Ultra-Thin Glass Market Size, Growth & Trends by 2034

Coverage: By Manufacturing Process (Float and Fusion), Application (Semiconductor Substrate, Flat Panel Displays and Touch Control Devices, Automotive Glazing, and Others), and End-Use Industry (Consumer Electronics, Automotive, Medical and Healthcare, and Others), and Geography

- Status : Data Released

- Report Code : TIPRE00009965

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : June 15, 2026

2025 Market Size

US$ 23.44 Bn

Base year value

2034 Forecast

US$ 55.85 Bn

Projected by 2034

CAGR 2026-2034

10.13 %

Growth rate

Addressable Market

US$ 352.47 Bn

(2026-2034)

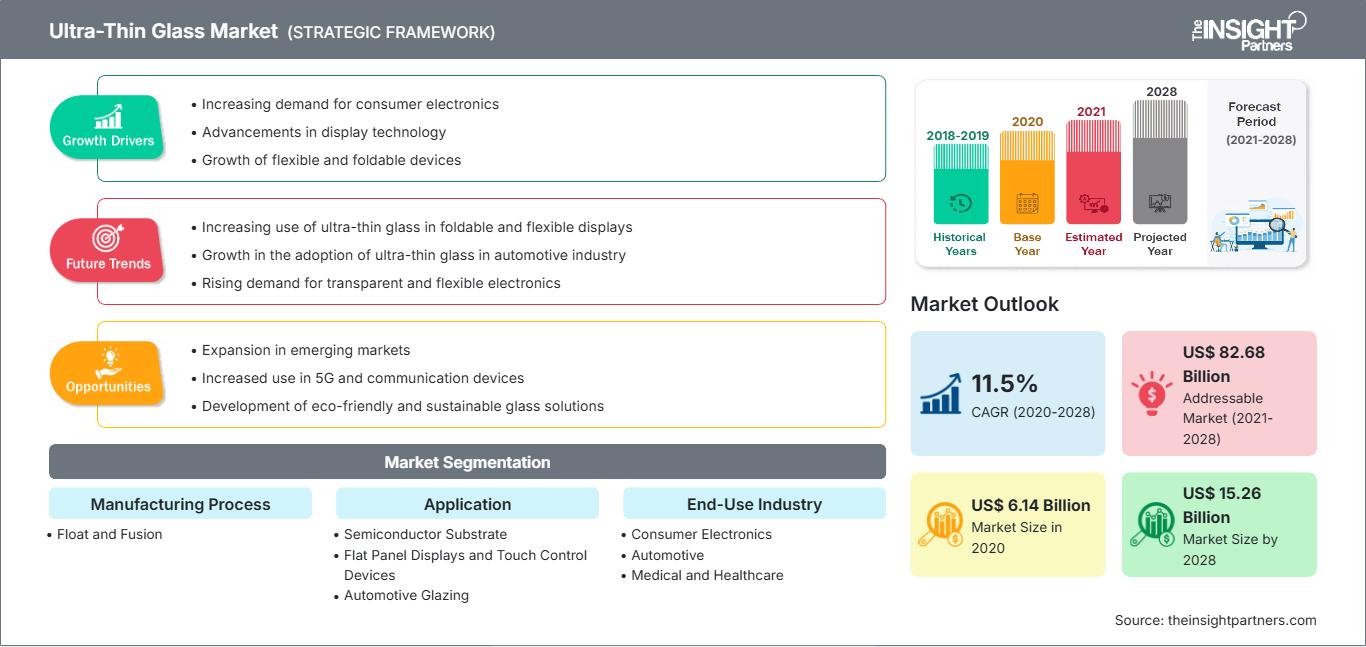

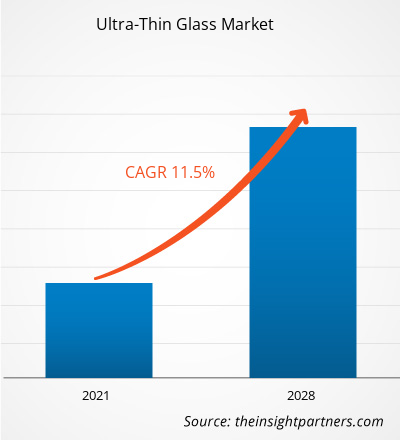

The global ultra-thin glass market size is projected to reach US$ 55.85 billion by 2034 from US$ 23.44 billion in 2025. The market is anticipated to register a CAGR of 10.13% during the forecast period 2026–2034.

Key market dynamics include a heightening global focus on lightweight and high-performance electronic components, rising consumer awareness regarding the superior durability and scratch resistance of glass over plastic polymers, and a significant shift toward foldable and flexible device architectures. Additionally, the market is expected to benefit from the growing popularity of electric vehicles with integrated smart cockpits, expansion in semiconductor packaging requirements for 5G and AI hardware, and the increasing inclusion of ultra-thin glass in high-value medical segments like diagnostic biosensors and wearable health monitors.

Ultra-Thin Glass Market Analysis

The ultra-thin glass market analysis shows a shift toward high-value functional substrates as manufacturers prioritize optical clarity and mechanical flexibility. The market is diversifying into traditional float-led automotive and display sectors and high-growth fusion-draw markets for premium foldable electronics. Strategic opportunities are emerging in specialty semiconductor and biotechnology applications, where ultra-thin glass’s superior thermal stability and chemical resistance compared to organic alternatives offer a clear competitive advantage. The market expansion depends on yield management during precision cutting and the integrity of automated handling systems for ultra-fragile sheets. Competitive differentiation now stands out depending on proprietary strengthening techniques like ion-exchange chemical tempering and the ability to provide multi-functional coatings for anti-reflection and fingerprint resistance. This approach helps top-tier glass manufacturers charge higher prices in a market requiring extreme technical precision.

Ultra-Thin Glass Market Overview

Ultra-thin glass has evolved from niche laboratory applications to mainstream high-tech industrial products. The market includes ultra-flexible cover glass for smartphones, high-frequency substrates for chip packaging, and lightweight glazing for the aerospace and automotive industries. Both global glass conglomerates and specialized material science firms compete in this market, using advanced manufacturing techniques to produce glass thinner than a human hair. Growing demand for sleeker, more portable electronics among tech-savvy consumers in Asia-Pacific and North America has increased the popularity of ultra-thin glass as a premier protection and interface solution. Asia-Pacific leads in revenue due to its established electronics manufacturing hub, while North America is advancing in aerospace applications and medical device innovation. The global market is the most developed in regions with high concentrations of display panel production, driven by the broad availability of OLED and Micro-LED technologies. Competition among brands is fueling greater innovation in glass composition, leading to the inclusion of specialized aluminosilicate and borosilicate variants. The US market is a primary hub for material innovation, underpinned by a robust semiconductor ecosystem and a high concentration of consumer electronics giants. Domestic demand is increasingly centered on foldable form factors and advanced semiconductor packaging. Strategic investments in local fabrication facilities are fueling the adoption of high-precision glass substrates.

Market Assessment and Insights

- Global market for Ultra-Thin Glass was valued at US$ 23.44 Billion in 2025

- Annual market size is expected to reach US$ 55.85 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 352.47 Billion

- Market is anticipated to register a CAGR of 10.13% during the forecast period

- The United States represents a key market, supported by Increasing demand for consumer electronics, Advancements in display technology, Growth of flexible and foldable devices, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion in emerging markets, Increased use in 5G and communication devices, Development of eco-friendly and sustainable glass solutions are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Corning Incorporated, AGC Inc., Nippon Electric Glass Co., Ltd., SCHOTT AG, Central Glass Co., Ltd., CSG Holding Co., Ltd., Emerge Glass, Nippon Sheet Glass Co., Ltd, Xinyi Glass Holdings Limited, Luoyang Glass Co., Ltd., while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Ultra-Thin Glass Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Ultra-Thin Glass Market Drivers and Opportunities

Market Drivers:

- Superior Optical and Mechanical Performance: Ultra-thin glass provides better transparency and a more premium tactile feel than plastic films. Its resistance to heat and chemicals makes it ideal for the rigorous manufacturing processes of modern high-definition displays.

- Mainstreaming of Foldable Form Factors: The expansion of the foldable smartphone and laptop category has sustained high demand for flexible glass inputs. As consumers trade up to flexible devices, ultra-thin glass continues to see stable volume gains over plastic polyimides.

- Rapid Expansion of 5G and Semiconductor Technologies: High-frequency data transmission requires substrates with low dielectric loss. Ultra-thin glass is increasingly adopted in advanced semiconductor packaging to support the infrastructure of 5G and high-speed computing.

Market Opportunities:

- Expansion into Automotive Glazing and Smart Interiors: Beyond handheld devices, ultra-thin glass offers significant opportunities in lightweight windows and large-scale curved dashboard displays for next-generation electric vehicles.

- Growth in Medical and Biotech Segments: Forming strategic partnerships between glass manufacturers and medical device firms may facilitate access to high-margin segments in point-of-care diagnostics, where ultra-thin glass serves as a stable substrate for microfluidic chips.

- Diversification into Sustainable Energy: There is a growing opportunity for producers to target the renewable energy sector through lightweight, flexible glass for building-integrated photovoltaics (BIPV) and portable solar chargers.

Ultra-Thin Glass Market Report Segmentation Analysis

The Ultra-Thin Glass Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Manufacturing Process:

- Float: The dominant volume driver, particularly within the automotive glazing and large-scale display sectors, due to established high-volume production capabilities and cost efficiencies in producing glass thicknesses down to 0.1 mm.

- Fusion: A fast-growing technical segment that produces glass with superior surface quality and thickness control. It is increasingly preferred for premium electronic applications where pristine, touch-sensitive surfaces are required without additional polishing.

By Application:

- Flat Panel Displays and Touch Control Devices: Remains the primary channel for ultra-thin glass usage, benefiting from the global demand for smartphones, tablets, and high-end televisions.

- Semiconductor Substrate: The fastest-rising application segment, especially for high-density chip packaging and interposers, enabling more compact and efficient electronic components.

- Automotive Glazing: Offers a select but growing range of applications for weight reduction and interior aesthetic enhancement in modern vehicle design.

- Others: Includes niche uses in sensors, biotechnology substrates, and solar energy components.

By End-Use Industry:

- Consumer Electronics: The largest sector, driven by the continuous cycle of device miniaturization and the rise of foldable screen technology.

- Automotive: A significant growth area focusing on reducing vehicle curb weight and enhancing the digitalization of car cabins.

- Medical and Healthcare: Utilizes ultra-thin glass for high-precision diagnostic tools, microscope slides, and wearable medical sensors.

- Others: Encompasses aerospace, defense, and specialized industrial manufacturing.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Ultra-Thin Glass Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 23.44 Billion |

| Market Size by 2034 | US$ 55.85 Billion |

| Global CAGR (2026 - 2034) | 10.13% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Manufacturing Process

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Ultra-Thin Glass Market Players Density: Understanding Its Impact on Business Dynamics

The Ultra-Thin Glass Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Ultra-Thin Glass Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in North America and Europe also have many untapped opportunities for premium glass applications in the medical and automotive sectors.

The ultra-thin glass market is undergoing a significant transformation, moving from a niche electronic component to a versatile high-tech material. Growth is driven by the surge in flexible electronics demand and the expansion of the premium automotive sector. Below is a summary of market share and trends by region:

1. North America

- Market Share: A niche but rapidly expanding segment, driven by early adoption of foldable devices and high-end aerospace applications.

- Key Drivers:

- Strong presence of global tech pioneers and an established luxury smartphone market.

- Rising demand for glass interposers in AI-driven semiconductor packaging.

- Expansion of medical and diagnostic sectors requiring high-purity glass substrates.

- Trends: Significant investment in biotechnology applications and the mainstreaming of ruggedized ultra-thin glass for military and industrial wearables.

2. Europe

- Market Share: Holds a substantial share, primarily driven by the region's elite automotive industry and sustainable architectural glass sectors.

- Key Drivers:

- High demand for lightweight, aerodynamic glazing from automotive giants in Germany and France.

- Established R&D framework for renewable energy and energy-efficient building materials.

- Strict environmental regulations are pushing for weight reduction in transport.

- Trends: A strategic focus on circular economy principles, prioritizing the recyclability of thin glass and its integration into building-integrated photovoltaics (BIPV).

3. Asia-Pacific

- Market Share: Holds the largest share globally, anchored by the world’s most dominant electronics manufacturing clusters in China, South Korea, Taiwan, and Japan.

- Key Drivers:

- Massive concentration of OLED and Micro-LED panel production facilities.

- Government-led initiatives for semiconductor self-sufficiency and 5G infrastructure.

- Rapid urbanization is fueling demand for premium, ultra-slim consumer tech.

- Trends: A strategic shift toward localized production of Ultra-Thin Glass (UTG) to reduce supply chain dependency, alongside heavy R&D in manufacturing for high-yield glass cutting.

4. South & Central America

- Market Share: Emerging market with a growing manufacturing footprint in Brazil and Chile.

- Key Drivers:

- Expanding assembly lines for regional consumer electronics brands.

- Modernization of the automotive supply chain to include digital interior interfaces.

- Trends: Increasing import of high-tech glass sheets for localized smartphone finishing and a rise in specialized industrial sensor production.

5. Middle East & Africa

- Market Share: Developing market transitioning toward formalized industrial production.

- Key Drivers:

- Strategic investments in cities (e.g., NEOM) requiring advanced display and glazing solutions.

- Growth in the solar energy sector, particularly for high-efficiency, lightweight panels.

- Trends: Implementation of modern logistics and finishing hubs to bridge the gap between Asian manufacturing and EMEA demand.

Major Companies operating in the Ultra-Thin Glass Market are:

- Corning Incorporated

- AGC Inc.

- Nippon Electric Glass Co., Ltd.

- SCHOTT AG

- Central Glass Co., Ltd.

- CSG Holding Co., Ltd.

- Emerge Glass

- Nippon Sheet Glass Co., Ltd

- Xinyi Glass Holdings Limited

- Luoyang Glass Co., Ltd.

Disclaimer: The companies listed above are not ranked in any particular order.

Ultra-Thin Glass Market News and Recent Developments

- In November 2025, Alpen High Performance Products (Alpen) announced a collaboration with Corning Incorporated, one of the world's leading innovators in glass, ceramic, and materials science. Under the collaboration, Alpen will use Corning® Enlighten™ Glass as the ultra-thin center pane for Alpen's triple and quadruple-paned glass units, helping to commercialize next-generation windows for the U.S. market.

- In September 2025, Nippon Electric Glass Co., Ltd. announced that its ultra-thin glass sheet designed exclusively for chemical strengthening, Dinorex UTG™, has been adopted for the cover of the inner main display of HONOR’s latest foldable smartphone, the Magic V Flip2. HONOR is a smart device manufacturer that is rapidly gaining global recognition.

Ultra-Thin Glass Market Report Coverage and Deliverables

The Ultra-Thin Glass Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Ultra-Thin Glass Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Ultra-Thin Glass Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Ultra-Thin Glass Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Ultra-Thin Glass Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends