Organic Flour Market Developments and Forecast by 2031

Coverage: By Product Type (Wheat Flour, Oat Flour, Corn Flour, Rice Flour, and Others), Category (Conventional and Gluten-Free), Distribution Channel (Supermarket and Hypermarket, Convenience Stores, Online Retail, and Others)

- Status : Published

- Report Code : TIPRE00017870

- Category : Food and Beverages

- No. of Pages : 223

- Available Report Formats :

- Last update date : June 14, 2024

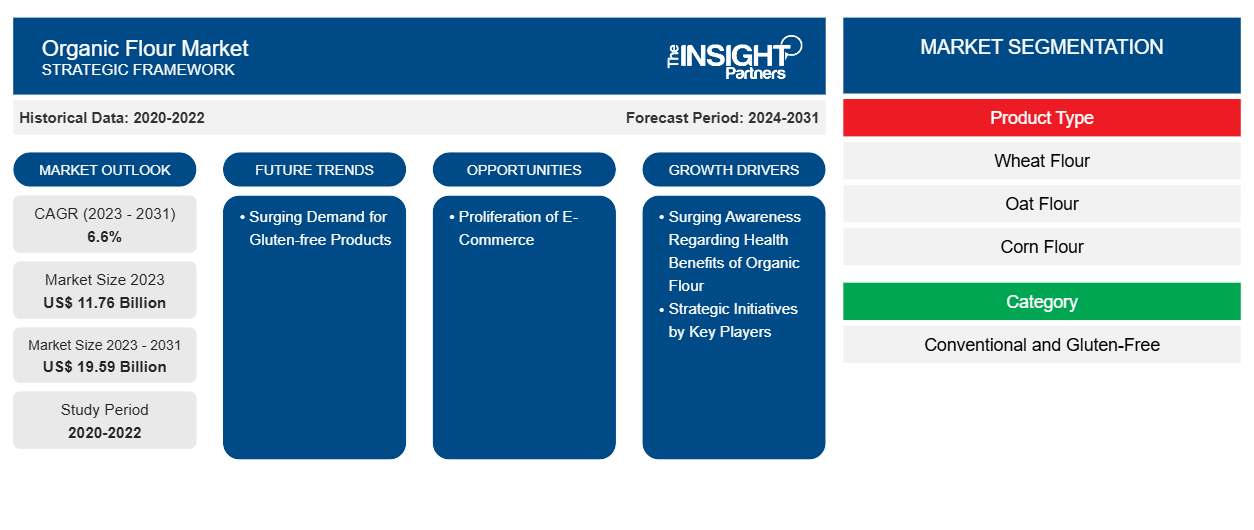

2023 Market Size

US$ 11.76 Bn

Base year value

2031 Forecast

US$ 19.59 Bn

Projected by 2031

CAGR 2024-2031

6.6 %

Growth rate

Addressable Market

US$ 126.78 Bn

(2024-2031)

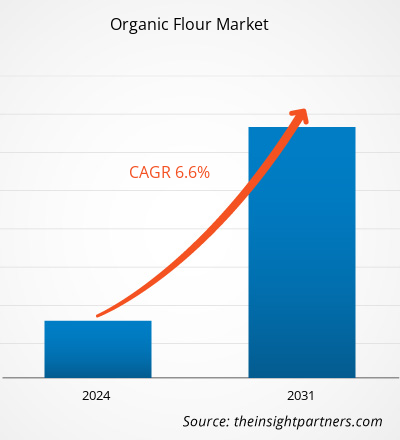

The organic flour market size is expected to grow from US$ 11.76 billion in 2023 to US$ 19.59 billion by 2031; it is estimated to register a CAGR of 6.6% from 2023 to 2031.

Market Insights and Analyst View:

The demand for organic flour has surged as consumers are becoming more health-conscious and seeking organic products. Organic flour is produced from grains grown without toxic pesticides, synthetic fertilizers, or genetic engineering techniques. Its demand has surged due to increasing consumer preferences for healthier, environmentally friendly, and ethically produced food products. Additionally, the rich nutritional value and potential health benefits of organic foods have contributed to the increase in demand. This surge is part of the larger trend in the organic food industry, which has seen significant growth in recent years. In addition, owing to a growing awareness of environmental sustainability, many consumers are opting for organic products to support more eco-friendly farming practices that prioritize soil health and biodiversity. Further, the desire to support local farmers and small-scale producers and offer transparency in food production contributes to the rising demand for organic flour.

Growth Drivers and Challenges:

Strategic initiatives such as mergers and acquisitions, partnerships, campaign launches, and product launches undertaken by various market players to strengthen their positions and capitalize on emerging opportunities are expected to contribute to the growing organic flour market size. For instance, in 2020, ADM acquired the remaining 50% stake in the UK-based organic flour milling company Gleadell Agriculture Ltd. This acquisition enabled ADM to expand its presence in the organic flour market and strengthen its supply chain capabilities. Campaign launches aimed at raising awareness and educating consumers about the benefits of organic flour also play a vital role in driving market growth. Key players often invest in marketing campaigns highlighting organic flour's nutritional advantages, environmental sustainability, and quality standards. These campaigns help create demand, shape consumer preferences, and differentiate organic flour products from conventional alternatives. These campaigns include digital advertising, social media promotions, and educational content to raise consumers' awareness about the advantages of using organic flour in their baking and cooking.

Product launches are integral for maintaining competitiveness and meeting evolving consumer preferences in the organic flour market. Key players continuously innovate and introduce new organic flour products tailored to specific dietary needs, taste preferences, and occasions. For instance, gluten-free organic flour variants cater to consumers with gluten intolerance or sensitivity, while specialty flours such as almond flour or coconut flour appeal to health-conscious consumers seeking alternative baking ingredients. For example, in 2021, Hodgson Mill introduced a new line of organic flour, including organic whole wheat flour, organic all-purpose flour, and organic pastry flour, to cater to consumers seeking organic alternatives for their baking needs and demonstrate Hodgson Mill's commitment to meeting the growing demand for organic flour options. Also, several companies are entering the organic market by launching products such as organic flour.

Regulatory compliances associated with organic flour such as stringent standards and certification processes mandated by regulatory authorities, including the USDA and the EU Organic Regulation, are expected to restrain the global organic flour market growth. Acquiring organic certification entails comprehensive inspections, documentation, and adherence to specific organic farming practices, all of which demand significant time and financial investment from producers. This exhaustive process can act as a deterrent for smaller producers or those with limited resources, hampering the ability to enter or expand within the organic flour market.

Market Research Highlights

- North America dominated the market with 35.5% share in 2023.

- Asia Pacific is poised to grow at a CAGR of 7.4% over the forecast period.

- United States market is projected to grow at a CAGR of 6.3% over the forecast period.

- By Product Type, the Wheat Flour segment accounted for the largest market share of 39.4% in 2023.

- By Category, the Gluten-Free segment is anticipated to witness the fastest growth, registering a CAGR of 7% over the forecast period

- By Distribution Channel, the Supermarket and Hypermarket segment accounted for the largest market share of 46% in 2023.

- The report profiles key industry players such as Bob’s Red Mill Natural Foods, HOMETOWN FOOD COMPANY, BetterBody Foods c/o, King Arthur Baking Company, KoRo, FWP Matthews Ltd, Shipton Mill Ltd, W and H Marriage and Sons Limited, Gilchesters Organics, ANITA’S ORGANIC GRAIN & FLOUR MILL LTD., while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Organic Flour Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Report Segmentation and Scope:

The "Global Organic Flour Market Analysis" has been performed by considering the following segments: product type, category, distribution channel, and geography. Based on product type, the organic flour market is segmented into wheat flour, oat flour, corn flour, rice flour, and others. Based on category, the market is segmented into conventional and gluten-free. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, online retail, and others. The geographic scope of the organic flour market report focuses on North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and the Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and the Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

Segmental Analysis:

Based on product type, the market is segmented into wheat flour, oat flour, corn flour, rice flour, and others. Based on type, the gluten-free segment is anticipated to hold a significant organic flour market share by 2030. Gluten-free flour is designed for individuals affected by celiac disease or gluten sensitivity and those opting for a gluten-free diet. The demand for gluten-free claims products has upsurged significantly due to the increasing prevalence of gluten-related disorders and a broader health-conscious trend. According to Beyond Celiac, 1 in 133 Americans, or ~1% of the population, suffer from celiac disease in the US. Celiac disease awareness has led many consumers to seek gluten-free alternatives, creating a substantial market for products that cater to dietary restrictions. Moreover, the perception that gluten-free options may be healthier has expanded the consumer base beyond those suffering from medical conditions, contributing to the sustained growth of the organic flour market for the gluten-free segment.

Regional Analysis:

Based on geography, the market is segmented into five key regions—North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa. In terms of revenue, North America dominated the global organic flour market share. The market in North America accounted for ~US$ 2,900 million in 2023. The Asia Pacific organic flour market is expected to grow at a highest CAGR during the forecast period. Asia Pacific is experiencing rapid urbanization and changing consumer lifestyles. Urban consumers seek organic flour as a critical ingredient for homemade bread, pastries, and other baked goods. Also, the shift toward home baking has been accelerated by factors such as the COVID-19 pandemic, which prompted more consumers to explore cooking and baking at home. As a result, the demand for organic flour as a versatile and nutritious baking ingredient has grown substantially in Asia Pacific, supporting the market expansion.

Asia Pacific is home to diverse agricultural landscapes and traditional farming practices, providing ample opportunities for organic flour production. Countries such as India, China, and Australia have witnessed a rise in organic farming initiatives supported by government policies promoting sustainable agriculture and organic certification programs. This growing interest in organic farming has increased the availability of organic grains and flour produced in the region. The increasing awareness of health and wellness is driving the organic flour market growth in Asia Pacific.

Europe is another major contributor, holding more than 30% of the global market share. Consumers across Europe are increasingly concerned about food safety, environmental sustainability, and the impact of agricultural practices on public health. This has led to a growing preference for organic products, including flour. Consumers in Europe actively seek organic flour produced without synthetic pesticides, herbicides, or GMOs, viewing it as a much safer and more environmentally friendly option than conventional flour. This shift toward organic flour is also driven by changing consumer lifestyles and dietary preferences, with many Europeans opting for healthier and more natural food choices.

Organic Flour Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 11.76 Billion |

| Market Size by 2031 | US$ 19.59 Billion |

| Global CAGR (2023 - 2031) | 6.6% |

| Historical Data | 2020-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Organic Flour Market Players Density: Understanding Its Impact on Business Dynamics

The Organic Flour Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industry Developments and Future Opportunities:

The organic flour market forecast can help stakeholders plan their growth strategies. The following are initiatives taken by the key players operating in the organic flour market:

- In 2022, Dairy major GCMMF, which markets its products under the Amul brand, announced entry into the organic food market with the launch of organic wheat flour. The first product launched in this portfolio is "Amul Organic Whole Wheat Atta."

Competitive Landscape and Key Companies:

Hometown Food Company, Bob's Red Mill Natural Foods, Betterbody Foods C/O, FWP Matthews Ltd, Shipton Mill Ltd, W and H Marriage and Sons Limited, Gilchesters Organics, and Anita's Organic Grain & Flour Mill Ltd. are among the prominent players profiled in the organic flour market report. Players operating in the global market focus on providing high-quality products to fulfill customer demand. They are also adopting various strategies such as new product launches, capacity expansions, partnerships, and collaborations in order to stay competitive in the market.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends