のオーガニックペットフード市場で最大のシェアを占めました。しかし、アジア太平洋地域は予測期間中に市場で最も高いCAGRを記録すると予測されています。アジア太平洋市場は、中国、インド、日本、韓国、オーストラリアなど、いくつかの発展途上国と先進国で構成されています。これらの経済圏では、中流階級の人口が急増し、都市化が進んでいるため、オーガニックペットフード市場で活動する主要企業に有利な機会が提供されています。アジア太平洋地域でのペット人口の増加とオーガニックペットフードに対する消費者の傾向の高まりが、市場の成長を牽引しています。また、ペットの人間化の高まりも、予測期間中にアジア太平洋地域のオーガニックペットフード市場の成長を促進するでしょう。

要件に合わせてレポートをカスタマイズする

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

オーガニックペットフード市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

COVID-19パンデミックがオーガニックペットフード市場に与える影響

COVID-19パンデミックは、さまざまな地域での長期にわたるロックダウン、国際貿易への制限、製造ユニットの閉鎖、渡航禁止、サプライチェーンの制限、原材料不足により、運用効率の面で製造部門に大きな混乱をもたらしました。パンデミックは、製造ユニットの閉鎖、原材料価格の高騰、労働力不足、サプライチェーンの混乱、金融不安により、世界のオーガニックペットフード市場に影響を及ぼしました。さまざまな国の政府は、ウイルスの拡散を制限するために2020年初頭にロックダウンを実施し、それがオーガニックペットフードの生産に悪影響を及ぼしました。政府はペットフードメーカーに生産を遅らせるように求め、オーガニックペットフードを含む食品とペットフードの世界的な供給に悪影響を及ぼしました。しかし、2021年以降、APACのさまざまな国の政府は、人々にワクチン接種を提供し、新型コロナウイルスの拡散を抑制するための予防措置を講じています。政府も事業の再編、生産施設の再構築、オーガニックペットフードに必要な原材料の事前調達などを行い、需要と供給の不均衡を回避しています。また、パンデミックの間、電子商取引ネットワークは食品やペットフードの流通に大きな役割を果たしており、人々は主にオンラインで製品を購入することを好んでいます。

市場分析

食中毒の事例増加Foodborne Hazards

衛生的で健康的なペットフードは、ペットの健康を確保するための基本です。そのため、ペットの飼い主は高品質のペットフードを購入することを好みます。ホリスティック、オーガニック、ナチュラルと表示された食品は、従来の製品よりも顧客を引き付ける傾向があります。一般的に、ペットフードは、鶏の皮や骨など、食品加工業界の副産物で作られています。このような慣行は、使用された原材料に追加の抗生物質が誘発された場合、食中毒につながる可能性があります。ペットフードによって広がる可能性のある食中毒を防ぐために、取り扱いの最初のステップから最後のステップまでのペットフードのサプライチェーンを維持する必要があります。飼い主がペットに生のペットフードを与える場合、サルモネラ汚染の発生が頻繁に確認されています。さらに、食品の人工的な強化はペット動物の健康を害し、ブランド名に影響を与える可能性があります。たとえば、Fromm Family Foodsブランドは、犬に有害であると予想されるビタミンD含有量の潜在的な上昇により、2021年10月にドッグフードをリコールしました。オーガニックトレード協会(OTA)は、オーガニックペットフードの売上が人間用オーガニックフードの売上よりも高い伸びを報告しました。さらに、オーガニック ペットフード市場は、2007 年に Menu Foods Inc. がペットフードをリコールして米国で 14 匹の動物が死亡して以来、成長を続けています。オーガニック ペットフード市場は、従来のペットフードに対する顧客の不安から、売上が大幅に増加しました。そのため、オーガニック ペットフードは安全な選択肢として好まれています。したがって、予測期間中、市場は高い成長を遂げると予想されます。

製品タイプの洞察

製品タイプに基づいて、オーガニックペットフード市場は、ドライフード、ウェットフード、その他に分類されます。ドライフードセグメントは2020年に最大の市場シェアを占め、予測期間中に市場で最高のCAGRを記録すると予想されています。ドライフードは水分含有量が少なく、ペレット、キブル、フレークシリアルなど、さまざまな形で入手できます。ドライドッグフードは、肉や穀物などの材料を組み合わせて調理して作られます。ドライペットフードは、歯垢の蓄積を減らすことで、犬や猫の歯の健康を確保します。ドライペットフードは冷蔵する必要がないため、これが主な利点です。このフードには、毎日の栄養所要量に加えて、微量栄養素も含まれています。

ペットの種類に関する洞察

ペットの種類に基づいて、オーガニックペットフード市場は犬、猫、その他に分類されます。犬セグメントは2020年に最大の市場シェアを占めましたが、猫セグメントは予測期間中に市場で最高のCAGRを記録すると予想されています。猫は世界中の人々の間で人気のあるペットの1つです。猫は絶対肉食動物です。彼らの食事要件は他の動物とは異なります。タウリン、アルギニン、ヒスチジン、イソロイシン、ロイシン、リジン、メチオニン、フェニルアラニン、トレオニン、トリプトファン、バリンなどのアミノ酸は、猫の成長、繁殖、腸の健康、骨の健康に不可欠です。さらに、タウリンは一般的に動物ベースの食事に含まれています。さらに、猫は成長と健康のためにかなりの量のビタミンAを必要とします。オーガニックペットフードには現在、猫の成長と健康全般に不可欠なさまざまな微量栄養素が強化されており、猫用のオーガニックペットフードの需要が高まっています。植物由来のウェットフードおやつなどの革新的な製品は、オーガニックペットフード市場における猫部門の需要をさらに押し上げると期待されています。

流通チャネルの洞察

流通チャネルに基づいて、オーガニックペットフード市場は、スーパーマーケットとハイパーマーケット、専門店、オンライン小売、その他に分類されます。スーパーマーケットとハイパーマーケットセグメントは2020年に最大の市場シェアを占めましたが、オンライン小売セグメントは予測期間中に市場で最高のCAGRを記録すると予想されています。eコマースプラットフォームは、世界中の顧客にさまざまなカテゴリの幅広い製品を提供しています。消費者は、自宅やオフィスから選択した製品を購入できます。オンライン小売は、アクセスのしやすさ、幅広い製品の入手可能性、製品の配送、キャッシュバック、割引クーポン、魅力的な取引の点でこれらのチャネルが提供する利便性により、オーガニックペットフードの流通チャネルとして最も急速に成長しています。さらに、COVID-19パンデミックによる実店舗での買い物の制限により、オンライン小売セグメントの市場は今後数年間で顕著な成長が見込まれています。

オーガニックペットフード市場で活動する主要企業としては、Tender and True Pet Nutrition、Castor and Pollux Natural Petworks、Nestlé、Raw Paws Pet, Inc.、NATIVE PET、Primal Pet Foods、Yarrah Organic Petfood BV、Organic Paws、Petcurean、Evangersなどが挙げられます。これらの企業は、市場に幅広い製品ポートフォリオを提供しています。市場プレーヤーは、顧客の要件を満たす高品質で革新的な製品を開発しています。これらの企業は、オーガニックペットフードの需要の高まりに応えるために、ベストセラーの従来のペットフードのオーガニック版を導入しています。たとえば、植物由来のペットフード製品は現在、クランベリー、ビートルート、ニンジンなどのフレーバーで利用できるオーガニックラベル付きカテゴリーで導入されています。

オーガニックペットフード市場の地域別分析

予測期間を通じてオーガニック ペットフード市場に影響を与える地域的な傾向と要因は、Insight Partners のアナリストによって徹底的に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東、アフリカ、南米、中米にわたるオーガニック ペットフード市場のセグメントと地理についても説明します。

- オーガニックペットフード市場の地域別データを入手

オーガニックペットフード市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2021年の市場規模 | 49億9000万米ドル |

| 2028年までの市場規模 | 90億9000万米ドル |

| 世界のCAGR(2021年~2028年) | 8.9% |

| 履歴データ | 2019-2020 |

| 予測期間 | 2022-2028 |

| 対象セグメント |

動物の種類別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業プロフィール |

|

オーガニックペットフード市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

オーガニック ペットフード市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認識の高まりなどの要因により、エンドユーザーの需要が高まり、急速に成長しています。需要が高まるにつれて、企業は提供品を拡大し、消費者のニーズを満たすために革新し、新たなトレンドを活用し、市場の成長をさらに促進しています。

市場プレーヤー密度とは、特定の市場または業界内で活動している企業または会社の分布を指します。これは、特定の市場スペースに、その市場規模または総市場価値に対してどれだけの競合相手 (市場プレーヤー) が存在するかを示します。

オーガニックペットフード市場で事業を展開している主要企業は次のとおりです。

- 優しく真のペットの栄養

- カストル&ポルックス ナチュラルペットワークス

- ネスレ

- RAW PAWS PET 株式会社

- ネイティブペット

免責事項:上記の企業は、特定の順序でランク付けされていません。

- オーガニックペットフード市場のトップキープレーヤーの概要を入手

レポートの注目点

- オーガニックペットフード市場における進歩的な業界動向は、プレーヤーが効果的な長期戦略を策定するのに役立ちます。

- 先進国市場と発展途上国市場で採用されているビジネス成長戦略

- 2019年から2028年までのオーガニックペットフード市場の定量分析

- オーガニックペットフードの世界需要の推定

- 業界で活動するバイヤーとサプライヤーの有効性を示すポーターの5つの力の分析

- 競争市場の状況を理解するための最近の動向

- オーガニックペットフード市場の成長を牽引・抑制する要因と市場動向と展望

- 商業的利益の基盤となる市場戦略を強調し、市場の成長につながる意思決定プロセスを支援する

- さまざまなノードにおけるオーガニックペットフード市場規模

- 市場の詳細な概要とセグメンテーション、およびオーガニックペットフード業界の動向

- 有望な成長機会があるさまざまな地域のオーガニックペットフード市場の規模

オーガニックペットフード市場 – 製品タイプ別

- ドライフード

- ウェットフード

- その他

オーガニックペットフード市場 – ペットの種類別

- 犬

- 猫

- その他

オーガニックペットフード市場 – 流通チャネル別

- スーパーマーケットとハイパーマーケット

- 専門店

- オンライン小売

- その他

企業プロフィール

- 優しくて本物のペット栄養

- カストルとポルックス ナチュラルペットワークス

- ネスレ

- ローポーズペット株式会社

- ネイティブペット

- プライマルペットフーズ

- ヤラオーガニックペットフードBV

- オーガニック・ポーズ

- ペットキュリアン

- エヴァンジャーズ

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応