Oncology Biosimilars Market Share and Forecast by 2031

Coverage: By Drug Class (Monoclonal Antibodies, Granulocyte Colony-Stimulating Factor, and Erythropoiesis-Stimulating Agents ), Cancer Type (Colorectal Cancer, Cervical Cancer, Breast Cancer, Supportive Care, Lymphoma, and Others), and Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy)

- Status : Data Released

- Report Code : TIPRE00002766

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : June 03, 2024

2024 Market Size

US$ 9,249.48 Mn

Base year value

2031 Forecast

US$ 26,618.00 Mn

Projected by 2031

CAGR 2025-2031

16.3 %

Growth rate

Addressable Market

US$ 123,923.81 Mn

(2025-2031)

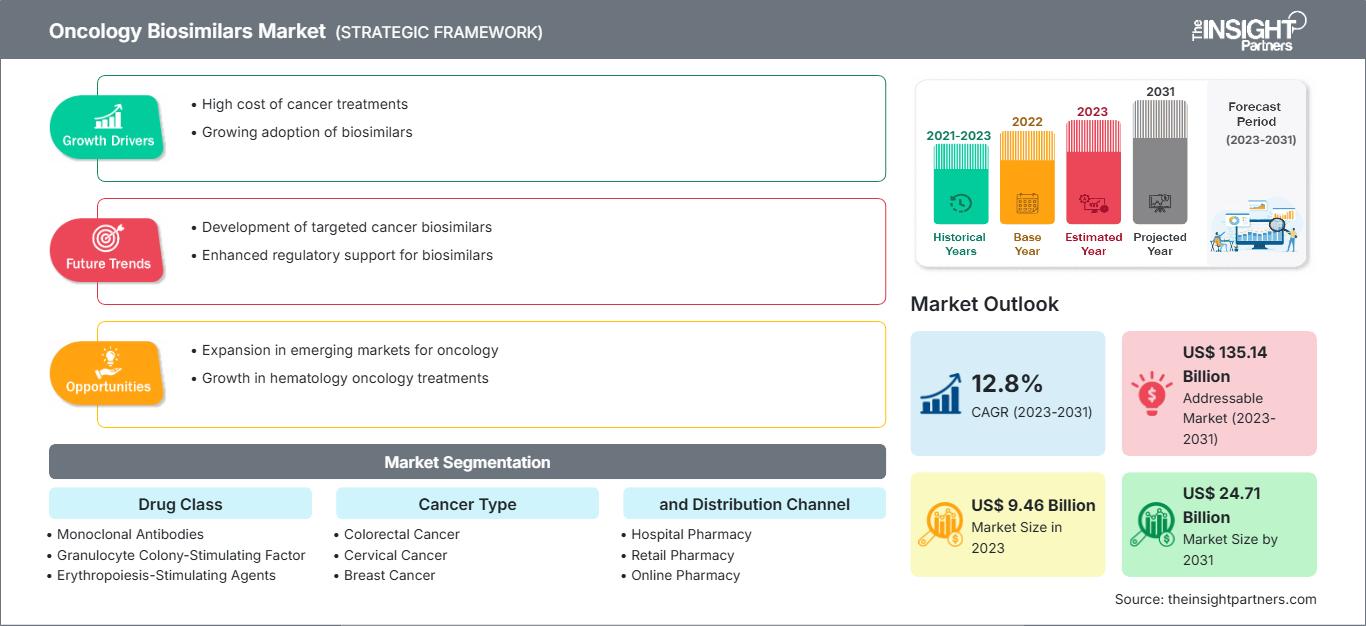

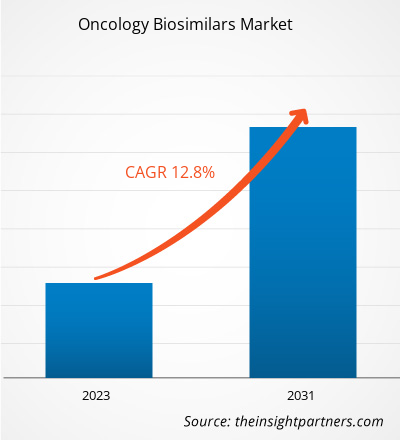

The Oncology Biosimilars Market size is expected to reach US$ 26,618 million by 2031. The market is anticipated to register a CAGR of 16.3% during 2025–2031.

Market Insights and Analyst View:

Biosimilars are biopharmaceutical products that closely resemble existing reference biologic drugs in terms of safety, efficacy, and quality but are not identical. Biosimilars such as monoclonal antibodies and supportive agents, including filgrastim, pegfilgrastim, epoetin α, and epoetin ζ, are available to treat various types of cancers. Factors such as a surge in incidences of cancers, the cost-effectiveness of biosimilar drugs, and a rise in the approvals of oncology biosimilars. Additionally, the collaborations among manufacturers for biosimilars and clinical trials are expected to bring new oncology biosimilars market trends in the coming years. However, high-cost involvement and complexities in biosimilar product manufacturing are among the market deterrent factors.

Oncology Biosimilars Market Size and Share – Market Drivers:

According to the World Health Organization (WHO), in 2022, ~20 million new cancer cases and 9.7 million deaths caused by cancer were reported worldwide. Additionally, the latest estimates from WHO’s Global Cancer Observatory indicated that in 2022, 10 different types of cancer accounted for approximately two-thirds of new cancer cases and deaths worldwide. Among these, lung cancer was the most commonly occurring cancer globally, accounting for 2.5 million new cases and 12.4% of the total new cases. Female breast cancer ranked second with 2.3 million cases and 11.6% of the total new cases, followed by colorectal cancer, accounting for 9.6% of the total new cases. Prostate cancer ranked fourth with 1.5 million cases, and stomach cancer ranked fifth with 970,000 cases. The advent of more affordable oncology biosimilars as a medical armamentarium can reduce the burden on healthcare expenditure and improve access to efficient cancer therapies because of their demonstrated safety and efficacy in real-world scenarios, clinical evidence, and physicochemical quality data. For instance, in an article published by the Multidisciplinary Digital Publishing Institute (MDPI) in July 2023, a comparative and descriptive study was performed to evaluate the safety information of biosimilar monoclonal antibodies (mAbs) used in cancer with that of the corresponding reference medicines and assess the post-marketing pharmacovigilance data. The study concluded that there were no significant variations in the safety profiles of bevacizumab, trastuzumab, and rituximab biosimilars and their originators. The results validated the safety equivalency of biosimilars and supported their use as competitive substitutes for biologic originators. Therefore, the growing burden of cancer and increasing deaths due to it creates the need for affordable treatments, which boosts the oncology biosimilars market growth.

Market Assessment and Insights

- Global market for Oncology Biosimilars was valued at US$ 9,249.48 Million in 2024

- Annual market size is expected to reach US$ 26,618.00 Million by 2031

- Total addressable market (TAM) during 2025-2031 is projected to reach approximately US$ 123,923.81 Million

- Market is anticipated to register a CAGR of 16.3% during the forecast period

- The United States represents a key market, supported by High cost of cancer treatments, Growing adoption of biosimilars, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion in emerging markets for oncology, Growth in hematology oncology treatments are expected to influence market dynamics and addressable market

- Report profiles industry participants, including CELLTRION, Inc., Teva Pharmaceutical Industries Ltd, Pfizer Inc, Sandoz Group AG, Biocon, Amgen Inc, Samsung Bioepis, Coherus BioSciences, BIOCAD, Lilly, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Oncology Biosimilars Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Segmentation and Scope:

The “Oncology Biosimilars Market Analysis and Forecast to 2030” is a specialized and in-depth study focusing on the global market dynamics to help identify the key drivers, future market trends, and lucrative market opportunities that would, in turn, aid in identifying major revenue pockets. The report aims to provide an overview of the market with detailed market segmentation on the basis of drug class, cancer type, and distribution channel. The report also includes a comprehensive analysis of the leading market players and their key strategic developments. The scope of the oncology biosimilars market report includes the assessment of the market performance in North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa.

Segmental Assessment:

The market, based on drug class, is segmented into monoclonal antibodies, granulocyte colony-stimulating factors, and erythropoiesis-stimulating agents(ESAs) . In 2023, the monoclonal antibodies segment held the largest oncology biosimilars market share and is anticipated to register the highest CAGR from 2023 to 2031. Monoclonal antibodies can destroy cancer cells through multiple methods, such as by obstructing ligand-receptor growth and survival pathways. The primary mechanism of action includes antibody-dependent cellular cytotoxicity (ADCC) and complement-mediated cytotoxicity. Rituximab, Trastuzumab, and Bevacizumab were a few biosimilar monoclonal antibodies approved by the European Medicines Agency (EMA) and the Food and Drug Administration (FDA) for cancer treatment until December 2019.

The market, based on cancer type, iscategorized as colorectal cancer, cervical cancer, breast cancer, supportive care, lymphoma, and others. The supportive care segment held the largest market share in 2023. Colorectal cancer is projected to register the highest CAGR from 2023 to 2031. According to WHO, cancer is a critical health concern and the primary cause of fatalities globally. With the growing prevalence of cancer, many oncology biosimilar manufacturers are engaged in developing and launching new products in the market. For instance, CT-P16 by Celltrion, 163 HD204 by Prestige Biopharma, CBT124 by Cipla Biotech, and MIL60 by Beijing Mabworks Biotech are potential biosimilars of bevacizumab that are currently undergoing phase 3 studies and being compared on the parameters of safety and efficacy. They are also being evaluated for their ability to treat patients suffering from non-small cell lung cancer.

The market, based on distribution channel, is segmented into hospital pharmacy, retail pharmacy, and online pharmacy.In 2022, the hospital pharmacy segment held the largest market share.Online pharmacy segment is expected to register the highest CAGR from 2023 to 2031. Hospital pharmacies are the primary platform where patients can buy prescription drugs such as biosimilars.

Regional

Analysis:

In terms of revenue, North America accounted for a major oncology biosimilars market share in 2023, followed by Europe. The growing cases of cancer, rising approvals of biosimilars for cancer treatment, and the advanced healthcare infrastructure are the factors anticipated to propel the oncology biosimilars market in North America during the forecast period.

The growing cases of cancer, rising approvals of biosimilars for cancer treatment, and the advanced healthcare infrastructure are the factors anticipated to propel the oncology biosimilars market in North America. Biologics are the most expensive medicines in the US. Biosimilars are expected to be more cost-effective than their reference products. In an article published by PubMed Central in October 2022, a cost comparison was conducted using the average wholesale price (AWP) per unit of biologics and biosimilars based on the drug prices in the US as of June 2021. The analysis stated that biosimilars can offer savings of 15–23% for bevacizumab. Among bevacizumab biosimilars, Zirbes offers significantly higher savings when compared to the originator product, Avastin. Biosimilars for supportive cancer care agents such as Filgrastim biosimilars offer savings ranging from 17.3% to 34% when compared to their reference products, while pegfilgrastim biosimilars offer savings from 33% to 37%. Also, Epogen biosimilar offers savings of 33.5%. According to the Cardinal Health Biosimilars Report published in 2022, the FDA has approved 33 biosimilars in the US, and 21 are commercially available. Out of these, 17 are being used for cancer treatments. As per the same source, biosimilars are expected to reduce US drug expenditure by US$ 133 billion by 2025. Thus, in the US, biosimilars have immense potential for lowering the costs of biologic medicine, making care more accessible to patients, and creating innovations and scientific breakthroughs, thereby driving the oncology biosimilars market in this region.

Oncology Biosimilars Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 9,249.48 Million |

| Market Size by 2031 | US$ 26,618.00 Million |

| Global CAGR (2025 - 2031) | 16.3% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Drug Class

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Oncology Biosimilars Market Players Density: Understanding Its Impact on Business Dynamics

The Oncology Biosimilars Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industry Developments and Future Opportunities:

Theoncology biosimilars market forecast can help stakeholders in this marketplace plan their growth strategies.As per the company press release, below are a few key developments and initiatives taken by key players operating in the oncology biosimilars market:

- In November 2022, Organon launched a biosimilar of Avastin, AYBINTIO, in Canada. The treatment is available for patients in Canada who are affected by certain aggressive forms of cancer, including metastatic colorectal cancer (mCRC); metastatic lung cancer; platinum-sensitive and resistant recurrent epithelial ovarian, including fallopian tube and primary peritoneal cancer; and glioblastoma. This launch aims to expand the company's biosimilar portfolio.

- In May 2022, Biocon Biologics and Viatris launched Abemy, a biosimilar to Roche’s Avastin (Bevacizumab). Biocon Biologics Ltd., a subsidiary of Biocon Ltd., and Vietris’ Inc. announced the availability of this oncology biosimilar in Canada. bevy, co-developed by Biocon Biologics and Vietri’s, has been approved by Health Canada for four types of cancers.

- In April 2020, Pfizer received approval from the European Commission (EC) for RUXIENCE, which is a monoclonal antibody (mob) and biosimilar to Mather (rituximab). This approval was for treating certain cancers, such as non-Hodgkin’s lymphoma (NHL), chronic lymphocytic leukemia (CLL), and autoimmune conditions.

- In January 2020, Chorus Biosciences entered into a license agreement with Innocents Biologics Co., Ltd. for the development and commercialization of bevacizumab (Avastin) biosimilar of any dosage form and presentation in the US and Canada.

Competitive Landscape and Key Companies:

CELLTRION, Inc.; Teva Pharmaceutical Industries Ltd; Pfizer Inc; Sandoz Group AG; Biocon; Amgen Inc; Samsung Bioepis; Coherus BioSciences; BIOCAD; and Lilly are among the top players profiled in the oncology biosimilars market report. These companies focus on presenting new hi-tech products, technological advancements in existing products, and geographic expansions to meet the growing consumer demand worldwide.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends