Diagnostic Imaging Market Growth, Trends, and Analysis by 2031

Diagnostic Imaging Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Modality (X-Ray, CT, Endoscopy, Ultrasound, MRI, Nuclear Imaging, Mammography, and Others), Application (Cardiology, Oncology, Neurology, Orthopaedics, Gastroenterology, Obstetrics and Gynaecology, and Others), and End User (Hospital and Clinics, Diagnostic Imaging Centres, Ambulatory Surgical Centres, and Others), and Geography

Historic Data: 2021-2022 | Base Year: 2023 | Forecast Period: 2024-2031- Status : Data Released

- Report Code : TIPHE100001107

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

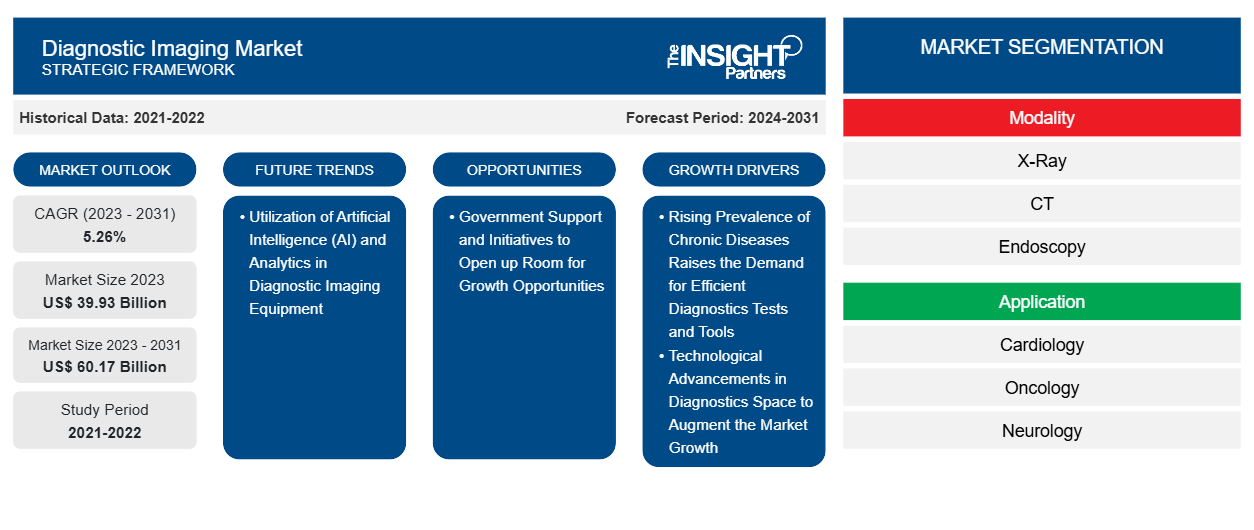

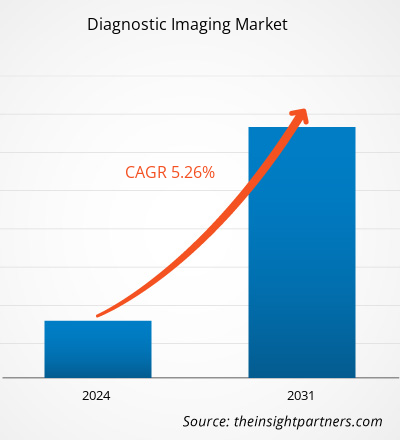

The Diagnostic Imaging market size is projected to reach US$ 60.17 billion by 2031 from US$ 39.93 billion in 2023. The market is expected to register a CAGR of 5.26% during 2023–2031. The growing utilization of artificial intelligence (AI) and analytics in diagnostic imaging equipment will likely remain key trends in the market.

Diagnostic Imaging Market Analysis

Diagnostic imaging describes various techniques for the visual representation of different tissues and organs of the human body to identify the causes of an illness or injury, confirm a diagnosis, and monitor treatment response. Various machines and techniques such as X-ray, computed tomography (CT), positron emission tomography (PET), magnetic resonance imaging (MRI), single-photon emission computed tomography (SPECT), digital mammography, and diagnostic sonography can generate images of the structures and activities within the body. Many imaging tests are noninvasive, simple, and painless. However, some may require you to remain still inside the machine for an extended period, which can be somewhat uncomfortable. Additionally, certain tests involve a small amount of radiation exposure. Increasing prevalence of chronic diseases is a major growth driving factor for the market. Additionally, new developments in the field of medical diagnostics contribute to the market growth during the forecast period.

Diagnostic Imaging Market Overview

In 2023, Asia Pacific is expected to grow with the highest CAGR in the global diagnostic imaging market. The Asia Pacific diagnostic imaging market is expected to grow significantly owing to the developments in countries including China, Japan, and India. According to an article published in National Library of Medicine (NLM) in September 2023, the number of CT scanners per 100,000 population was the highest in Kochi Prefecture, while Tokyo Prefecture had the highest number of CT scanners in hospitals. Therefore, the market in Asia Pacific is driven by growing investments from international players in several Asian countries. Therefore, the region holds huge potential for the diagnostic imaging market players to grow during the forecast period.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONDiagnostic Imaging Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Diagnostic Imaging Market Drivers and Opportunities

Advancements in Diagnostic Imaging Technologies to Favor Market

As highlighted by the World Health Organization (WHO) diagnostic imaging has advanced rapidly and plays a vital role in healthcare by supporting the diagnosis and treatment of various diseases. Diagnostic imaging services include confirming, assessing, and documenting the course of many conditions for ultimately drawing the response to treatment. According to an article published by AdventHealth University in October 2021, in recent years, there have been many advancements in digital radiography. These include AI-aided X-ray interpretation, dual-energy imaging, computer-aided diagnosis, tomosynthesis, automatic image stitching, and digital mobile radiography. These advancements have improved image quality, ultimately enhanced patient care and supporting better patient outcomes. Furthermore, the use of digital radiography reduces the need for retakes, which lowers radiation exposure.

Such advancements in imaging technologies for disease diagnostics boosts the diagnostics imaging market growth.

Government Initiatives Brings Growth Opportunities

Government plays a vital role in purchasing, pricing, and distributing medical devices worldwide. Governments undertake various initiatives for developing healthcare infrastructure, and focus on offering safe and cost-effective medical products through fundings for opening new healthcare facilities. For instance, in the UK, the National Health Service targets addressing patients' unmet medical needs through cost-effective ways to enhance the country's economic growth. Additionally, the Canadian government paid US$ 1,400 per scan per patient to hospitals, owing to a lack of private funding in the country in 2020.

Furthermore, non-profit regulatory bodies such as the WHO and United Nations International Children's Emergency Fund (UNICEF) collaborates with manufacturers to develop effective solutions targeting to improve diagnostic services in remote locations. Additionally, these organizations provide training programs on the use and management of imaging technologies, focusing more on patient safety. For example, in February 2022, Siemens Healthineers partnered with UNICEF for the support in improving access to healthcare in Sub-Saharan Africa for diagnostic techniques.

Such factors mentioned above are responsible for offering lucrative opportunities for boosting the growth of the diagnostic imaging market.

Diagnostic Imaging Market Report Segmentation Analysis

Key segments that contributed to the derivation of the Diagnostic Imaging market analysis are modality, application, and end user.

- The diagnostic imaging market is segmented based on modality into X-Ray, CT, endoscopy, ultrasound, MRI, nuclear imaging, mammography, and others. The ELISA tests segment held the largest market share in 2023.

- By application, the market is segmented into cardiology, oncology, neurology, orthopaedics, gastroenterology, obstetrics and gynaecology, and others. The avian influenza segment held the largest market share in 2023.

- The market is segmented based on end user into hospital and clinics, diagnostic imaging centres, ambulatory surgical centres, and others. The hospital and clinics segment held the largest market share in 2023.

Diagnostic Imaging Market Share Analysis by Geography

The geographic scope of the Diagnostic Imaging market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America holds the largest market share of the next-generation sequencing market. The Diagnostic Imaging market in North America is analyzed based on the US, Canada, and Mexico. The US is estimated to dominate the North America Diagnostic Imaging market in 2023. The utilization of diagnostic imaging is high in the US due to innovative launches of imaging modalities and approvals by the regulatory bodies. For instance, in September 2021, FDA announced clearance for the first new significant technological advancement for computed tomography (CT) imaging. The device utilizes the emerging CT technology of photon-counting detectors to measure every individual X-ray passing through a patient's body. The FDA also reviewed a new diagnostic imaging device, "NAEOTOM Alpha," manufactured by Siemens in 2021. Such technological advancements in imaging modalities accelerate the uptake of diagnostic imaging in the US.

Additionally, as the US population ages, the demand for diagnostic imaging technologies is expected to rise at a high pace for diagnosing, detecting, and treating many chronic health conditions and diseases common in the aging population.

Therefore, the growth of the market in North America is due to growing demand of diagnostic imaging technologies in the region.

Diagnostic Imaging Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 39.93 Billion |

| Market Size by 2031 | US$ 60.17 Billion |

| Global CAGR (2023 - 2031) | 5.26% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Modality

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Diagnostic Imaging Market Players Density: Understanding Its Impact on Business Dynamics

The Diagnostic Imaging Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Diagnostic Imaging Market News and Recent Developments

The Diagnostic Imaging market is evaluated by gathering qualitative and quantitative data from primary and secondary research, which includes essential corporate publications, association data, and databases. A few of the developments in the Diagnostic Imaging market are listed below:

- Wipro GE Healthcare announced the launch of its next-generation Revolution Aspire CT (Computed Tomography) scanner. Revolution Aspire is an advanced imaging solution designed and manufactured end-to-end in India, at the newly launched Wipro GE Medical Devices Manufacturing plant, in line with ‘Atmanirbhar Bharat’ initiative. The CT system is equipped with higher imaging intelligence to improve clinical confidence when diagnosing diseases and anomalies. (Source: GE HealthCare, Press Release, 2022)

- Zionexa, a leading innovator of in-vivo oncology and neurology biomarkers that help enable more personalized healthcare, has been acquired by GE Healthcare. Cerianna (fluoroestradiol F-18), an FDA-approved PET imaging agent used as an adjunct to biopsy for the detection of oestrogen receptor (ER) positive lesions to help inform treatment selection for patients with recurrent or metastatic breast cancer, is being scaled up by the company. (Source: GE HealthCare, Press Release, 2021)

Diagnostic Imaging Market Report Coverage and Deliverables

The “Diagnostic Imaging Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Diagnostic Imaging market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Diagnostic Imaging market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Diagnostic Imaging market analysis covering key market trends, global and regional framework, significant players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Diagnostic Imaging market

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For