Informe de mercado de gestión de datos de suscriptores 2031 por segmentos, geografía, dinámica, desarrollos recientes e ideas estratégicas

Tamaño y pronóstico del mercado de gestión de datos de suscriptores (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por solución (repositorio de datos de usuario, federación de datos de suscriptores, gestión de políticas y gestión de identidad), tipo de red (redes fijas y redes móviles), implementación (nube y local) y aplicación (voz sobre IP y móvil), y por geografía.

- Estado : Datos publicados

- Código de informe : TIPTE100000738

- Categoría : Tecnología, medios y telecomunicaciones

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : February 15, 2025

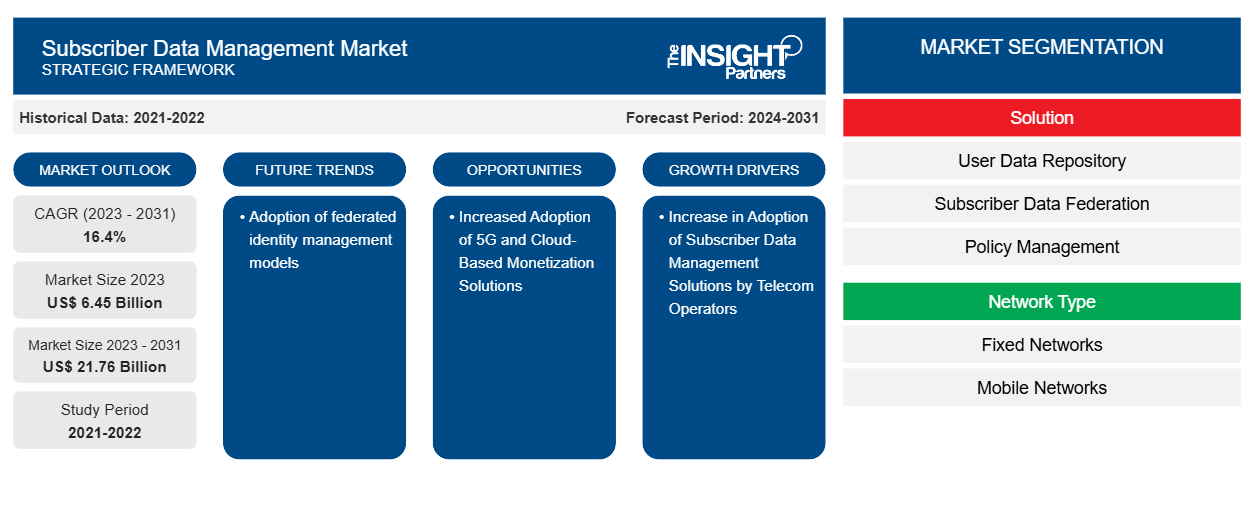

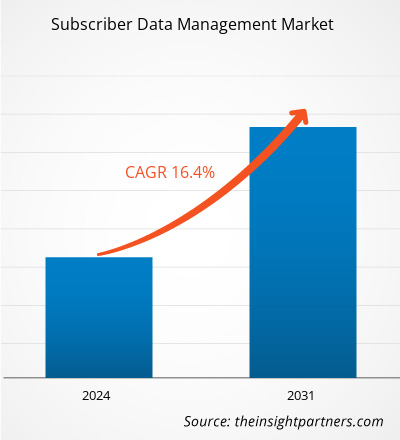

Se prevé que el tamaño del mercado de gestión de datos de suscriptores alcance los 21.760 millones de dólares en 2031, frente a los 6.450 millones de dólares en 2023. Se espera que el mercado registre una CAGR del 16,4 % durante el período 2023-2031. Es probable que la adopción de modelos de gestión de identidad federada siga siendo una tendencia clave en el mercado.

Análisis del mercado de gestión de datos de suscriptores

El aumento en la cantidad de usuarios y dispositivos móviles, así como la implementación de la virtualización de funciones de red (NFV) y sistemas IP, junto con la mayor demanda de los suscriptores de tecnologías LTE y VoLTE, están impulsando la demanda de gestión de datos de suscriptores.

Descripción general del mercado de gestión de datos de suscriptores

La gestión de datos de suscriptores (SDM) se refiere a la forma en que las redes de telecomunicaciones administran de manera eficiente los datos de sus consumidores en una sola ubicación. La práctica de la industria para la gestión de datos era emplear repositorios separados según la ubicación del suscriptor, la red (por ejemplo, 2G/3G/5G) y otros factores. SDM es una solución de sentido común que consolida todos los datos de los suscriptores para una gestión de datos de usuario más eficiente y segura. La solución SDM unifica y administra los datos de los suscriptores de los operadores de red, incluidas las preferencias de acceso, los servicios, las ubicaciones, la autenticación, las identidades y la presencia, en repositorios de datos unificados. Además, mejora las redes de los operadores al reducir sus costos operativos y al mismo tiempo mantener un servicio consistente para los usuarios. También permite a los operadores examinar los datos de los suscriptores de manera centralizada, lo que les permite monetizar sus datos de suscriptores de manera más efectiva. SDM también ayuda a los operadores de telecomunicaciones a reducir la complejidad de la red, el costo total de propiedad y el tiempo de comercialización de nuevos servicios.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de gestión de datos de suscriptores: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Impulsores y oportunidades del mercado de gestión de datos de suscriptores

El aumento de la adopción de soluciones de gestión de datos de abonados por parte de los operadores de telecomunicaciones favorecerá al mercado

La solución de gestión de datos de suscriptores (SDM) converge la gestión de los datos de suscriptores en diferentes dominios de red. La solución SDM unifica y gestiona los datos de suscriptores de los operadores de red, incluidas las preferencias de acceso, los servicios, las ubicaciones, la autenticación, las identidades y la presencia, en repositorios de datos unificados. Además, mejora las redes de los operadores al reducir sus costos operativos y al mismo tiempo mantener un servicio consistente para los usuarios. También permite a los operadores examinar los datos de los suscriptores de manera centralizada, lo que les permite monetizar sus datos de suscriptores de manera más efectiva. SDM también ayuda a los operadores de telecomunicaciones a reducir la complejidad de la red, el costo total de propiedad y el tiempo de comercialización de nuevos servicios.

La necesidad de reducir los gastos operativos y facilitar la convergencia entre redes, así como el aumento de la demanda de los suscriptores de LTE y VoLTE, la implementación de IMS y el cambio de las empresas de telecomunicaciones a tecnologías NFV, impulsarán el crecimiento del mercado de gestión de datos de suscriptores entre las empresas de telecomunicaciones. Además, terceros pueden ayudar a los operadores de telecomunicaciones a proporcionar servicios nuevos y mejorados al proporcionar nuevas cadenas de valor que se reconocen de manera lenta pero constante. Las empresas de telecomunicaciones están estudiando la posibilidad de proporcionar grados similares de personalización y seguimiento de la actividad a sus clientes. Los terceros pueden encontrar los datos de los suscriptores particularmente atractivos para mejorar los servicios que pueden proporcionar aprovechando la infraestructura de los operadores de telecomunicaciones. Por lo tanto, la creciente adopción de soluciones SDM por parte de los operadores de telecomunicaciones está impulsando significativamente el crecimiento del mercado.

Mayor adopción de soluciones de monetización basadas en la nube y 5G

La creciente adopción de la tecnología 5G y de las soluciones de monetización basadas en la nube está impulsando la demanda de soluciones de gestión de datos de suscriptores. La tecnología 5G permite a las empresas de telecomunicaciones recopilar datos de los consumidores en tiempo real y tomar decisiones informadas. Al implementar una gestión del valor del cliente basada en análisis, las telecomunicaciones pueden aumentar los ingresos entre un 5 y un 8 % en solo cuatro semanas. El aumento del procesamiento y el almacenamiento basados en la nube, junto con la expansión de las redes sociales y el contenido de video a pedido de alta definición, impulsa la necesidad de soluciones de gestión de datos de suscriptores. La introducción de las tecnologías de monetización basadas en la nube y 5G crea potencial para los principales participantes de la industria. Las empresas de telecomunicaciones pueden llegar a acuerdos con los creadores de contenido para monetizar experiencias habilitadas para 5G que atraigan a un número menor de usuarios. 5G ofrece a los operadores dos oportunidades comerciales importantes: entretenimiento y juegos de azar.

Análisis de segmentación del informe de mercado de gestión de datos de suscriptores

Los segmentos clave que contribuyeron a la derivación del análisis del mercado de gestión de datos de suscriptores son la solución, el tipo de red, la implementación y la aplicación.

- Según la solución, el mercado está segmentado por repositorio de datos de usuarios, federación de datos de suscriptores, gestión de políticas y gestión de identidades. El segmento de repositorio de datos de usuarios tuvo una participación de mercado significativa en 2023.

- Según el tipo de red, el mercado se segmenta en redes fijas y redes móviles. El segmento de redes fijas tuvo una mayor participación de mercado en 2023.

- Según la implementación, el mercado se segmenta en la nube y en las instalaciones locales. El segmento de la nube tuvo la mayor participación del mercado en 2023.

- Según la aplicación, el mercado está segmentado en voz sobre IP y móvil. El segmento de voz sobre IP tuvo la mayor participación del mercado en 2023.

Análisis de la cuota de mercado de la gestión de datos de suscriptores por geografía

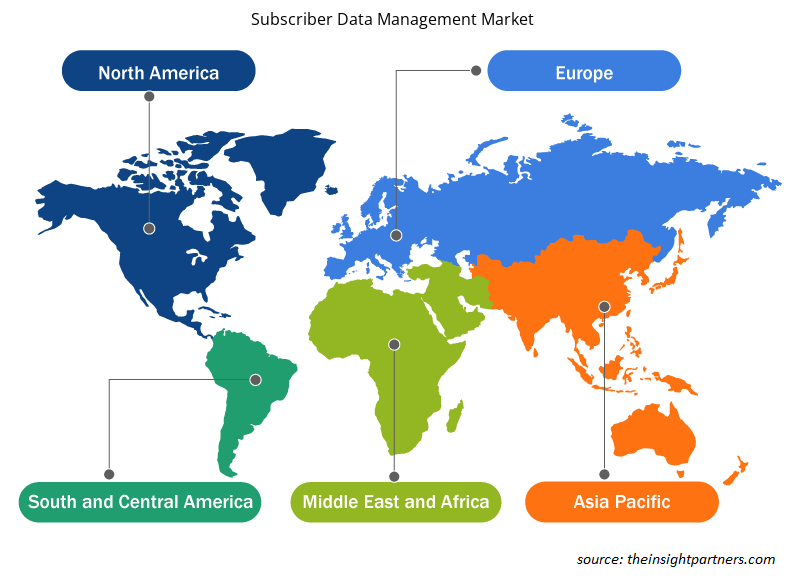

El alcance geográfico del informe de mercado de Gestión de datos de suscriptores se divide principalmente en cinco regiones: América del Norte, Asia Pacífico, Europa, Medio Oriente y África, y América del Sur y Central.

Norteamérica dominó el mercado en 2023. Según el informe de la Asociación GSM, Norteamérica tendrá 100 millones de conexiones 5G en 2022, debido a los continuos gastos en red de los operadores y a una creciente selección de dispositivos 5G en varios niveles de precios. Norteamérica será la primera zona en la que 5G representará más de la mitad de todas las conexiones en 2025. Como resultado, el creciente número de suscriptores de 5G presionaría a los operadores de red a priorizar la gestión adecuada de los planes móviles de los clientes, lo que resultaría en una mayor demanda de gestión de datos de suscriptores. El brote de COVID-19 y los posteriores confinamientos impuestos en países como Estados Unidos, Canadá y México han aumentado significativamente el número de suscriptores de OTT en toda la región. Por ejemplo, según el estudio de 2020 de Comscore, 69,8 millones de hogares en Estados Unidos utilizaron OTT en abril de 2020, un aumento de 5,2 millones con respecto al año anterior.

Además, el streaming de música cayó durante tres semanas consecutivas en marzo de 2020, cuando la pandemia comenzó a tener un impacto sustancial en los EE. UU. Primero un 2%, luego un 8,8% y finalmente un 3,2%. Sin embargo, el streaming de música en los EE. UU. comenzó a experimentar un aumento del 2% en la semana que finalizó el 2 de abril de 2020, y la tendencia ha continuado hasta la fecha. Por lo tanto, el aumento de suscriptores en varias plataformas ha tenido un impacto positivo en el mercado de gestión de datos de suscriptores en toda la región durante la pandemia.

Perspectivas regionales del mercado de gestión de datos de suscriptores

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de gestión de datos de suscriptores durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de gestión de datos de suscriptores en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de gestión de datos de suscriptores

Alcance del informe de mercado de gestión de datos de suscriptores

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2023 | 6.450 millones de dólares estadounidenses |

| Tamaño del mercado en 2031 | US$ 21,76 mil millones |

| CAGR global (2023 - 2031) | 16,4% |

| Datos históricos | 2021-2022 |

| Período de pronóstico | 2024-2031 |

| Segmentos cubiertos |

Por solución

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de gestión de datos de suscriptores: comprensión de su impacto en la dinámica empresarial

El mercado de gestión de datos de suscriptores está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de gestión de datos de suscriptores son:

- Sistemas Cisco, Inc.

- Desarrollo empresarial de Hewlett Packard LP

- Tecnologías Huawei Co., Ltd.

- Corporación Nokia

- Corporación Oracle

- Telefonaktiebolaget LM Ericsson

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de gestión de datos de suscriptores

Noticias y desarrollos recientes del mercado de gestión de datos de suscriptores

El mercado de gestión de datos de suscriptores se evalúa mediante la recopilación de datos cualitativos y cuantitativos a partir de investigaciones primarias y secundarias, que incluyen publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se enumeran algunos de los avances en el mercado de gestión de datos de suscriptores:

- Cisco anunció la finalización de la adquisición de Socio Labs, Inc. Con esto, la empresa pretende ampliar las ofertas de WebEx más allá de las reuniones, seminarios web y transmisiones web para incluir conferencias e impulsar el futuro de los eventos híbridos. Socio Labs es una plataforma de tecnología de eventos moderna que administra el ciclo de vida completo de conferencias virtuales, presenciales e híbridas de múltiples sesiones y múltiples pistas. (Fuente: Cisco, comunicado de prensa, julio de 2021)

- Cisco se asoció con Vodafone Idea Limited para simplificar y automatizar la red para admitir casos de uso 4G y 5G. También ofrece una experiencia de mejor calidad para sus clientes de consumo, minoristas y empresariales. Para ello, Vodafone Idea está implementando Ultra Packet Core de Cisco en toda la India para acelerar la transformación digital. (Fuente: Cisco, comunicado de prensa, junio de 2021)

Informe sobre el mercado de gestión de datos de suscriptores: cobertura y resultados

El informe “Tamaño y pronóstico del mercado de gestión de datos de suscriptores (2021-2031)” proporciona un análisis detallado del mercado que cubre las siguientes áreas:

- Tamaño del mercado de gestión de datos de suscriptores y pronóstico a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos bajo el alcance

- Tendencias del mercado de gestión de datos de suscriptores, así como dinámicas del mercado, como impulsores, restricciones y oportunidades clave

- Análisis detallado de las cinco fuerzas de Porter y PEST y FODA

- Análisis del mercado de gestión de datos de suscriptores que abarca las tendencias clave del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado

- Análisis del panorama de la industria y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes para el mercado de gestión de datos de suscriptores

- Perfiles detallados de empresas

Ankita es una profesional dinámica en investigación de mercados y consultoría con más de 8 años de experiencia en los sectores de tecnología, medios de comunicación, TIC, electrónica y semiconductores. Ha liderado y ejecutado con éxito más de 100 proyectos de consultoría e investigación para clientes globales como Microsoft, Oracle, NEC Corporation, SAP, KPMG y Expeditors International. Sus principales competencias incluyen la evaluación de mercado, el análisis de datos, la previsión, la formulación de estrategias, la inteligencia competitiva y la redacción de informes.

Ankita es experta en la gestión de ciclos completos de proyecto, desde el diseño de propuestas de preventa y las conversaciones con los clientes hasta la entrega de información práctica posventa. Es experta en la gestión de equipos multifuncionales, la estructuración de módulos de investigación complejos y la alineación de soluciones con los objetivos de negocio específicos del cliente. Sus excelentes habilidades de comunicación, liderazgo y presentación le han permitido obtener constantemente resultados orientados al valor en entornos de mercado dinámicos y en constante evolución.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias