Independent Software Vendors (ISVs) Market Size, Trends & Demand by 2034

Independent Software Vendors (ISVs) Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Deployment (Cloud, On-Premise); Industry (BFSI, Healthcare, IT and Telecom, Retail, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Status : Data Released

- Report Code : TIPRE00011709

- Category : Technology, Media and Telecommunications

- No. of Pages : 150

- Available Report Formats :

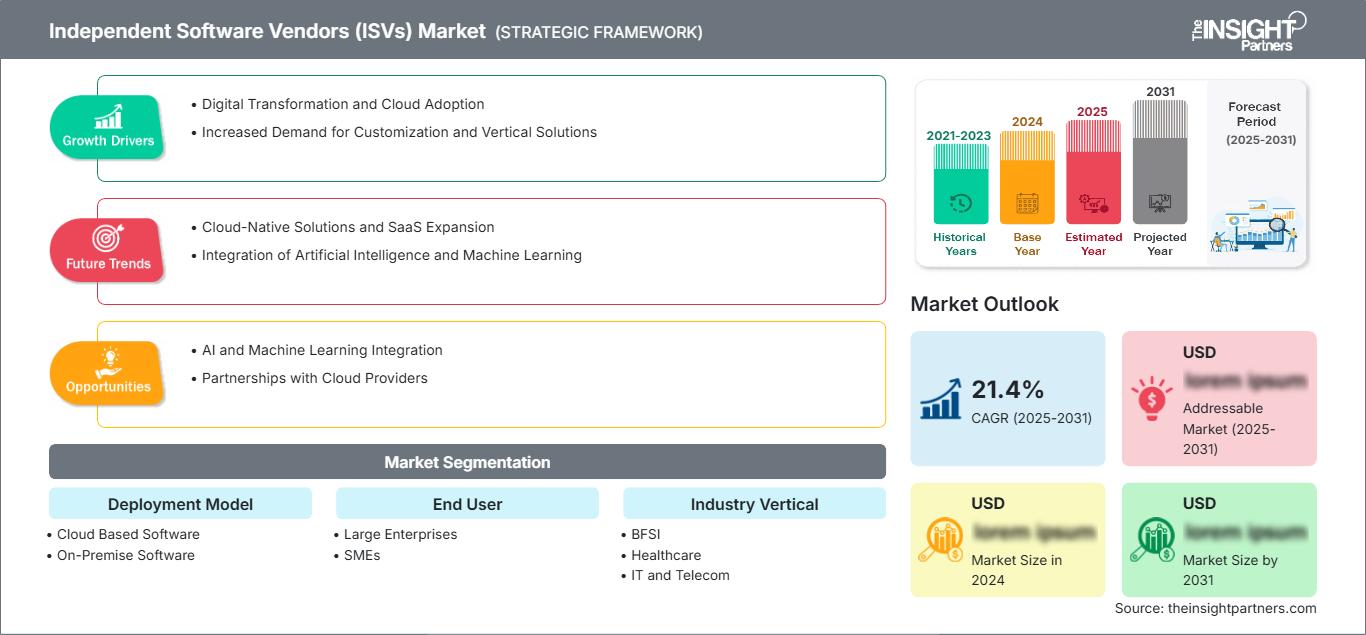

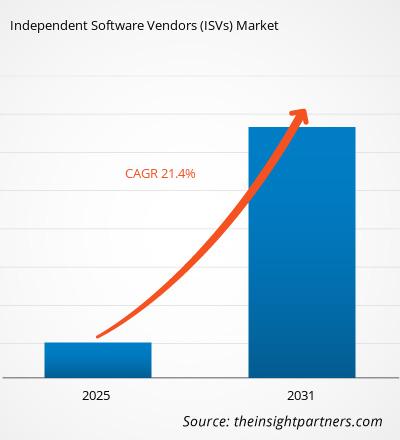

The global Independent Software Vendors (ISVs) Market size is projected to reach US$ 4,605.66 billion by 2034 from US$ 2,133.81 billion in 2025. The market is anticipated to register a CAGR of 13.26% during the forecast period 2026–2034

Key market dynamics include a heightening global focus on digital transformation mandates, rising enterprise demand for specialized, niche software applications, and a significant shift toward cloud-native architectures. Additionally, the market is expected to benefit from the growing integration of Artificial Intelligence (AI) and Machine Learning (ML) into software products, the expansion of global partner ecosystems through cloud marketplaces, and the increasing adoption of low-code/no-code platforms that accelerate the software development lifecycle.

Independent Software Vendors (ISVs) Market Analysis

The independent software vendors market analysis shows a strategic shift toward vertical-specific Vertical SaaS solutions as enterprises move away from one-size-fits-all software models. Organizations are increasingly seeking tailored applications that address specific operational challenges in regulated industries like healthcare and finance, where ISVs hold a clear competitive advantage over general-purpose platforms. Strategic opportunities are emerging in the integration of generative AI, which allows ISVs to offer more intelligent, automated, and personalized products that optimize decision-making for end-users. The analysis also notes that market expansion is heavily dependent on the ability of vendors to navigate complex legacy-system integration and escalating regulatory compliance burdens. Competitive differentiation now stands out based on the depth of an ISV's partnership within hyperscaler ecosystems, such as AWS or Microsoft Azure, which provides the necessary scalability and global reach to capture high-growth segments.

Independent Software Vendors (ISVs) Market Overview

Independent software vendors are shifting from a landscape of standalone proprietary tools to an interconnected ecosystem of cloud-based services. While historically focused on on-premise licensing for enterprise resource planning and database management, the market is now dominated by subscription-based models and Software-as-a-Service (SaaS) offerings. Both large established players and agile niche startups are leveraging cloud-native environments to deliver globally accessible applications. Health-conscious and security-focused industries are looking for specialized third-party providers to enhance their digital infrastructure, particularly in areas like cybersecurity, data analytics, and workflow automation. For instance, the market in the US represents the most mature landscape for independent software vendors, characterized by a high concentration of established tech giants and a thriving startup ecosystem. Rapid technological advancements drive innovation, and a strong corporate culture of outsourcing specialized software needs to improve operational agility and competitive edge.

Market Research Highlights

- Global market for Independent Software Vendors (ISVs) was valued at US$ 2,133.81 Billion in 2133

- Annual market size is expected to reach US$ 4,605.66 Billion by 4605

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ XX

- Market is anticipated to register a CAGR of 13.26% during the forecast period

- The United States represents a key market, supported by Digital Transformation and Cloud Adoption, Increased Demand for Customization and Vertical Solutions, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as AI and Machine Learning Integration, Partnerships with Cloud Providers are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Avgi Solutions, Cisco Systems, Inc., Google, LLC, HP Development Company, L.P., IBM Corporation, Magic Software Enterprises, Oracle Corporation, Microsoft Corporation, Red Hat, Inc., Virtusa Corporation, while analyzing competitive strategies and innovation developments

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONIndependent Software Vendors (ISVs) Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Independent Software Vendors (ISVs) Market Drivers and Opportunities

Market Drivers:

- Accelerated Digital Transformation Initiatives: Global enterprises are aggressively modernizing their IT stacks to remain competitive. This shift creates a massive requirement for third-party software that can provide specialized functionalities, such as automated supply chain management or advanced customer relationship tools, which are not natively available in standard operating systems.

- Surge in Cloud Adoption and SaaS Preference: The transition from capital-intensive on-premise software to predictable, subscription-based cloud models is a primary driver. Cloud platforms enable ISVs to deploy updates instantly and scale their solutions globally without the need for physical infrastructure, significantly lowering the barrier to entry for innovations.

- Integration of Advanced Technologies (AI & ML): The emergence of AI-powered features within software—such as predictive analytics in retail or diagnostic tools in healthcare—is compelling businesses to adopt ISV products. These technologies allow vendors to offer higher value-added services that improve end-user productivity and data-driven insights.

Market Opportunities:

- Expansion into Industry-Specific Vertical SaaS: There is a significant opportunity for ISVs to develop deeply specialized software for underserved niches. By focusing on the unique regulatory and operational needs of sectors like logistics, life sciences, or public utilities, vendors can achieve higher customer retention and command premium pricing.

- Growth through Cloud Marketplace Ecosystems: Partnering with hyperscalers (AWS, Azure, Google Cloud) offers ISVs access to millions of active customers. Leveraging these marketplaces for co-selling and streamlined billing represents a high-growth channel for vendors to expand their footprint with minimal direct sales investment.

- Adoption of Low-Code and No-Code Frameworks: The move toward modular, easily deployable software environments allows ISVs to reach small and medium-sized enterprises (SMEs) that lack extensive IT departments. This segment offers rapid expansion potential as smaller businesses seek to automate their core operations.

Independent Software Vendors (ISVs) Market Report Segmentation Analysis

The Independent Software Vendors (ISVs) Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Deployment:

- Cloud: The dominant and fastest-growing segment, favored for its scalability and cost-effectiveness. It enables vendors to deliver continuous updates and allows users to access software from any location, aligning with modern remote-work requirements.

- On-Premise: Continues to be utilized by large organizations and government entities with sensitive data requirements. This segment remains relevant where local data ownership, high-level security protocols, and deep customizations are mandatory.

By Industry:

- BFSI: A leading segment that utilizes ISV products for risk modeling, fraud analytics, and automated regulatory reporting. The sector's rapid move toward digital banking fuels constant demand for specialized financial software.

- Healthcare: Focusing on improving patient outcomes and data management, this segment uses ISV solutions for electronic medical records and diagnostic AI, representing one of the highest growth trajectories.

- IT and Telecom: A primary driver of market volume, where software is essential for network orchestration, service delivery, and managing complex infrastructure across global networks.

- Retail: Leverages ISV modules for e-commerce automation, real-time inventory tracking, and loyalty program analytics to enhance the customer experience in an increasingly digital shopping environment.

- Others: Includes sectors such as manufacturing, education, and logistics, each requiring specialized tools for process automation, remote learning, and supply chain visibility.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Independent Software Vendors (ISVs) Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 2133.81 Billion |

| Market Size by 2034 | US$ 4605.66 Billion |

| Global CAGR (2026 - 2034) | 13.26% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Deployment Model

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Independent Software Vendors (ISVs) Market Players Density: Understanding Its Impact on Business Dynamics

The Independent Software Vendors (ISVs) Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Independent Software Vendors (ISVs) Market Share Analysis by Geography

North America is expected to hold the largest market share throughout the forecast period, while Asia-Pacific is projected to grow the fastest. Emerging markets in South & Central America, the Middle East, and Africa are increasingly recognized as high-potential zones for mobile-first software applications and cloud-native startups looking to bypass legacy IT infrastructure.

The independent software vendors market is undergoing a significant transformation, moving from traditional on-premise licensing to a globally distributed SaaS ecosystem. Growth is driven by the rapid infusion of Generative AI into enterprise workflows, a surge in vertical-specific software requirements, and the proliferation of low-code/no-code environments. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the dominant global share, anchored by a mature IT ecosystem and the highest concentration of software tech giants in the world.

- Key Drivers:

- Mainstreaming of AI-native enterprise architectures across healthcare and finance.

- Aggressive migration of legacy government and federal workloads to secure cloud environments.

- High density of venture capital funding for niche SaaS startups focusing on workflow automation.

- Trends: A shift toward AI-resilient software that prioritizes proprietary data security. There is also a notable rise in hyperscaler marketplace co-selling, where ISVs leverage platforms like Azure and AWS to reach enterprise clients faster.

Europe

- Market Share: Represents a substantial and stable segment, characterized by a deep focus on data sovereignty and regional compliance software.

- Key Drivers:

- Strict regulatory environments (GDPR, Digital Markets Act) are driving demand for localized compliance tools.

- Strong government support for Digital Europe initiatives and cross-border innovation hubs.

- Increasing adoption of industry-specific software in the automotive and manufacturing sectors (Industry 4.0).

- Trends: A strategic move toward Sovereign Clouds to ensure data remains within EU borders. Additionally, European ISVs are increasingly focusing on sustainability-tracking software to meet new ESG reporting mandates.

Asia-Pacific

- Market Share: The fastest-growing region globally, fueled by rapid industrialization and the digital transformation of massive SME sectors in India, China, and Southeast Asia.

- Key Drivers:

- Massive surge in e-commerce and fintech applications tailored for a mobile-first population.

- Government-led smart city projects require specialized IoT and urban management software.

- Rising disposable incomes are leading to increased enterprise spending on customer experience (CX) tools.

- Trends: Heavy reliance on Super-App ecosystems for software distribution. The region is also seeing a boom in low-code/no-code adoption, allowing non-technical business owners to deploy specialized software solutions rapidly.

South and Central America

- Market Share: An emerging market with a vibrant startup culture, particularly in Brazil, Argentina, and Colombia.

- Key Drivers:

- Modernization of banking and retail sectors through localized fintech and logistics software.

- Expansion of high-speed internet infrastructure facilitates cloud-based software adoption.

- Growing middle-to-high income segments seeking westernized digital service experiences.

- Trends: Rapid growth in Fintech-as-a-Service (FaaS) as ISVs provide the backbone for new digital banks. There is also an increasing focus on agritech software to optimize the region's massive agricultural exports.

Middle East and Africa

- Market Share: A developing market with a strategic focus on reducing reliance on oil through aggressive digital diversification.

- Key Drivers:

- Strategic national visions (e.g., Saudi Vision 2030) prioritize digital public goods and e-governance.

- High demand for cybersecurity and infrastructure software in arid, high-growth urban centers.

- Investments in local data centers by global hyperscalers, lowering latency for regional ISVs.

- Trends: Implementation of Smart Government platforms and a transition toward formalized commercial software markets in the pediatric and educational sectors through Smart Agriculture and EdTech.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Microsoft Corp, SAP SE, Salesforce Inc., and Oracle Corp. The landscape is also being reshaped by high-growth specialized players like CrowdStrike (Cybersecurity), Snowflake (Data), and Veeva Systems (Life Sciences).

This competitive environment pushes vendors to differentiate through:

- Ecosystem Integration: Vendors are prioritizing service-attach requirements and deep integration with major cloud marketplaces to ensure their software is the preferred choice for enterprises already using AWS or Azure.

- Vertical Specialization: Companies are moving away from horizontal tools to develop Vertical SaaS that addresses the specific pain points of a single industry, making their products more sticky and harder to replace.

- AI-Native Features: Incorporating generative AI and automated machine learning as core components of the software to provide superior functionality over legacy competitors.

Opportunities and Strategic Moves

- Strategic Co-Selling Partnerships: ISVs are increasingly entering into co-sell agreements with cloud providers to leverage their massive sales forces and gain access to high-value enterprise accounts.

- Focus on SME Automation: Developing modular, low-cost versions of software tailored for small businesses allows vendors to tap into a high-volume market segment that is currently undergoing rapid digital adoption.

Major Companies operating in the Independent Software Vendors (ISVs) Market are:

- Avgi Solutions

- Cisco Systems, Inc.

- Google, LLC

- HP Development Company, L.P.

- IBM Corporation

- Magic Software Enterprises

- Oracle Corporation

- Microsoft Corporation

- Red Hat, Inc.

- Virtusa Corporation

Disclaimer: The companies listed above are not ranked in any particular order.

Independent Software Vendors (ISVs) Market News and Recent Developments

- In June 2025, Oracle announced the Oracle Defense Ecosystem, a first-of-its-kind global initiative intended to redefine the delivery of defense and government technology innovation. The ecosystem was designed to strengthen U.S. and allied national security and help accelerate the disruptive potential of emerging defense technology by creating new opportunities for defense-focused ISVs to leverage the latest cloud and AI technologies. Initial members of the ecosystem that joined as participating ISVs included Arqit, Blackshark.ai, Entanglement, Fenix Group (now part of Nokia Federal Solutions), Koniku, Kraken, Mattermost, Metron, SensusQ, and Whitespace.

- In January 2025, Amazon Web Services provided more resources and aligned sales incentives to encourage AWS Sellers to prioritize co-selling with a diverse set of Partners. The SaaS co-sell benefit (also known as SaaS Revenue Recognition), previously an invite-only benefit for large technology solution Partners, was expanded to all ISV Accelerate Partners who were transacting in AWS Marketplace, including eligible startups. AWS Sellers began receiving quota retirement for co-selling SaaS solutions with any ISV Accelerate Partner on private offers that transacted through AWS Marketplace.

Independent Software Vendors (ISVs) Market Report Coverage and Deliverables

The Independent Software Vendors (ISVs) Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Independent Software Vendors (ISVs) Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Independent Software Vendors (ISVs) Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Independent Software Vendors (ISVs) Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Independent Software Vendors (ISVs) Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For