Newborn Screening Market Size, Trends & Demand by 2034

Coverage: By Product Type (Reagents and Assay Kits, and Instruments), Technology [Tandem Mass Spectrometry (TMS), Molecular Assays, Immunoassays and Enzymatic Assays, Pulse Oximetry Screening Technology, and Others], Test Type [Dry Blood Spot Test, Hearing Screen Test, Critical Congenital Heart Diseases (CCHD) Test, and Others], End User (Hospitals and Clinics, and Diagnostic Laboratories), and Geography

- Status : Data Released

- Report Code : TIPHE100001294

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : June 26, 2026

2025 Market Size

US$ 1.01 Bn

Base year value

2034 Forecast

US$ 2.16 Bn

Projected by 2034

CAGR 2026-2034

8.79 %

Growth rate

Addressable Market

US$ 14.18 Bn

(2026-2034)

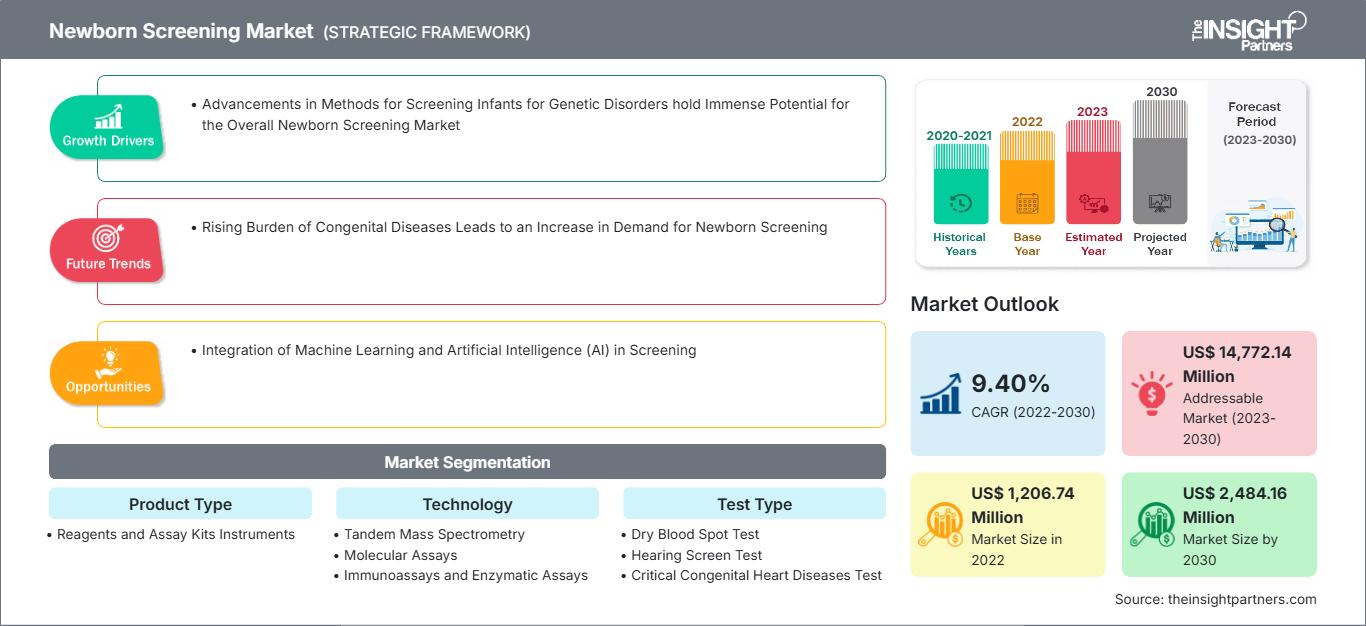

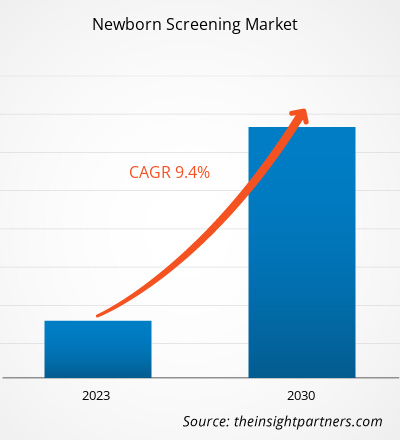

The global newborn screening market size is projected to reach US$ 2.16 billion by 2034 from US$ 1.01 billion in 2025. The market is anticipated to register a CAGR of 8.79% during the forecast period 2026–2034.

Key market dynamics include a heightening global focus on early disease detection and preventive pediatric healthcare, rising incidence of congenital anomalies and inherited metabolic disorders, and a significant shift toward mandatory screening programs globally. Additionally, the market is expected to benefit from the growing integration of advanced diagnostic technologies like next-generation sequencing, expansion of screening panels in emerging economies, and the increasing development of non-invasive screening techniques.

Newborn Screening Market Analysis

The newborn screening market analysis shows a shift toward high-throughput and multi-disorder testing as healthcare systems prioritize early intervention to reduce long-term disability and mortality. The market is dominated by instrumentation, specifically advanced analytical systems like tandem mass spectrometry. Strategic opportunities are emerging in molecular diagnostics and genomic sequencing, where the ability to identify rare genetic conditions with high precision offers a clear competitive advantage. The analysis also notes that market expansion depends on laboratory automation efficiency and robust follow-up testing procedures to ensure diagnostic accuracy. Competitive differentiation now stands out depending on the development of comprehensive, standardized assay kits and data interpretation software. This approach helps leading diagnostic firms secure recurring revenue through long-term contracts with public health laboratories.

Newborn Screening Market Overview

Newborn screening has evolved from niche metabolic tests to a foundational public health initiative. The market includes blood-based metabolic screening, universal hearing tests, and critical congenital heart disease pulse oximetry. Both global diagnostic giants and specialized biotechnology startups compete in this market, using technologies such as tandem mass spectrometry, enzyme-based assays, and DNA sequencing. Growing demand for rapid postnatal clinical care among health-conscious parents and government mandates in North America and Europe has increased the popularity of comprehensive screening panels. North America leads in revenue due to its established mandatory programs and high adoption of advanced diagnostic tools, while Asia-Pacific is advancing in infrastructure development and high birth-rate-driven adoption. The US market is the most developed, driven by policies covering dozens of serious conditions and the broad availability of specialized pediatric care. Competition among brands is fueling the inclusion of a wider range of biomarkers for rare endocrine and infectious diseases.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Newborn Screening Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Newborn Screening Market Drivers and Opportunities

Market Drivers:

- Rising Incidence of Congenital and Metabolic Disorders: The increasing prevalence of genetic conditions like phenylketonuria, cystic fibrosis, and sickle cell disease makes early diagnosis highly imperative for survival.

- Favorable Government Initiatives and Mandates: Many countries are making newborn screening compulsory before hospital discharge, with government bodies expanding budgets to cover an increasing number of conditions.

- Technological Advancements in Diagnostics: The adoption of tandem mass spectrometry and molecular screening allows for the simultaneous detection of multiple disorders from a single dried blood spot.

Market Opportunities:

- Integration of Next-Generation Sequencing: There is a significant opportunity to incorporate genome sequencing into routine screening to identify thousands of rare diseases that traditional biochemical tests might miss.

- Expansion in Emerging APAC and MEA Corridors: High birth rates in countries like India and China, coupled with rising healthcare spending, offer massive untapped potential for diagnostic service providers.

- Growth in Point-of-Care Testing: Developing portable, easy-to-use devices for hearing and cardiac screening in non-hospital settings can facilitate broader screening coverage in rural regions.

Newborn Screening Market Report Segmentation Analysis

The newborn screening market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Reagents and Assay Kits: A stable revenue-generating segment driven by the recurring demand for testing consumables required for daily operations in high-volume laboratories.

- Instruments: Includes high-end analytical hardware such as mass spectrometers and hearing screening devices, representing a significant initial capital investment.

By Technology:

- Tandem Mass Spectrometry (TMS): The gold standard for metabolic screening, allowing for the detection of numerous disorders from a single sample.

- Molecular Assays: Rapidly growing technology used for DNA-based testing, including the detection of spinal muscular atrophy and cystic fibrosis.

- Immunoassays and Enzymatic Assays: Traditional methods widely used for identifying endocrine disorders and enzyme deficiencies.

- Pulse Oximetry Screening Technology: Essential for the non-invasive detection of critical congenital heart defects by measuring oxygen saturation.

- Others: Includes various specialized diagnostic technologies used for niche screening requirements.

By Test Type:

- Dry Blood Spot Test: The primary method for metabolic and genetic screening, involving the collection of blood on specialized filter paper.

- Hearing Screen Test: Conducted shortly after birth to identify permanent hearing loss using automated brainstem response or otoacoustic emissions.

- Critical Congenital Heart Diseases (CCHD) Test: Utilizes pulse oximetry to screen for heart defects that require surgery or intervention in the first year of life.

- Others: Encompasses additional screening procedures such as visual screening or specific infectious disease tests.

By End User:

- Hospitals and Clinics: The primary point of care where screening is initiated immediately following birth.

- Diagnostic Laboratories: Centralized facilities that process large volumes of screening samples on behalf of regional or national health programs.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Newborn Screening Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1.01 Billion |

| Market Size by 2034 | US$ 2.16 Billion |

| Global CAGR (2026 - 2034) | 8.79% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Newborn Screening Market Players Density: Understanding Its Impact on Business Dynamics

The Newborn Screening Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Newborn Screening Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for diagnostic manufacturers and clinical laboratories to expand.

The newborn screening market is undergoing a significant transformation, moving from basic metabolic testing to comprehensive genomic and point-of-care screening. Growth is driven by the rising prevalence of congenital disorders, a surge in personalized pediatric medicine, and the expansion of mandatory national screening panels. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the largest share globally, driven by universal adoption of the Recommended Uniform Screening Panel and high healthcare expenditure.

- Key Drivers:

- Stringent federal and state mandates for screening at least 31 serious conditions.

- Mainstreaming of next-generation sequencing for second-tier testing in high-end diagnostic centers.

- Strong presence of major industry leaders and favorable reimbursement policies for pediatric genetic testing.

- Trends: Integration of machine learning for data interpretation and a rapid shift toward screening for rare conditions like spinal muscular atrophy.

Europe

- Market Share: Holds a significant share globally, anchored by established public health infrastructure in the UK, Germany, France, and Italy.

- Key Drivers:

- Robust government funding for nationalized screening programs and strict regulatory frameworks for in-vitro diagnostics.

- Established processing infrastructure for tandem mass spectrometry and molecular diagnostics.

- High emphasis on early intervention to reduce long-term social healthcare costs.

- Trends: A strategic push toward harmonizing screening panels across EU nations and an increasing focus on expanding pilot programs for lysosomal storage disorders.

Asia-Pacific

- Market Share: The fastest-growing region, with China and India acting as primary due to massive annual birth rates.

- Key Drivers:

- Massive consumer base seeking premium diagnostic services and rising disposable incomes among the urban middle class.

- Government-supported healthcare initiatives focused on reducing infant mortality.

- Rapid urbanization leading to the establishment of centralized state-of-the-art diagnostic laboratories.

- Trends: Heavy reliance on public-private partnerships to scale screening coverage and the adoption of low-cost, high-throughput technologies for rural demographics.

South and Central America

- Market Share: Emerging market with a growing public sector screening initiative in countries like Brazil and Chile.

- Key Drivers:

- Increasing awareness of the socio-economic benefits of early diagnosis for metabolic and thyroid disorders.

- Modernization of public health labs into commercial-grade facilities to support national screening goals.

- Rising interest in preventing childhood disabilities through early metabolic intervention.

- Trends: Growth of decentralized point-of-care testing for hearing and cardiac defects and the introduction of newborn screening for infectious diseases.

Middle East and Africa

- Market Share: Developing market with deep historical roots in regional health challenges, transitioning toward formalized commercial production.

- Key Drivers:

- Traditional presence of high consanguinity rates driving demand for genetic and metabolic screening.

- High demand for shelf-stable reagents and portable screening devices in varied climates.

- Strategic investments in smart healthcare infrastructure to improve regional health security.

- Trends: Implementation of modern data management technologies to formalize screening registries and a focus on high-sensitivity tests for hemoglobinopathies.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as PerkinElmer (Revvity), Waters Corporation, and Thermo Fisher Scientific. Regional diagnostic experts and niche players like Natus Medical, Trivitron Healthcare, and Masimo Corporation, alongside innovators such as Bio-Rad Laboratories and Agilent Technologies, also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Advanced Laboratory Automation: Integrating robotics and data software to handle massive testing volumes with minimal human error.

- Comprehensive Service Portfolios: Offering everything from screening instruments and reagents to follow-up diagnostic confirmation tests.

- Strategic Partnerships: Collaborating with government health departments to manage nationwide screening programs through turnkey solutions.

Opportunities and Strategic Moves

- Partner with Government Health Ministries: Tap into the surging demand for universal screening programs by securing long-term public sector contracts in high-growth markets like Asia-Pacific and Latin America.

- Incorporate Genomic and AI Solutions: Integrate next-generation sequencing and artificial intelligence to appeal to modern clinical laboratories seeking to identify a wider range of rare genetic disorders with extreme precision

Major Companies operating in the Newborn Screening Market are:

- LifeCell International Pvt Ltd

- Zentech SA

- Trivitron Healthcare Pvt Ltd

- PerkinElmer Inc

- Waters Corp

- Bio-Rad Laboratories Inc.

- Masimo Corp

- Natus Medical Inc.

- Baebies Inc

- MRC Holland BV

- Medtronic Plc

Disclaimer: The companies listed above are not ranked in any particular order.

Newborn Screening Market News and Recent Developments

- In November 2025, Enfanos announced agreement with Waters to advance mass spectrometry solutions for newborn screening research and applications. This agreement enables Enfanos to seamlessly connect innovative enzyme activity and biomarker assay products, such as the Enfanos 10-Plex RUO kit and GAG EndoNRE™ biomarkers, with Waters mass spectrometry products, service, and technical support.

- In March 2025, LaCAR MDx Technologies, a company specialized in automated solutions for newborn screening, announced the strategic acquisition of the Newborn Screening division of Baebies, Inc., a U.S. company known for its innovative neonatal diagnostic technologies. This acquisition is part of LaCAR’s strategy to expand its range of solutions and accelerate its expansion into the U.S. market.

Newborn Screening Market Report Coverage and Deliverables

The Newborn Screening Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Newborn Screening Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Newborn Screening Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Newborn Screening Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Newborn Screening Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends