Tendances et perspectives de croissance du marché de la thérapie génique (2025-2031)

Rapport d'analyse du marché de la thérapie génique : taille et prévisions (2021-2031), parts de marché mondiales et régionales, tendances et opportunités de croissance. Couverture : par vecteurs (vecteurs non viraux et viraux), indication (maladies neurologiques, cancer, dystrophie musculaire de Duchenne, maladies hépatologiques et autres indications), mode d'administration (in vivo et ex vivo).

- Statut : Publié

- Code du rapport : TIPHE100001165

- Catégorie : Sciences de la vie

- Nombre de pages : 300

- Formats de rapport disponibles :

- Date de dernière mise à jour : April 23, 2026

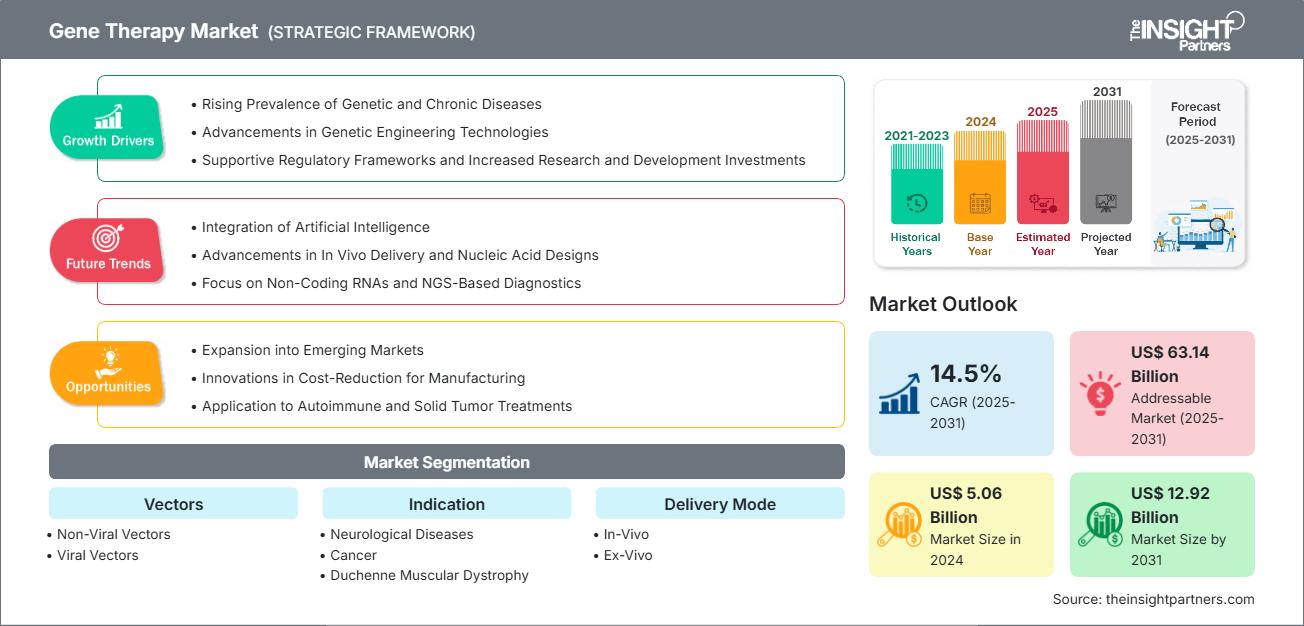

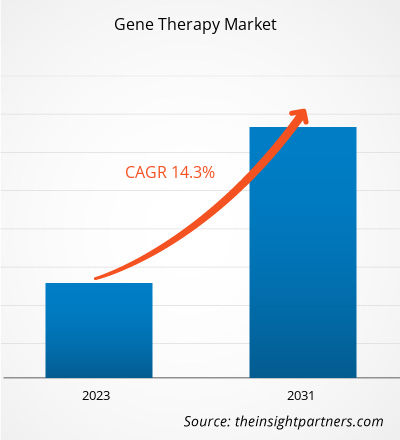

Le marché de la thérapie génique devrait atteindre 34 100 millions de dollars américains d’ici 2031. Ce marché devrait enregistrer un TCAC de 19,2 % entre 2025 et 2031.

Perspectives du marché et point de vue des analystes :

La thérapie génique est un procédé de traitement des maladies qui consiste à inactiver un gène responsable de la maladie, à le remplacer par une copie saine, ou à introduire un gène nouveau ou modifié dans l'organisme afin de traiter et de prévenir la maladie. On distingue la thérapie génique in vivo et ex vivo. Elle vise à remplacer ou corriger les gènes défectueux par des gènes normaux, permettant ainsi à l'organisme de produire les protéines ou enzymes nécessaires à son fonctionnement normal, ce qui peut potentiellement guérir la cause sous-jacente des maladies. La prévalence croissante des maladies génétiques et des cancers dans le monde, ainsi que le nombre croissant d'approbations de thérapies géniques par la FDA, favorisent la croissance du marché de la thérapie génique. Par ailleurs, les progrès technologiques en matière de thérapie génique devraient stimuler la croissance future de ce marché.

Facteurs de croissance :

Les progrès de la biotechnologie ont permis le développement de traitements pour un large éventail d'indications. Les thérapies géniques sont utilisées pour traiter diverses maladies, telles que le cancer, les troubles neurologiques et les maladies génétiques. À l'échelle mondiale, les thérapies géniques sont largement adoptées grâce à la disponibilité de produits approuvés par la FDA (Food and Drug Administration) aux États-Unis. Voici quelques exemples de produits de thérapie génique approuvés par la FDA ces dernières années :

- En décembre 2023, la FDA a approuvé deux thérapies géniques cellulaires pour la drépanocytose. Lyfgenia (lovotibeglogene autotemcel) de Bluebird Bio a été autorisé pour les patients drépanocytaires âgés de 12 ans et plus ayant des antécédents d'événements vaso-occlusifs. Son approbation a été concomitante à celle de Casgevy (exagamglogene autotemcel), développé par Vertex Pharmaceuticals et CRISPR Therapeutics.

- En juin 2023, la FDA a approuvé Roctavian, une thérapie génique utilisant un vecteur viral adéno-associé pour traiter les adultes atteints d'hémophilie A sévère ne présentant pas d'anticorps préexistants contre le sérotype 5 du virus adéno-associé. L'hémophilie A héréditaire est une maladie hémorragique grave due à une mutation génétique responsable de la production du facteur VIII (FVIII), une protéine essentielle à la coagulation sanguine. Roctavian est une thérapie génique administrée en une seule fois, contenant un vecteur viral porteur du gène codant pour le facteur VIII de coagulation.

- En juin 2023, la FDA a approuvé Elevidys, la première thérapie génique pour le traitement de la dystrophie musculaire de Duchenne chez les patients pédiatriques âgés de 4 à 5 ans présentant une mutation confirmée du gène de la dystrophie musculaire de Duchenne et ne souffrant d'aucune affection médicale préexistante empêchant le traitement par cette thérapie.

- En novembre 2022, la FDA a approuvé HEMGENIX, fabriqué par CSL Behring LLC, une thérapie génique recombinante à base de virus adéno-associé de type 5 pour traiter les patients adultes atteints de certains types d'hémophilie B.

Par conséquent, l'approbation croissante de ces thérapies géniques alimente la croissance du marché de la thérapie génique.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché de la thérapie génique : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Segmentation et portée du rapport :

L'analyse du marché de la thérapie génique a été réalisée en considérant les segments suivants : vecteurs, indications, modes d'administration et zones géographiques. Selon les vecteurs, le marché est segmenté en vecteurs non viraux et vecteurs viraux. En termes d'indications, il est classé en maladies neurologiques, cancers, dystrophie musculaire de Duchenne, maladies hépatologiques et autres indications. Quant aux modes d'administration, le marché est divisé en administration in vivo et ex vivo. Le rapport sur le marché de la thérapie génique couvre l'Amérique du Nord (États-Unis, Canada et Mexique), l'Europe (France, Allemagne, Royaume-Uni, Espagne, Italie et reste de l'Europe), l'Asie-Pacifique (Chine, Japon, Inde, Australie, Corée du Sud et reste de l'Asie-Pacifique), le Moyen-Orient et l'Afrique (Arabie saoudite, Afrique du Sud, Émirats arabes unis et reste du Moyen-Orient et de l'Afrique) et l'Amérique du Sud et centrale (Brésil, Argentine et reste de l'Amérique du Sud et centrale).

Analyse segmentaire :

Le marché de la thérapie génique, segmenté par vecteurs, se divise en vecteurs non viraux et vecteurs viraux. Le segment des vecteurs viraux détenait une part de marché importante en 2023 et devrait enregistrer un TCAC plus élevé entre 2023 et 2030.

Selon l'indication, le marché est segmenté en maladies neurologiques, cancer, dystrophie musculaire de Duchenne, maladies hépatiques et autres indications. Le segment du cancer détenait une part importante du marché de la thérapie génique en 2023 et devrait enregistrer le taux de croissance annuel composé (TCAC) le plus élevé entre 2023 et 2030.

Selon le mode d'administration, le marché est segmenté en thérapie génique in vivo et ex vivo. Le segment in vivo détenait une part de marché importante en 2023 et devrait enregistrer un TCAC plus élevé entre 2023 et 2030. La thérapie génique in vivo permet un traitement systémique, c'est-à-dire qu'elle peut atteindre de multiples sites et organes dans tout le corps. Ceci est particulièrement utile pour les maladies qui affectent plusieurs zones ou présentent des signes systémiques, permettant ainsi une approche thérapeutique globale. De plus, le développement de technologies d'administration avancées, telles que les vecteurs viraux, les nanoparticules et les vecteurs lipidiques, a amélioré l'efficacité et la spécificité de la thérapie in vivo. Ces progrès optimisent l'administration ciblée du matériel génétique et améliorent la sécurité et l'efficacité de la thérapie.

Analyse régionale :

Géographiquement, le marché de la thérapie génique est segmenté en Amérique du Nord, Europe, Asie-Pacifique, Amérique du Sud et centrale, et Moyen-Orient et Afrique. En 2023, l'Amérique du Nord détenait une part importante de ce marché. Les États-Unis dominaient alors le marché de la thérapie génique dans cette région. La croissance du marché en Amérique du Nord s'explique par la prévalence croissante des maladies génétiques, le nombre croissant de patients atteints de cancer, l'augmentation des financements publics, l'adoption croissante des thérapies géniques avancées pour le traitement des maladies et le nombre croissant d'autorisations de mise sur le marché.

Selon les Centres pour le contrôle et la prévention des maladies (CDC), environ 1 603 844 nouveaux cas de cancer ont été diagnostiqués en 2020 aux États-Unis, et 602 347 décès liés au cancer ont été recensés. On compte 403 nouveaux cas de cancer pour 100 000 habitants. Par ailleurs, selon le Centre international de recherche sur le cancer (CIRC), le nombre de nouveaux cas de cancer devrait atteindre 30,2 millions d’ici 2040. D’après les estimations du Bureau de la responsabilité gouvernementale des États-Unis (GAO), publiées en octobre 2021, entre 25 et 30 millions de personnes souffrent de maladies rares aux États-Unis ; près de la moitié des patients atteints de maladies rares sont des enfants. Les maladies rares sont souvent dues à une mutation génétique ; on estime que 80 % d’entre elles sont d’origine génétique.

D'après une mise à jour d'octobre 2021 des Instituts nationaux de la santé (NIH), dix entreprises pharmaceutiques et cinq organisations à but non lucratif ont collaboré pour accélérer le développement des thérapies géniques destinées aux 30 millions d'Américains atteints de maladies rares. La FDA américaine a approuvé sept médicaments de thérapie cellulaire et génique, et le portefeuille de nouveaux produits compte environ 1 200 thérapies expérimentales. La moitié d'entre elles sont en phase II d'essais cliniques. Selon les estimations de Chemical & Engineering News pour 2023, la croissance annuelle des ventes devrait atteindre 15 % pour les thérapies cellulaires et environ 30 % pour les thérapies géniques. Tous ces facteurs contribuent à la croissance du marché des thérapies géniques dans la région.

Aperçu régional du marché de la thérapie génique

Les tendances régionales et les facteurs influençant le marché de la thérapie génique tout au long de la période prévisionnelle ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments de marché et la répartition géographique de la thérapie génique en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et centrale.

Rapport sur le marché de la thérapie génique

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2024 | XX millions de dollars américains |

| Taille du marché d'ici 2031 | 34 100 millions de dollars américains |

| TCAC mondial (2025 - 2031) | 19,2% |

| Données historiques | 2021-2023 |

| Période de prévision | 2025-2031 |

| Segments couverts |

Par vecteurs

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché de la thérapie génique : comprendre son impact sur la dynamique commerciale

Le marché de la thérapie génique connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux, elle-même alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages de ces produits. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, contribuant ainsi à la croissance du marché.

- Découvrez un aperçu des principaux acteurs du marché de la thérapie génique

Évolutions du secteur et perspectives d'avenir :

Voici quelques initiatives prises par les acteurs du marché mondial de la thérapie génique :

- En janvier 2022, Ori Biotech Ltd a levé plus de 100 millions de dollars américains lors d'un tour de table de série B sursouscrit afin de lancer sur le marché une plateforme de fabrication innovante de thérapie cellulaire et génique.

- En janvier 2020, Astellas Pharma Inc. a acquis Audentes Therapeutics, Inc. Cette acquisition permet à l'entreprise fusionnée de devenir un leader mondial de la médecine génétique basée sur les AAV.

Paysage concurrentiel et entreprises clés :

Les prévisions du marché de la thérapie génique peuvent aider les acteurs du secteur à planifier leurs stratégies de croissance. Novartis AG, Astellas Pharma Inc., Bristol-Myers Squibb Company, Bluebird Bio Inc., CSL Behring, Sanofi, F. Hoffmann-La Roche Ltd, Daiichi Sankyo, Biogen et Oxford Biomedica figurent parmi les principaux acteurs présentés dans le rapport sur le marché de la thérapie génique. Ces entreprises s'attachent à lancer de nouveaux produits de haute technologie, à perfectionner leurs produits existants et à étendre leur présence géographique afin de répondre à la demande croissante des consommateurs à travers le monde.

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires