Markt für nutzungsbasierte Kfz-Versicherungen – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Marktgröße und Prognose für nutzungsbasierte Kfz-Versicherungen (2021–2031), Berichtsabdeckung für globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach eingebauter Technologie (Smartphones, Blackbox, Dongles und andere); und Versicherungsart (Pay-As-You-Drive (PAYD) und Pay-How-You-Drive (PHYD)); und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPAT100001345

- Kategorie : Banken, Finanzdienstleistungen und Versicherungen

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 16, 2024

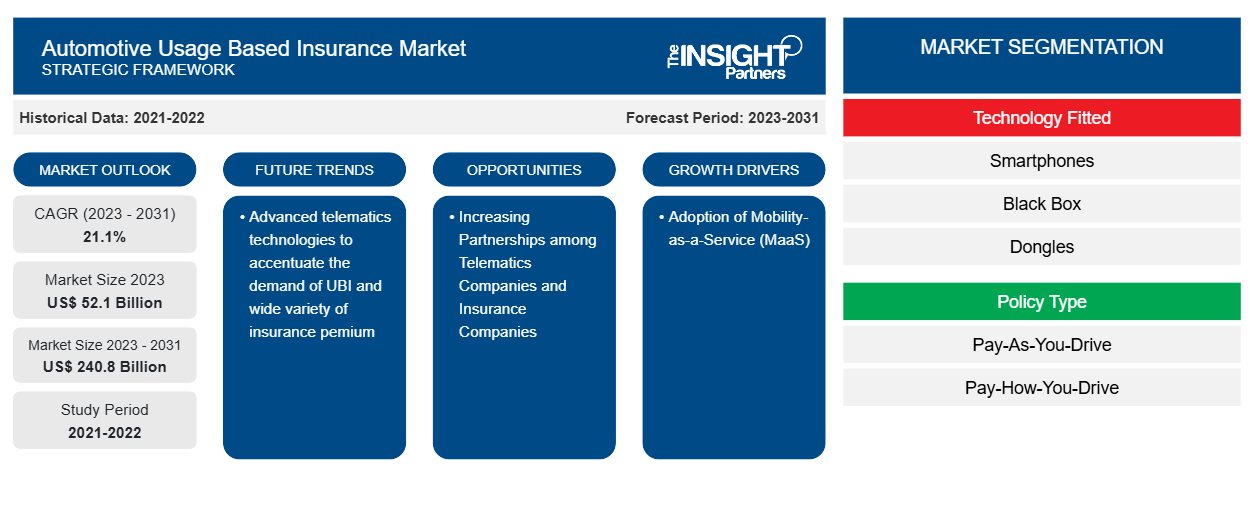

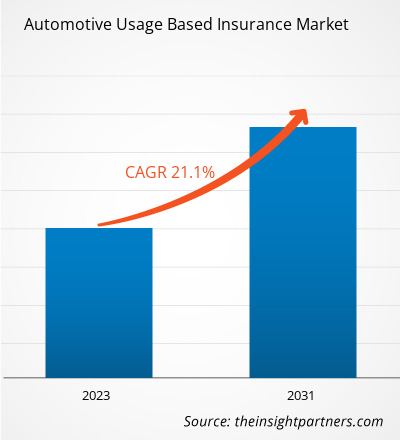

Der Markt für nutzungsbasierte Kfz-Versicherungen soll von 52,1 Milliarden US-Dollar im Jahr 2023 auf 240,8 Milliarden US-Dollar im Jahr 2031 anwachsen. Der Markt soll zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 21,1 % verzeichnen. Fortschrittliche Telematik-Technologien zur Steigerung der Nachfrage nach UBI und einer breiten Palette von Versicherungsprämien gehören zu den Schlüsselfaktoren, die den Markt für nutzungsbasierte Kfz-Versicherungen ankurbeln.CAGR of 21.1% in 2023–2031. Advanced telematics technologies to accentuate the demand for UBI and a wide variety of insurance premiums are among the key factors fueling the automotive usage based insurance market.

Analyse des nutzungsbasierten Kfz-Versicherungsmarktes

Mit der ständigen Weiterentwicklung der Telematikbranche und ihrer raschen Einführung in der Automobilbranche entwickeln sich neue Partnerschaften zwischen Versicherern, Automobilherstellern, Geräteherstellern und Anbietern von Telematiklösungen. Diese Partnerschaften zielen darauf ab, die Vorteile der aufkommenden datengesteuerten Technologie zu nutzen. Die junge Bevölkerung schließt am häufigsten eine nutzungsbasierte Kfz-Versicherung ab, da sie mit der Technologie vertrauter ist und von niedrigeren Prämien profitieren möchte. Auf den Märkten in Italien und den USA richtet sich UBI an eine breite Palette von Fahrern. Darüber hinaus war die Bekanntheit ein Wachstumshindernis, insbesondere auf dem britischen Markt, wo UBI hauptsächlich auf den Flottenmarkt sowie auf junge Fahrer ausgerichtet war. Mit den zunehmend lohnenden Programmen, die von den UBI-Akteuren eingeführt werden, erfährt der Markt jedoch eine enorme Dynamik. Mit dem zunehmenden Wachstum bei vernetzten Autos und der ADAS-Branche wird erwartet, dass alle Neuwagen in naher Zukunft mit vorinstallierten Telematikgeräten ausgestattet sein werden . Dieses Wachstum wird voraussichtlich dem Markt für nutzungsbasierte Kfz-Versicherungen Auftrieb verleihen.

Überblick über den Markt für nutzungsbasierte Kfz-Versicherungen

In der aktuellen Kfz-Versicherungsbranche befindet sich die UBI oder Telematikversicherung noch in einem frühen Stadium, da nur sehr wenige Länder die Technologie in großem Umfang übernommen haben. Kfz-Versicherungsunternehmen gehen zunehmend Partnerschaften mit Telematikunternehmen ein, um ihr Segment der Telematikversicherung oder UBI im aktuellen Marktszenario und auch für die Zukunft zu erweitern. Darüber hinaus ergreifen mehrere Unternehmen, die auf dem globalen Markt für nutzungsbasierte Kfz-Versicherungen tätig sind, ständig Initiativen, um Verbraucher mit verschiedenen attraktiven Policen und Technologien anzulocken. Der Markt ist stark fragmentiert, da die Branche von mehreren etablierten Unternehmen sowie aufstrebenden Akteuren auf der ganzen Welt beherrscht wird. Aus der Investitionsperspektive erzielen die Versicherungsunternehmen und Telematikunternehmen in Entwicklungsländern sowie in Industrieländern erhebliche Investitionen, was dem Markt in jüngster Zeit zu einem Aufschwung verhilft. Die Regierungen mehrerer Länder vereinfachen ihre Versicherungsgesetze, was ein weiterer Faktor ist, der den Markt antreibt.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Der Markt für nutzungsbasierte Kfz-Versicherungen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem Markt für nutzungsbasierte Versicherungen im Automobilbereich

Einführung von Mobility-as-a-Service (MaaS)MaaS)

In den letzten Jahren hat sich das Verbraucherverhalten gegenüber dem innerstädtischen und zwischenstädtischen Verkehr auf ein neues Niveau gewandelt. Ein erheblicher Prozentsatz der Reisenden auf der ganzen Welt ist nicht mehr bereit, mit dem eigenen Auto zu fahren, um dem Verkehr zu entgehen. Dies hat in Industrie- und Entwicklungsländern zu verschiedenen anderen Verkehrspraktiken geführt, wie etwa Carsharing und Mitfahrgelegenheiten. Diese Praktiken werden als Mobilität als Dienstleistung bezeichnet, da der Verbraucher das Fahrzeug und den Fahrer von einem Drittanbieter erhält. Mobility-as-a-Service zielt darauf ab, dem Verbraucher einen End-to-End-Transport unter Verwendung verschiedener Transportmittel bereitzustellen und so die vorhandene Verkehrsinfrastruktur in einem Gebiet in erheblichem Maße zu nutzen. Die zunehmende Akzeptanz von MaaS bei den Verbrauchern führt dazu, dass Drittanbieter eine größere Anzahl von Fahrzeugen anschaffen, um das Kundenerlebnis zu verbessern. Dieser Faktor führt auch dazu, dass die Zahl der Dienstleister auf der ganzen Welt zunimmt; einige der bekanntesten Mobility-as-a-Service-Anbieter sind unter anderem Uber, Lyft, Zipcar, Car2go, Beeline Singapore, UbiGo AB und Smile Mobility.intracity transit has transformed to a newer level. A significant percentage of travelers across the globe are no longer willing to drive their vehicles with the objective of avoiding traffic. This has given rise to various other transit practices, such as car sharing and ride-hailing, in developed countries and developing countries. These practices are known as mobility as a service, as the consumer avails the vehicle and the driver from a third-party service provider. MaaS among consumers is leading third-party service providers to procure an increased count of vehicles so as to enhance the customer experience. This factor is also increasing the number of service providers across the globe; some of the prominent mobility-as-a-service providers are Uber, Lyft, Zipcar, Car2go, Beeline Singapore, UbiGo AB, and Smile Mobility, among others.

Zunehmende Partnerschaften zwischen Telematikunternehmen und VersicherungsunternehmenTelematics Companies and Insurance Companies

Der Markt für nutzungsbasierte Kfz-Versicherungen reift in den USA, Italien und Großbritannien im Laufe der Jahre deutlich. Die Versicherungsunternehmen, die Telematikversicherungen anbieten, nutzen ständig verschiedene Faktoren, um die Lösungen zu verbessern und ihren Kunden bessere Angebote zu unterbreiten. Einer der wichtigsten Trends auf dem globalen Markt für nutzungsbasierte Kfz-Versicherungen ist die steigende Zahl von Partnerschaften zwischen Telematik- und Versicherungsunternehmen. Diese Partnerschaften erweitern die Ökosysteme für nutzungsbasierte Versicherungen in verschiedenen Volkswirtschaften, und derselbe Trend wird voraussichtlich in den kommenden Jahren die Marktgröße vergrößern. Einige der wichtigsten Partnerschaften zwischen Versicherungsunternehmen und Telematikunternehmen sind:

- Im November 2022 ging Ford eine Partnerschaft mit CerebrumX Lab Inc. ein, einer KI-gestützten Plattform für Datendienste und -verwaltung im Automobilbereich. Ziel dieser Partnerschaft war es, die vernetzten Fahrzeugdaten von Ford als Teil der nutzungsbasierten Versicherungsinitiative für Versicherer zu integrieren.

- Im November 2022 unterzeichnete die Wejo Group Limited eine Vereinbarung mit der Ford Motor Company. Ziel dieser Vereinbarung war die Ausweitung des End-to-End-Versicherungsangebots für Verbraucher in den gesamten USA.

- Im Februar 2022 ging Ford eine Partnerschaft mit dem Unternehmen State Farm ein. Ziel dieser Partnerschaft war die Entwicklung nutzungsbasierter Versicherungsprodukte für Ford- und Lincoln-Fahrzeugbesitzer mit geeigneten vernetzten Fahrzeugen.

Abgesehen von den oben genannten Partnerschaften gehen weltweit mehrere andere Versicherungsunternehmen, Telematikunternehmen und Automobilhersteller zunehmend Partnerschaften ein, um den Markt für UBI zu stärken. Diese Praxis der zunehmenden Partnerschaften im Ökosystem des automobilnutzungsbasierten Versicherungsmarktes wird voraussichtlich dazu beitragen, dass der Markt für automobilnutzungsbasierte Versicherungen in den nächsten Jahren stark ansteigt. Darüber hinaus interessieren sich Telematikunternehmen für die Automobilindustrie in Entwicklungsregionen auf der ganzen Welt, was ebenfalls den Umsatzstrom des globalen automobilnutzungsbasierten Versicherungsmarktes ankurbelt.

Segmentierungsanalyse des Marktberichts zur nutzungsbasierten Kfz-Versicherung

Wichtige Segmente, die zur Ableitung der auf der Autonutzung basierenden Versicherungsmarktanalyse beigetragen haben, sind die eingebaute Technologie und die Art der Police.

- Basierend auf der eingebauten Technologie wurde der Markt für nutzungsbasierte Kfz-Versicherungen in Smartphones, Blackboxen, Dongles und andere unterteilt. Das Dongle-Segment hatte im Jahr 2023 einen größeren Marktanteil.

- Basierend auf der Art der Police wurde der Markt für nutzungsbasierte Kfz-Versicherungen in Pay-as-you-drive (PAYD) und Pay-how-you-drive (PHYD) unterteilt. Das PHYD-Segment hatte im Jahr 2023 einen größeren Marktanteil.

Analyse der Marktanteile nutzungsbasierter Kfz-Versicherungen nach geografischer Lage

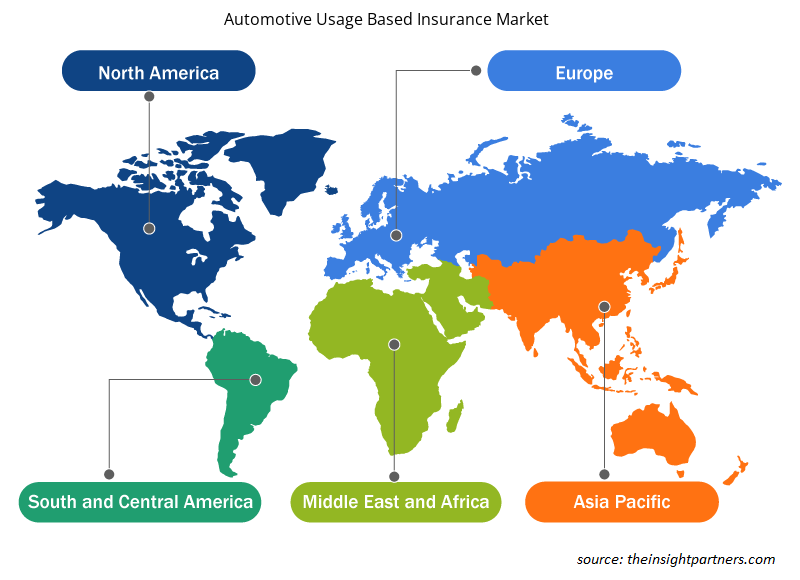

Der geografische Umfang des Berichts zum Markt für nutzungsbasierte Kfz-Versicherungen ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika sowie Südamerika.

Nordamerika dominierte 2023 den Markt für nutzungsbasierte Kfz-Versicherungen. Die Region Nordamerika umfasst die USA, Kanada und Mexiko. Die Dominanz Nordamerikas auf dem globalen Markt für nutzungsbasierte Kfz-Versicherungen ist darauf zurückzuführen, dass das Land eine große Anzahl von Automobilherstellern, Telematik- und Versicherungsunternehmen hat. Darüber hinaus ist der Trend zur Einführung neuerer Technologien und Lösungen im Land hoch, was die Einwohner dazu veranlasst hat, sich für eine Telematikversicherung zu entscheiden. Darüber hinaus ist die Region einer der Vorreiter von Mobility-as-a-Service auf der ganzen Welt, und der MaaS-Markt hat in der Region im Laufe der Jahre stark zugenommen und verzeichnet ständig Aufwärtstrends.

Aufgrund des höheren verfügbaren Einkommens der Bevölkerung ist die Anschaffung von Neuwagen im Land außerdem hoch. Im Zusammenhang mit der steigenden Zahl an Fahrzeugen verzeichnen auch mehrere damit verbundene Technologien und Lösungen in den USA einen rasanten Anstieg. Diese Faktoren haben das Wachstum des auf der Nutzung von Kraftfahrzeugen basierenden Versicherungsmarktes in den USA positiv beeinflusst.

Regionale Einblicke in den Markt für nutzungsbasierte Kfz-Versicherungen

Die regionalen Trends und Faktoren, die den Markt für nutzungsbasierte Kfz-Versicherungen im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für nutzungsbasierte Kfz-Versicherungen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum nutzungsbasierten Kfz-Versicherungsmarkt

Umfang des Marktberichts zur nutzungsbasierten Kfz-Versicherung

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 52,1 Milliarden US-Dollar |

| Marktgröße bis 2031 | 240,8 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 21,1 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Technologie ausgestattet

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für nutzungsbasierte Kfz-Versicherungen wächst rasant. Dies wird durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für nutzungsbasierte Kfz-Versicherungen sind:

- Allstate Versicherungsgesellschaft

- AXA SA

- Allianz SE

- Metromile, Inc.

- Ingenie Services Limited

- Liberty Mutual Versicherungsgesellschaft

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für nutzungsbasierte Kfz-Versicherungen

Neuigkeiten und aktuelle Entwicklungen zum Markt für nutzungsbasierte Kfz-Versicherungen

Der Markt für nutzungsbasierte Kfz-Versicherungen wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für nutzungsbasierte Kfz-Versicherungen und Strategien:

- Im Januar 2022 ging Otonomo eine Partnerschaft mit Audi ein. Ziel dieser Partnerschaft war es, Verbraucherangebote zu erproben, die von Pay-as-you-drive-Versicherungen über den allgemeinen Fahrzeugstatus bis hin zur ersten Schadensmeldung reichten.

- Im September 2021 unterzeichnete LexisNexis Risk Solutions eine Vereinbarung mit Ford Motor Co. Diese Vereinbarung zielte darauf ab, die Verfügbarkeit von Daten zu mit Ford verbundenen Fahrzeugen für US-Autoversicherer über den LexisNexis Telematics Exchange sicherzustellen.

Marktbericht zu nutzungsbasierten Versicherungen für Kraftfahrzeuge – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für nutzungsbasierte Kfz-Versicherungen (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte Porter's Five Forces Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile mit SWOT-Analyse

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends