超薄型ガラス市場の規模、成長率、および2034年までの動向

超薄型ガラス市場規模と予測(2021~2034年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:製造プロセス(フロート法と溶融法)、用途(半導体基板、フラットパネルディスプレイおよびタッチコントロールデバイス、自動車用ガラス、その他)、最終用途産業(家電、自動車、医療・ヘルスケア、その他)、および地域別

- ステータス : 公開されたデータ

- レポートコード : TIPRE00009965

- カテゴリー : 化学薬品および材料

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : June 11, 2026

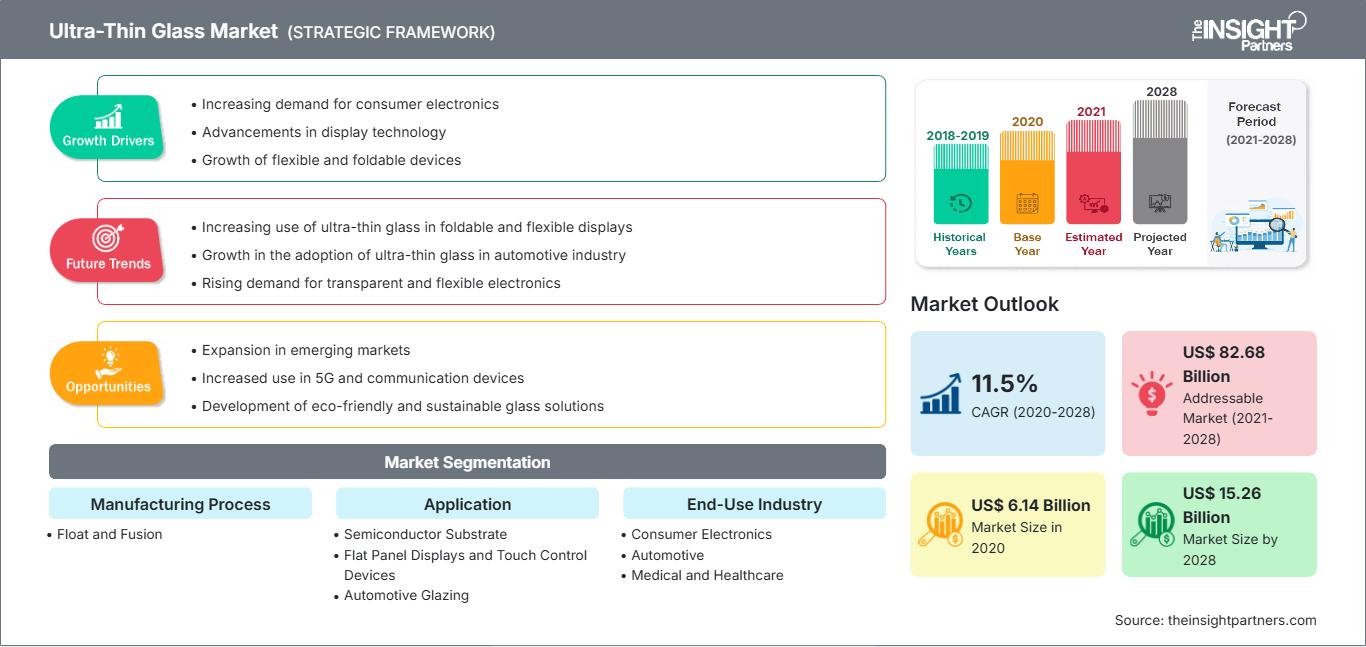

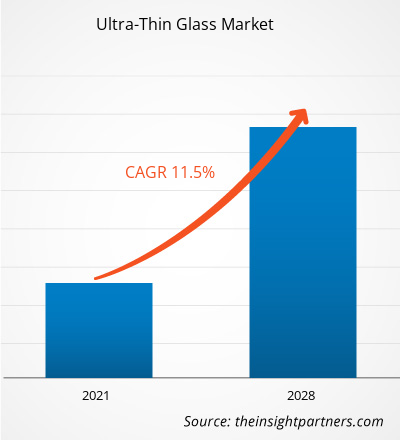

世界の超薄型ガラス市場規模は、2025年の234億4000万米ドルから、2034年には558億5000万米ドルに達すると予測されている。同市場は、2026年から2034年の予測期間中に年平均成長率(CAGR)10.13%を記録すると見込まれている。

市場の主要な動向としては、軽量かつ高性能な電子部品に対する世界的な注目度の高まり、プラスチックポリマーよりもガラスの優れた耐久性と耐傷性に対する消費者の意識の高まり、そして折りたたみ式およびフレキシブルなデバイスアーキテクチャへの大きなシフトが挙げられます。さらに、スマートコックピットを統合した電気自動車の人気上昇、5GおよびAIハードウェア向け半導体パッケージング要件の拡大、診断用バイオセンサーやウェアラブル健康モニターなどの高付加価値医療分野における超薄型ガラスの採用増加も、市場の追い風になると予想されます。

超薄型ガラス市場分析

極薄ガラス市場の分析によると、メーカー各社が光学的な透明度と機械的柔軟性を優先するにつれ、高付加価値の機能性基板へのシフトが見られます。市場は、従来型のフロートガラスを主体とした自動車およびディスプレイ分野に加え、プレミアムな折りたたみ式電子機器向けの高成長な溶融ガラス市場へと多様化しています。特殊半導体およびバイオテクノロジー分野では、極薄ガラスが有機材料に比べて優れた熱安定性と耐薬品性を持ち、明確な競争優位性を発揮するため、戦略的な機会が生まれています。市場の拡大は、精密切断時の歩留まり管理と、極めて脆弱なシートを取り扱う自動搬送システムの健全性にかかっています。現在、競争上の差別化は、イオン交換化学強化などの独自の強化技術や、反射防止および指紋防止のための多機能コーティングの提供能力によって際立っています。このアプローチにより、トップティアのガラスメーカーは、極めて高い技術精度が求められる市場で、より高い価格を設定することができます。

超薄型ガラス市場の概要

極薄ガラスは、ニッチな実験室用途から主流のハイテク産業製品へと進化を遂げました。市場には、スマートフォン用の超柔軟なカバーガラス、チップパッケージ用の高周波基板、航空宇宙産業や自動車産業向けの軽量ガラスなどが含まれます。世界的なガラスコングロマリットと専門の材料科学企業の両方がこの市場で競争しており、高度な製造技術を用いて人間の髪の毛よりも薄いガラスを製造しています。アジア太平洋地域と北米のテクノロジーに精通した消費者の間で、より洗練された、より持ち運びやすい電子機器への需要が高まっていることから、極薄ガラスは最高の保護およびインターフェースソリューションとして人気が高まっています。アジア太平洋地域は確立された電子機器製造拠点であるため収益でリードしており、北米は航空宇宙用途と医療機器のイノベーションで進歩しています。世界市場は、OLEDおよびマイクロLED技術の幅広い普及により、ディスプレイパネル生産が集中している地域で最も発展しています。ブランド間の競争はガラス組成のさらなるイノベーションを促進し、特殊なアルミノケイ酸塩およびホウケイ酸塩のバリエーションの導入につながっています。米国市場は、強固な半導体エコシステムと多数の家電大手企業が集積する地域に支えられ、材料イノベーションの中心地となっている。国内需要は、折りたたみ式フォームファクターと高度な半導体パッケージングにますます集中している。国内製造施設への戦略的な投資が、高精度ガラス基板の採用を促進している。

お客様のご要望に合わせてこのレポートをカスタマイズしてください

無料カスタマイズ超薄型ガラス市場:戦略的洞察

-

本レポートの主要市場トレンドをご覧ください。この無料サンプルには、市場動向から予測、見通しまで、幅広いデータ分析が含まれています。

超薄型ガラス市場の推進要因と機会

市場の推進要因:

- 優れた光学性能と機械的性能:極薄ガラスは、プラスチックフィルムよりも高い透明度と上質な触感を実現します。耐熱性、耐薬品性にも優れているため、現代の高精細ディスプレイの厳しい製造工程に最適です。

- 折りたたみ式フォームファクターの主流化:折りたたみ式スマートフォンやノートパソコンの普及に伴い、フレキシブルガラスへの需要は依然として高い水準を維持しています。消費者がフレキシブルデバイスへと移行するにつれ、超薄型ガラスはプラスチックポリイミドに比べて安定した販売量増加を続けています。

- 5Gと半導体技術の急速な発展:高周波データ伝送には、誘電損失の低い基板が求められる。5Gや高速コンピューティングのインフラを支えるため、超薄型ガラスが先進的な半導体パッケージングにますます採用されている。

市場機会:

- 自動車用ガラスおよびスマートインテリアへの展開:携帯機器にとどまらず、超薄型ガラスは、次世代電気自動車向けの軽量窓や大型曲面ダッシュボードディスプレイにおいて、大きな可能性を秘めている。

- 医療・バイオテクノロジー分野の成長:ガラスメーカーと医療機器メーカーが戦略的パートナーシップを締結することで、超薄型ガラスがマイクロ流体チップの安定した基板として機能する、高収益が見込めるポイントオブケア診断分野への参入が容易になる可能性がある。

- 持続可能なエネルギーへの多角化:軽量で柔軟なガラスを建材一体型太陽光発電(BIPV)や携帯型ソーラー充電器に活用することで、生産者が再生可能エネルギー分野をターゲットにする機会が拡大している。

超薄型ガラス市場レポートのセグメンテーション分析

超薄型ガラス市場の市場シェアは、その構造、成長可能性、および新たなトレンドをより明確に理解するために、さまざまなセグメントにわたって分析されています。以下は、ほとんどの業界レポートで使用されている標準的なセグメンテーション手法です。

製造工程別:

- フロートガラス:確立された大量生産能力と、0.1mmまでの薄さのガラスを生産する際のコスト効率の良さから、特に自動車用ガラスや大型ディスプレイ分野において、主要な販売量牽引役となっている。

- フュージョン:表面品質と厚み制御に優れたガラスを製造する、急速に成長している技術分野。研磨加工なしで、傷一つないタッチ感度の高い表面が求められる高級電子機器用途において、ますます好まれるようになっている。

申請方法:

- フラットパネルディスプレイおよびタッチコントロールデバイス:スマートフォン、タブレット、ハイエンドテレビに対する世界的な需要の恩恵を受け、超薄型ガラスの主要な用途分野であり続けている。

- 半導体基板:最も急速に成長している用途分野であり、特に高密度チップパッケージングやインターポーザーにおいて、より小型で効率的な電子部品の実現を可能にする。

- 自動車用ガラス:現代の車両デザインにおいて、軽量化と内装の美観向上を目的とした、厳選された用途が拡大しつつある分野です。

- その他:センサー、バイオテクノロジー用基質、太陽エネルギー部品などのニッチな用途を含む。

最終用途産業別:

- 家電製品:デバイスの小型化の継続的なサイクルと折りたたみ式スクリーン技術の台頭によって牽引される、最大のセクター。

- 自動車分野:車両の軽量化と車内空間のデジタル化の促進に重点を置いた、著しい成長分野。

- 医療・ヘルスケア分野:超薄型ガラスを用いて、高精度診断ツール、顕微鏡スライド、ウェアラブル医療センサーなどを製造する。

- その他:航空宇宙、防衛、特殊産業製造業などを含む。

地域別:

- 北米

- ヨーロッパ

- アジア太平洋地域

- 南米および中央アメリカ

- 中東・アフリカ

超薄型ガラス市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2025年の市場規模 | 234億4000万米ドル |

| 2034年までの市場規模 | 558億5000万米ドル |

| 世界の年間平均成長率(2026年~2034年) | 10.13% |

| 履歴データ | 2021年~2024年 |

| 予測期間 | 2026年~2034年 |

| 対象分野 |

製造工程による

|

| 対象地域および国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

超薄型ガラス市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

超薄型ガラス市場は、消費者の嗜好の変化、技術革新、製品の利点に対する認識の高まりといった要因によるエンドユーザー需要の増加を背景に、急速に成長しています。需要の高まりに伴い、企業は製品ラインナップを拡充し、消費者のニーズに応えるべく革新を進め、新たなトレンドを活用することで、市場の成長をさらに加速させています。

地域別超薄型ガラス市場シェア分析

アジア太平洋地域は今後数年間で最も急速な成長が見込まれる。北米とヨーロッパの新興市場にも、医療および自動車分野における高級ガラス用途の未開拓の機会が数多く存在する。

極薄ガラス市場は、ニッチな電子部品から多用途なハイテク素材へと、大きな変革期を迎えています。フレキシブルエレクトロニクスの需要急増と高級自動車分野の拡大が、この成長を牽引しています。以下に、地域別の市場シェアと動向の概要を示します。

1. 北アメリカ

- 市場シェア:折りたたみ式デバイスの早期導入とハイエンドの航空宇宙用途に牽引され、ニッチながらも急速に拡大しているセグメント。

-

主な推進要因:

- 世界的なテクノロジーのパイオニア企業が数多く存在し、高級スマートフォン市場も確立されている。

- AIを活用した半導体パッケージングにおいて、ガラス製インターポーザーの需要が高まっている。

- 高純度ガラス基板を必要とする医療・診断分野の拡大。

- トレンド:バイオテクノロジー応用への多額の投資と、軍事および産業用ウェアラブル機器向けの高耐久性超薄型ガラスの主流化。

2. ヨーロッパ

- 市場シェア:この地域のエリート自動車産業と持続可能な建築用ガラス分野に牽引され、相当なシェアを占めている。

-

主な推進要因:

- ドイツとフランスの自動車大手から、軽量で空力性能に優れたガラスに対する高い需要が見込まれる。

- 再生可能エネルギーおよび省エネルギー建築材料に関する研究開発の枠組みを確立した。

- 厳しい環境規制により、輸送における軽量化が求められている。

- トレンド:循環型経済の原則に戦略的に重点を置き、薄型ガラスのリサイクル性と、それを建築一体型太陽光発電(BIPV)に組み込むことを優先する。

3. アジア太平洋地域

- 市場シェア:世界最大のシェアを占めており、中国、韓国、台湾、日本といった世界で最も有力な電子機器製造拠点群がその中心となっている。

-

主な推進要因:

- OLEDおよびマイクロLEDパネルの生産施設が大規模に集中している。

- 半導体の自給自足と5Gインフラ整備に向けた政府主導の取り組み。

- 急速な都市化は、高級で超薄型の消費者向けテクノロジー製品への需要を高めている。

- トレンド:サプライチェーンへの依存度を低減するため、超薄型ガラス(UTG)の現地生産への戦略的な転換が進むとともに、高歩留まりのガラス切断のための製造分野における研究開発が活発化している。

4. 南米および中央アメリカ

- 市場シェア:ブラジルとチリで製造拠点が拡大している新興市場。

-

主な推進要因:

- 地域家電ブランド向けの組立ラインを拡張する。

- 自動車サプライチェーンの近代化:デジタルインテリアインターフェースの導入。

- トレンド:スマートフォンの現地仕上げ向けハイテクガラス板の輸入増加と、特殊な産業用センサー生産の増加。

5. 中東・アフリカ

- 市場シェア:発展途上市場は、正式な工業生産へと移行しつつある。

-

主な推進要因:

- 高度なディスプレイおよびガラスソリューションを必要とする都市(例:NEOM)への戦略的投資。

- 太陽光発電分野、特に高効率・軽量パネルの分野での成長。

- トレンド:アジアの製造業とEMEA(欧州・中東・アフリカ)地域の需要とのギャップを埋めるため、最新の物流・仕上げ拠点を導入する。

超薄型ガラス市場で事業を展開する主要企業は以下のとおりです。

- コーニング株式会社

- AGC株式会社

- 日本電気硝子株式会社

- ショットAG

- セントラル・グラス株式会社

- CSGホールディング株式会社

- エマージグラス

- 日本板硝子株式会社

- 新義ガラスホールディングス株式会社

- 洛陽ガラス有限公司

免責事項:上記に掲載されている企業は、特定の順序でランク付けされているわけではありません。

超薄型ガラス市場のニュースと最新動向

- 2025年11月、アルペン・ハイパフォーマンス・プロダクツ(アルペン)は、ガラス、セラミック、材料科学分野における世界有数のイノベーターであるコーニング社との提携を発表しました。この提携に基づき、アルペンはコーニング社のEnlighten™ガラスを、アルペンのトリプルガラスおよびクワッドガラスユニットの超薄型中央パネルとして採用し、米国市場向け次世代窓の商業化を支援します。

- 日本電気硝子株式会社は2025年9月、化学強化専用に設計された超薄型ガラスシート「Dinorex UTG™」が、HONORの最新折りたたみ式スマートフォン「Magic V Flip2」の内部メインディスプレイのカバーに採用されたことを発表しました。HONORは、世界的に急速に認知度を高めているスマートデバイスメーカーです。

超薄型ガラス市場レポートの対象範囲と成果物

超薄型ガラス市場規模と予測(2021年~2034年)レポートでは、以下の分野を網羅した市場の詳細な分析を提供しています。

- 超薄型ガラス市場の規模と予測(世界、地域、国レベル)を、調査範囲に含まれるすべての主要市場セグメントについて分析します。

- 超薄型ガラス市場の動向、および推進要因、阻害要因、主要な機会などの市場ダイナミクス

- 詳細なPEST分析とSWOT分析

- 超薄型ガラス市場の分析:主要な市場動向、世界および地域的な枠組み、主要企業、規制、および最近の市場動向を網羅

- 超薄型ガラス市場における市場集中度、ヒートマップ分析、主要企業、および最近の動向を網羅した業界概況および競争分析。

- 詳細な企業プロフィール

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応