Agricultural Robots Market Trends, Size & Forecast by 2034

Coverage: By Product and Application , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPTE100000491

- Category : Electronics and Semiconductor

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 10, 2026

2025 Market Size

US$ 19.01 Bn

Base year value

2034 Forecast

US$ 110.99 Bn

Projected by 2034

CAGR 2026-2034

21.66 %

Growth rate

Addressable Market

US$ 516.67 Bn

(2026-2034)

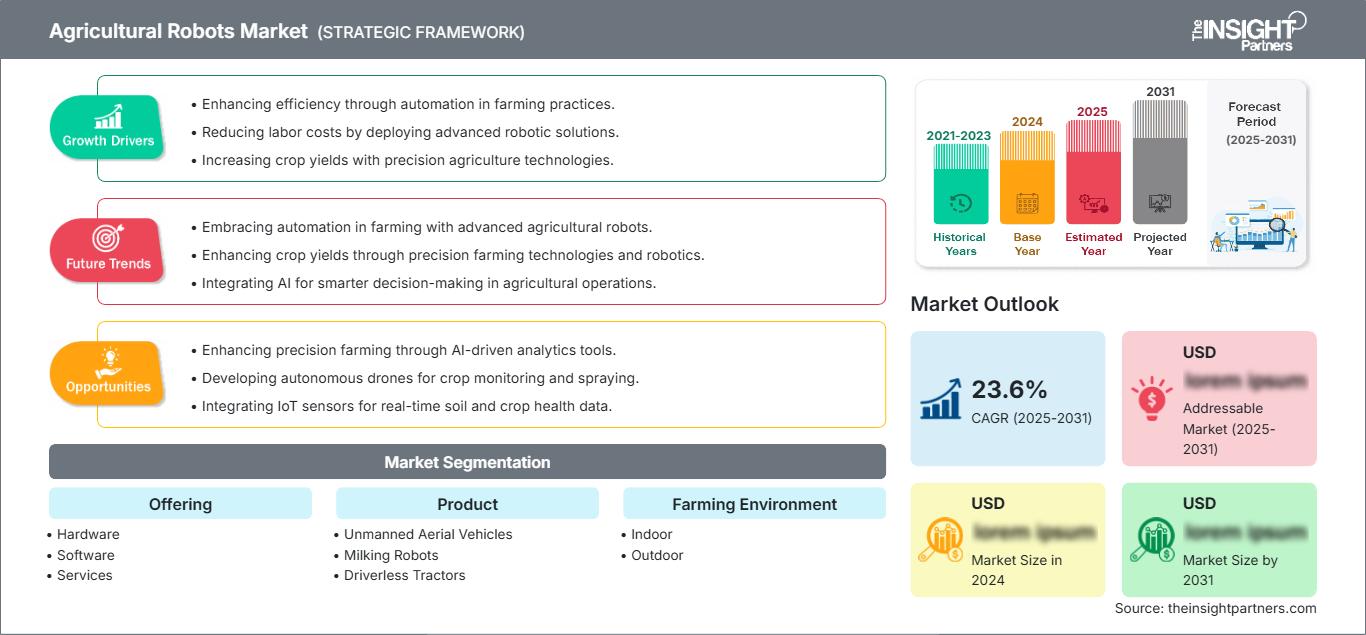

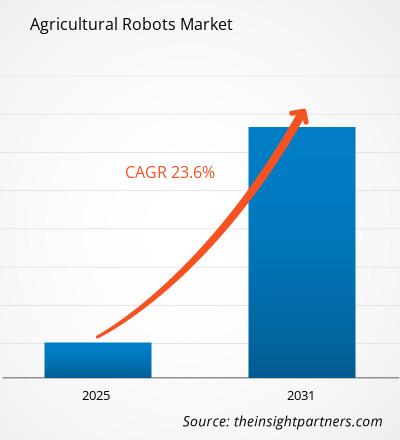

The Agricultural Robots Market was valued at US$ 19.01 Billion in 2025 and is projected to reach US$ 110.99 Billion by 2034, expanding at a CAGR of 21.66% from 2026 to 2034. Adoption is moving beyond pilot programs as farms deploy autonomous machines, aerial systems, milking units, harvesting robots, and decision software to improve productivity, input precision, and labor efficiency across field, dairy, and controlled-environment operations.

North America is expected to grow at an estimated 20.8%–22.1% CAGR, supported by large farm acreage, labor shortages, precision agriculture adoption, and strong OEM presence. The region benefits from autonomous tractor testing, drone-based scouting, robotic dairy systems, and input-reduction technologies that align with farm profitability, water stewardship, and sustainable crop protection priorities. The Agricultural Robots Market share in North America is strengthened by early technology adoption, advanced farm mechanization, and increasing investment in autonomous farming solutions.

Agricultural Robots Market Assessment and Insights

- North America: The region accounted for 31%–35% share in 2025 and is growing at a 20.8%–22.1% CAGR between 2026–2034, supported by high mechanization, precision agriculture spending, and autonomous field trials.

- US: The U.S. represented 77%–82% of North America in 2025 and is growing at a 21.0%–22.3% CAGR between 2026–2034, led by row-crop automation, dairy robotics, and drone services.

- Europe: Europe held 24%–28% share in 2025 and is growing at a 19.2%–20.6% CAGR between 2026–2034, led by Germany, France, the Netherlands, Spain, and Italy.

- Asia Pacific: Asia Pacific held 27%–31% share in 2025 and is growing at a 23.4%–24.8% CAGR between 2026–2034, led by China, Japan, South Korea, India, and Australia.

- Largest Segment: Hardware held 62%–67% market share in 2025 and is growing at a 20.1%–21.4% CAGR between 2026–2034 due to tractors, drones, milking robots, and harvest platforms.

- High Growth Segment: Unmanned Aerial Vehicles held 28%–33% market share in 2025 and is growing at a 24.5%–26.2% CAGR between 2026–2034 as spraying, scouting, and mapping scale.

- Key companies analyzed in detail: AGCO Corporation, AgEagle Aerial Systems Inc., BouMatic Robotics B.V., Trimble Inc., GEA Group Aktiengesellschaft, Ag Leader Technology, Deere & Company, Topcon Corporation, SZ DJI Technology Co., Ltd., Lely International N.V.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Agricultural Robots Market has shifted from isolated guidance systems to integrated autonomy that combines machine vision, GNSS positioning, AI, sensors, and cloud-based farm management. Production dynamics are changing because hardware platforms now require software updates, dealer service capability, data connectivity, and retrofit compatibility. Deere & Company’s second-generation autonomy kit and AGCO Corporation’s mixed-fleet PTx strategy show how the Agricultural Robots analysis is moving toward whole-cycle automation rather than single-task mechanization.

Forward demand will be shaped by water scarcity, declining rural labor availability, food-security investment, and regulation favoring lower chemical use. FAO-linked productivity concerns, national digital agriculture programs, and farm consolidation are widening the Agricultural Robots Market size in emerging economies. Asia Pacific is likely to add volume through drone spraying and compact robots, while Europe and North America will emphasize certified safety, autonomous tractors, and high-value specialty crop automation.

Agricultural Robots Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 19.01 Billion |

| Market Size by 2034 | US$ 110.99 Billion |

| Global CAGR (2026 - 2034) | 21.66% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Agricultural Robots Market Analysis

Demand is anchored in farm labor constraints, higher input prices, precision agronomy, and pressure to raise output from limited land and water. The Agricultural Robots Market forecast indicates that demand is strongest where repetitive field, dairy, monitoring, irrigation, and harvesting tasks can be automated with measurable payback. Robots reduce operator fatigue, improve timing of field operations, and support variable-rate decisions through sensors and analytics.

The value chain includes sensors, cameras, LiDAR, GNSS modules, electric drives, actuators, flight controllers, robotics software, farm management platforms, dealers, and service providers. Supply dynamics favor companies that combine hardware durability with agronomic data and field support. Component reliability, safety certification, battery performance, connectivity, and dealer training remain decisive because autonomous equipment must operate in dust, mud, heat, rain, and uneven terrain. The Agricultural Robots Market trends are increasingly shaped by advancements in autonomy, precision sensing, artificial intelligence, and integrated farm management capabilities.

Competitive structure includes machine players, drone makers, dairy equipment companies, and agricultural software providers. The main competitors in the category are Deere & Company, AGCO Corporation, Trimble Inc., Topcon Corporation, SZ DJI Technology Co., Ltd., GEA Group Aktiengesellschaft, Lely International N.V., BouMatic Robotics B.V., AgEagle Aerial Systems Inc., and Ag Leader Technology.

The investment pattern is geared toward the adoption of autonomous tractors, aerial crop spraying via drones, robotic milkers, artificial intelligence in weed detection, harvesting systems, and retrofitted automation kits for current machinery. John Deere mentioned more than one million acres using See & Spray by the year 2024, and DJI revealed more than 500,000 agricultural drones being utilized worldwide by 2025. These adoption numbers back up the findings provided in the Agricultural Robots Market Report.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Agricultural Robots Market: Strategic Insights

Regional Insights

North America Agricultural Robots

North America held 31%–35% share in 2025 and is growing at a 20.8%–22.1% CAGR between 2026–2034. The Agricultural Robots Market is supported by large farms, high equipment replacement value, autonomous tractor trials, drone-based scouting, and robotic dairy investments across row crops, orchards, specialty crops, and livestock operations.

The structural factors are related to a lack of farm labor, increased costs of inputs, familiarity with precision farming, and dealer networks that can provide services for connected farming. The market share of the Agricultural Robots in North America will be driven by such companies as Deere & Company, Trimble Inc., AGCO Corporation, Ag Leader Technology, and companies providing drone services.

U.S. Agricultural Robots Market

The U.S. represented 77%–82% of North America in 2025 and is growing at a 21.0%–22.3% CAGR between 2026–2034. The Agricultural Robots Market is concentrated in corn, soybean, cotton, dairy, orchards, vineyards, and specialty crops, where automation can improve field timing and reduce dependence on seasonal labor.

There is a high company presence in autonomous tractors, precision spraying, guidance, and farm management systems. Companies such as Deere & Company, AGCO Corporation, Trimble Inc., Topcon Corporation, and Ag Leader Technology help in field automation, while the companies supplying dairy and drones help increase application cases. The applications are inclined towards driverless tractors, UAV scouting, robotic milkings, harvest tracking, and automated irrigation.

Europe Agricultural Robots Market

Europe held 24%–28% share in 2025 and is growing at a 19.2%–20.6% CAGR between 2026–2034. Germany is the leading country because machinery manufacturing, precision farming adoption, and sustainability requirements support robotics in field operations, dairy automation, and crop monitoring. The Agricultural Robots Market is benefiting from these factors as farmers increasingly adopt automation technologies to improve efficiency, productivity, and resource utilization.

The UK market features farm labor restrictions, controlled environment horticulture, dairy upgrades, and experimentation with robot technology for weed control and harvesting. Germany enjoys advantages such as advanced engineering skills, dealership networks, and powerful machine fleets, which allow the adoption of GNSS guidance systems and autonomous implement solutions.

France, Italy, and Spain increase demand for products due to vineyards, orchards, dairy farming, vegetable cultivation, and irrigation. France focuses on efficient crop protection systems, Italy has high-value crops, and Spain offers stressed irrigation where automation of spraying and irrigation is beneficial.

APAC Agricultural Robots Market

Asia Pacific held 27%–31% share in 2025 and is growing at a 23.4%–24.8% CAGR between 2026–2034. China is the leading country, supported by drone scale, protected cultivation, mechanization policy, and large agri-tech manufacturing capacity. The Agricultural Robots Market is benefiting from these advantages as automation adoption accelerates across crop production, monitoring, spraying, and precision farming applications throughout the region.

For Japan and South Korea, the preferred technologies are smaller robots, automated rice growing, greenhouse solutions, and equipment to reduce labor for aging farmers. For India and Australia, technologies like spraying by drones, monitoring crops, autonomous guidance, and irrigation management make their contribution.

The industrial factors that influence the growth of agricultural robot trends include electronics supply chain, UAV production, government agricultural digitalization programs, and corporate farm consolidation.

Middle East & Africa Agricultural Robots Market

The Middle East & Africa is growing at a 18.6%–20.2% CAGR between 2026–2034. Saudi Arabia is the leading country, supported by food-security investment, protected farming, irrigation modernization, and automation for harsh-climate production systems. The Agricultural Robots Market is gaining momentum across the region as governments and agricultural operators invest in advanced technologies to enhance productivity, resource efficiency, and climate-resilient food production.

Both Saudi Arabia and the UAE use robots in their greenhouses, dairies, irrigation systems, and other high-value crops associated with controlled environment agriculture. Investments in energy and infrastructure facilitate the deployment of sensor technology, water management, and logistics capabilities.

Other nations in MEA, like South Africa, have adopted these robots slowly for their fruits and vineyards, livestock, and large farms. Their growth is contingent upon financing, dealer presence, water supply, training, and return on investment.

Segmentation Analysis

Offering

The Offering segment is growing at a 20.8%–22.2% CAGR between 2026–2034. Hardware leads because robots, drones, sensors, actuators, and charging systems represent the core capital purchase. Software is gaining strategic value through route planning, perception, analytics, and fleet management, while services are expanding around installation, training, maintenance, and performance-based operation. The Agricultural Robots Market continues to benefit from the growing integration of hardware, software, and service offerings that improve operational efficiency and automation outcomes.

- Hardware: Hardware will continue to be the largest source of income as autonomous tractors, UAVs, milking machines, harvesters, sensors, and robotic arms are built using durable designs for use on farms.

- Software: The demand for software is increasing because robots need algorithms for perceiving, task planning, coordinating fleets, analyzing data, maintaining regulatory compliance, and integration with farm management systems.

- Services: Services are critical because farmers require services like deployment assistance, operator training, calibration, maintenance, financing, upgrades, and monitoring services to maintain uptime.

Product

The Product segment is growing at a 22.1%–23.7% CAGR between 2026–2034. UAVs are scaling fastest because spraying, scouting, and mapping can be delivered without full farm mechanization. Milking robots provide steady dairy demand, driverless tractors address labor scarcity, and automated harvesting systems target high-value crops where manual labor costs are acute. The Agricultural Robots Market is being driven by the increasing adoption of these product categories as farms seek greater efficiency, precision, and operational scalability.

- Unmanned Aerial Vehicles: UAVs are strategic tools for crop scouting, variable-rate spraying, seeding, and mapping of the farm owing to their quick deployment and cost-effective input use.

- Milk Robot: The demand for milking robots remains robust among dairy farms requiring flexibility, cow tracking, scheduling of milking sessions, and better herd data collection.

- Driverless Tractors: Driverless tractors solve repetitive tasks like tillage, transportation, and spraying, where there is a lack of qualified personnel and timely scheduling.

- Automated Harvesting Solutions: Automated harvesting systems are developed to solve harvesting tasks involving fruits, vegetables, and specialty crops owing to labor-intensive processes and timely requirements.

Farming Environment

The Farming Environment segment is growing at a 21.0%–22.6% CAGR between 2026–2034. Outdoor farms account for broad-acreage-based deployment in scouting, spraying, tillage, and harvesting. Indoor environments are gaining attention because greenhouses, vertical farms, and controlled facilities can standardize lighting, navigation, and crop conditions, improving robotic reliability and repeatability. The Agricultural Robots Market is benefiting from expanding adoption across both outdoor and indoor farming environments as producers pursue higher productivity, consistency, and automation efficiency.

- Indoor: Indoor farming robots are used in greenhouses and vertical farms where controlled layouts support automated monitoring, pruning, harvesting, spraying, and logistics.

- Outdoor: Outdoor robots serve the largest operating base across field crops, orchards, vineyards, and livestock environments where scale creates strong productivity benefits.

Application

The Application segment is growing at a 21.5%–23.0% CAGR between 2026–2034. Field farming and harvest management dominate near-term deployment because robots directly improve timing, labor productivity, and input precision. Dairy and livestock management, irrigation, pruning, weather tracking, and inventory management expand the Agricultural Robots Market by connecting physical automation with operational decision-making.

- Harvest Management: Harvest management robots aid in scheduling, assessing crop maturity, minimizing crop loss, and labor scheduling during harvest seasons.

- Field Farming: Field farming incorporates the use of autonomous tractors, sprayers, weeders, drones, and sensors for efficient placement of inputs and operations in fields.

- Dairy and Livestock Management: Dairy and livestock robots help in activities such as milk collection, feeding, manure collection, and well-being tracking on dairy and livestock farms.

- Irrigation Management: Irrigation robots, together with sensor-based technologies, assist in monitoring soil moisture levels and watering plants in areas that suffer from drought.

- Pruning Management: Pruning robots are highly effective in orchards and vineyards where there is a need for pruning tasks to be done consistently and accurately.

- Weather Tracking and Monitoring: Weather tracking and monitoring tools enable the connection between sensors, drones, and analytics in decision-making for spraying, watering, disease prevention, and harvesting.

- Inventory Management: Inventory management helps in managing feeds, inputs, machinery, produce, and supplies in farm operations.

Opportunity Snapshot

| Application | Revenue Contribution | Trend Tag | Adoption Stage |

| Harvest Management | High | Yield Timing | Scaling |

| Field Farming | High | Autonomous Tillage | Scaling |

| Dairy and Livestock Management | High | Robotic Milking | Mature |

| Irrigation Management | Medium | Smart Water | Scaling |

| Pruning Management | Medium | Canopy Automation | Emerging |

| Weather Tracking and Monitoring | Medium | Microclimate Data | Scaling |

| Inventory Management | Low | Input Tracking | Emerging |

| Others | Low | Niche Tasks | Emerging |

Agricultural Robots Market Growth Drivers and Impact Analysis

Farm Labor Shortage and Seasonal Work Compression

The availability of labor is a key factor since crop planting, spraying, milk production, pruning, and harvesting have to be done within limited time frames. Millions of agricultural jobs requiring coverage each year have been stated by the American Farm Bureau Federation, and machine manufacturers are marketing autonomy as an answer to such a structure. The Agricultural Robots Market is thus profiting from this development since farmers require robotics to solve labor shortage issues and make operations more efficient. Such an effect on the market is best seen in large farms cultivating rows of crops, dairy farming, orchards, and vineyards, since a delay may lower yields or quality. In this case, robots enable operators to oversee many machines, work long hours, and direct the skilled labor towards strategic decisions.

Input Efficiency and Sustainable Crop Protection

Increasing prices for fertilizer, chemicals, fuel, and water drive farms toward using robots that distribute these resources only in necessary spots. For instance, Deere & Company announced that its See & Spray customers have had an average of 59% decrease in herbicide use per acre in 2024. It means that the technology brings not only economic benefits but also helps to be more environmentally friendly. All these advantages help the Agricultural Robots Market to prosper since farmers start implementing precision technology to reduce costs. UAV spraying, weed detection through artificial intelligence, autonomous watering, and sensor-based nutrients management help to economize these resources. Moreover, it assists in meeting sustainability requirements.

Digital Farm Platforms and Mixed-Fleet Autonomy

The rate of robotics adoption is increasing as farms begin to integrate machinery, implements, drones, sensors, and agro-economic data into unified platforms. This is important for mixed-fleet approaches, as the majority of farms have fleets of equipment manufactured by different companies and are not able to replace the entire fleet of equipment at one time. The PTx approach of AGCO Corporation and autonomy technologies of Trimble Inc. are focused on the process of retrofitting, office software, guidance, and task automation. The result is an increase in addressable markets that consist of old tractors, contractor fleets, and regional service providers.

Agricultural Robots Market Future Trends

Autonomy Moving from Single Tasks to Full Crop-Cycle Coverage

Future systems will move from autonomous point solutions toward crop-cycle orchestration across land preparation, planting, spraying, irrigation, harvesting, and transport. The shift will require perception systems, safety controls, route planning, task verification, and farm management integration. Deere & Company’s autonomous 9RX tractor and AGCO Corporation’s goal of expanding autonomy across crop operations illustrate this direction. The trend will change procurement from buying a robot for one task to subscribing to a coordinated automation stack. Farms will evaluate uptime, interoperability, dealer support, and data ownership as carefully as horsepower or payload, expanding the strategic Agricultural Robots Market beyond machine sales.

AI Vision Systems for Specialty Crop Automation

AI vision will become more important in orchards, vineyards, vegetables, berries, and greenhouse crops because these environments need plant-level recognition rather than broad-acre guidance alone. Cameras, LiDAR, multispectral sensors, and edge processors will help robots identify fruit maturity, canopy density, weed pressure, pest risk, and equipment hazards. This trend supports automated harvesting, pruning, targeted spraying, and yield forecasting where manual labor is expensive, and crop quality is sensitive. As datasets improve by crop and region, suppliers can localize models for different cultivars and field conditions. That will expand the size of opportunities in high-value specialty agriculture.

Agricultural Robots Market Opportunities

Robotics-as-a-Service for Small and Mid-Sized Farms

Robotics-as-a-service can unlock adoption where farmers cannot justify full ownership of drones, harvest robots, or autonomous tractors. Service providers can spread equipment cost across multiple farms, offer trained operators, and provide performance-based pricing for spraying, scouting, weeding, mowing, and harvest support. This model is especially attractive in fragmented markets, specialty crops, and developing regions where capital access is limited. OEMs, dealers, and agri-service firms can build recurring revenue through maintenance, software, insurance, and data services. The opportunity is investment-oriented because it converts high upfront robot cost into variable operating expense aligned with farm seasons and acreage.

Water-Smart Robotics in Climate-Stressed Agriculture

Water scarcity creates a clear opportunity for robots that combine sensing, irrigation control, crop monitoring, and targeted application. Farms in arid regions need tools that identify moisture stress, leaks, uneven application, and crop variability before yield losses become visible. Autonomous ground robots, UAVs, and sensor networks can support irrigation scheduling, fertigation precision, and disease monitoring with fewer field passes. Suppliers should prioritize rugged sensors, solar-compatible charging, local agronomy partnerships, and dashboards that translate data into simple actions. This opportunity is distinct because adoption is driven by resource security and climate resilience rather than labor savings alone.

Recent Developments

- July 2026: SZ DJI Technology Co., Ltd. — DJI Agriculture launched the Agras T55 and Agras T100 Dual Battery Spraying System globally, expanding spraying, spreading, and lifting capabilities for orchards, small plots, and large-field operations. DJI stated that more than 600,000 agricultural drones were operating worldwide across 300 crop types in more than 100 countries.

- September 2025: AGCO Corporation — AGCO Tech Day 2025 showcased PTx FarmENGAGE, PTx Trimble OutRun autonomous tillage and fertilization, and AI-based weed control. The company highlighted mixed-fleet compatibility and its ambition to deliver autonomous solutions across the crop cycle by 2030, reinforcing retrofit autonomy as a commercial pathway.

- January 2025: Deere & Company — John Deere revealed second-generation autonomous machines at CES 2025, including an autonomous 9RX tractor for large-scale agriculture and an autonomous 5ML orchard tractor for air blast spraying. The autonomy kit uses computer vision, AI, cameras, and LiDAR to address labor shortages and improve machine operation.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends