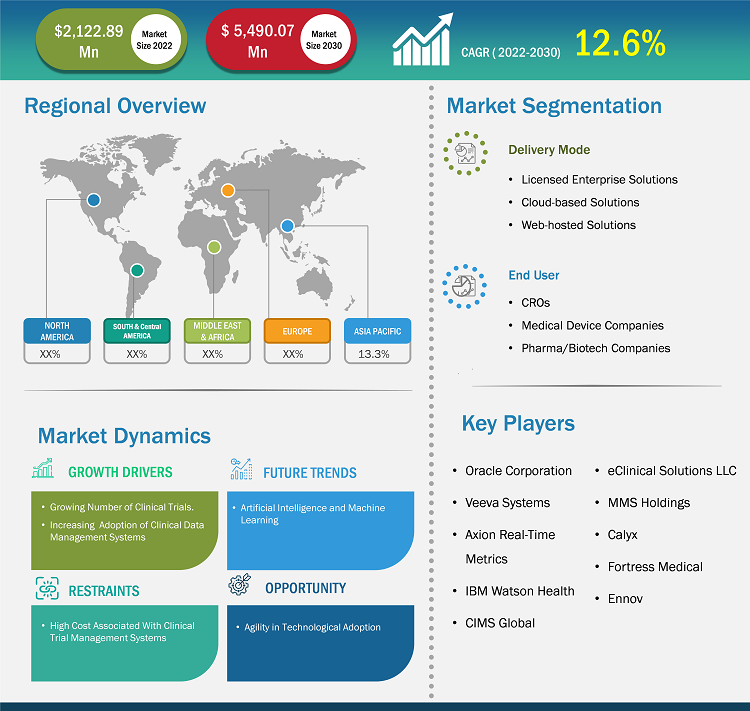

The clinical data management systems market size is projected to grow from US$ 2,122.89 million in 2022 to US$ 5,490.07 million by 2030; the market is estimated to record a CAGR of 12.6% during 2022–2030.

Market Insights and Analyst View:

The collection, documentation, and data storage process, which are important for clinical trials or procedures and biotechnology companies and pharmaceutical manufacturers, is termed Clinical Data Management. Data management systems for clinical trials are widely for the development of new medical treatments and diagnostic tests. A clinical data management tool is employed in clinical research to manage a clinical trial's data. Clinical data management is an initial phase in clinical research, leading to generating high-quality, reliable, and statistically comprehensive data to reduce the time duration from drug development to marketing. The major goal of Clinical data management is to ensure the data supports inferences drawn from the research to protect public health and trust in marketed therapeutics.

The clinical research data management systems market is expected to grow due to increasing numbers of startups in the sector. Merative Clinical Development, Clinion, and Bioclinica ICL are some startups.

The huge number of clinical trials carried out in the healthcare industry has helped the market record considerable growth over the period. The active support that the government provides for various research trials to introduce modern medicines into the market that have a better success rate is helping the market record considerable revenue over time.

The prevalence of several chronic diseases among people has propelled the demand for clinical trials and research programs to be carried out by the key market leaders, which are managed with the help of clinical trial management systems. The government funds provided for research programs have helped the market conduct quality research programs and clinical trials, which has boosted the market for management systems as well. The rapid increase in geriatric population has also emerged as a significant growth factor for the market.

Growth Drivers:

Growing Number of Clinical Trials

Research and development are an important part of pharmaceutical companies, including drug development and product development. Among all industry sectors, the pharmaceutical industry spends the largest revenue on research and development. Many companies are active in pharmaceutical research and development globally. Several advantages of web-based data collection tools, such as minimizing time and ease in data entry, flexibility in format, low cost, and the ability to capture additional response-set information, propel the clinical data management systems market. In addition, high levels of productivity and efficiency offered by clinical data management systems are expected to redefine the companies' traditional data management process, thus augmenting the clinical data management market growth. Also, the increase in R&D expenditure of clinical research and life science industries, combined with an increasing number of clinical trials, contributes to the growth of the clinical data management systems market.

As per Statista, Clinical studies are an integral part of the drug development process. The total number of registered clinical trials has increased significantly in recent years. As of May 29, 2023, nearly 454,000 clinical studies were registered globally. The number of clinical studies has significantly increased since there were just 2,119 registered in 2000.

Moreover, increasing innovative technological advancements to curb the increasing costs associated with clinical trials have resulted in the development of the clinical trial data management system market. For instance, in November 2022, the Singapore Clinical Research Institute (SCRI) launched the Master Clinical Trials Agreement (MCTA) at the Clinical Research Roundtable. The MCTA provided a legal template that shortens the initiation of clinical trials in Singapore by decreasing the processing time in reviewing trial agreements between industry sponsors and public healthcare institutions.

Rising funding and investments by biotechnology and pharmaceutical firms are promoting medical research activities. This factor, coupled with technological advancements, is anticipated to propel the market growth in the future. For instance, a cloud-based clinical trial management system reduces the expenses of hardware acquisition, provisioning, installation, maintenance, support, and software licensing. These systems automatically update software and patch management systems, which lowers the burden of in-house IT staff and saves costs. Furthermore, the cloud-based software allows access to the server through mobile with maximum data security.

The growing number of decentralized clinical trials is further expected to boost market growth in the future. These are also known as virtual, digital, mobile, siteless, and remote trials that utilize telemedicine solutions. For instance, Labcorp's decentralized clinical trials (DCTs) solution offers a set of solutions to design and implement decentralized clinical trials, including the technology, necessary infrastructure, and services.

Strategic Insights

Report Segmentation and Scope:

The “Clinical Data Management Systems Market” is segmented on the basis of delivery mode and end users. Based on delivery mode, the market is categorized into licensed enterprise solutions, cloud-based solutions, web-hosted solutions. Based on end user, the market is segmented into CROs, medical device companies, pharma/biotech companies.

Segmental Analysis:

Based on delivery mode, the clinical data management systems market is divided into licensed enterprise solutions, cloud-based solutions, web-hosted solutions. The cloud-based solutions segment held a larger market share in 2022 and the same segment is expected to register a higher CAGR during the 2022–2030. The growth is attributed to the technological developments in the healthcare industry and the increasing adoption of cloud-based solutions. The cloud-based model offers several benefits, such as flexibility, scalability, and collaboration. Such benefits associated with the cloud-based model are expected to propel the market. In addition, the cloud-based model also eliminates the requirement of buying, maintaining, and deploying on-premises services, thereby minimizing installation and maintenance costs and contributing to the overall expansion.

The majority of businesses are using cloud-based security and safety solutions as a result of these advantages. Organizations are progressively implementing cloud-based solutions in response to customer demands and business objectives. The growing need for efficient cloud storage, access, and administration of the huge volumes of data produced by these organizations has been a crucial growth facilitator.

Based on end user, the clinical data management systems market is segmented into CROs, medical device companies, pharma/biotech companiess. The CROs segment held a larger market share in 2022. It is expected to register a higher CAGR during 2022–2030. Globally expanding contract research organizations (CROs) are expected to boost market revenue. The market demand is also anticipated to be further fuelled by a growing trend of outsourcing clinical trials to CROs, which lowers the overall cost of drug development. In addition, several CROs have chosen to use the clinical data management system (CDMS) and electronic data capture (EDC) as two of the most popular digital solutions to handle the growing volume of data. Therefore, the use of CDMS in various clinical research initiatives will positively impact market growth in the upcoming year.

Furthermore, partnerships with multinational companies or local CROs streamline this process. For instance, Clario offers solutions for all trial models, such as site-based, decentralized, and hybrid clinical trials. It generates diverse and reliable evidence by its 30 facilities across 9 countries in North America, Europe, and Asia Pacific. In October 2022, Veeva Systems partnered with nearly 40 CROs to deploy its clinical trial management tools suite, including the Veeva Vault CTMS. Moreover, the company witnessed rapid growth during the COVID-19 pandemic, as virtual or hybrid clinical trials became necessary.

Regional Analysis:

Based on geography, the global clinical data management systems market is segmented into five key regions: North America, Europe, Asia Pacific, Middle East & Africa, South & Central America. In 2022, North America contributed the largest share of the global clinical data management systems market size. Asia Pacific is expected to register the highest CAGR during 2022-2030.

North America holds the largest share of the clinical data management systems market. The market in this region is split into the US, Canada, and Mexico. The growth of the market in the region is ascribed to factors such as the presence of key players and the increasing adoption of technology in research and development. Favorable regulatory policies and increasing investment by pharmaceutical companies also favor to regional growth. In November 2021, ERT, a clinical endpoint technology leader, merged with Bioclinica to form Clario. This merger helped the company to deliver technology-based therapeutic area solutions to meet clinical trial objectives.

The US is the largest contributor to the clinical data management systems market in North America and the world. Per the ClinicalTrials.gov, as of June 2023 in North America, 1,95,130 clinical trials were ongoing. Out of those, 163,336 were taking place in the US. The increasing number of clinical trials and studies, combined with the increased funding for clinical research, will likely drive the market’s growth.

Research and development budgets of pharmaceutical companies have also increased in the last few years in the region. For instance, the National Institute of Health (NIH) funds clinical research heavily, and its funding in the United States was USD 45 billion in 2022. Hence, with strong investments in R&D activities and a pipeline of therapeutics under development, the market is expected to grow significantly. Additionally, in February 2023, Suvoda launched a purpose-built software platform that brings proven tech innovation to clinical trial management. It delivers the next generation of clinical trial applications designed to handle complexity and reduce overall risk throughout trials easily.

Thus, the market is projected to grow during the forecast period due to increasing research and development investments and the rising demand for drug development.

Competitive Landscape and Key Companies:

Oracle Corporation, Veeva Systems, Axion Real-Time Metrics, IBM Watson Health, CIMS Global, eClinical Solutions LLC, MMS Holdings, Calyx, Fortress Medical and Ennov are the prominent clinical data management systems market companies. These companies focus on new technologies, existing products’ advancements, and geographic expansions to meet the growing consumer demand worldwide.

Industry Developments and Future Opportunities:

Various initiatives taken by leading players operating in the clinical data management systems market are listed below:

- In March 2023, Assentia launched tech platforms to support payments in the clinical trial space. The company released two SaaS-based applications, GrantPay and GrantPact, to provide clinical trial contract negotiation and payment services.

- In February 2023, Vial partnered with Egnyte. By integrating Egnyte’s eTMF, Vial will offer clients the gold standard in eTMF management, compliance, and audit readiness with the increased bar in clinical trial technology.

- In June 2022, Medidata announced technology enhancements that address key clinical trial management and oversight issues. Enhancements to Medidata Detect and Rave Clinical Trial Management System will improve data oversight and reporting for sponsors and CROs in two meaningful ways on how they comprehensively monitor their trial data and visualize those data to make faster decisions.

- In April 2021, Accenture acquired Zafgen, a provider of Clinical Trial Management Systems (CTMS). The deal expands Accenture’s capabilities in clinical trial management and analytics.

- In March 2021, Peachtree BioResearch Solutions, Inc., a CRO serving emerging mid-sized companies, adopted Oracle Health Sciences Cloud Services and the Siebel Clinical Trial Management System (CTMS) to simplify clinical trials start-up and monitoring.

- In February 2021, eClinical Solutions LLC launched elluminate CTMS for life sciences companies to support drug development. The elluminate CTMS platform delivers benefits such as Increased Operational Oversight and Control, Improve Trial Performance, and optimized resources.

- In November 2020, Oracle Corporation announced its acquisition of ICON, a provider of CTMS services. The deal expands Oracle’s global presence in the life sciences industry and helps organizations accelerate the development of new treatments and therapies.

- In May 2019, IQVIA Technologies announced its acquisition of Medidata Solutions, a provider of cloud-based CTMS solutions. The deal expanded IQVIA’s presence in the clinical trial management market.

- In March 2019, Oracle Corporation announced its acquisition of Comprehend Systems, a cloud-based clinical trial management solutions provider. The deal expands Oracle’s capabilities in the healthcare and life sciences industries.

- In December 2018, Veeva Systems announced its acquisition of CloudNine, a cloud-based clinical trial management solutions provider. The deal strengthens Veeva’s portfolio of clinical trial management solutions.

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Clinical Data Management Systems Market Report Analysis

-

CAGR (2023 - 2031)12.60% -

Market Size 2023

US$ 2.39 Billion -

Market Size 2031

US$ 6.18 Billion

Report Coverage

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Key future trends

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Industry landscape and competition analysis & recent developments

- Detailed company profiles

- Global and regional market analysis covering key market trends, major players, regulations, and recent market developments

Key Players

- Oracle Corporation

- Veeva Systems

- Axion Real-Time Metrics

- IBM Watson Health

- CIMS Global

- eClinical Solutions LLC

- MMS Holdings

- Calyx

- Fortress Medical

- Ennov

Regional Overview

- North America

- Europe

- Asia-Pacific

- South and Central America

- Middle East and Africa

Market Segmentation

By Delivery Mode

By Delivery Mode

- Licensed Enterprise Solutions

- Cloud-based Solutions

- Web-hosted Solutions

By By End User

By By End User

- CROs

- Medical Device Companies

- Pharma/Biotech Companies

By Geography

By Geography

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- South and Central America

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Clinical Data Management Systems Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 2.39 Billion |

| Market Size by 2031 | US$ 6.18 Billion |

| Global CAGR (2023 - 2031) | 12.60% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Delivery Mode

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

- Oracle Corporation

- Veeva Systems

- Axion Real-Time Metrics

- IBM Watson Health

- CIMS Global

- eClinical Solutions LLC

- MMS Holdings

- Calyx

- Fortress Medical

- Ennov

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Clinical Data Management Systems Market

Apr 2024

Emergency Call Systems Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Application (Fall Prevention and Detection, Workflow Optimization, Patient Care Reminders, Alarms and Communication Management, Wander Management, Reporting and Analytics, Real-Time Staff Locating, and Others), End User (Hospital and Clinics, Assisted Living and Independent Living Facilities, Ambulatory Surgical Centers, and Others), Technology (Wired and Wireless), Offering (Hardware, Software, and Services), Product Type (Nurse Call Systems, Call Box Systems, Emergency Stanchions, Intercom System, and Others),, and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Apr 2024

Outpatient Central Fulfillment Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Automated Medication Dispensing Systems, Automated Packaging and Labeling Systems, Automated Tabletop Counters, Automated Storage and Retrieval Systems, and Others), End User (Hospital Pharmacies, Retail Pharmacies, and Mail-Order Pharmacies), and Geography (North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa)

Apr 2024

Well-Being Platform Market

Forecast to 2030 - Global Analysis by Service (Health Risk Assessment, Fitness, Smoking Cessation, Health Screening, Nutrition & Weight Management, Stress Management, Comprehensive Well-Being, and Others), Category (Fitness and Nutrition Consultant, Psychological Therapists, and Organizations/Employers), Delivery Model (Onsite and Offsite), End User (Small-Scale Organizations, Medium-Scale Organizations, Large-Scale Organizations, and Home Use), and Geography

Apr 2024

Product Design and Development Services Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Services (Research, Strategy, and Concept Generation; Concept and Requirement Development; Detailed Design and Process Development; Process Validation, Manufacturing Transfer, and Design Validation; and Other Services), Application (Diagnostic Equipment, Therapeutic Equipment, Surgical Instruments, Clinical Laboratory Equipment, Biological Storage, Consumables, and Others), and End User (Medical Companies, Pharmaceutical Companies, Biotechnology Companies, and Contract Research Organizations)

Apr 2024

Patient Engagement Technology Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Component (Services, Hardware, and Software), Therapeutic Area (Fitness, Chronic Diseases, Women’s Health, and others), Delivery Mode (Cloud-Based and On-Premises), Application (Health Management, Financial Health Management, Home Healthcare Management, and Others), and End User (Patients, Payers, Providers, and Others)

Apr 2024

IVD Contract Research Organization Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Type (Clinical Chemistry, Molecular Diagnostics, Immunochemistry, Companion Diagnostics, Hematology, Histology & Cytology, Microbiology, and Others), Services (Clinical Research, Biostatistics & Data Management Services, Therapeutic Expertise, Regulatory Services, Reimbursement Support Services, Assay Development Services, and Others), and Geography

Apr 2024

Dental CAD/CAM Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Product [Dental CAD/CAM Materials (Glass Ceramics, Alumina-Based Ceramics, Lithium Disilicate, Zirconia, and Others) and Dental CAD/CAM Systems], Type (In-Office Systems and In-Lab Systems), Components [Hardware (Dental Printers, Milling Machines, Scanners, and Others) and Software], Application (Dental Prosthesis, Dental Implants, and Others), and End User (Dental Clinics, Dental Laboratories, Milling Centers, and Others)

Apr 2024

Emergency Medical Software Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Product [Early Warning and Vulnerability Alert System (EWVAS), EMS Computer Aided Dispatch (CAD) System, Incident Response Software, Ambulance Management Software, and Others], Mode of Delivery [On Premises and Software as a Service (SaaS)], Platform (Android, iOS, Windows, and Others), and End User (Commercial, Municipal, State City Agencies, and Others)