Healthcare CRM Market Analysis by Size, Share & Growth 2030

Coverage: By Deployment Mode (Cloud Based and On-Premise), Product Type (Operational CRM, Analytical CRM, and Collaborative CRM), Application (Relationship Management, Case Management, Case Coordination, Community Outreach, and Others), End User (Providers, Payers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

- Status : Published

- Report Code : TIPHE100000841

- Category : Technology, Media and Telecommunications

- No. of Pages : 255

- Available Report Formats :

- Last update date : June 12, 2024

2022 Market Size

US$ 5.75 Bn

Base year value

2030 Forecast

US$ 12.95 Bn

Projected by 2030

CAGR 2023-2030

10.7 %

Growth rate

Addressable Market

US$ 74.67 Bn

(2023-2030)

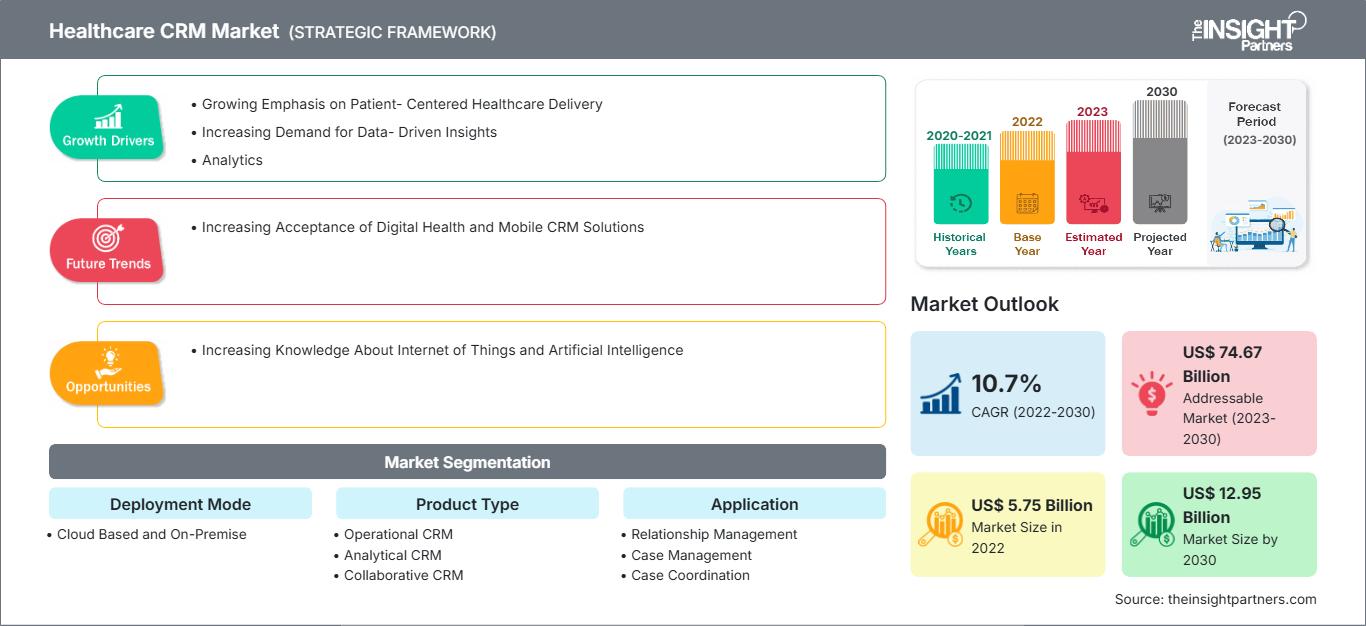

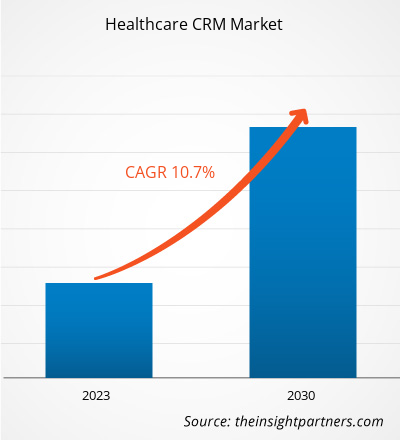

[Research Report] The healthcare CRM market value is projected to grow from US$ 5,750.95 million in 2022 to US$ 12,947.15 million by 2030; with a CAGR of 10.7% from 2022 to 2030.

Market Insights and Analyst View:

Healthcare CRM is an industry-specific system that assists medical service providers in storing and managing patient information, improving service and engagement, improving patient acquisition strategy, and automating marketing and sales operations while adhering to healthcare security standards. Key factors driving the healthcare CRM market growth include the growing emphasis on patient-centered healthcare delivery and increasing demand for data-driven insights, analytics, and population health management. However, the lack of data security and concerns related to patient information privacy hinder the healthcare CRM market growth.

Growth Drivers and Restraints:

A patient-centric approach in healthcare systems can establish a partnership among patients, their families, and healthcare practitioners to align decisions in accordance with patients’ needs, preferences, and demands. It also includes the delivery of specific education and support to patients to make certain decisions and participate in their care.

Increased engagement with all stakeholders (providers, patients, and others) reduces overall expenses. Additionally, improved knowledge and understanding of health, well-being, and healthcare choices among patients lead to enhanced care and reduced levels of illness. This improved knowledge can facilitate care after discharge, hospital visits, reduced readmissions, and secondary consults. By engaging and collaborating with patients in decision-making, health providers can make more suitable decisions regarding a patient’s health. There is also an increased competitive advantage as more hospitals compete for patients based on both qualities of care and cost. Better quality of life for patients leads to an increase in the satisfaction of both doctor and patient.

Market Research Highlights

- North America dominated the market with 42.9% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 11.3% over the forecast period.

- United States market is projected to grow at a CAGR of 11% over the forecast period.

- By Deployment Mode, the Cloud Based segment accounted for the largest market share of 59.9% in 2022.

- By Product Type, the Operational CRM segment is anticipated to witness the fastest growth, registering a CAGR of 11.2% over the forecast period

- By Application, the Relationship Management segment accounted for the largest market share of 37.7% in 2022.

- By Case Management, the Clinical trials Relationship Management segment is anticipated to witness the fastest growth, registering a CAGR of 11.4% over the forecast period

- By Community Outreach, the Services Outreach/Promotion segment accounted for the largest market share of 63% in 2022.

- By Case Coordination, the Patient information Management segment is anticipated to witness the fastest growth, registering a CAGR of 10.8% over the forecast period

- By End User, the Providers segment accounted for the largest market share of 45.8% in 2022.

- The report profiles key industry players such as International Business Machines Corp, Microsoft Corp, Oracle Corp, SAP SE, Veeva Systems Inc, Pegasystems Inc, IQVIA Holdings Inc, Sage Group Plc, Salesforce Inc, Zendesk Inc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Healthcare CRM Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Technological innovations and software development are crucial to the healthcare industry revolution. These technological developments support medical and administrative services that dramatically enhance and ease healthcare processes, communications, and workflow. Patient-centric healthcare boosts patient satisfaction levels, which benefits healthcare providers and practices. Thus, the rising adoption of a patient-centric approach by healthcare providers is driving the growth of the healthcare CRM market.

However, the protection of sensitive health data stored in CRM portals is a major concern among healthcare providers and care receivers. As the end users operating the CRM may sell personal data to third parties, patients are worried about the privacy of their private data, which may include their biological data. Additionally, if these devices are connected to the medical billing records of the patients, the risk might further entail a financial data breach. According to the HIPAA Journal, 5,150 healthcare data breaches of over 500 records have been reported between 2009 and 2022 to the HHS’ Office for Civil Rights. Those breaches have exposed or impermissibly disclosed 382,262,109 healthcare records. That equates to over 1.2x the population of the US. In 2022, an average of 1.94 data breaches of 500 or more healthcare records were reported daily. Despite technology companies investing increasingly high amounts to enhance the security of their offerings, consumers are likely to take some time to rely completely on software for their healthcare-related activities. Thus, issues related to data security and privacy are limiting the adoption of CRM software, thereby hindering market growth.

Trends:

The increasing trend of accepting digital health and mobile customer relationship management (CRM) solutions in the healthcare sector is reshaping the landscape of healthcare CRM, thereby driving the demand for innovative platforms that streamline patient engagement, virtual healthcare delivery, and mobile care coordination. Increasing acceptance of digital health further helps the healthcare industry leverage digital channels, mobile technology, and enhanced patient experiences to optimize care delivery and patient satisfaction.

The acceptance of digital health within healthcare infrastructure influences integrating care coordination tools, secure messaging platforms, and remote care coordination capabilities to support multi-channel care interactions, facilitate clinician-patient communication, and enhance patient engagement across diverse touchpoints. Additionally, rapid advancements in mobile technologies and applications, new opportunities for integrating mobile health into existing eHealth services, and ongoing expansion of mobile cellular network coverage are among the major factors supporting the proliferation of mobile healthcare solutions such as mobile CRM. As per the International Telecommunication Union (ITU) estimates, there are over 5 billion wireless subscribers, with over 70% living in low- and middle-income countries in 2020. According to the GSM Association, commercial wireless transmissions have reached ~85% of the world's population, i.e., far beyond the reach of the electric grid. The proliferation of wireless communication would help enhance the quality of care and patient health and save huge unnecessary healthcare costs every year by simply assisting in addressing issues such as remote patient monitoring and medical scheduling. The applications of mHealth are likely to expand in the coming years. According to Salesforce, ~52% of hospitals use three or more connected health technologies, including 58% with mobile-optimized patient portals. Thus, the increasing applications of mobile health solutions and increasing acceptance of digital health globally will increase the demand for healthcare CRM in various healthcare infrastructures.

Report Segmentation and Scope:

The global healthcare CRM market is segmented on the basis of deployment mode, product type, application, and end user. Based on deployment mode, the market is bifurcated into cloud based and on-premise. Based on product type, the market is divided into operational CRM, analytical CRM, and collaborative CRM. The healthcare CRM market, by application, is divided relationship management, case management, case coordination, community outreach, and others. In terms of end user, the healthcare CRM market is segmented into providers, payers, and others. Geographically, the healthcare CRM market is segmented into North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and the Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and the Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

Segmental Analysis:

Based on deployment mode, the healthcare CRM market is segmented into cloud-based and on-premise. The cloud-based segment held a larger share of the market in 2022 and is expected to register a higher CAGR in the market from 2022 to 2030. Cloud-based healthcare CRM solutions are hosted on the vendor's servers and accessed through a web browser. Cloud-based CRM solutions offer unparalleled accessibility, allowing healthcare professionals to access patient data and CRM tools from any location with internet connectivity. This flexibility is particularly valuable for healthcare providers working remotely or across multiple locations.

The healthcare CRM market, by product type, is segmented into analytical CRM, collaborative CRM, and operational CRM. The operational CRM segment held the largest share of the market in 2022 and is anticipated to register the highest CAGR in the market during 2022–2030. Operational CRM focuses on streamlining and automating operational processes such as appointment scheduling, patient registration, billing, and claim processing within healthcare organizations. These solutions help healthcare providers improve efficiency, reduce administrative burden, and enhance the overall patient experience.

By application, the healthcare CRM market is segmented into case management, relationship management, community outreach, case coordination, and others. The relationship management segment held the largest share of the market in 2022 and is expected to register the highest CAGR in the market from 2022 to 2030. Relationship management in the healthcare CRM market focuses on building and maintaining strong relationships with patients, caregivers, and other stakeholders.

In terms of end user, the healthcare CRM market is segmented into providers, payers, and others. The providers segment held the largest share of the market in 2022 and is expected to register the highest CAGR in the market from 2022 to 2030. Providers, including hospitals, clinics, and individual healthcare professionals, require CRM solutions to help them manage patient cases, coordinate care, and build strong relationships with patients.

Regional Analysis:

Geographically, the healthcare CRM market is segmented into North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa. In 2022, North America held the largest share of the global healthcare CRM market. Asia Pacific is estimated to register the highest CAGR during 2022–2030.

The majority of hospitals and clinics in the US are experiencing financial and operational stress. Healthcare CRM software is primarily associated with hospitals, clinics, and ambulatory surgical centers to schedule and manage appointments, especially in emergency departments, and inefficient scheduling in outpatient, in-patient, and surgical departments. Efficient patient scheduling management remains an urgent issue for most hospitals and clinics. Due to improper medical scheduling, patients experience delays in receiving quality care in public and private healthcare systems. The 2022 survey of Physician Appointment Wait Times and Medicare and Medicaid Acceptance Rates states that there is a waiting period of an average of 26 days to schedule a first-time appointment with a physician, an 8% increase since 2017 when the average wait time was ~24 days. This leads to prolonged wait times, scheduling difficulties, and an imbalance of supply and demand in the public and private healthcare sectors. Healthcare CRM software enables hospitals and clinics to track the arrival and departure of patients and gain real-time updates on co-pays and cancellations. The use of software reduces the no-shows by 30% with appointment reminder calls. It enhances the entire treatment procedure and improves communication with the patient.

Furthermore, the US reports a high prevalence of chronic and acute diseases. According to the “Heart Disease and Stroke Statistics - 2023 Update” by the American Heart Association, coronary heart disease (CHD) was a leading cause (41.2%) of deaths associated with CVDs in the US in 2020, followed by stroke (17.3%), other CVDs (16.8%), high blood pressure (12.9%), heart failure (9.2%), and diseases of the arteries (2.6%). As per the US Centers for Disease Control and Prevention (CDC), ~1 in 20 adults in the US aged 20 and above suffer from coronary artery disease. Thus, a high prevalence of CVDs and other chronic diseases propels the demand for medical scheduling and adoption of healthcare CRM in the US. Also, the rapid adoption of healthcare IT in the US is anticipated to drive the healthcare CRM market growth in the future.

Healthcare CRM Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 5.75 Billion |

| Market Size by 2030 | US$ 12.95 Billion |

| Global CAGR (2022 - 2030) | 10.7% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Deployment Mode

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Healthcare CRM Market Players Density: Understanding Its Impact on Business Dynamics

The Healthcare CRM Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industry Developments and Future Opportunities:

Various initiatives by key players operating in the global healthcare CRM market are listed below:

- In August 2023, IBM and Salesforce announced a collaboration to help businesses worldwide across industries accelerate their adoption of AI for CRM. Together, the two companies support clients to revolutionize customer, partner, and employee experiences while helping safeguard their data.

- In April 2022, Cured announced the launch of the next evolution of its digital marketing and customer relationship management (CRM) platform built for healthcare, further enabling the company to deliver on its mission to bring care full circle. These platform advancements empower healthcare organizations to build unparalleled relationships with new customers and existing patients.

- In November 2021, Pegasystems Inc collaborated with Google Cloud, which improved experiences in healthcare with better data insights and personalization. This partnership between Pega and Google Cloud brought together the capabilities of Google Cloud’s Healthcare Data Engine and Pega’s suite of intelligent healthcare solutions.

Competitive Landscape and Key Companies:

Pegasystems Inc, Sage Group Plc, IQVIA Holdings Inc, VerioMed Corp, Pipedrive Inc, WebMD Ignite Inc, Zendesk Inc, SugarCRM Inc, SAP SE, Veeva Systems Inc, Oracle Corp, ScienceSoft USA Corp, Microsoft Corp, Salesforce Inc, and International Business Machines Corp are among the prominent players operating in the healthcare CRM market. These companies focus on new technologies, advancements in existing products, and geographic expansions to meet the growing consumer demand worldwide and increase their product range in specialty portfolios.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends