Data Center Construction Market Growth, Demand & Size by 2034

Coverage: By Types of Construction (General Construction, Electrical Design, and Mechanical Design); By Tier Standards (Tier 1 and Tier 2, Tier 3, and Tier 4); and By Industry Verticals (BFSI, Government, Education, Manufacturing, Retail, Transportation, Media & Entertainment, Others), and Geography

- Status : Data Released

- Report Code : TIPTE100000432

- Category : Technology, Media and Telecommunications

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 18, 2026

2025 Market Size

US$ 260.11 Bn

Base year value

2034 Forecast

US$ 520.14 Bn

Projected by 2034

CAGR 2026-2034

8.81 %

Growth rate

Addressable Market

US$ 3,656.07 Bn

(2026-2034)

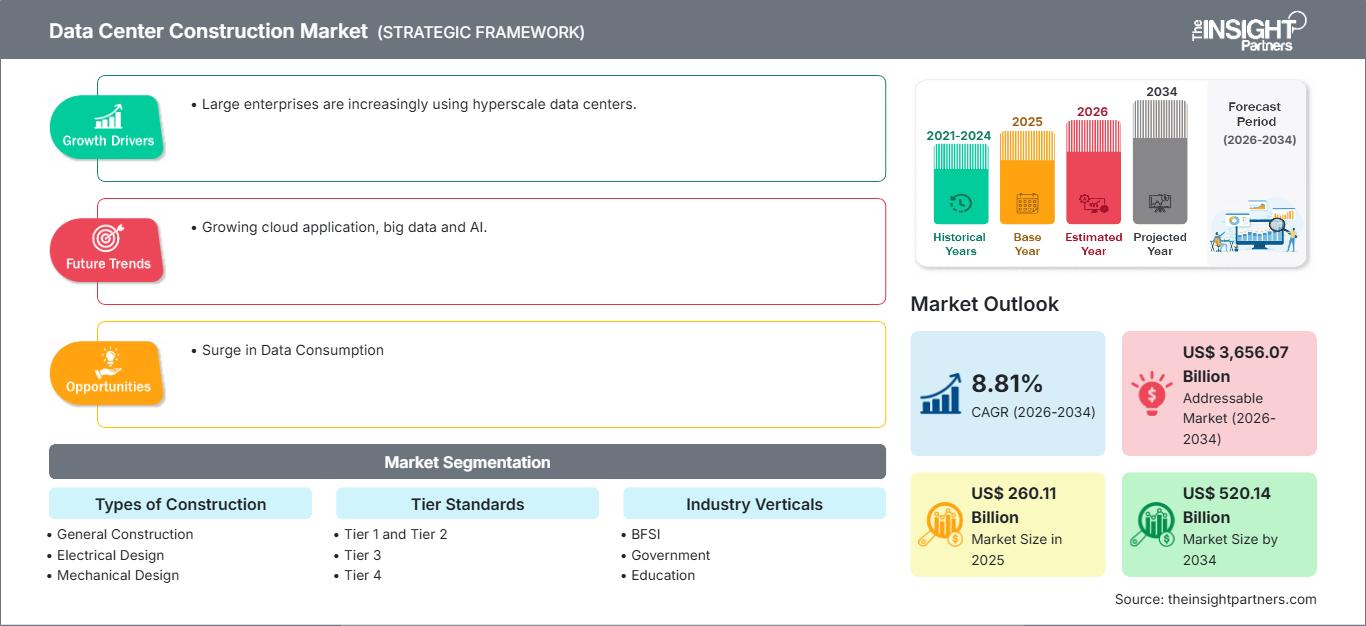

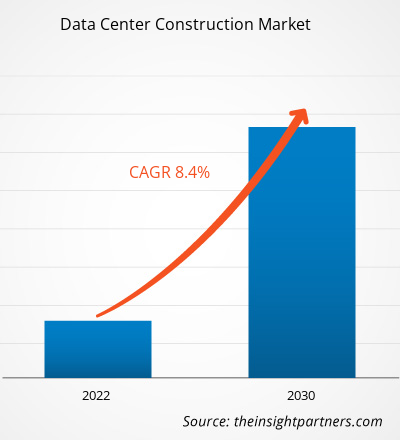

The global Data Center Construction Market size is projected to reach US$ 520.14 billion by 2034 from US$ 260.11 billion in 2025. The market is anticipated to register a CAGR of 8.81% during the forecast period 2026–2034

Key market dynamics include a global surge in generative AI workloads, an accelerating shift toward hyperscale cloud architectures, and an urgent focus on sustainable, energy-efficient building practices. Additionally, the market is expected to benefit from the deployment of 5G networks, the rising demand for edge computing facilities to reduce latency, and the integration of advanced liquid cooling technologies to manage the high thermal loads of modern high-performance computing (HPC) environments.

Data Center Construction Market Analysis

The data center construction market analysis indicates a fundamental shift toward high-density, AI-ready infrastructure as enterprises move beyond traditional storage to complex real-time processing. Procurement trends suggest a bifurcated market: massive multi-gigawatt hyperscale campuses driven by global tech giants and a rapidly expanding network of modular edge data centers designed for localized data sovereignty. Strategic opportunities are emerging in the integration of on-site renewable energy and small modular reactors (SMRs), as power availability replaces land as the primary constraint for site selection. The analysis also highlights that successful market entry now depends on securing long-lead equipment, such as transformers and custom cooling loops, well in advance of groundbreaking. Competitive differentiation is increasingly defined by the ability to offer speed-to-market through prefabricated modular construction and standardized design-build methodologies that mitigate the global shortage of specialized labor.

Data Center Construction Market Overview

Data center construction is evolving from a localized utility to a global backbone of the digital economy. While traditionally concentrated in established FLAP-D hubs (Frankfurt, London, Amsterdam, Paris, Dublin) and Northern Virginia, the market is expanding into secondary and tertiary cities to satisfy regional data residency laws and lower operational costs. This expansion encompasses diverse project types, from massive greenfield developments to the retrofitting of existing facilities with high-density cooling. Both specialized construction firms and large-scale industrial contractors are pivoting to meet the unique mechanical and electrical demands of modern facilities. As digital transformation reaches maturity in North America and Europe, the focus is shifting toward Asia-Pacific region, which is emerging as the new engine for incremental capacity growth. For instance, the market in the US remains the most mature and influential landscape for data center development, characterized by a transition from traditional metropolitan hubs to expansive rural campuses. Development is increasingly focused on regions offering abundant renewable energy and tax incentives. Infrastructure strategies emphasize sustainability and the rapid scaling of hyperscale capacity to support domestic AI innovation.

Market Assessment and Insights

- Global market for Data Center Construction was valued at US$ 260.11 Billion in 2025

- Annual market size is expected to reach US$ 520.14 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 3,656.07 Billion

- Market is anticipated to register a CAGR of 8.81% during the forecast period

- The United States represents a key market, supported by Large enterprises are increasingly using hyperscale data centers., as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Surge in Data Consumption are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Ascenty, Acer Inc., Cisco Systems, Inc., Dell Inc., Fujitsu, Hewlett Packard Enterprise Development LP, Huawei Technologies Co., Ltd., IBM, Lenovo, Oracle, Inspur, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Data Center Construction Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Data Center Construction Market Drivers and Opportunities

Market Drivers:

- Surge in AI and High-Performance Computing (HPC): The explosion of generative AI models requires specialized facilities capable of supporting significantly higher power densities per rack. This demand is forcing a complete redesign of electrical and cooling architectures, driving a new wave of high-value construction projects.

- Rapid Migration to Hyperscale Cloud Services: As organizations transition their core workloads to the cloud, providers like AWS, Microsoft, and Google are investing billions in massive data center campuses. This continuous capital expenditure on giga-sites ensures a steady pipeline for industrial-scale construction firms.

- Mandatory Focus on Sustainability and Green Building: Increasing regulatory pressure and corporate ESG goals are driving the adoption of Green Data Centers. This includes the use of low-carbon building materials, advanced water-recycling systems, and LEED-certified designs to minimize environmental footprints.

Market Opportunities:

- Expansion of Edge Computing Infrastructure: The rollout of 5G and IoT applications creates a need for smaller, distributed data centers closer to end-users. Construction firms specializing in rapid-deployment modular units have significant opportunities to capture the growing decentralized market.

- Retrofitting and Modernization of Legacy Facilities: Many older data centers lack the cooling and power infrastructure to support modern server hardware. Strategic opportunities exist in upgrading these facilities with liquid-to-chip cooling and reinforced electrical paths to extend their operational lifespan.

- Growth in Sovereign Data Centers: Strengthening data privacy laws globally is prompting governments and enterprises to build localized facilities. Partnering with regional developers to build sovereign clouds offers a high-margin opportunity in markets with strict data residency requirements.

Data Center Construction Market Report Segmentation Analysis

The Data Center Construction Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Types of Construction:

- General Construction: Focuses on the physical shell, including site preparation, building structures, and specialized flooring. This segment is increasingly adopting modular and prefabricated components to shorten project timelines.

- Electrical Design: A critical high-value segment covering power distribution, backup generators, and UPS systems. The shift toward higher density and redundancy makes this the most capital-intensive part of modern construction.

- Mechanical Design: Primarily concerns HVAC and cooling systems. With the rise of AI, this segment is transitioning from traditional air cooling to advanced liquid-based and immersion cooling technologies.

By Tier Standards:

- Tier 1 and Tier 2: Typically used by smaller enterprises or for non-mission-critical applications. These facilities offer basic redundancy and are often part of smaller regional edge deployments.

- Tier 3: The global standard for colocation and enterprise data centers. It offers N+1 redundancy, allowing for maintenance without downtime, making it the most dominant segment in terms of volume.

- Tier 4: The most advanced fault-tolerant facilities are designed for zero downtime. These are increasingly sought after by financial institutions and hyperscale providers where service interruptions carry severe consequences.

By Industry Verticals:

- BFSI: A leading segment requiring high-tier facilities to manage sensitive financial data and ensure 24/7 service availability.

- Government & Education: Focused on data sovereignty and secure public-sector infrastructure, often involving large-scale sovereign cloud projects.

- Manufacturing & Retail: Driven by the adoption of Industry 4.0 and e-commerce, requiring localized processing to manage supply chain and customer data.

- Media & Entertainment: Requires massive storage and high-bandwidth capabilities for content delivery and real-time rendering.

- Others: Includes healthcare, energy, and transportation, all of which are undergoing digital transformation.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Data Center Construction Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 260.11 Billion |

| Market Size by 2034 | US$ 520.14 Billion |

| Global CAGR (2026 - 2034) | 8.81% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Types of Construction

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Data Center Construction Market Players Density: Understanding Its Impact on Business Dynamics

The Data Center Construction Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Data Center Construction Market Share Analysis by Geography

North America currently holds the largest share of the global market, anchored by the presence of major hyperscale providers and a mature digital ecosystem. However, Asia-Pacific region is expected to grow fastest in the coming years due to rapid urbanization and the proliferation of digital services in India and Southeast Asia. Emerging markets in South & Central America, the Middle East, and Africa also present significant untapped opportunities for developers as they formalize their digital infrastructure.

The data center construction market is undergoing a significant transformation, moving from centralized metropolitan hubs to a diverse global network. The AI revolution, sovereign data mandates, and the pursuit of carbon-neutral infrastructure drive growth. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the dominant global position (approx. 38-41% share), led by the United States.

- Key Drivers:

- Massive capital infusion from hyperscalers (AWS, Google, Meta) for AI-focused campuses.

- High availability of land and fiber in secondary markets like Ohio and Texas.

- Early adoption of liquid cooling and modular construction techniques.

- Trends: A shift toward land banking, where developers secure large tracts of land with pre-approved power connections to bypass utility queue delays.

Europe

- Market Share: Second-largest market, characterized by strict energy efficiency standards and mature regulatory frameworks.

- Key Drivers:

- Stringent EU regulations (GDPR) are driving demand for local data residency.

- Increasing focus on heat reuse projects where data center waste heat warms local communities.

- Transition from traditional FLAP-D hubs to secondary markets like Norway and Spain.

- Trends: Rapid implementation of the Energy Efficiency Directive, forcing operators to report on sustainability metrics and modernize older infrastructure.

Asia-Pacific

- Market Share: The fastest-growing region, with major activity centers in China, India, and Southeast Asia.

- Key Drivers:

- Rapid digital adoption and internet penetration among massive populations.

- Government initiatives for data localization and smart city developments.

- Favorable tax incentives for digital infrastructure in countries like Malaysia and Indonesia.

- Trends: Heavy investment in subsea cables to improve regional connectivity and the emergence of India as a global hub for hyperscale and AI capacity.

South and Central America

- Market Share: An emerging market with high growth potential in Brazil, Chile, and Argentina.

- Key Drivers:

- The growing presence of global cloud providers is expanding their Latin American footprint.

- Rising demand for low-latency services for the regional fintech and e-commerce sectors.

- Investments in renewable energy sources like wind and solar to power facilities.

- Trends: Development of large-scale colocation facilities in Brazil to serve as the gateway for the continent's digital traffic.

Middle East and Africa

- Market Share: Developing market focused on digital sovereignty and economic diversification.

- Key Drivers:

- Vision programs (e.g., Saudi Vision 2030) are aiming to modernize national infrastructure.

- Strategic geographical position as a bridge between Europe and Asia.

- Investments in smart agriculture and oil/gas digital twins.

- Trends: Construction of high-efficiency facilities in arid climates using innovative cooling solutions that minimize water consumption.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as AECOM, Skanska, Jacobs Solutions Inc., and Schneider Electric. These giants are joined by specialized niche players and regional experts such as HITT Contracting, DPR Construction, and Gilbane Building Company, as well as global operators who manage their own construction, like Equinix and Digital Realty.

This competitive environment pushes vendors to differentiate through:

- Speed-to-Market: Utilizing modular and prefabricated designs to cut construction times by up to 30%, a critical factor for hyperscalers racing to deploy AI capacity.

- Vertical Integration: Companies are increasingly managing the entire lifecycle, from site selection and zoning to the commissioning of complex liquid cooling loops.

- Sustainability Certifications: Differentiating through Net Zero construction goals, incorporating timber framing, and high-efficiency electrical designs that appeal to ESG-conscious tenants.

- Supply Chain Resilience: Establishing long-term partnerships with equipment vendors to ensure a steady supply of mission-critical components like backup generators and transformers.

Opportunities and Strategic Moves

- Invest in High-Density Cooling Technologies: Partner with liquid cooling manufacturers to offer turnkey solutions for the surging AI and HPC market segments.

- Adopt Digital Twin and AI in Construction: Utilize BIM (Building Information Modeling) and AI-driven project management to reduce waste, predict maintenance needs, and optimize energy usage from day one.

Major Companies operating in the Data Center Construction Market are:

- Ascenty

- Acer Inc.

- Cisco Systems, Inc.

- Dell Inc.

- Fujitsu

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- IBM

- Lenovo

- Oracle

- Inspur

Disclaimer: The companies listed above are not ranked in any particular order.

Data Center Construction Market News and Recent Developments

- In December 2025, the Canada Pension Plan Investment Board (CPP Investments) and Equinix, Inc. entered into a joint agreement to purchase atNorth, a leading Nordic provider specializing in high-density colocation and built-to-suit Data Center Construction. The acquisition from Partners Group allowed the firms to expand their presence in the high-growth Nordic region significantly.

- In October 2025, Adani Enterprises, through its joint venture AdaniConneX, and Google announced a landmark partnership to develop India's largest AI data center campus in Visakhapatnam, Andhra Pradesh. This strategic collaboration integrated large-scale Data Center Construction with new green energy infrastructure to support the region's burgeoning demand for sustainable, high-performance computing.

Data Center Construction Market Report Coverage and Deliverables

The Data Center Construction Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Data Center Construction Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Data Center Construction Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Data Center Construction Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Data Center Construction Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends