Atherectomy Devices Market Size, Growth & Trends by 2034

Coverage: By Product (Rotational Atherectomy Systems, Directional Atherectomy Systems, Orbital Atherectomy Systems, Photo-Ablative (Laser) Atherectomy Systems, Support Devices); Application (Cardiovascular, Peripheral Vascular, Neurovascular); End User (Hospitals, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPHE100001272

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 18, 2026

2025 Market Size

US$ 1.08 Bn

Base year value

2034 Forecast

US$ 1.96 Bn

Projected by 2034

CAGR 2026-2034

6.85 %

Growth rate

Addressable Market

US$ 13.74 Bn

(2026-2034)

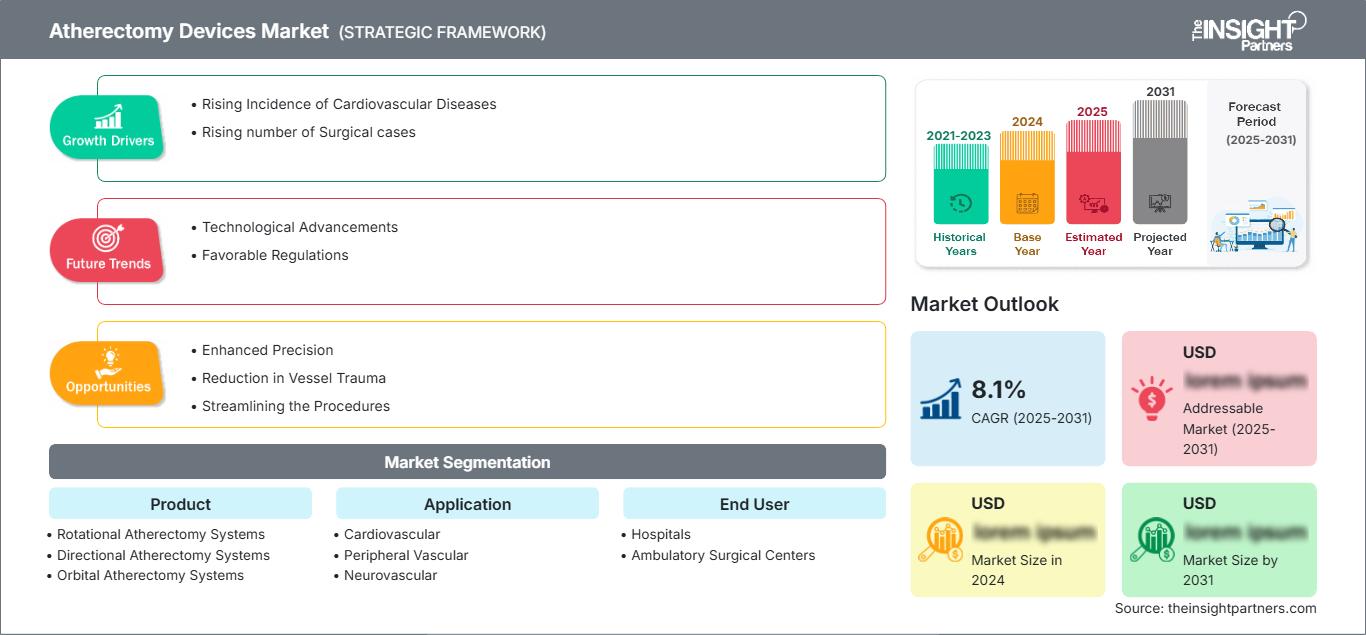

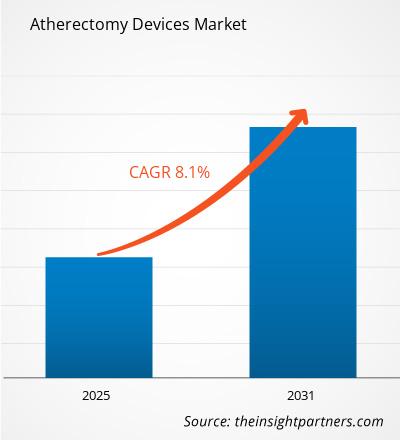

The global Atherectomy Devices Market size is projected to reach US$ 1.96 billion by 2034 from US$ 1.08 billion in 2025. The market is anticipated to register a CAGR of 6.85% during the forecast period 2026–2034

Key market dynamics include a rising global prevalence of cardiovascular diseases, an aging population more prone to arterial calcification, and a significant shift toward minimally invasive endovascular procedures. Additionally, the market is expected to benefit from technological advancements in plaque modification, expansion of specialized vascular centers, and the growing clinical adoption of combination therapies like atherectomy followed by drug-coated balloon (DCB) applications.

Atherectomy Devices Market Analysis

The atherectomy devices market analysis shows a transition toward high-precision plaque debulking as clinicians seek to improve long-term vessel patency. The market is diversifying from traditional inpatient hospital settings into high-growth outpatient environments such as office-based labs (OBLs). Strategic opportunities are emerging in the management of complex, heavily calcified lesions where traditional balloon angioplasty often fails. The analysis also notes that market expansion depends on the integration of advanced intravascular imaging and the availability of robust clinical data to support reimbursement. Competitive differentiation now hinges on catheter profile reduction and the ability of devices to minimize distal embolization through active aspiration or specialized crown designs.

Atherectomy Devices Market Overview

Vascular intervention tools have advanced from niche surgical instruments to mainstream endovascular solutions. The atherectomy devices include specialized systems designed for rotational, orbital, and directional plaque removal. Both global medical technology leaders and specialized vascular startups compete in this market, utilizing various energy and mechanical sources to clear arterial blockages. Growing demand for outpatient-friendly procedures among health-conscious patients in North America and Europe has increased the popularity of atherectomy as an alternative to open bypass surgery. North America leads in revenue due to its established reimbursement framework and high procedural volume, while Asia-Pacific is advancing in technical adoption and infrastructure investment. The US market is the most developed, driven by a high incidence of peripheral artery disease (PAD) and a mature network of ambulatory surgical centers. Competition among brands is fueling the inclusion of smart technologies like real-time imaging and AI-guided navigation.

Market Assessment and Insights

- Global market for Atherectomy Devices was valued at US$ 1.08 Billion in 2025

- Annual market size is expected to reach US$ 1.96 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 13.74 Billion

- Market is anticipated to register a CAGR of 6.85% during the forecast period

- The United States represents a key market, supported by Rising Incidence of Cardiovascular Diseases, Rising number of Surgical cases, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Enhanced Precision, Reduction in Vessel Trauma, Streamlining the Procedures are expected to influence market dynamics and addressable market

- Report profiles industry participants, including B. Braun Melsungen AG, Koninklijke Philips N.V., Cardinal Health, Medtronic, TERUMO CORPORATION, C. R. Bard, Inc., Minnetronix, Inc., Avinger, Straub Medical AG., Biomerics, Abbott, RA Medical Systems, Boston Scientific Corporation, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Atherectomy Devices Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Atherectomy Devices Market Drivers and Opportunities

Market Drivers:

- Growing Preference for Minimally Invasive Procedures: Endovascular techniques offer shorter hospital stays and faster recovery times compared to traditional surgery, driving higher patient and provider acceptance.

- Rising Prevalence of Peripheral and Coronary Diseases: Global increases in diabetes and obesity rates have led to a surge in arterial blockages, particularly in the lower extremities, necessitating advanced debulking tools.

- Advancements in Image-Guided Technology: The integration of intravascular ultrasound (IVUS) and optical coherence tomography (OCT) with atherectomy systems allows for more precise treatment and better safety outcomes.

Market Opportunities:

- Expansion into Neurovascular Interventions: There is significant potential for adapting atherectomy technology to treat carotid artery stenosis and other neurovascular conditions.

- Growth in Ambulatory Surgical Centers (ASCs): The shift of vascular procedures to outpatient settings creates a demand for efficient, high-performance devices tailored for same-day discharge models.

- Emerging Market Penetration in Asia-Pacific: Increasing healthcare expenditure and a growing burden of cardiovascular disease in China and India provide a massive opportunity for global device manufacturers.

Atherectomy Devices Market Report Segmentation Analysis

The Atherectomy Devices Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product:

- Rotational Atherectomy Systems: Primarily used for heavily calcified coronary and peripheral lesions, utilizing high-speed burrs to pulverize plaque.

- Directional Atherectomy Systems: A leading segment favored for its ability to physically excise and remove plaque, providing a wide lumen for subsequent treatment.

- Orbital Atherectomy Systems: Known for a unique mechanism that allows for continuous blood flow during the procedure, reducing the risk of thermal injury.

- Photo-Ablative Atherectomy Systems: Employ laser energy to vaporize plaque and thrombus, particularly effective in treating in-stent restenosis.

- Support Devices: Includes essential accessories such as catheters, guidewires, and distal protection filters that ensure procedural safety and success.

By Application:

- Cardiovascular: Focuses on treating coronary artery disease (CAD) by preparing calcified vessels for stent placement.

- Peripheral Vascular: The largest application segment, driven by the high volume of atherectomy procedures performed for peripheral artery disease (PAD) in the lower limbs.

- Neurovascular: An emerging application area targeting plaque removal in the carotid arteries to reduce stroke risk.

By End User:

- Hospitals: Remain the primary site for complex and high-risk vascular interventions due to the presence of comprehensive emergency support and multidisciplinary teams.

- Ambulatory Surgical Centers (ASCs): The fastest-growing end-user segment, benefiting from cost-effectiveness and the global trend toward outpatient cardiovascular care.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Atherectomy Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1.08 Billion |

| Market Size by 2034 | US$ 1.96 Billion |

| Global CAGR (2026 - 2034) | 6.85% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Atherectomy Devices Market Players Density: Understanding Its Impact on Business Dynamics

The Atherectomy Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Atherectomy Devices Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years due to a rapidly aging population and the modernization of healthcare facilities. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for medical device manufacturers as they adopt international treatment guidelines.

The atherectomy devices market is undergoing a significant transformation, moving from a niche intervention to a global standard for complex plaque management. Growth is driven by the rising prevalence of calcified lesions, a surge in leave-nothing-behind clinical strategies, and the expansion of the outpatient vascular sector. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the largest share, driven by high procedural volumes and early adoption of new technologies.

- Key Drivers:

- Favorable reimbursement frameworks (Medicare/Medicaid) and established Office-Based Labs (OBLs).

- Presence of major market leaders like Boston Scientific, Abbott, and Medtronic.

- High incidence of peripheral artery disease (PAD) affecting over 6.5 million Americans.

- Trends: A rapid migration of procedures from inpatient hospitals to ambulatory surgical centers (ASCs) and the successful adoption of real-time imaging (IVUS/OCT) to improve procedural precision.

Europe

- Market Share: A substantial segment anchored by advanced healthcare systems in Germany, France, and the UK.

- Key Drivers:

- High domestic burden of coronary and peripheral artery diseases.

- Strict regulatory standards (MDR) ensuring high device safety and long-term efficacy.

- Robust government support for minimally invasive cardiovascular research.

- Trends: A strategic shift toward combination therapy, using atherectomy to prep vessels for drug-coated balloons (DCB). There is also an increasing focus on laser atherectomy for treating in-stent restenosis.

Asia-Pacific

- Market Share: The fastest-growing region, with China and Japan acting as the primary growth for the continent.

- Key Drivers:

- Massive consumer base seeking premium, minimally invasive cardiovascular interventions.

- Government-supported infrastructure initiatives focused on smart healthcare and modernizing cath labs.

- Rapid urbanization and rising disposable incomes are leading to a preference for high-end westernized medical tech.

- Trends: Heavy reliance on clinical education and B2B contracts for hospital-based training. Japan is progressing rapidly in the adoption of orbital and laser systems due to recent regulatory clearances.

South and Central America

- Market Share: Emerging market with a growing specialized vascular sector in countries like Brazil and Chile.

- Key Drivers:

- Increasing awareness of the nutritional and lifestyle links to coronary artery disease.

- Modernization of private clinics into commercial-grade outpatient centers to supply urban hubs.

- Rising interest in Western medical standards among high-income segments.

- Trends: Growth of center of excellence models and the introduction of rotational atherectomy systems to differentiate from standard balloon angioplasty.

Middle East and Africa

- Market Share: Developing market with deep clinical roots in traditional surgery, transitioning toward formalized endovascular production.

- Key Drivers:

- Traditional prevalence of diabetes-related vascular complications in regional populations.

- Strategic investments in smart hospitals to improve local health security and reduce medical tourism.

- High demand for durable, efficient medical technologies in rapidly expanding urban centers.

- Trends: Implementation of modern imaging and navigation technologies to formalize the informal vascular market, coupled with a focus on high-performance catheters for the geriatric segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Medtronic, Boston Scientific, and Abbott. Regional innovators and specialized players like Avinger, AngioDynamics, and Cardiovascular Systems (now part of Abbott) also contribute to a dynamic and technologically evolving market landscape.

This competitive environment pushes vendors to differentiate through:

- Clinical Evidence Generation: Leading companies invest heavily in large-scale clinical trials to demonstrate the superiority of atherectomy over balloon angioplasty in complex lesions.

- Procedural Integration: Vendors are offering comprehensive vascular portfolios that include debulking devices, embolic protection, and drug-delivery platforms.

- Technological Innovation: New processing technologies, such as miniaturized cutters and improved laser modules, help create high-performance catheters that can navigate tortuous anatomy.

Opportunities and Strategic Moves

- Partner with Ambulatory Surgical Centers (ASCs): Tap into the surging demand for cost-effective, same-day discharge models in the North American and European markets.

- Incorporate AI and Robotics: Integrate robotic-assisted navigation and AI-driven imaging to appeal to modern clinicians seeking to standardize outcomes and reduce operator fatigue.

Major Companies operating in the Atherectomy Devices Market are:

- B. Braun Melsungen AG

- Koninklijke Philips N.V.

- Cardinal Health

- Medtronic

- TERUMO CORPORATION

- C. R. Bard, Inc.

- Minnetronix, Inc.

- Avinger

- Straub Medical AG.

- Biomerics

- Abbott

- RA Medical Systems

- Boston Scientific Corporation

Disclaimer: The companies listed above are not ranked in any particular order.

Atherectomy Devices Market News and Recent Developments

- In January 2025, the FireRaptor® Integrated Coronary Rotational Atherectomy System, including the FireRaptor® Coronary Rotational Atherectomy Console, the FireRaptor® Coronary Atherectomy Catheter, and the FireRaptor® Coronary Atherectomy Guidewire, developed by MicroPort® RotaPace, had officially received market approval in China. The approval of FireRaptor® represents a significant milestone for MicroPort® in advancing the treatment of resistant coronary lesions. Combined with the Scoring Balloon and the Coronary Shockwave Catheter System, FireRaptor® provides interventional cardiologists with a comprehensive solution for addressing complex coronary lesions.

- In August 2024, Avinger, Inc. announced the full commercial launch of the Pantheris LV image-guided directional atherectomy system. With the initiation of full commercial launch, all current and prospective accounts can now order the Pantheris LV device, a line extension of the first and only image-guided atherectomy device for the treatment of peripheral artery disease (PAD).

Atherectomy Devices Market Report Coverage and Deliverables

The Atherectomy Devices Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Atherectomy Devices Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Atherectomy Devices Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Atherectomy Devices Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Atherectomy Devices Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends