Crescita, quota e previsioni del mercato delle navi metaniere di tipo C (2026-2034)

Dimensioni e previsioni del mercato delle navi metaniere di tipo C (2021-2034), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per tipo di prodotto (cilindrico, bilobo e trilobo), applicazione (marino, petrolio e gas, petrolchimico e altri) e geografia.

- Stato : Dati rilasciati

- Codice del report : TIPRE00029686

- Categoria : Automotive e trasporti

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : December 22, 2025

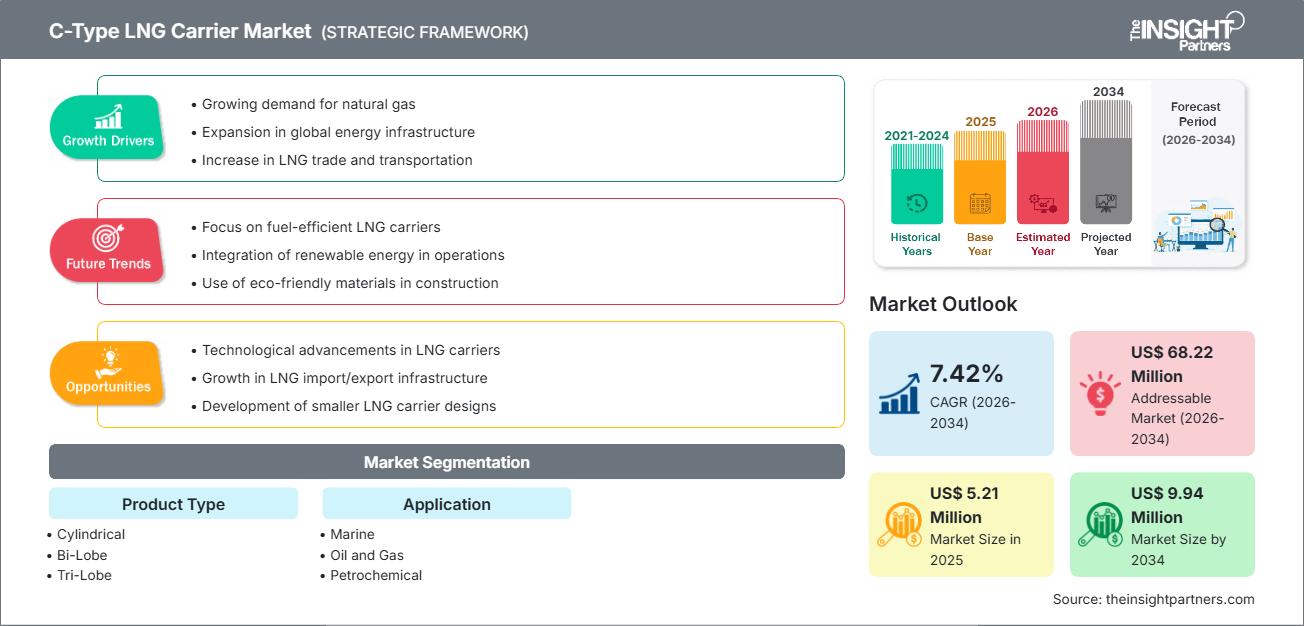

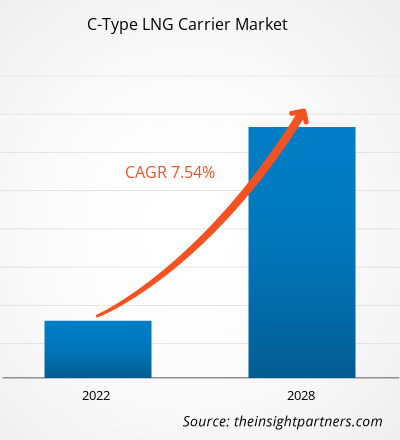

Si prevede che il mercato delle navi metaniere di tipo C raggiungerà i 9,94 milioni di dollari entro il 2034, rispetto ai 5,21 milioni di dollari del 2025. Si prevede che il mercato registrerà un CAGR del 7,42% nel periodo 2026-2034.

Analisi del mercato delle navi metaniere di tipo C

Il mercato delle metaniere di tipo C è in espansione a causa della crescente domanda globale di gas naturale come combustibile di transizione più pulito e dell'espansione delle infrastrutture di GNL in tutto il mondo. Le metaniere di tipo C, che utilizzano serbatoi cilindrici, bilobi o trilobi isolati, completamente o parzialmente pressurizzati, sono utilizzate principalmente per metaniere di piccole e medie dimensioni e altri gas liquefatti. Svolgono un ruolo cruciale nel facilitare il commercio internazionale di GNL, in particolare per la distribuzione regionale, il rifornimento e l'approvvigionamento di aree remote. La crescita del mercato è alimentata da nuovi progetti di liquefazione, da un'impennata di nuovi contratti di costruzione navale per navi alimentate a GNL e dalla necessità di metaniere più versatili per supportare il crescente segmento di mercato del GNL su piccola scala.

Panoramica del mercato delle navi metaniere di tipo C

Una nave metaniera di tipo C è una nave specializzata progettata per il trasporto di gas naturale liquefatto (GNL) a temperature criogeniche. Il "tipo C" si riferisce al sistema di contenimento, costituito da serbatoi a pressione indipendenti di forma cilindrica, bilobata o trilobata, tipicamente installati all'interno dello scafo. Questo design offre una maggiore integrità strutturale e flessibilità nella movimentazione del carico, rendendolo la scelta preferita per il trasporto di GNL su piccola e media scala. Il mercato è caratterizzato da progressi tecnologici volti a migliorare l'efficienza dei consumi e la sostenibilità ambientale, come l'adozione di motori a doppio combustibile.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, incluse parti di questo report, analisi a livello nazionale, pacchetto dati Excel e potrai usufruire di fantastiche offerte e sconti per start-up e università.

Mercato delle navi metaniere di tipo C: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato delle navi metaniere di tipo C

Fattori trainanti del mercato:

- Capacità di liquefazione del GNL in crescita a livello globale: l'espansione degli impianti di liquefazione e della capacità di esportazione in tutto il mondo, in particolare in regioni come il Nord America e la Russia, crea una continua necessità per le compagnie di trasporto di trasportare la crescente fornitura di GNL verso le regioni consumatrici.

- Crescente domanda di gas naturale da parte di diversi settori: il gas naturale viene sempre più adottato come combustibile fossile alternativo più pulito per la produzione di energia, per applicazioni industriali e come combustibile marino (rifornimento di GNL), il che determina direttamente la domanda delle necessarie navi da trasporto.

- Aumento dei nuovi contratti di costruzione navale e nuova espansione della flotta: la necessità di modernizzare la flotta per conformarsi alle normative ambientali (come le misure di riduzione dei gas serra dell'IMO 2023) e l'espansione delle flotte di navi alimentate a GNL (tra cui navi portacontainer e traghetti) incrementano i nuovi ordini per le navi C-Type e altre navi metaniere.

Opportunità di mercato:

- Crescita del mercato del GNL su piccola scala: le navi cisterna di tipo C sono ideali per il mercato del GNL su piccola scala, che si concentra sulla fornitura di aree remote, clienti industriali e sulla fornitura di GNL come combustibile marittimo (bunkeraggio). L'espansione delle reti di distribuzione regionali di GNL offre un'importante opportunità di nicchia.

- Progressi tecnologici nella progettazione delle portaerei: esistono opportunità nello sviluppo e nell'integrazione di nuove tecnologie, come progetti di navi più efficienti in termini di consumo di carburante e più rispettose dell'ambiente, nonché sistemi di intelligenza artificiale e digitali per l'ottimizzazione delle navi, la manutenzione predittiva e l'analisi dei dati in tempo reale per ridurre i costi operativi e l'impatto ambientale.

- Espansione dell'infrastruttura GNL: gli investimenti in nuovi terminali di importazione, impianti di rigassificazione e hub di rifornimento di GNL a livello globale creano opportunità per le navi cisterna di tipo C di servire questi nuovi punti infrastrutturali.

Analisi della segmentazione del rapporto di mercato delle navi metaniere di tipo C

La quota di mercato delle navi metaniere di tipo C viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per tipo di prodotto:

- Cilindrico

- Bi-Lobo

- Trilobo

Per applicazione:

- Marino

- Petrolio e gas

- Petrolchimico

Per geografia:

- America del Nord

- Europa

- Asia-Pacifico

- America meridionale e centrale

- Medio Oriente e Africa

Approfondimenti regionali sul mercato delle navi metaniere di tipo C

Le tendenze e i fattori regionali che hanno influenzato il mercato delle navi metaniere di tipo C durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione analizza anche i segmenti e la geografia del mercato delle navi metaniere di tipo C in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato sulle navi metaniere di tipo C

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 5,21 milioni di dollari USA |

| Dimensioni del mercato entro il 2034 | 9,94 milioni di dollari USA |

| CAGR globale (2026 - 2034) | 7,42% |

| Dati storici | 2021-2024 |

| Periodo di previsione | 2026-2034 |

| Segmenti coperti |

Per tipo di prodotto

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato delle navi metaniere di tipo C: comprendere il suo impatto sulle dinamiche aziendali

Il mercato delle metaniere di tipo C è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni una panoramica dei principali attori del mercato delle navi metaniere di tipo C

Analisi della quota di mercato delle navi metaniere di tipo C per area geografica

Si prevede che l'area Asia-Pacifico crescerà nel periodo di previsione e rappresenterà la quota maggiore del mercato. Questa posizione dominante è attribuita alla massiccia e crescente domanda di gas naturale della regione, alla forte crescita industriale e all'adozione di fonti di energia pulita. La Cina contribuisce in modo significativo al mercato, ma la sua flotta è ancora fortemente dipendente dalle navi metaniere straniere.

Il mercato delle navi metaniere di tipo C mostra una traiettoria di crescita diversa in ciascuna regione, a causa di fattori quali l'aumento dei nuovi contratti di costruzione navale e l'espansione della flotta. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

-

America del Nord

- Quota di mercato: detiene una quota di mercato sostanziale, trainata dalla sua posizione di importante esportatore di GNL.

-

Fattori chiave:

- Significativa espansione della capacità di esportazione di GNL negli Stati Uniti e in Canada.

- Presenza di importanti produttori di GNL e un solido investimento del settore marittimo nelle risorse di GNL.

- Concentrarsi sul GNL come fonte di energia pulita.

- Tendenze: investimenti in attività nazionali di trasporto di GNL, come le chiatte per il trasporto di GNL.

-

Europa

- Quota di mercato: un mercato importante con crescente capacità di liquefazione e rigassificazione.

-

Fattori chiave:

- Forte attenzione alla sicurezza energetica e alla diversificazione dell'approvvigionamento di gas.

- Le normative ambientali più severe (ad esempio le norme IMO) stanno accelerando l'adozione di imbarcazioni alimentate a GNL.

- Domanda di nuovi servizi (ad esempio, distribuzione su piccola scala) presso i terminali di importazione di GNL esistenti.

- Tendenze: investimenti in nuove navi metaniere, tra cui rompighiaccio per le rotte artiche, e passaggio a navi a doppio combustibile e rispettose dell'ambiente.

-

Asia Pacifico

- Quota di mercato: si prevede che sarà il mercato regionale in più rapida crescita e detiene una quota significativa, grazie all'enorme domanda di importazione di GNL.

-

Fattori chiave:

- Rapida crescita industriale e crescente domanda di energia.

- Adozione, sostenuta dal governo, di fonti energetiche più pulite come il GNL.

- Elevato volume di importazioni di GNL, in particolare in Cina e India.

- Tendenze: Predominio del segmento marittimo nelle applicazioni. Grande attenzione allo sviluppo della capacità di rigassificazione.

-

America meridionale e centrale

- Quota di mercato: mercato emergente con crescente adozione.

-

Fattori chiave:

- Aumento della domanda di energia e sviluppo dei giacimenti di gas.

- Investimenti nelle infrastrutture regionali di GNL e negli impianti di importazione.

- Tendenze: sviluppo di strumenti di traduzione automatica per un pubblico multilingue, intelligenza artificiale predittiva per l'ottimizzazione delle campagne e piattaforme di social listening.

-

Medio Oriente e Africa

- Quota di mercato: mercato emergente con forte potenziale di crescita.

-

Fattori chiave:

- Importanti strategie nazionali in ambito digitale ed energetico per promuovere l'innovazione nel trasporto del gas.

- Attori chiave come il Qatar continuano a dominare il commercio mondiale di GNL, stimolando la domanda di nuove navi.

- Tendenze: monitoraggio del sentiment del pubblico basato sull'intelligenza artificiale, rilevamento delle frodi degli influencer e moderazione dei contenuti multilingue tramite apprendimento automatico.

Densità degli operatori del mercato delle navi metaniere di tipo C: comprendere il suo impatto sulle dinamiche aziendali

Il mercato delle navi metaniere di tipo C è estremamente competitivo, con poche grandi compagnie di navigazione e cantieristica navale globali che dominano gli ordini di nuove costruzioni e le operazioni di flotta. La differenziazione si ottiene principalmente attraverso l'innovazione tecnologica, il rispetto delle severe normative ambientali e la gestione strategica della flotta.

Il panorama competitivo spinge i fornitori a differenziarsi attraverso:

- Investire in sistemi di contenimento avanzati e in sistemi di propulsione a basso consumo di carburante per ridurre il consumo di carburante e le emissioni.

- Collaborazioni tra costruttori navali, fornitori di tecnologia e grandi aziende energetiche per garantire contratti a lungo termine e finanziamenti per nuove navi.

- Puntando al segmento crescente del mercato che richiede portaerei C-Type più piccole e versatili per servizi di distribuzione regionale e rifornimento.

Opportunità e mosse strategiche

- Modernizzazione ed espansione della flotta: le aziende ordinano continuamente nuove navi per sostituire unità più vecchie e meno efficienti e per ampliare la capacità di soddisfare il crescente volume di scambi globali di GNL.

- Catena del valore integrata: le principali compagnie energetiche e le grandi compagnie di navigazione stanno integrando le loro operazioni lungo l'intera catena del valore del GNL, dalla liquefazione alla spedizione e alla distribuzione.

- Adozione di tecnologie digitali e autonome: sviluppo e integrazione di soluzioni di spedizione intelligenti (intelligenza artificiale, IoT, monitoraggio remoto) per migliorare l'efficienza operativa, la sicurezza e la manutenzione predittiva.

Le principali aziende che operano nel mercato delle navi metaniere di tipo C sono:

- China Shipbuilding Trading Co., Ltd

- DSME Co., Ltd

- GAS Entec

- Gaslog Ltd

- HYUNDAI SAMHO HEAVY INDUSTRIES CO., LTD.

- Spedizione OAS di Knutsen

- Komarine Co

- Mitsubishi Heavy Industries, Ltd.

- TGE Marine Gas Engineering GmbH

Disclaimer: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e sviluppi recenti sul mercato delle navi metaniere di tipo C

- Ad esempio, nel novembre 2024, HD KSOE ha annunciato di aver firmato contratti di costruzione navale per un totale di 25 navi con società estere situate in Europa, Oceania, Asia e Medio Oriente. I contratti includono due grandi navi porta-ammoniaca (Very Large Ammonia Carrier, VLAC), 15 navi porta-prodotti di medie dimensioni (Medium-sized Product Carrier, PC), sei grandi navi porta-gas di petrolio liquefatto (Very Large Liquefied Petroleum Gas Carrier, VLGC) e due navi porta-gas naturale liquefatto (LNG). L'importo totale del contratto è di 2,82 trilioni di KRW.

Copertura e risultati del rapporto sul mercato delle navi metaniere di tipo C

Il rapporto "Dimensioni e previsioni del mercato delle navi metaniere di tipo C (2021-2034)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato delle navi metaniere di tipo C a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato delle navi metaniere di tipo C, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato delle navi metaniere di tipo C che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti nel mercato delle navi metaniere di tipo C. Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative