Cell and Gene Therapy Manufacturing Services Market Overview and Growth by 2030

Coverage: By Type [Cell Therapy (Autologous, Allogenic) and Gene Therapy (Viral, Non-Viral Vector)], Indication (Cancer, Orthopaedics, Others), Application (Clinical Manufacturing, Commercial Manufacturing), End User [Pharmaceutical, Biotechnology Companies, Contract Research Organization (CROs), and Geography

- Status : Published

- Report Code : TIPRE00024304

- Category : Life Sciences

- No. of Pages : 216

- Available Report Formats :

- Last update date : August 13, 2024

2022 Market Size

US$ 7,581.97 Mn

Base year value

2030 Forecast

US$ 26,724.90 Mn

Projected by 2030

CAGR 2022-2030

17.1 %

Growth rate

Addressable Market

US$ 131,647.46 Mn

(2022-2030)

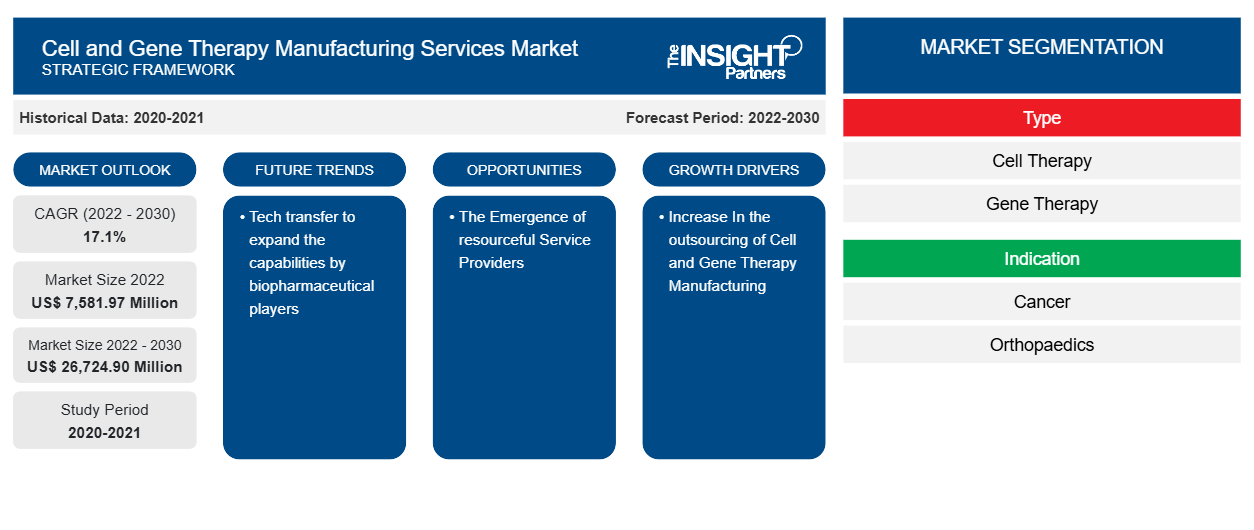

The cell and gene therapy manufacturing services market size is projected to reach US$ 26,724.90 million by 2030 from US$ 7,581.97 million in 2022. The market is expected to register a CAGR of 17.1% during 2022–2030. Automation of manufacturing services for cell and gene therapy is likely to remain a key trend in the market.

Cell and Gene Therapy Manufacturing Services Market Analysis

In recent years, the outsourced cell and gene manufacturing sector has undergone significant expansion and change. As cell and gene therapies progress, drug innovator firms are progressively depending on service providers to fulfill their manufacturing requirements. Outsourcing enables innovators to take advantage of the specialized expertise and capabilities of contract development and manufacturing organizations (CDMOs) to reduce costs and expedite time to market. The landscape of cell and gene therapy manufacturing has evolved over the past five years, with a shift towards more sophisticated platforms allowing scale-up, increased automation, and enhanced quality systems, shaping the contract manufacturing industry. With the growing number of approved cell and gene therapy products in the market each year, the need to enhance processes is becoming increasingly important.

Cell and Gene Therapy Manufacturing Services Market Overview

Both publicly and privately funded contract biopharmaceutical manufacturing has increased as a result of the surge in new biopharmaceutical products competing for approval. As a result, while established industry players are attempting to hold onto their positions and lead, new organizations are engaged in providing manufacturing services for cell and gene therapy. Healthcare policies in many regions now prioritize the ability to manufacture pharmaceutical (small molecule) products of all kinds. Additionally, a shift toward larger-molecule biomanufacturing, recombinant therapies, and increasingly complex biologics has occurred in many regions.

Market Assessment and Insights

- North America dominated the market with 54.8% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 17.3% over the forecast period.

- United States market is projected to grow at a CAGR of 17.1% over the forecast period.

- By Type, the Cell Therapy segment accounted for the largest market share of 68.3% in 2022.

- By Cell Therapy, the Allogenic segment is anticipated to witness the fastest growth, registering a CAGR of 20.9% over the forecast period

- By Gene Therapy, the Viral Vector segment accounted for the largest market share of 65.3% in 2022.

- By Indication, the Cancer segment is anticipated to witness the fastest growth, registering a CAGR of 18% over the forecast period

- By Application, the Commercial Manufacturing segment accounted for the largest market share of 62.8% in 2022.

- By End Users, the Pharmaceutical and Biotechnological Companies segment is anticipated to witness the fastest growth, registering a CAGR of 17.2% over the forecast period

- The report profiles key industry players such as Thermo Fisher Scientific Inc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Cell and Gene Therapy Manufacturing Services Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Cell and Gene Therapy Manufacturing Services Market Drivers and Opportunities

Increase in Demand for Cell and Gene Therapy Manufacturing Favors Market Growth

Significant therapeutic advances in cell and gene therapy manufacturing services have resulted from the growing cell therapy research activities. The industry is striving to expand its manufacturing scale and overall accessibility to a broader population while emphasizing the advantages of advanced therapy medicinal products (ATMPs). The increasing complexity of personalized medicine necessitates the development of manufacturing capabilities to keep up with demand and guarantee patient access to these innovative treatments. Contract manufacturing now has more options due to the rise in global production. Funding for newly approved biopharmaceutical products, as well as contract biopharmaceutical manufacturing, has increased from both public and private sources. Worldwide organizations offer manufacturing services for cell and gene therapy, and well-established industry participants strive to sustain their operations. Thus, the emerging focus on the development of cell therapy manufacturing is likely to drive the growth of the market.

Strategic Initiatives by Key Players

Because of the rise in approvals and investments, there is an increasing need to manufacture therapies at preclinical, clinical, and commercial stages. Key players are making strategic development investments, which are opening up a lot of market opportunities. As an illustration of the rising need for cell and gene therapy manufacturing services, Bristol Myers Squibb and the start-up Cellares inked a $380 million deal in May 2024. In August 2023, Cellares completed a $255 million series C funding round, with BMS among the investors. Cellares will make chimeric antigen receptor (CAR) T-cell treatments for BMS. BMS will reserve spaces in Cellares' automated cell therapy manufacturing machines, or Cell Shuttle machines, in accordance with the terms of the agreement. With the money from the BMS sale, Cellares intends to open more locations in the US, Europe, and Japan in addition to running the ones in San Francisco and New Jersey.

Cell and Gene Therapy Manufacturing Services Market Report Segmentation Analysis

Key segments that contributed to the derivation of the cell and gene therapy manufacturing services market analysis are type, indication, application, and end user.

- Based on type, the cell and gene therapy manufacturing services market is divided into cell therapy and gene therapy. Cell therapy is further sub-segmented into autologous and allogeneic therapy. Gene Therapy is further sub-segmented into viral and non-viral vectors.

- By indication, the market is categorized into cancer, orthopedics, and others. The cancer segment held the largest share of the market in 2022.

- By application, the market is categorized into clinical manufacturing and commercial manufacturing. The commercial manufacturing segment held the largest share of the market in 2022.

- By end user, the market is segmented into pharmaceutical and biotechnology companies and contract research organizations (CROs). The pharmaceutical and biotechnology companies segment held the largest share of the market in 2022.

Cell and Gene Therapy Manufacturing Services Market Share Analysis by Geography

The geographic scope of the cell and gene therapy manufacturing services market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The market for manufacturing services related to cell and gene therapy is anticipated to expand as a result of the rising demand for these products. This growth is linked to an increase in startups, an increase in R&D activities, and increased investments in the construction of cell and gene therapy manufacturing facilities in the US and Canada.

Additionally, for the forecast period, the Asia Pacific market has grown significantly at a robust CAGR. This growth can be attributed to a number of factors, including the growing need for advanced treatment solutions, favorable regulatory scenarios, and an increasing emphasis on research and development activities. Additionally, during the forecast period, the Asia Pacific market is expected to be driven by the expansion of healthcare infrastructure and rising investments meant to stimulate research activities.

Cell and Gene Therapy Manufacturing Services Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 7,581.97 Million |

| Market Size by 2030 | US$ 26,724.90 Million |

| Global CAGR (2022 - 2030) | 17.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2022-2030 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Cell and Gene Therapy Manufacturing Services Market Players Density: Understanding Its Impact on Business Dynamics

The Cell and Gene Therapy Manufacturing Services Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Cell and Gene Therapy Manufacturing Services Market News and Recent Developments

The cell and gene therapy manufacturing services market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the cell and gene therapy manufacturing services market are listed below:

- RoslinCT and Lykan Bioscience, two leading Contract Development and Manufacturing Organizations (CDMOs) in the Cell and Gene Therapy industry, announce their integration, creating a unified business that will operate under the RoslinCT brand. The integration, facilitated by GHO Capital, a global investment firm, aims to establish a dominant player in the Advanced Cell and Gene Therapy CDMO market. (Source: RoslinCT, Press Release, June 2023)

- Cincinnati Children's Hospital Medical Center and the research service provider CTI Clinical Trial & Consulting Services have agreed to form a company that will focus on providing cell and gene therapy manufacturing services to the biotechnology and pharmaceutical industries. (Source: Cincinnati Children's Hospital Medical Center, Press Release, December 2021)

Cell and Gene Therapy Manufacturing Services Market Report Coverage and Deliverables

The “Cell and Gene Therapy Manufacturing Services Market Size and Forecast (2020–2030)” report provides a detailed analysis of the market covering below areas:

- Cell and gene therapy manufacturing services market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Cell and gene therapy manufacturing services market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Cell and gene therapy manufacturing services market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the cell and gene therapy manufacturing services market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends