الحد الأدنى من تحليل بقايا الأمراض واختبار السوق والتنبؤ بها حسب الحجم والمشاركة والنمو والاتجاهات 2031

البيانات التاريخية : 2021-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2024-2031حجم سوق اختبار الحد الأدنى من بقايا المرض وتوقعاته (2021-2031)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب التقنية (قياس التدفق الخلوي، تفاعل البوليميراز المتسلسل، التسلسل التسلسلي للجيل التالي، وغيرها)، ونوع السرطان (سرطان الدم، واللمفوما، والأورام الصلبة، والورم النقوي المتعدد)، والمستخدم النهائي (المستشفيات، والعيادات التخصصية، ومختبرات التشخيص، وغيرها)، والجغرافيا (أمريكا الشمالية، وأوروبا، وآسيا والمحيط الهادئ، وأمريكا الجنوبية والوسطى، والشرق الأوسط وأفريقيا).

- تاريخ التقرير : Mar 2026

- رمز التقرير : TIPRE00039104

- الفئة : علوم الحياة

- الحالة : البيانات الصادرة

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

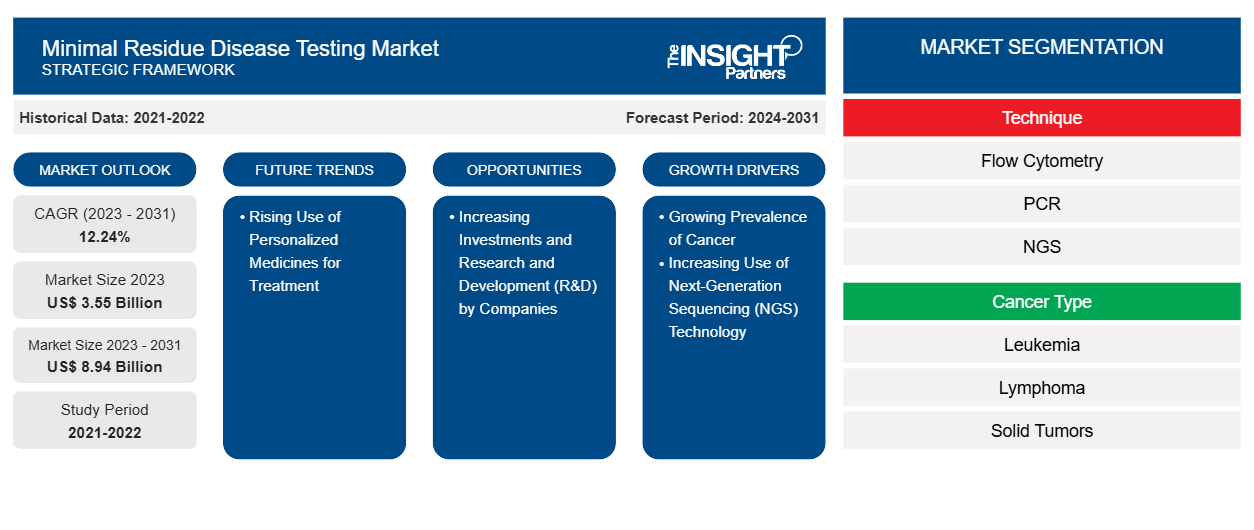

من المتوقع أن يرتفع حجم سوق اختبار الحد الأدنى من بقايا الأمراض من 3.55 مليار دولار أمريكي في عام 2023 إلى 8.94 مليار دولار أمريكي بحلول عام 2031؛ ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 12.24٪ خلال الفترة 2023-2031.

وجهة نظر المحلل:

يتضمن التقرير آفاق النمو بسبب اتجاهات سوق اختبار مرض البقايا الدنيا الحالية وتأثيرها المتوقع خلال فترة التنبؤ. الانتشار العالمي المتزايد لمختلف أنواع السرطان، مثل سرطان الدم والليمفوما والأورام الصلبة، والطلب على منتجات وخدمات اختبار مرض البقايا الدنيا. يدرك مقدمو الرعاية الصحية والباحثون الفائدة السريرية لتقييم مرض البقايا الدنيا في مراقبة استجابة العلاج والتنبؤ بالانتكاس وتوجيه التدخلات العلاجية. مع استمرار تطور اختبار مرض البقايا الدنيا وظهوره كأداة حاسمة في إدارة السرطان، يركز اللاعبون في السوق على الابتكار والتوحيد القياسي وإمكانية الوصول للاستفادة من الفرص المربحة في سوق اختبار مرض البقايا الدنيا.

نظرة عامة على السوق:

إن إدراج اختبار الحد الأدنى من بقايا المرض في خطط التغطية الصحية وتطبيق هذا النهج الاختباري في تشخيص الأورام الصلبة هي العوامل التي تدفع سوق اختبار الحد الأدنى من بقايا المرض. كما زاد الطلب على اختبار الحد الأدنى من بقايا المرض مع زيادة وعي المستهلكين في جميع أنحاء العالم. يدرك مقدمو الرعاية الصحية والباحثون هذا الاتجاه ويسعون جاهدين لتلبية توقعات المرضى من خلال دمج اختبار الحد الأدنى من بقايا المرض في الممارسة السريرية. تشمل العوامل الرئيسية الأخرى التي تدفع نمو سوق اختبار الحد الأدنى من بقايا المرض الانتشار المتزايد للسرطان والاستخدام المتزايد لتكنولوجيا التسلسل من الجيل التالي.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق اختبار الأمراض بالحد الأدنى من البقايا: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محرك السوق:

انتشار السرطان المتزايد يدفع نمو السوق

في عام 2020، بلغ عدد حالات الإصابة بالسرطان 19.3 مليون حالة، وبلغ عدد الوفيات المرتبطة بالسرطان 9.96 مليون حالة. ووفقًا للوكالة الدولية لأبحاث السرطان، من المتوقع أن يصل عدد حالات الإصابة بالسرطان إلى 21.9 مليون حالة بحلول عام 2025 و24.6 مليون حالة بحلول عام 2030. ووفقًا لتقرير فبراير 2021 الصادر عن الجمعية الأمريكية لعلم الأورام السريري، تم تشخيص إصابة حوالي 235760 بالغًا (119100 رجل و1166600 امرأة) في الولايات المتحدة بسرطان الرئة. وتشير بيانات GLOBOCAN 2020 إلى أن الهند تمثل 18.3٪ من إجمالي حالات السرطان الجديدة المسجلة في العالم؛ علاوة على ذلك، يمثل سرطان عنق الرحم 9.4٪ من جميع حالات السرطان. وفقًا للجمعية الأمريكية للسرطان (ACS)، تم اكتشاف ما يقرب من 26560 حالة جديدة من سرطان المعدة في الولايات المتحدة في عام 2021، 16160 رجلاً و10400 امرأة. وفقًا للإحصاءات التي أصدرتها مؤسسة سرطان الثدي الوطنية في يوليو 2021، تم تشخيص حوالي 63٪ من مرضى سرطان الثدي بسرطان الثدي في المرحلة المحلية، وتم تشخيص 27٪ بسرطان الثدي في المرحلة الإقليمية، وتم تشخيص 6٪ بمرض بعيد (نقيلي). بالإضافة إلى ذلك، فإن الانتشار المتزايد لسرطان الدم في جميع أنحاء العالم يعزز الطلب على خيارات علاج أفضل ودقة في إزالة الخلايا السرطانية المتبقية. وفقًا للإحصاءات التي نشرتها الجمعية الأمريكية للسرطان، تم تشخيص ما يقدر بنحو 34920 حالة جديدة من الورم النقوي المتعدد في الولايات المتحدة في يناير 2022. ومن المرجح أن تجبر مثل هذه الزيادة في عدد حالات السرطان الحكومات على إطلاق برامج جديدة للوقاية من السرطان، ومن المتوقع أن يؤدي ذلك إلى دفع نمو سوق اختبار بقايا المرض.

التحليل القطاعي:

تم إجراء تحليل سوق اختبار مرض البقايا الدنيا من خلال النظر في القطاعات التالية: التقنية، ونوع السرطان، والاستخدام النهائي.

بناءً على التقنية، يتم تقسيم سوق اختبار مرض البقايا الدنيا إلى قياس التدفق الخلوي، وتفاعل البوليميراز المتسلسل، وتسلسل الجيل التالي، وغيرها. احتل قطاع قياس التدفق الخلوي أكبر حصة في السوق في عام 2023. ومن المتوقع أن يسجل قطاع تفاعل البوليميراز المتسلسل أعلى معدل نمو سنوي مركب بنسبة 12.39٪ خلال الفترة 2023-2031. يمكن لطريقة تفاعل البوليميراز المتسلسل اكتشاف الخلايا السرطانية بناءً على التشوهات الجينية المميزة مثل الطفرات أو التغيرات الصبغية. تتضمن التقنية بالضرورة تضخيم شظايا صغيرة من الحمض النووي أو الحمض النووي الريبي للمساعدة في اكتشافها وإمكانية عدها. يسمح هذا بتحديد التشوهات الجينية حتى باستخدام عينات (مثل خلايا الدم أو نخاع العظم) تحتوي على عدد نادر من الخلايا السرطانية. تسمح الحساسية العالية لتفاعل البوليميراز المتسلسل باكتشاف خلية سرطانية واحدة فقط من بين 100000 خلية طبيعية. يمكن أن يستغرق الحصول على نتائج الاختبار من 5 إلى 14 يومًا.

ينقسم السوق، بناءً على نوع السرطان، إلى سرطان الدم والليمفوما والأورام الصلبة والورم النقوي المتعدد. احتل قطاع الأورام الصلبة أكبر حصة سوقية لاختبار مرض البقايا الدنيا في عام 2023. يُعزى نمو السوق لهذا القطاع إلى الدراسات البحثية الجارية التي تركز على تقييم المرضى المصابين بأورام صلبة. لا توجد توصيات مقبولة لاستخدام اختبار الحد الأدنى من البقايا للكشف عن الأورام الخبيثة غير الدموية. يتم دمج النهج الذي يتضمن الحمض النووي للورم الدائر (ctDNA) كعلامة حيوية تشخيصية لتشخيص المرض الجزيئي المتبقي بعد علاج الورم الصلب بسرعة في تصميم التجارب السريرية وتحقيقات البحث الترجمي. هذا النهج مناسب للاستخدام في الرعاية السريرية القياسية. على الرغم من تطور تقنيات اكتشاف ctDNA بسرعة، إلا أن الحساسية المنخفضة لطرق الكشف هذه تقلل من فائدتها في اكتشاف الحد الأدنى من البقايا في التطبيقات السريرية المختلفة.

بناءً على المستخدم النهائي، ينقسم سوق اختبار مرض البقايا الدنيا إلى المستشفيات والعيادات المتخصصة والمختبرات التشخيصية وغيرها. احتل قطاع المستشفيات أكبر حصة سوقية لاختبار مرض البقايا الدنيا في عام 2022، ومن المتوقع أن يسجل نفس القطاع أعلى معدل نمو سنوي مركب بنسبة 12.79٪ خلال الفترة 2023-2031. تمتلك المستشفيات حصة كبيرة من السوق، والتي يمكن أن تُعزى في المقام الأول إلى دورها في الرعاية الحادة وإدارة المرضى. غالبًا ما تكون عمليات الدخول إلى المستشفى ضرورية للمرضى الذين يعانون من حالات صحية خطيرة، حيث تتيح مرافق المستشفيات قدرات أفضل في اتخاذ القرار، مما يسمح للأطباء ومقدمي الرعاية الصحية بتحليل المرضى وتقديم خيارات علاج أفضل لهم.

التحليل الإقليمي:

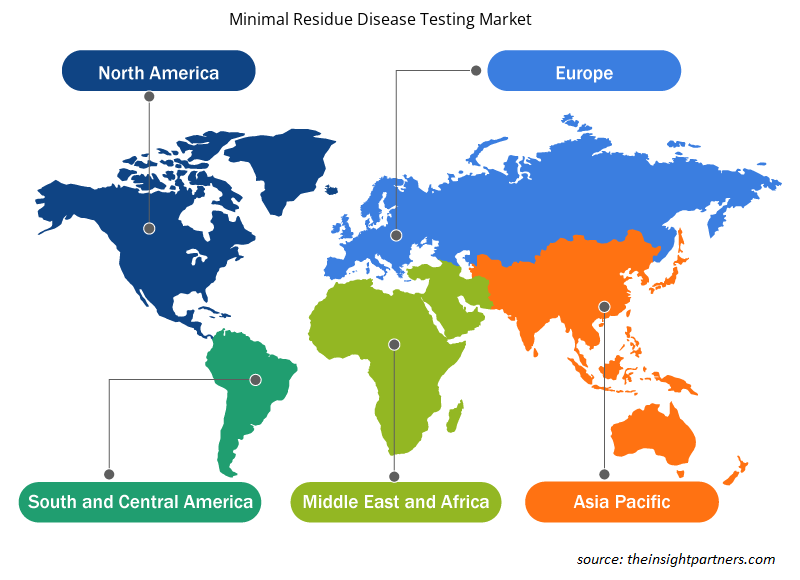

يشمل نطاق تقرير سوق اختبار مرض البقايا الدنيا أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى. بلغت قيمة السوق في أمريكا الشمالية 0.93 مليار دولار أمريكي في عام 2023 ومن المتوقع أن تصل إلى 2.34 مليار دولار أمريكي بحلول عام 2031؛ ومن المتوقع أن تسجل معدل نمو سنوي مركب بنسبة 12.12٪ خلال الفترة 2023-2031. الزيادة الكبيرة في حالات الإصابة بالسرطان؛ وإدخال أحدث التقنيات؛ والبنية الأساسية الراسخة لأبحاث علم البروتينات والجينوم والأورام تعزز مكانة أمريكا الشمالية كمساهم رئيسي في سوق اختبار مرض البقايا الدنيا.

من المتوقع أن يسجل سوق اختبار مرض البقايا الدنيا في منطقة آسيا والمحيط الهادئ أسرع معدل نمو سنوي مركب بنسبة 12.68٪. تعد المنطقة، وخاصة مع دول مثل الهند والصين، موطنًا لصناعة الأدوية الكبيرة. في أكتوبر 2021، بدأت Genetron Health (الصين) وJiangsu Fosun (الصين) في تسويق اختبارات الكشف عن مرض البقايا الدنيا في الصين. كما قاموا أيضًا بالترويج لاختبار Seq-MRD في المستشفيات والعيادات التي تركز على أمراض الدم في الصين في الماضي. يوفر هذا الاختبار الدقة والإنتاجية العالية والفعالية من حيث التكلفة والاتساق وأوقات الاستجابة السريعة. يُنظر إلى البحث باعتباره مجال تركيز أساسي من قبل كبار اللاعبين في السوق لتطوير اختبارات جديدة. بالإضافة إلى التركيز المتزايد على البحث، فإن الحاجة المتزايدة لمراقبة مرضى السرطان بعد العلاج تستمر في دفع تقدم سوق اختبار مرض البقايا الدنيا في منطقة آسيا والمحيط الهادئ. بالإضافة إلى ذلك، فإن التحسينات في البنية التحتية للرعاية الصحية وقطاع الأدوية الناشئ تجعل منطقة آسيا والمحيط الهادئ مركزًا رئيسيًا للنمو والتطوير الكبيرين للسوق.

تحليل اللاعب الرئيسي:

تعد Adaptive Biotechnologies؛ Natera؛ Bio-Rad Laboratories؛ F-Hoffmann La Roche Ltd؛ Guardant Health؛ LabCorp؛ Sysmex Corporation؛ ARUP Laboratories؛ Invivoscribe، Inc.؛ NeoGenomics Laboratories، Inc.؛ و Mission Bio، Inc من بين اللاعبين الرئيسيين الذين تم تحديدهم في تقرير سوق اختبار الأمراض ذات البقايا الدنيا.

رؤى إقليمية حول سوق اختبار الأمراض بالحد الأدنى من المخلفات

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق اختبار مرض البقايا الدنيا طوال فترة التنبؤ بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق اختبار مرض البقايا الدنيا والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق اختبار الأمراض ذات البقايا الدنيا

نطاق تقرير سوق اختبار مرض البقايا الدنيا

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 3.55 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 8.94 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 12.24% |

| البيانات التاريخية | 2021-2022 |

| فترة التنبؤ | 2024-2031 |

| القطاعات المغطاة |

حسب التقنية

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

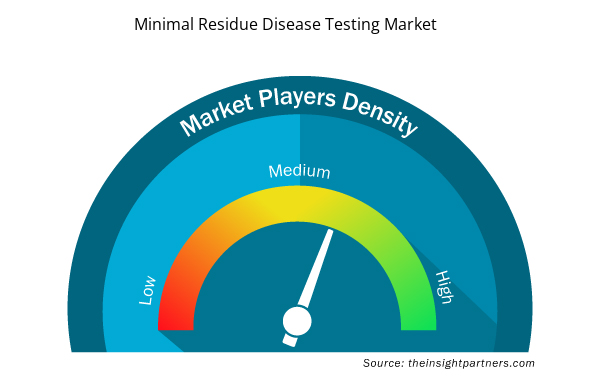

كثافة اللاعبين في سوق اختبار الأمراض المتبقية: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق اختبار الأمراض باستخدام الحد الأدنى من البقايا نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق اختبار مرض الحد الأدنى من البقايا هي:

- التكنولوجيات الحيوية التكيفية

- ناتيرا،

- مختبرات بايو راد،

- شركة اف هوفمان لاروش المحدودة،

- حارس الصحة،

- شركة لاب كورب،

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق اختبار مرض الحد الأدنى من المخلفات

التطورات الأخيرة:

تتبنى الشركات العاملة في سوق اختبار الأمراض التي تتطلب الحد الأدنى من المخلفات عمليات الدمج والاستحواذ كإستراتيجيات رئيسية للنمو. ووفقًا للبيانات الصحفية للشركة، فيما يلي بعض التطورات الأخيرة في السوق:

- في أبريل 2023، استحوذت شركة Quest Diagnostics على شركة Haystack Oncology لتوسيع محفظة علاج الأورام لديها من خلال تضمين تقنية خزعة السائل المتقدمة. وقد سمح هذا الإضافة لشركة Quest بتحسين علاج السرطان الشخصي من خلال توفير أدوات ومنتجات أخرى ذات قدرات تشخيصية عالية الحساسية.

- في أبريل 2023، أطلقت شركة Integrated DNA Technologies لوحة Archer FUSIONPlex Core Solid Tumor Panel. وقد تم تحسين هذا الحل الاختباري الرائد وصقله لتغطية مجموعة أوسع من المتغيرات النوكليوتيدية المفردة (SNVs) وقدرات الحذف (أي الإدراج أو الحذف أو إدراج وحذف النوكليوتيدات) أو المساعدة في أبحاث السرطان.

- في ديسمبر 2022، أطلقت شركة Adaptive Biotechnologies تقنية clonoSEQ لتقييم الحد الأدنى من المرض المتبقي باستخدام الحمض النووي للورم الدائر (ctDNA) لدى المرضى الذين يعانون من سرطان الغدد الليمفاوية المنتشر للخلايا البائية الكبيرة (DLBCL).

- في أكتوبر 2022، دخلت شركة Adaptive Biotechnologies وشركة Epic Systems Corporation في شراكة لدمج اختبار clonoSEQ في نظام السجلات الطبية الإلكترونية الشامل (EMR) الخاص بشركة Epic. تمت مراقبة اختبار clonoSEQ والموافقة عليه من قبل إدارة الغذاء والدواء الأمريكية (FDA) للكشف عن أدنى حد من الأمراض المتبقية المرتبطة بالورم النقوي المتعدد (MM) وسرطان الدم الليمفاوي المزمن (CLL) وسرطان الدم الليمفاوي الحاد B-cell (ALL).

- في أغسطس 2022، أطلقت شركة روش نظام Digital LightCycler الأول الخاص بها، والذي تم تصميمه لقياس كميات ضئيلة من الحمض النووي الريبي والحمض النووي DNA بدقة.

- في فبراير 2022، تعاونت شركة Personalis مع مركز Moores للسرطان لدعم الاختبارات التشخيصية السريرية لدى المرضى المصابين بأورام صلبة متقدمة وأورام خبيثة في الدم. ركز التعاون على إجراء دراسات للكشف عن الأمراض المتبقية شديدة الحساسية وتكرار السرطان باستخدام اختبار خزعة سائل تم تقديمه حديثًا.

مرينال محللة أبحاث مخضرمة، تتمتع بخبرة تزيد عن 8 سنوات في مجال استخبارات واستشارات سوق علوم الحياة. بفضل عقليتها الاستراتيجية والتزامها الراسخ بالتميز، اكتسبت خبرة واسعة في التنبؤ بالصناعات الدوائية، وتقييم فرص السوق، وتطوير معايير الصناعة. يرتكز عملها على تقديم رؤى عملية تُمكّن العملاء من اتخاذ قرارات استراتيجية مدروسة.

تكمن قوة مرينال الأساسية في ترجمة مجموعات البيانات الكمية المعقدة إلى معلومات استخباراتية قيّمة. وتُعدّ براعتها التحليلية ركيزةً أساسيةً في صياغة استراتيجيات دخول السوق (GTM) واكتشاف فرص النمو في قطاعي الأدوية والأجهزة الطبية. وبصفتها مستشارةً موثوقةً، تُركز مرينال باستمرار على تبسيط إجراءات سير العمل وترسيخ أفضل الممارسات، مما يُعزز الابتكار والكفاءة التشغيلية لعملائها.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق اختبار الأمراض ذات البقايا الدنيا

احصل على عينة مجانية ل - سوق اختبار الأمراض ذات البقايا الدنيا