Disposable Endoscope Market Share, Demand & Growth by 2034

Coverage: By Application (Urologic Endoscopy, GI Endoscopy, Bronchoscopy, Arthroscopy, Proctoscopy, and Others), End User (Hospitals, Diagnostic Centers, and Clinics), and Geography

- Status : Data Released

- Report Code : TIPRE00004924

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

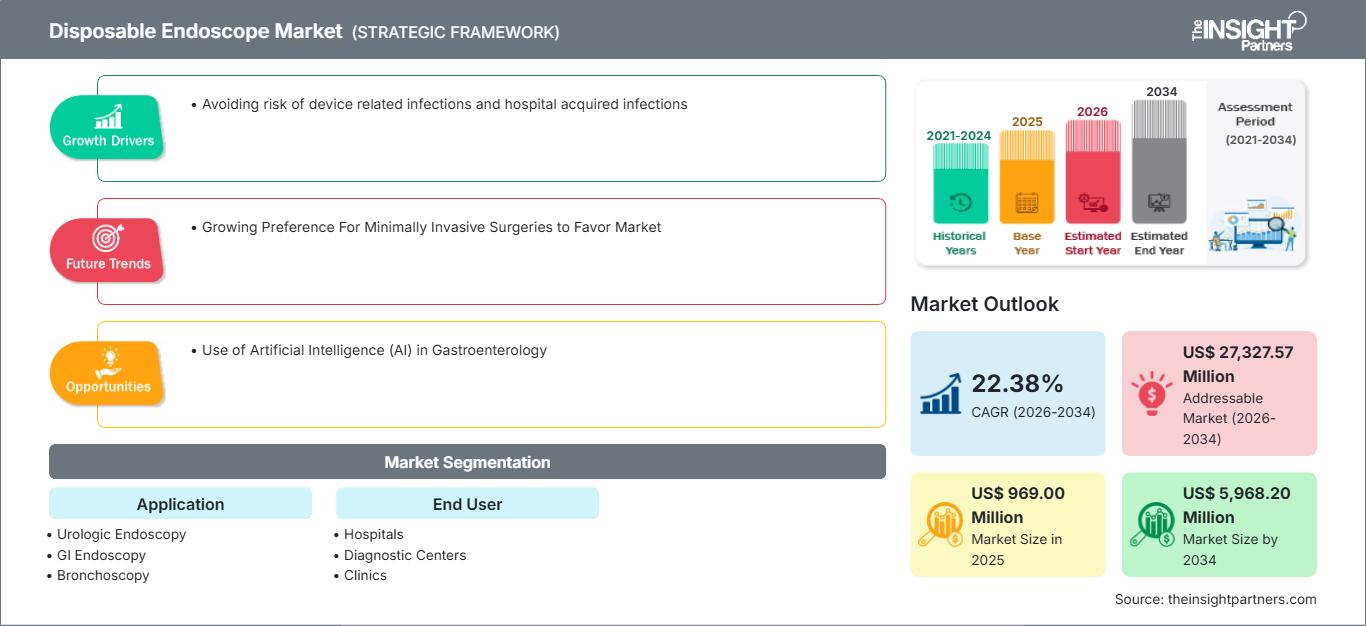

2025 Market Size

US$ 969.00 Mn

Base year value

2034 Forecast

US$ 5,968.20 Mn

Projected by 2034

CAGR 2026-2034

22.38 %

Growth rate

Addressable Market

US$ 27,327.57 Mn

(2026-2034)

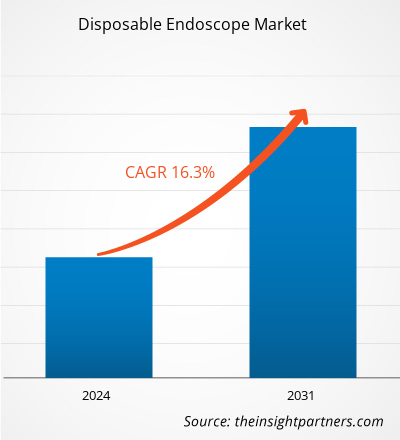

The Disposable Endoscope Market is advancing from a niche infection-control solution into a mainstream device category across endoscopy suites, operating rooms, ICUs, and outpatient care settings. The market is valued at US$ 969.00 million in 2025 and is projected to reach US$ 5,968.20 million by 2034, expanding at a CAGR of 22.38% from 2026 to 2034. Growth reflects rising procedure volumes, reprocessing constraints, and stronger hospital focus on sterile, ready-to-use visualization tools.

North America remains a critical adoption hub for the Disposable Endoscope Market, with an estimated regional CAGR of about 20%–22% through 2034. Growth is supported by stringent infection-prevention expectations, high use of minimally invasive procedures, and hospital investments in workflow efficiency. Wider use of single-use bronchoscopes, cystoscopes, and emerging GI platforms is strengthening demand across acute-care and ambulatory settings.

Disposable Endoscope Market Assessment and Insights

- North America: North America accounted for 38–42% of the disposable endoscope market share in 2025 and is anticipated to expand at a CAGR of 21.5%–22.5% during 2026–2034. Strong infection control regulations, high procedural volumes, and rapid adoption of advanced single-use visualization technologies continue to support regional market leadership.

- U.S.: The U.S. represented 84–88% of the North American disposable endoscope market size in 2025 and is projected to register a CAGR of 21.8%–22.8% during 2026–2034, supported by increasing adoption of disposable endoscopy systems, advanced healthcare infrastructure, and growing demand for infection prevention solutions.

- Europe: Europe held 25–29% of the disposable endoscope market share in 2025 and is expected to grow at a CAGR of 20.5%–21.5% during 2026–2034. Germany, the United Kingdom, and France remain the leading regional markets due to advanced healthcare systems and expanding adoption of minimally invasive surgical procedures.

- Asia Pacific: Asia Pacific accounted for a 22–26% share in 2025 and is forecast to expand at a CAGR of 24.0%–25.0% during 2026–2034. China, Japan, and India continue to drive regional growth through healthcare modernization, expanding hospital infrastructure, and increasing procedural volumes.

- Largest Segment: Application – Bronchoscopy represented the largest disposable endoscope market segment and is expected to record a CAGR of 22.5%–23.5% during 2026–2034, reflecting its extensive use in pulmonary diagnostics and increasing emphasis on infection prevention through single-use devices.

- High Growth Segment: Application – Urologic Endoscopy is projected to grow at a CAGR of 24.5%–25.5% during 2026–2034, driven by the rising prevalence of urological disorders and increasing preference for minimally invasive outpatient procedures.

- Key companies analyzed in detail: Boston Scientific Corporation; Ambu A/S; KARL STORZ SE & Co. KG; ProSurg, Inc.; Baxter International Inc.; Zsquare Ltd.; FUJIFILM Holdings Corporation; HOYA Corporation; ScoutCam Ltd.; and Verathon Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Disposable Endoscope Market report has evolved from usage for infection risks to clinical utilization where factors like turnaround time, availability of devices, and contamination become key parameters that affect purchase decisions. Its adoption is the highest in fields where reuse, endoscope cleaning, and processing are expensive, resource-limited, or complicated. Urology and Bronchoscopy are some of the applications that have benefited, while GI Endoscopy becomes relevant as imaging becomes better.

Going forward, the adoption of disposable endoscopes in hospitals is expected not just based on their capabilities in preventing infections but also on their productivity capabilities. Purchase decisions would increasingly take into account overall procedure cost, staff availability, maintenance of scopes, and flexibility. Some of the companies that include Boston Scientific Corporation, Ambu A/S, KARL STORZ SE & Co. KG, FUJIFILM Holdings Corporation, HOYA Corporation, and Verathon Inc. have strengths in specialty applications and imaging capabilities.

Disposable Endoscope Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 969.00 Million |

| Market Size by 2034 | US$ 5,968.20 Million |

| Global CAGR (2026 - 2034) | 22.38% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Disposable Endoscope Market Analysis

Disposable endoscope Market conditions are driven by the burden of risk of infection caused by the use of endoscopes, increased interest in the quality of the process of reprocessing, and a need to increase the number of endoscopy cases conducted outside the confines of standard procedure rooms. Single-use technology decreases the reliance on sterilization cycles, repair needs, and scope inventories.

The ecosystem consists of suppliers of optical components, suppliers of image processors, manufacturers of medical devices, hospitals, diagnostic centers, clinics, and waste management companies. The value proposition is built on the balance between the quality of imaging and the economic benefits per procedure. With the increasing penetration of single-use devices into GI endoscopy and arthroscopy, the suppliers will need to consider the issues of ergonomics, torque characteristics, lighting, accessory compatibility, and disposal.

The competitive environment consists of big medical technology players as well as innovative single-use specialists. Boston Scientific Corporation is strong in therapeutic single-use endoscopy, Ambu A/S in the fields of bronchoscopy, ENT, GI and urology platforms, while KARL STORZ SE & Co. KG and FUJIFILM Holdings Corporation have strong visualization know-how. Zsquare Ltd., ScoutCam Ltd., ProSurg, Inc., Baxter International Inc., HOYA Corporation, and Verathon Inc. complement the list with application-based innovations.

Trends include investments in high-resolution imaging, small displays, procedure-oriented design, and platform standardization. The key strategic move for vendors is demonstrating that single-use endoscopes provide reliable clinical performance along with reduced indirect costs through lower repair frequency and downtime. Vendors combining a wide product line, education support, and purchasing options may find themselves in a winning position as single-use initiatives become more standardized in hospitals.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Disposable Endoscope Market: Strategic Insights

Regional Insights

North America Disposable Endoscope Market

North America is expected to maintain leadership in the Disposable Endoscope Market, expanding at an estimated CAGR of 20%–22%. Adoption is supported by high procedure intensity, strong hospital infection-control governance, and rapid uptake of devices that reduce reprocessing dependence. The region benefits from established reimbursement infrastructure and early acceptance of single-use tools in bronchoscopy and urology.

Hospitals and diagnostic centers are increasingly assessing disposable scopes through operational metrics such as room turnover, staff utilization, and equipment availability. Boston Scientific Corporation, Ambu A/S, Verathon Inc., and other suppliers are strengthening regional competition by emphasizing sterile access, imaging performance, and integrated visualization platforms suited for acute-care, outpatient, and emergency environments.

U.S. Disposable Endoscope Market

The U.S. Disposable Endoscope Market is projected to grow at roughly 20%–22% and accounts for an estimated 75%–80% of North American revenue. Large hospital networks, ambulatory surgery centers, and specialty clinics are adopting single-use scopes to address infection risk, procedure backlog, and rising costs associated with reusable scope maintenance.

Company presence is strongest in urologic endoscopy, bronchoscopy, and therapeutic visualization. Boston Scientific Corporation has visibility in single-use endoscopy platforms, while Ambu A/S has broadened its urology and GI portfolio. Demand is increasingly tied to kidney stone management, ICU airway procedures, cystoscopy, and selective GI applications where sterile access and rapid setup create measurable workflow value.

Europe Disposable Endoscope Market

Europe holds an estimated 25%–30% share of the Disposable Endoscope Market and is likely to expand at a CAGR of around 19%–21%. The region combines advanced endoscopy infrastructure with strict infection-prevention protocols, creating a favorable environment for selective single-use adoption. Germany is the leading country, supported by procedural volume, clinical specialization, and strong hospital purchasing discipline.

The UK Disposable Endoscope Market is shaped by waiting-list pressure, outpatient procedure expansion, and demand for portable endoscopy capacity. Single-use bronchoscopes and cystoscopes are gaining relevance where rapid access and infection control are operational priorities. Adoption is measured, as public healthcare procurement weighs total lifecycle cost against clinical convenience and reprocessing constraints.

Germany leads European adoption due to its high procedural standards, advanced hospital infrastructure, and strong medtech ecosystem. Disposable endoscopes are evaluated for urology, pulmonology, and selected GI applications where reusable scope logistics can limit throughput. KARL STORZ SE & Co. KG contributes regional expertise in visualization systems and procedure-specific endoscopy design.

France, Italy, and Spain are expanding gradually as hospitals modernize infection-control pathways and increase minimally invasive procedure capacity. Procurement remains sensitive to budget pressure, but clinical departments are recognizing the value of single-use scopes for urgent procedures, immunocompromised patients, and settings where reprocessing infrastructure is stretched or geographically fragmented.

APAC Disposable Endoscope Market

APAC is the fastest-growing region in the Disposable Endoscope Market, with an estimated CAGR of 24%–27% and a global share range of roughly 20%–25%. China is the leading country, supported by hospital expansion, rising endoscopy volumes, and domestic investment in medical device manufacturing. Policy efforts to improve healthcare access strengthen long-term demand.

China and India offer scale-driven opportunities as public and private providers expand diagnostic and surgical capacity. Disposable scopes can reduce infrastructure gaps in secondary hospitals and mobile care settings. Japan and South Korea emphasize imaging quality and procedural reliability, creating demand for high-performance systems from FUJIFILM Holdings Corporation, HOYA Corporation, and other advanced visualization suppliers.

Australia is adopting single-use endoscopy where infection-control assurance and dispersed care delivery matter. Across APAC, industrial drivers include component localization, low-cost manufacturing, and digital imaging innovation. Policy priorities around hospital modernization, cancer screening, and procedural access are expected to accelerate adoption, although reimbursement variability and medical waste concerns may influence purchasing pace.

Middle East & Africa Disposable Endoscope Market

The Middle East & Africa Disposable Endoscope Market is developing from a smaller base, with an estimated CAGR of 18%–20%. Saudi Arabia is the leading country, supported by healthcare infrastructure investment, hospital modernization, and specialist-care expansion. The UAE follows with private hospital growth, medical tourism, and demand for advanced procedural technologies.

Energy and infrastructure context indirectly supports Disposable Endoscope market development as Gulf countries invest in resilient hospitals, smart facilities, and high-acuity care networks. Disposable endoscopes fit environments where sterile access, rapid readiness, and reduced dependence on reprocessing departments can improve service reliability. Adoption is strongest in tertiary hospitals and premium clinics.

South Africa and the rest of MEA show gradual uptake, constrained by procurement budgets and uneven endoscopy infrastructure. However, single-use systems can support outreach care, infection-sensitive procedures, and facilities with limited sterilization capacity. Suppliers that provide training, service-light platforms, and cost-flexible purchasing models can improve adoption prospects across diverse healthcare systems.

Segmentation Analysis

Application

- Urologic Endoscopy: Urologic endoscopy leads adoption because cystoscopy, ureteroscopy, and stone procedures benefit from sterile access, reduced repair burden, and immediate scope availability in hospitals and clinics.

- GI Endoscopy: GI endoscopy is gaining attention as imaging quality improves and providers seek flexible solutions for gastroscopy, urgent procedures, and settings facing reprocessing bottlenecks.

- Bronchoscopy: Bronchoscopy remains a high-value use case because bedside airway inspection, ICU procedures, and infection-sensitive respiratory care require fast, sterile, and portable visualization tools.

- Arthroscopy: Arthroscopy adoption is emerging as single-use digital scopes support smaller procedure rooms, office-based evaluations, and orthopedic workflows that value simplified setup and predictable sterility.

- Proctoscopy: Proctoscopy demand is comparatively selective, supported by outpatient colorectal evaluation, infection-control needs, and clinics seeking low-maintenance visualization options for routine examinations.

End User

- Hospitals: Hospitals generate the greatest demand because complex procedures, emergency use, infection-control audits, and reusable scope repair costs make single-use platforms strategically relevant.

- Diagnostic Centers: Diagnostic centers adopt disposable endoscopes to improve scheduling flexibility, reduce sterilization infrastructure needs, and support consistent patient turnover across routine procedures.

- Clinics: Clinics use disposable endoscopes where compact systems, low maintenance, and rapid setup allow specialists to expand office-based evaluations without large capital investment.

Opportunity Snapshot

| Application | Revenue Contribution | Trend Tag | Adoption Stage |

| Urologic Endoscopy | High | Stone Care | Mature |

| GI Endoscopy | Medium | Access Expansion | Scaling |

| Bronchoscopy | High | ICU Readiness | Mature |

| Arthroscopy | Medium | Office Orthopedics | Emerging |

| Proctoscopy | Low | Clinic Screening | Emerging |

Disposable Endoscope Market Growth Drivers and Impact Analysis

Infection-Control Pressure Reshaping Endoscopy Procurement

Infection control is the most influential driver for the Disposable Endoscope Market because reusable endoscopes are difficult to clean consistently due to narrow channels, complex tips, and repeated exposure to biological material. Hospitals are under pressure to demonstrate stronger sterilization assurance, especially for vulnerable patients and high-acuity departments. Disposable endoscopes remove reprocessing variability by providing a sterile device for each procedure, reducing dependence on manual cleaning, drying, storage, and documentation steps.

The practical implication here is a change in cost-based decision-making that accounts for risk in addition to device cost. The focus for hospitals will be on cost savings through fewer infections, fewer postponed cases, and lower maintenance and reprocessing costs when evaluating disposable technology options. It will also promote greater use of disposable technology in ICU bronchoscopy, urologic procedures, and other procedures where reusables are scarce.

Procedure Growth Across Urology, Respiratory Care, and GI

Rising demand for minimally invasive diagnostics and therapy is expanding the addressable base for disposable endoscopes. Urologic endoscopy is benefiting from kidney stone management, cystoscopy, and ureteroscopy, while demand for bronchoscopy is supported by airway assessment, ICU care, and pulmonary diagnostics. GI endoscopy is seeing growing interest as single-use gastroscopes improve image quality and become more practical for urgent or decentralized care models.

The effect is evident in the diversification of procedural sites. Hospitals, laboratories, and clinics require solutions that enable fast setup without requiring an endoscopy suite environment. The disposable scopes enable doctors to cope with high demand, avoid cancellations due to a shortage of reusable scopes, and perform procedures at the bedside or in office settings.

Operational Efficiency Becoming a Board-Level Priority

Endoscopy departments struggle with capacity constraints due to rising patient volumes, labor shortages, and increasingly complex equipment maintenance. Reusable scope solutions require technicians, washers and dryers, tracking systems, leak tests, repairs, and spare scopes. The use of disposable endoscopes simplifies this process by reducing the number of stages between procedures and limiting the operational risks of damaging or delaying the processing of the reusable endoscope. It is especially beneficial for high-throughput hospitals and small facilities without large sterilization teams.

Disposable endoscopes affect the market by improving the correlation between endoscopy procurement and hospital efficiency. The procurement team assesses the impact of using disposable systems on scheduling, emergency response, and staffing. Even though environmental concerns and increased per-unit costs remain problems, the operational benefits can prove worthwhile when performing high-end procedures.

Disposable Endoscope Market Future Trends

Platform-Based Single-Use Endoscopy Ecosystems

A key development shaping disposable endoscope market trends is the shift toward platform ecosystems instead of standalone single-procedure devices. Hospitals prefer systems that can support multiple scopes through one processor, display, and user interface. This reduces training burden and makes purchasing more scalable across departments. Ambu A/S, Boston Scientific Corporation, and other competitors are advancing portfolios where urology, bronchoscopy, and GI tools can share visualization infrastructure.

Future demand will reward those platforms that offer quality imaging, user-friendly controls, accessory support, and documentable imaging. With the growth of the product portfolio, purchasing may shift from an ad hoc process, where devices are purchased departmentally, to a more standardized, enterprise-wide process. This is good news for vendors who can show value across all specialties and have reliable supply chains. Platforms will also enable analytics, procedure documentation, and software upgrades that extend differentiation beyond the disposable scope itself.

Sustainability-Driven Design and Waste Accountability

The environmental aspect will be one of the most pronounced trends amid the rise of disposable endoscopes. Healthcare facilities are trying to balance the advantages of infection prevention with their sustainability policies, particularly in Europe and within large U.S. health systems. Future developments in this field will place greater emphasis on low material intensity, recycling and repurposing of packaging, take-back services, and improved waste separation.

Future development will have to include an analysis of lifecycle and evidence-backed sustainability claims. Manufacturers can stand out from the crowd by reducing plastic intensity, improving logistics, and offering hospitals waste management options. Sustainability will not make hospitals abandon single-use technologies altogether, but it will affect the selection of specific devices. The greatest potential lies in companies that combine sterility, clinical superiority, and sustainability.

Disposable Endoscope Market Opportunities

Expansion into Ambulatory and Office-Based Procedures

Ambulatory surgery centers, diagnostic centers, and specialist clinics represent a major opportunity for the disposable endoscope market forecast. These settings often have limited reprocessing infrastructure but need reliable visualization for routine diagnostics, minor procedures, and follow-up care. Disposable scopes reduce capital requirements, avoid complex sterilization workflows, and support flexible scheduling. This makes them attractive for urology clinics, pulmonary practices, GI access points, and orthopedic evaluation settings.

The investment strategy needs to center on channel partnerships, procedure-specific bundle sales, and training programs for non-hospital purchasers. The companies have an opportunity to generate value by providing portable visualization units, clear pricing, and light-service models. The clinics would be more interested in simplicity than in the platform's complexity. Organizations that can design their products based on office economics can benefit from this approach.

Specialty-Specific Innovation in High-Risk Procedures

There is high potential for differentiated disposable endoscopes across these procedures. High-risk/high-complexity urologic stone management, ICU bronchoscopy, bladder cancer assessment, and emergency GI endoscopy all demand devices that are sterile and have high-quality imaging and procedural capabilities. Disposable products without special qualities may not perform in such scenarios, leaving room for more expensive products with better maneuverability, enhanced imaging, irrigation capability, and integrated display screens.

For action-oriented investments, focusing on clinical evidence, surgeon feedback, and product specialization by specialty is essential. A company might gain market share by addressing unique challenges, rather than competing solely on disposability. For instance, urology specialists will benefit from dual visualization and compatibility with stone procedures, while pulmonology teams may prioritize portable bedside access. This specialization supports premium positioning and reduces vulnerability to low-cost competition.

Recent Developments

- June, 2025: Ambu A/S received expanded U.S. FDA 510(k) clearance for the Ambu aScope 5 Cysto HD, authorizing use in percutaneous nephrolithotomy procedures and strengthening its single-use urology portfolio across cystoscopy, cysto-nephroscopy, and ureteroscopy.

- March, 2026: Boston Scientific Corporation received U.S. FDA 510(k) clearance for the Asurys Fluid Management System, designed for ureteroscopy, cystoscopy, PCNL, and BPH procedures. While not an endoscope launch, the system strengthens the procedural ecosystem supporting urologic endoscopy workflows.

- October, 2024: Ambu A/S received U.S. FDA 510(k) clearance for its HD cystoscopy solution, including the Ambu aScope 5 Cysto HD and full-HD endoscopy systems, supporting enhanced imaging for urologic procedures and expanding single-use cystoscopy commercialization in the United States.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends