Gas Pipeline Infrastructure Market Drivers and Forecasts by 2030

Coverage: By Operation (Transmission and Distribution), Equipment (Pipeline, Compressor Station, Metering Skids, and Others), and Application (Onshore and Offshore) and Geography

- Status : Published

- Report Code : TIPRE00029705

- Category : Energy and Power

- No. of Pages : 177

- Available Report Formats :

- Last update date : July 25, 2024

2022 Market Size

US$ 31,782.8 Mn

Base year value

2030 Forecast

US$ 40,703.5 Mn

Projected by 2030

CAGR 2022-2030

3.1 %

Growth rate

Addressable Market

US$ 292,420.72 Mn

(2022-2030)

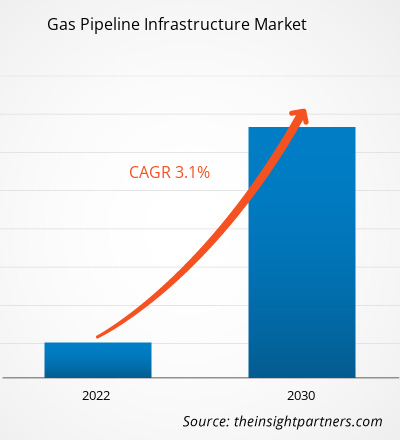

The Gas Pipeline Infrastructure Market size is projected to reach US$ 40,703.5 million by 2030 from US$ 31,782.8 million in 2022. The market is expected to register a CAGR of 3.1% in 2022–2030.

Gas Pipeline Infrastructure Market Analysis

The natural gas market is highly dynamic and requires liquidity, flexibility, and transparency to function effectively. Therefore, multiple sources of supply, multiple users, and a comprehensive infrastructure for transmission and distribution are required. The natural gas market is significantly developed in the US, Europe, and Asia Pacific, which is expected to drive the growth of the gas pipeline infrastructure with the rise in demand for gas in the future.

Gas Pipeline Infrastructure Market Overview

The gas pipeline infrastructure ecosystem includes the production phase, where natural gas is extracted from underground reservoirs. Exploration and production companies employ drilling technologies to extract raw natural gas. Once extracted, the gas is typically processed to remove impurities and then compressed for transportation. The production phase involves considerations of geological factors, extraction technologies, and environmental impact assessments. The primary players engaged in the production of natural gas are Royal Dutch Shell, ExxonMobil Corporation, Gazprom, ConocoPhillips, and TotalEnergie. The key players in the gas pipeline transmission network include Kinder Morgan Inc., Enbridge Inc., TC Energy Corporation, Pembina Pipeline Corporation, and Texas Gas Transmission LLC, among others.

Market Research Highlights

- North America dominated the market with 66.3% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 6.9% over the forecast period.

- US market is projected to grow at a CAGR of 3.4% over the forecast period.

- By Operation, the Distribution segment accounted for the largest market share of 81.8% in 2022.

- By Equipment, the Pipeline segment is anticipated to witness the fastest growth, registering a CAGR of 3.3% over the forecast period

- By Application, the Onshore segment accounted for the largest market share of 77.9% in 2022.

- The report profiles key industry players such as Saipem SpA, China Petroleum & Chemical Corp (Sinopec), TC Energy Corp, Berkshire Hathaway Inc, Enbridge Inc, Kinder Morgan Inc, Pembina Pipeline Corp, Enagas SA, Pipeline Infrastructure Ltd, Beltps, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Gas Pipeline Infrastructure Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Gas Pipeline Infrastructure Market Drivers and Opportunities

Increase in energy demand across the globe is Expected to be the Prime Driver for the Gas Pipeline Infrastructure Market

The rising population and growing urbanization are a few factors boosting the consumption of energy worldwide. Natural gas has the potential application in electricity generation, which boosts its demand. Furthermore, due to the increasing energy uncertainties in Europe owing to the Russia-Ukraine war, governments of several countries are also boosting the application of natural gas. Thus, the increase in energy demand fuels the growth of the gas pipeline infrastructure market.

Rise in Shale Gas Production in North America

North America has secured its position as one of the leading shale gas producers worldwide. Canada is the fifth-largest producer and fourth-largest exporter of natural gas worldwide. The main Canadian shale gas plays include the Horn River Basin and Montney shales in northeast British Columbia, the Utica Shale of Quebec, the Colorado Group of Alberta and Saskatchewan, and the Horton Bluff Shale of New Brunswick and Nova Scotia. Energy uncertainties owing to geopolitical disturbances are boosting the production of shale gas in North America, which is likely to create major opportunities for the gas pipeline infrastructure market growth in the coming years.

Gas Pipeline Infrastructure Market Report Segmentation Analysis

Key segments that contributed to the derivation of the gas pipeline infrastructure market analysis are operation, equipment, and application.

- Based on the operation, the gas pipeline infrastructure market has been divided into transmission and distribution. The distribution segment held a larger market share in 2022.

- In terms of equipment, the market has been segmented into pipeline, compressor station, metering skids, and others. The pipeline segment dominated the market in 2022.

- In terms of application, the market has been segmented into onshore and offshore. The onshore segment dominated the market in 2022.

Gas Pipeline Infrastructure Market Share Analysis by Geography

The geographic scope of the Gas Pipeline Infrastructure Market report is mainly divided into five regions: North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America is one of the leading gas exporters. The mounting demand for energy and the growing application of natural gas are boosting the market development of gas pipeline infrastructure in North America. In 2022, the US showcased the highest natural gas production capacity, followed by Canada and Mexico. Ixachi, Coulomb Phase 2, Quesqui, Nejo (IEPC), Leo, May, Koban, and Powerball are a few of the natural gas-producing fields in North America. The Ixachi plant is in Veracruz, Mexico, and it produced 618.09mmcfd (million cubic feet per day) in 2022. Also, the growing number of government initiatives and funding for the development of gas pipeline infrastructure is anticipated to boost the market for gas pipeline infrastructure over the forecast period.

Gas Pipeline Infrastructure Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 31,782.8 Million |

| Market Size by 2030 | US$ 40,703.5 Million |

| Global CAGR (2022 - 2030) | 3.1% |

| Historical Data | 2020-2021 |

| Forecast period | 2022-2030 |

| Segments Covered |

By Operation

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Gas Pipeline Infrastructure Market Players Density: Understanding Its Impact on Business Dynamics

The Gas Pipeline Infrastructure Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Gas Pipeline Infrastructure Market News and Recent Developments

The Gas Pipeline Infrastructure Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. The following is a list of developments in the market for Gas Pipeline Infrastructure Markets market and strategies:

- On February 2023, Enagas S.A. signed an agreement with Reganosa in which Enagas paid US$ 58.14 million to Reganosa to procure a network of 130 km of natural gas pipelines. The Iberian gas market's efficient operation and supply security are dependent on this network. (Source: Enagas S.A., Press Release/Company Website/Newsletter)

- On August 2022, A strategic agreement was agreed upon by TC Energy Corp and the CFE, the state-owned electric utility in Mexico, with the aim of expediting the development of natural gas infrastructure in the central and southeast parts of the country. In connection with the natural gas pipeline assets in central Mexico, TC Energy and the CFE have decided to combine earlier take-or-pay agreements (TSAs) underwritten by TC Energy's Mexico-based subsidiary TGNH and the CFE into a single, take-or-pay agreement priced in US dollars that would run through 2055. Related new infrastructure projects that are being planned in collaboration with the CFE will also be governed by this new TSA. (Source: TC Energy, Press Release/Company Website/Newsletter)

Gas Pipeline Infrastructure Market Report Coverage and Deliverables

The “Gas Pipeline Infrastructure Market Size and Forecast (2020–2030)” report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market dynamics such as drivers, restraints, and key opportunities

- Key future trends

- Detailed PEST analysis

- Global and regional market analysis covering key market trends, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles with SWOT analysis

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends