微量残留病害检测市场分析及预测(按规模、份额、增长、趋势划分)2031 年

历史数据 : 2021-2022 | 基准年 : 2023 | 预测期 : 2024-2031微小残留疾病检测市场规模和预测(2021-2031 年)、全球和区域份额、趋势和增长机会分析报告覆盖范围:按技术(流式细胞术、PCR、NGS 等)、癌症类型(白血病、淋巴瘤、实体瘤和多发性骨髓瘤)、最终用户(医院、专科诊所、诊断实验室等)和地理区域(北美、欧洲、亚太地区、南美和中美、中东和非洲)

- 状态 : 数据发布

- 报告代码 : TIPRE00039104

- 类别 : 生命科学

- 页数 : 150

- 可用报告格式 :

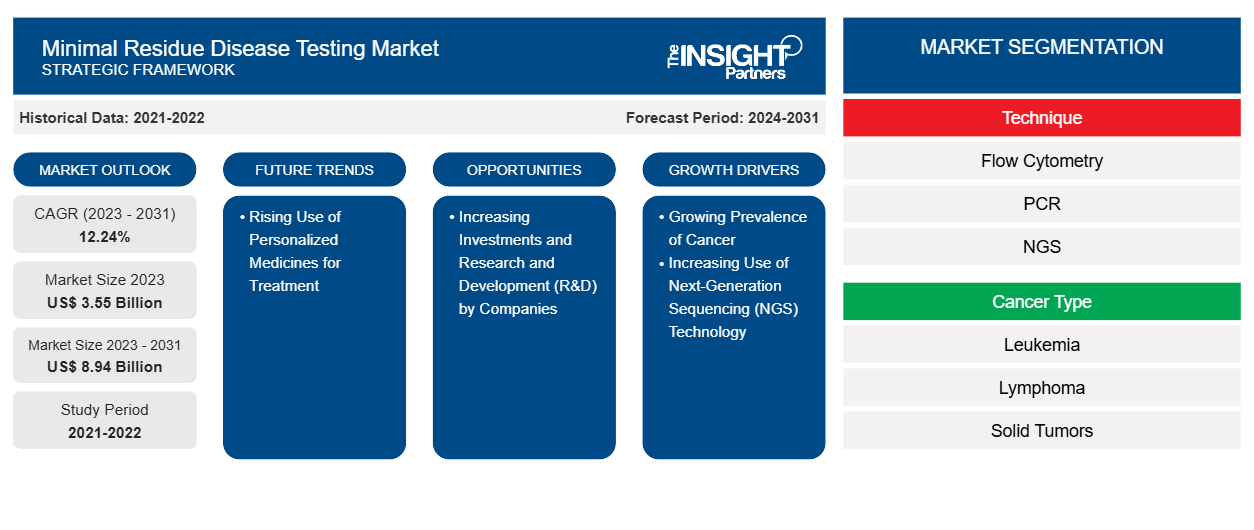

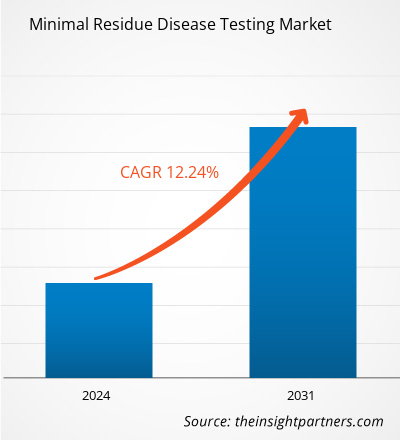

微小残留病害检测市场规模预计将从 2023 年的 35.5 亿美元飙升至 2031 年的 89.4 亿美元;预计 2023-2031 年期间的复合年增长率为 12.24%。

分析师观点:

该报告包括由于当前微小残留病检测市场趋势及其在预测期内可预见的影响而产生的增长前景。全球各种癌症(如白血病、淋巴瘤和实体瘤)的患病率不断上升,对微小残留病检测产品和服务的需求也不断增加。医疗保健提供者和研究人员认识到微小残留病评估在监测治疗反应、预测复发和指导治疗干预方面的临床效用。随着微小残留病检测不断发展并成为癌症管理的重要工具,市场参与者专注于创新、标准化和可及性,以利用微小残留病检测市场中的丰厚机会。

市场概况:

将微小残留病检测纳入健康保险计划以及将这种检测方法应用于实体肿瘤诊断是推动微小残留病检测市场发展的因素。随着全球消费者意识的增强,对微小残留病检测的需求也随之增加。医疗保健提供者和研究人员认识到这一趋势,并努力通过将微小残留病检测整合到临床实践中来满足患者的期望。推动微小残留病检测市场增长的其他关键因素包括癌症患病率的上升和下一代测序技术的使用增加。

定制此报告以满足您的需求

您可以免费定制任何报告,包括本报告的部分内容、国家级分析、Excel 数据包,以及为初创企业和大学提供优惠和折扣

微量残留疾病检测市场:战略洞察

-

获取此报告的关键市场趋势。这个免费样品将包括数据分析,从市场趋势到估计和预测。

市场驱动因素:

癌症患病率上升推动市场增长

2020年,癌症病例达到1930万,癌症死亡人数达到996万。根据国际癌症研究机构的数据,预计到2025年癌症病例数将达到2190万,到2030年将达到2460万。根据美国临床肿瘤学会2021年2月的报告,美国约有235,760名成年人(119,100名男性和116,6600名女性)被诊断出患有肺癌。GLOBOCAN 2020的数据显示,印度占全球新发癌症病例总数的18.3%;此外,宫颈癌占所有癌症病例的9.4%。根据美国癌症协会(ACS)的数据,2021年美国发现了近26,560例新的胃癌病例,其中男性16,160例,女性10,400例。美国国家乳腺癌基金会 2021 年 7 月发布的统计数据显示,约 63% 的乳腺癌患者被诊断为局部乳腺癌,27% 被诊断为区域性乳腺癌,6% 被诊断为远处(转移性)疾病。此外,全球血癌患病率的不断上升,也推动了对更好的治疗方案和去除残留癌细胞准确性的需求。根据美国癌症协会发布的统计数据,2022 年 1 月,美国诊断出约 34,920 例多发性骨髓瘤新病例。癌症病例数量的激增可能会迫使政府推出新的癌症预防计划,这有望推动微量残留疾病检测市场的增长。

节段分析:

最小残留疾病检测市场分析已考虑以下几个部分:技术、癌症类型和最终用途。

根据技术,微量残留疾病检测市场细分为流式细胞术、PCR、NGS 等。流式细胞术细分市场在 2023 年占据了最大的市场份额。PCR 细分市场预计在 2023-2031 年期间的复合年增长率最高,为 12.39%。PCR 方法可以根据突变或染色体变化等特征性遗传异常检测癌细胞。该技术必然涉及微小 DNA 或 RNA 片段的扩增,以帮助提高其可检测性和可计数性。即使使用含有少量癌细胞的样本(例如血细胞或骨髓),也可以识别遗传异常。PCR 的高灵敏度使其能够从 100,000 个正常细胞中检测到少至一个癌细胞。获取测试结果可能需要 5-14 天。

根据癌症类型,市场分为白血病、淋巴瘤、实体瘤和多发性骨髓瘤。2023 年,实体瘤细分市场占据了最小残留病检测市场份额的最大值。该细分市场的市场增长归因于正在进行的针对评估实体瘤患者的研究。目前尚无关于使用 MRD 检测检测非血液系统恶性肿瘤的公认建议。将循环肿瘤 DNA (ctDNA) 作为实体瘤治疗后残留分子病诊断的预后生物标志物的方法正在迅速被纳入临床试验设计和转化研究调查中。这种方法适用于标准临床护理。尽管 ctDNA 检测技术发展迅速,但这些检测方法的低灵敏度降低了它们在各种临床应用中检测 MRD 的实用性。

根据最终用户,微量残留病检测市场分为医院、专科诊所、诊断实验室和其他。医院部门在 2022 年占据了微量残留病检测最大的市场份额,预计在 2023-2031 年期间将录得 12.79% 的最高复合年增长率。医院占据了相当大的市场份额,这主要归因于其在急性护理和患者管理中的作用。对于患有严重健康状况的患者来说,住院通常是必要的,因为医院设施可以提高决策能力,让医生和医疗保健专业人员分析患者并为他们提供更好的治疗选择。

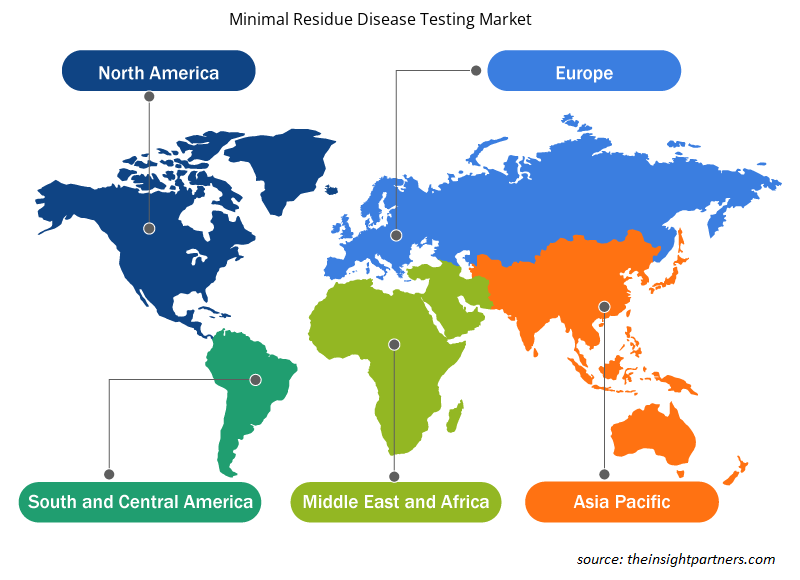

区域分析:

微量残留病检测市场报告的范围包括北美、欧洲、亚太地区、中东和非洲以及南美和中美。北美市场在 2023 年的价值为 9.3 亿美元,预计到 2031 年将达到 23.4 亿美元;预计在 2023-2031 年期间的复合年增长率为 12.12%。癌症发病率的显著增加;最新技术的引入;以及已建立的蛋白质组学、基因组学和肿瘤学研究基础设施巩固了北美作为微量残留病检测市场主要贡献者的地位。

亚太地区微量残留病检测市场预计将录得最快的复合年增长率 12.68%。该地区,尤其是印度和中国等国家,拥有庞大的制药业。2021 年 10 月,Genetron Health(中国)和江苏复星(中国)开始在中国商业化 MRD 检测测试。他们过去还在中国专注于血液学的医院和诊所推广过 Seq-MRD。该测试提供准确性、高通量、成本效益、一致性和快速的周转时间。主要市场参与者将研究视为开发新型测试的主要关注领域。除了对研究的日益关注之外,对治疗后癌症患者监测的需求不断增长,继续推动亚太地区微量残留病检测市场的进步。此外,医疗保健基础设施的改善和新兴的制药行业使亚太地区成为市场显着增长和发展的关键枢纽。

关键球员分析:

Adaptive Biotechnologies;Natera;Bio-Rad Laboratories;F-Hoffmann La Roche Ltd;Guardant Health;LabCorp;Sysmex Corporation;ARUP Laboratories;Invivoscribe, Inc.;NeoGenomics Laboratories, Inc.;和 Mission Bio, Inc 是微残留疾病检测市场报告中介绍的关键参与者。

微量残留病害检测市场区域洞察

Insight Partners 的分析师已详细解释了预测期内影响微量残留病害检测市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的微量残留病害检测市场细分和地理位置。

- 获取微量残留疾病检测市场的区域特定数据

微量残留疾病检测市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2023 年的市场规模 | 35.5亿美元 |

| 2031 年市场规模 | 89.4 亿美元 |

| 全球复合年增长率(2023 - 2031) | 12.24% |

| 史料 | 2021-2022 |

| 预测期 | 2024-2031 |

| 涵盖的领域 |

按技术分类

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

最小残留疾病检测市场参与者密度:了解其对业务动态的影响

微量残留病害检测市场正在快速增长,这得益于终端用户需求的不断增长,这些需求源于消费者偏好的不断变化、技术进步以及对产品优势的认识不断提高等因素。随着需求的增加,企业正在扩大其产品范围,进行创新以满足消费者的需求,并利用新兴趋势,从而进一步推动市场增长。

市场参与者密度是指在特定市场或行业内运营的企业或公司的分布情况。它表明在给定市场空间中,相对于其规模或总市场价值,有多少竞争对手(市场参与者)存在。

在微小残留疾病检测市场运营的主要公司有:

- 自适应生物技术,

- 纳特拉,

- Bio-Rad 实验室,

- F-霍夫曼罗氏有限公司,

- Guardant Health,

- LabCorp,

免责声明:上面列出的公司没有按照任何特定顺序排列。

- 了解最小残留疾病检测市场的主要参与者概况

最新动态:

在微量残留病害检测市场运营的公司采用并购作为主要增长战略。根据公司新闻稿,以下列出了一些近期市场发展情况:

- 2023 年 4 月,Quest Diagnostics 收购了 Haystack Oncology,以扩大其肿瘤学产品组合,包括先进的液体活检技术。此次收购使 Quest 能够通过提供具有高灵敏度诊断功能的工具和其他产品来改善个性化癌症治疗。

- 2023 年 4 月,Integrated DNA Technologies 推出了 Archer FUSIONPlex Core Solid Tumor Panel。这一突破性的检测解决方案经过改进和完善,可以覆盖更广泛的单核苷酸变异 (SNV) 和 indel(即插入、缺失或插入和缺失核苷酸)功能或辅助癌症研究。

- 2022 年 12 月,Adaptive Biotechnologies 推出了 clonoSEQ,用于使用循环肿瘤 DNA (ctDNA) 评估弥漫大 B 细胞淋巴瘤 (DLBCL) 患者的微小残留疾病。

- 2022 年 10 月,Adaptive Biotechnologies 与 Epic Systems Corporation 合作,将 clonoSEQ 检测整合到 Epic 的综合电子病历 (EMR) 系统中。clonoSEQ 检测由美国食品药品管理局 (FDA) 监控和批准,用于检测与多发性骨髓瘤 (MM)、慢性淋巴细胞白血病 (CLL) 和 B 细胞急性淋巴细胞白血病 (ALL) 相关的微小残留疾病。

- 2022 年 8 月,罗氏推出了首款数字 LightCycler 系统,旨在准确量化特定 RNA 和 DNA 的微量含量。

- 2022 年 2 月,Personalis 与 Moores Cancer Center 合作,为晚期实体瘤和血液系统恶性肿瘤患者提供临床诊断检测支持。此次合作的重点是使用新推出的液体活检检测方法进行高灵敏度微小残留病和癌症复发检测研究。

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 微量残留病检测市场

获取免费样品 - 微量残留病检测市场