Marktanalyse und Prognose zur DNA-Sequenzierung der nächsten Generation nach Größe, Anteil, Wachstum, Trends 2025

Historische Daten : 2015-2016 | Basisjahr : 2017 | Prognosezeitraum : 2018-2025Markt für DNA-Sequenzierung der nächsten Generation bis 2025 – Globale Analyse und Prognosen nach Produkt (Plattformen, Dienstleistungen und Verbrauchsmaterialien); Anwendung (Diagnostik, Arzneimittelforschung, Präzisionsmedizin und andere Anwendungen); und Endbenutzer (akademische und Forschungsinstitute, Pharma- und Biotechnologieunternehmen, Krankenhäuser, Kliniken und andere Endbenutzer) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPRE00002934

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 246

- Verfügbare Berichtsformate :

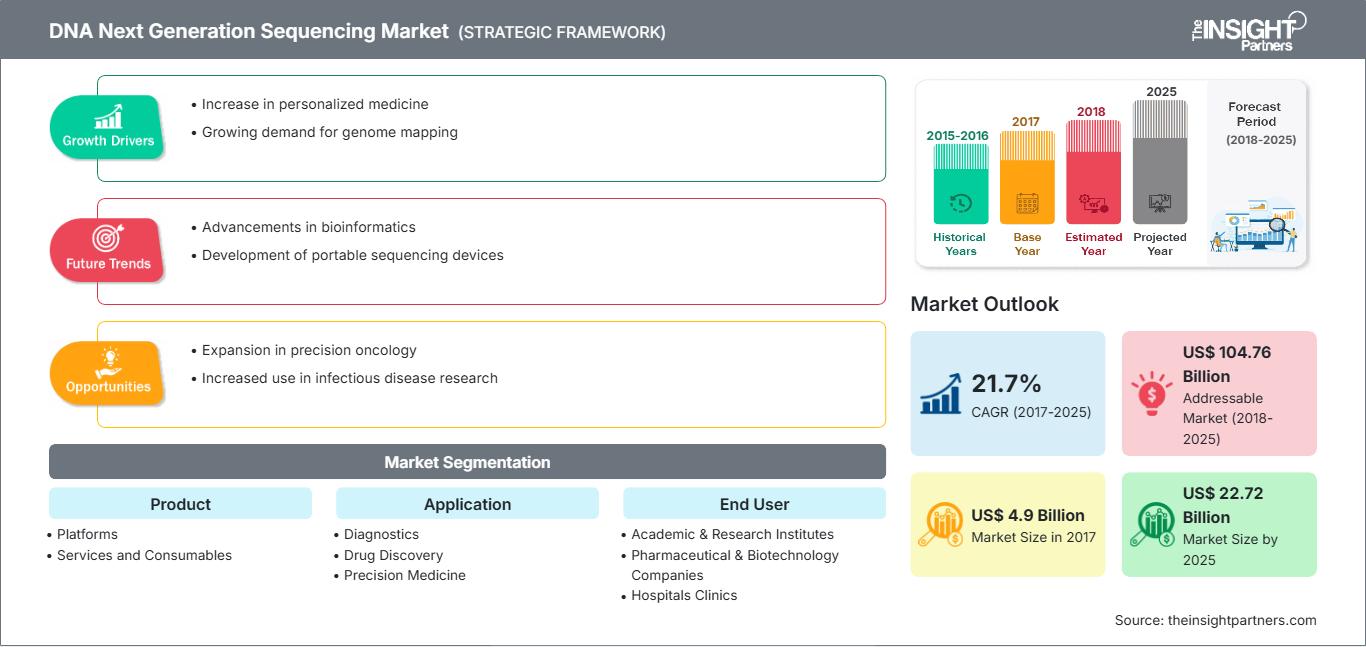

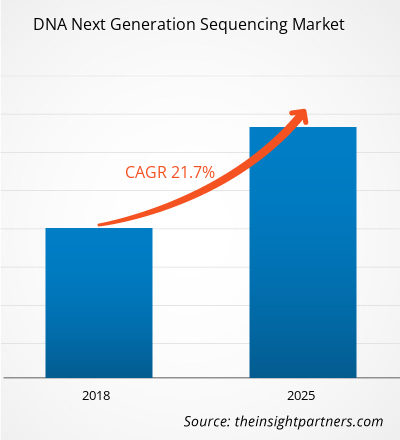

[Forschungsbericht]Der Markt für DNA-Sequenzierung der nächsten Generation wird voraussichtlich von 4.898,5 Millionen US-Dollar im Jahr 2017 auf 22.716,9 Millionen US-Dollar im Jahr 2025 anwachsen; für den Zeitraum 2018–2025 wird ein durchschnittliches jährliches Wachstum von 21,7 % erwartet.

Sequenzierung der nächsten Generation wird auch als Hochdurchsatzsequenzierung bezeichnet. NGS ermöglicht die schnelle Sequenzierung der Basenpaare in DNA-Proben. NGS treibt die Anwendung in der Arzneimittelforschung voran und ermöglicht die Zukunft der personalisierten Medizin, genetischer Erkrankungen und der klinischen Diagnostik. Darüber hinaus ist Next-Generation-Sequenzierung (NGS) eine massiv parallele Sequenzierungstechnologie, die die Reihenfolge der Nukleotide in einem gesamten Genom skalierbar, mit ultrahohem Durchsatz und hoher Geschwindigkeit bestimmen kann. Da sie die Vorbereitung der Probe für die nachfolgende Sequenzierungsreaktion umfasst, ist die DNA-Vorsequenzierung einer der wichtigsten Prozesse im gesamten Sequenzierungsprotokoll. Im globalen Gesundheitssektor wird NGS zunehmend in klinische Laboranalysen, Tests und Krankheitsdiagnosen integriert. In der Pharmakogenomik wird NGS häufig eingesetzt, um den Prozess der Arzneimittelforschung zu beschleunigen.

Das Marktwachstum für DNA-Next-Generation-Sequenzierung ist auf die weltweit steigende Zahl von Krebsfällen, die Zunahme von Forschungsstudien, die zunehmende Zusammenarbeit zwischen Forschungsinstituten und Marktteilnehmern sowie die zunehmende Anwendung von DNA-Next-Generation-Sequenzierung und den technologischen Fortschritt in der Sequenzierungstechnologie zurückzuführen. Es wird jedoch erwartet, dass der Mangel an qualifizierten Fachkräften das Gesamtmarktwachstum für DNA-Next-Generation-Sequenzierung entscheidend beeinflussen wird.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für DNA-Sequenzierung der nächsten Generation: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markteinblicke

Sinkende Preise für Sequenzierung und technologische Fortschritte bei Sequenzierungsmethoden treiben den Markt für DNA-Sequenzierung der nächsten Generation an

In den letzten Jahren sind die Preise für DNA-Sequenzierung der nächsten Generation erheblich gesunken. Im Jahr 2000 betrugen die Kosten für die Sequenzierung des menschlichen Genoms 3,7 Milliarden US-Dollar und dauerten 13 Jahre. In den letzten Jahren sanken die Kosten jedoch auf 10 Millionen US-Dollar im Jahr 2006 und sanken 2012 weiter, und der Prozess dauerte weniger Tage. Große Akteure auf dem Markt für DNA-Sequenzierung der nächsten Generation wie Illumina und Roche haben bahnbrechende Technologien eingeführt, die kosteneffizient sind und weniger Zeit für Sequenzierungsprozesse benötigen.

Darüber hinaus haben Fortschritte auf dem Gebiet der Molekularbiologie die Sequenzierungsverfahren gleichermaßen verbessert. Viele Branchenakteure haben in den letzten Jahren innovative NGS-Technologien entwickelt. Zum Beispiel Pacific Biosciences mit Sequel und Oxford Nanopore mit PromethION. Darüber hinaus dominieren drei fortschrittliche NSG-Systeme den Markt: Roche GS FLX (454), Illumina HiSeq 2000 (Solexa) und AB SOLiD (Agencourt).

Die weitere Modifikation und Automatisierung dieses Prozesses führte zu einer weiteren Zunahme der Sequenzierungsdaten und einem effizienteren Zeitmanagement, sodass Forscher wichtige Meilensteine im Humangenomprojekt erreichen konnten. NGS macht die sequenzbasierte Genexpressionanalyse zu einer „digitalen“ Alternative zu analogen Techniken. Fortschritte in der Genomsequenzierung haben die Sequenzierung einfach und genau gemacht. Diese technologischen Fortschritte werden den Markt für DNA-Sequenzierung der nächsten Generation in naher Zukunft voraussichtlich stark vergrößern.

Produktbasierte Erkenntnisse

Der globale Markt für DNA-Sequenzierung der nächsten Generation ist produktbezogen in Plattformen, Dienstleistungen und Verbrauchsmaterialien unterteilt. Das Plattformsegment ist weiter unterteilt in HiSeq Series, MiSeq Series, SOLiD, Ion Torrent, Pacbio Rs II und Sequel Systems und andere. Das Servicesegment ist weiter unterteilt in Sequenzierungsdienste und Datenverwaltungs- und -analysedienste. Das Verbrauchsgütersegment ist zudem weiter unterteilt in Probenvorbereitung und andere NGS-Verbrauchsgüter. Das Verbrauchsgütersegment hatte 2017 einen größeren Anteil an den Produktuntersegmenten im Markt für DNA-Sequenzierung der nächsten Generation und dürfte im Prognosezeitraum einen ähnlichen Trend aufweisen. Neuere NGS-Plattformen haben eine neue Sequenzierungsmethode namens Einzelmolekülsequenzierung (SMS) übernommen, die keine vorherige Amplifikation von DNA erfordert und somit PCR-bedingte Fehler beim Lesen oder eine Amplifikationsverzerrung in Richtung Wiederholungsregionen vermeidet. In den letzten fünf Jahren hat die Sequenzierung der nächsten Generation (NGS) den Übergang von der Forschung zur klinischen Anwendung vollzogen. Mindestens 14 Länder haben Initiativen zur Sequenzierung großer Bevölkerungsgruppen ins Leben gerufen und Prognosen zufolge wird bis 2025 das Genom von über 60 Millionen Menschen weltweit sequenziert sein.

Anwendungsbasierte Erkenntnisse

Der globale Markt für DNA-Sequenzierung der nächsten Generation ist nach Anwendung segmentiert in Diagnostik, Arzneimittelforschung, Präzisionsmedizin und andere Anwendungen. Das Diagnostiksegment hatte 2017 den größten Anteil und dürfte in den nächsten fünf bis sechs Jahren deutlich wachsen. Der Einsatz von Next-Generation-Sequencing-Technologie (NGS) in der diagnostischen Genomversorgung erfordert Präzision und Genauigkeit. Die NGS-Technologien nutzen kosteneffiziente Sequenzierung, um aus der Gesamtgenomsequenzierung genomische Informationen über die Patienten zu gewinnen und klinische Maßnahmen durchzuführen. Next-Generation-Sequencing wird zunehmend konventionelle Technologien zur Diagnose verschiedener genetischer Störungen ersetzen. Große Genmengen können nun in einem einzigen Test analysiert werden, anstatt Gen für Gen zu analysieren.

Endnutzerbasierte Erkenntnisse

Der globale Markt ist nach Endnutzern segmentiert in akademische und Forschungsinstitute, Pharma- und Biotechnologieunternehmen, Krankenhäuser und Kliniken sowie andere Endnutzer. Das Segment der akademischen und Forschungsinstitute wird im Prognosezeitraum voraussichtlich das höchste Wachstum verzeichnen. Die Sequenzierung hilft Wissenschaftlern, die Art der genetischen Informationen zu identifizieren, die in einem bestimmten DNA-Abschnitt enthalten sind. So können Wissenschaftler beispielsweise anhand von Sequenzinformationen bestimmen, welche DNA-Abschnitte Gene enthalten und welche Abschnitte regulatorische Anweisungen zum An- oder Abschalten von Genen enthalten. Der automatisierte, industrialisierte Ansatz basierend auf Zufalls- oder Shotgun-Sequenzierung wurde vom Institute for Genomic Research (TIGR) in Rockville, Maryland, eingeführt und führte zur Veröffentlichung von 337 neuen menschlichen Genen und 48 homologen Genen aus anderen Organismen.

DNA Next Generation Sequencing

Regionale Einblicke in den Markt für DNA-Sequenzierung der nächsten GenerationDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für DNA-Sequenzierung der nächsten Generation im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zur DNA-Sequenzierung der nächsten Generation

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2017 | US$ 4.9 Billion |

| Marktgröße nach 2025 | US$ 22.72 Billion |

| Globale CAGR (2017 - 2025) | 21.7% |

| Historische Daten | 2015-2016 |

| Prognosezeitraum | 2018-2025 |

| Abgedeckte Segmente |

By Produkt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer im Bereich DNA-Sequenzierung der nächsten Generation: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für DNA-Sequenzierung der nächsten Generation wächst rasant. Die steigende Nachfrage der Endverbraucher ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für DNA-Sequenzierung der nächsten Generation Übersicht der wichtigsten Akteure

Produkteinführungen und -zulassungen sind gängige Strategien von Unternehmen, um ihre globale Präsenz und ihr Produktportfolio zu erweitern. Darüber hinaus setzen Marktteilnehmer auf Partnerschaftsstrategien, um ihren Kundenstamm zu erweitern und so ihren Markennamen weltweit zu etablieren. Es wird erwartet, dass der Marktanteil durch die Entwicklung neuer innovativer Produkte durch Marktteilnehmer floriert. Zu den Marktteilnehmern auf dem betreffenden Markt gehören unter anderem THERMO FISHER SCIENTIFIC INC., Illumina, Inc., Qiagen NV, Beijing Genomics Institute, PerkinElmer, Inc., F.Hoffman-La Roche Ltd., Agilent Technologies, Eurofins Scientific, Oxford Nanopore Technologies Ltd. und Macrogen Inc.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Markt für DNA-Sequenzierung der nächsten Generation

Kostenlose Probe anfordern für - Markt für DNA-Sequenzierung der nächsten Generation