Housewares Market Dynamics and Trends by 2030

Coverage: By Product Type (Cookware and Bakeware, Tableware, Kitchen Appliances, Bathroom Essentials, and Others) and Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online Retail, and Others)

- Status : Published

- Report Code : TIPRE00030119

- Category : Consumer Goods

- No. of Pages : 150

- Available Report Formats :

- Last update date : June 12, 2024

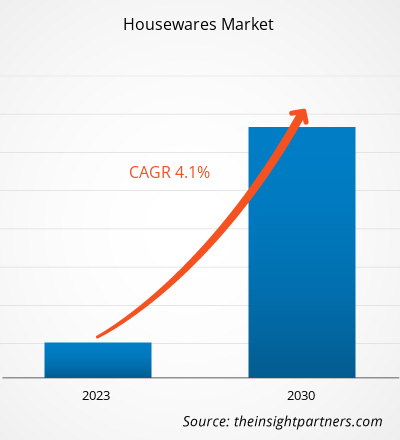

2022 Market Size

US$ 321.4 Bn

Base year value

2030 Forecast

US$ 442.51 Bn

Projected by 2030

CAGR 2023-2030

4.1 %

Growth rate

Addressable Market

US$ 3,093.88 Bn

(2023-2030)

[Research Report] The housewares market size was valued at US$ 321.40 billion in 2022 and is expected to reach US$ 442.51 billion by 2030; it is estimated to register a CAGR of 4.1% from 2022 to 2030.

Market Insights and Analyst View:

Housewares are products and items used within a household for cooking, baking, and home organization, among other purposes. The housewares market has been growing steadily due to factors such as changing lifestyles and more time spent at home, which have triggered the demand for functional and aesthetically pleasing housewares. During the COVID-19 pandemic, people spent more time at home and invested in improving their living spaces. Additionally, a rise of e-commerce and online shopping platforms has made it easier for consumers to access and buy a wide range of houseware products from their homes. These factors, coupled with innovative designs and sustainable options made available by houseware companies favor the expansion of the housewares market.

Growth Drivers and Challenges:

Dynamic changes in lifestyle and the rising dual-income families led to an upsurge in disposable incomes and improved living standards of households. With increasing disposable incomes, consumers spend significant amounts on housewares and other appliances supporting convenient living. They are often willing to purchase new products owing to their unique styles, which appeal to their individuality, resulting in a higher buying frequency. Moreover, a burgeoning number of single-person households triggers the need for home modifications, thereby driving the demand for housewares such as kitchen appliances, cookware, bakeware, tableware, and bathroom essentials.

Further, a rise in urbanization has been bolstering the demand for residential units and, ultimately, homewares products. As per the US Census Bureau and the US Department of Housing and Urban Development, the US completed construction of ~1,3 million housing units in 2021, whereas construction of ~1,7 million housing units was in progress. Similarly, rising urbanization in European countries has created a huge demand for residential housing. According to the European Commission, residential building permits increased by 42.3% from 2015 to 2021 in the European Union. In 2021, France, Germany, and Poland accounted for the most commencements of residential construction in Europe. Thus, the increasing construction of housing units across various countries further boosts the demand for housewares. Thus, the increasing purchase of housewares along with the rising number of households propels the housewares market growth.

However, the housewares market is highly fragmented and disorganized due to many untapped small private enterprises and street vendors operating in developing countries. According to an article published in Business Standards, as of 2020, 80% of the kitchenware market was unorganized in India. Local small businesses use low-quality raw materials to manufacture housewares such as cookware, bakeware, bathroom accessories, and tableware. The usage of low-quality raw materials results in poor-quality end products that are prone to damage. Also, manufacturers offer these products at low costs; therefore, the majority of consumers buy these products due to affordability and easy availability. This factor results in the shrinkage of the customer base of major houseware manufacturers.

Further, more often, local manufacturers in the unorganized housewares market do not comply with the regulatory standards, which can raise quality issues and hamper the perception of consumers toward houseware products. Further, the availability of counterfeit products can hamper the brand image of key players. Thus, the lack of uniformity in operations and regulations hampers the growth of the housewares market.

Market Research Highlights

- Asia Pacific dominated the market with 37.5% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 4.7% over the forecast period.

- United States market is projected to grow at a CAGR of 2.9% over the forecast period.

- By Product Type, the Kitchen Appliances segment accounted for the largest market share of 46.1% in 2022.

- By Distribution Channel, the Online Retail segment is anticipated to witness the fastest growth, registering a CAGR of 4.9% over the forecast period

- The report profiles key industry players such as Inter IKEA Holding BV, BSH Hausgerate GmbH, Newell Brands Inc, Kohler Co, Haier US Appliance Solutions Inc, Bradshaw Home Inc, The Denby Pottery Co Ltd, Hutzler Manufacturing Co Inc, TTK Prestige Ltd, HF Coors Co Inc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Housewares Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Report Segmentation and Scope:

The global housewares market is segmented on the basis of product type, distribution channel, and geography. Based on product type, the market is categorized into cookware and bakeware, tableware, kitchen appliances, bathroom essentials, and others. By distribution channel, the market is categorized into supermarkets and hypermarkets, specialty stores, online retail, and others. By geography, the global housewares market is broadly segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America.

Segmental Analysis:

Based on product type, the housewares market is categorized into cookware and bakeware, tableware, kitchen appliances, bathroom essentials, and others. The tableware segment is expected to register the highest CAGR during 2022–2030. The tableware segment includes products such as crockery, cutlery, glassware, and serveware. A surge in demand for tableware in the housewares market can be attributed to transformed dining habits during the COVID-19 pandemic. With more people dining at home, people have started focusing on aesthetic and functional tableware, as it enhances home dining experiences. From everyday meals to special gatherings, consumers are looking for tableware sets that elevate their dining experience. Furthermore, the growing appreciation for unique and artisanal designs plays a significant role in driving the demand for tableware. Consumers are increasingly drawn to handcrafted and artistically inspired tableware pieces that bring a touch of individuality and personality to their dining settings. Thus, a shift toward more personalized and visually striking tableware choices has contributed to the progress of the housewares market for the tableware segment. Vivo - Villeroy & Boch Group, Corelle, Pyrex, Luminarc, and Schott Zwiesel are a few of the prominent players operating in the market for tableware.

Regional Analysis:

The housewares market is segmented into five key regions: North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa. Asia Pacific dominated the global housewares market in 2022 as the market in this region was valued at US$ 120.63 billion in that year. Europe is a second major contributor, holding more than 23% share of the global market. Asia Pacific is expected to register a considerable CAGR of over 5% during 2022–2030. The growing urbanization and disposable income of the middle-class population is a prime factor propelling the demand for modern and convenient housewares, including advanced kitchen appliances and stylish tableware.

Housewares Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 321.4 Billion |

| Market Size by 2030 | US$ 442.51 Billion |

| Global CAGR (2022 - 2030) | 4.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Housewares Market Players Density: Understanding Its Impact on Business Dynamics

The Housewares Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

COVID-19 Pandemic Impact:

The COVID-19 pandemic initially hindered the global housewares market due to the shutdown of manufacturing units, shortage of labor, disruption of supply chains, and financial instability. The disruption of operations in various industries due to the economic slowdown caused by the COVID-19 outbreak restrained the housewares supply. Moreover, various stores were closed, which limited the sales of housewares. Nevertheless, businesses started gaining ground as previously imposed limitations were revoked across various countries in 2021. Moreover, the implementation of COVID-19 vaccination drives by governments of different countries eased the situation, leading to a rise in business activities worldwide. Several markets, including the housewares market, reported growth after the ease of lockdowns and movement restrictions.

Competitive Landscape and Key Companies:

Bradshaw Home Inc, Denby Pottery, HF Coors Co Inc, Inter Ikea Holding Bv, Hutzler Manufacturing Co Inc, TTK Prestige Ltd, Newell Brands Inc, BSH Hausgerate GmbH, Kohler Co, and Haier US Appliance Solutions Inc are among the prominent players operating in the global housewares market.

Frequently Asked Questions

Energy-saving appliances, notifications enabled on connected devices, and Wi-Fi capabilities are the key functional upgrades in smart kitchen appliances. For example, smart microwaves can seamlessly download cooking instructions, read barcodes on food products, and offer AI voice assistants to enable a completely hands-free experience. Whirlpool, in January 2022, announced that some of its smart, Wi-Fi-connected microwave would be upgraded to incorporate an air fry mode via a software update to replicate the crispy reheating specifications. Thus, the incorporation of innovative technologies into housewares is likely to bring new trends in the housewares market in the coming years.

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends