Marktanalyse und Prognose für digitale Therapeutika nach Größe, Anteil, Wachstum, Trends 2028

Marktgröße und Prognose für digitale Therapeutika bis 2028 – Auswirkungen von COVID-19 und globale Analyse nach Anwendung [(Diabetes, Herz-Kreislauf-Erkrankungen, Erkrankungen des zentralen Nervensystems (ZNS), Atemwegserkrankungen, Raucherentwöhnung, Erkrankungen des Bewegungsapparats und andere] und Vertriebskanal (Patienten, Anbieter, Kostenträger und Arbeitgeber)

- Status : Veröffentlicht

- Berichtscode : TIPHC00002236

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 181

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

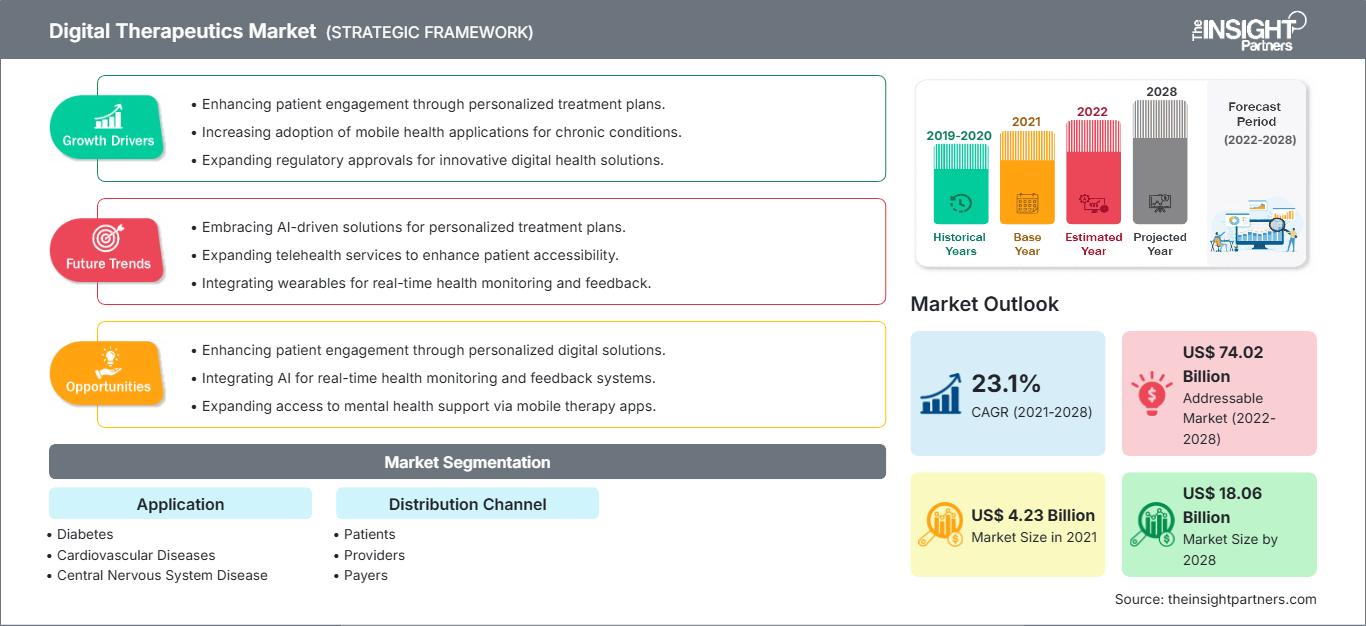

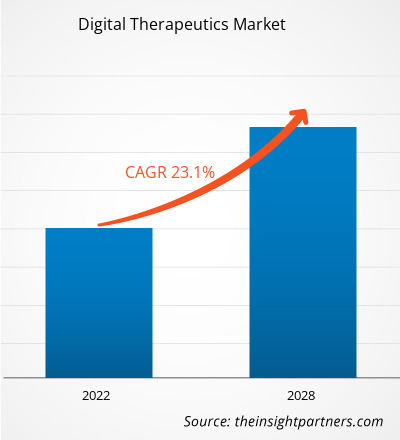

[Forschungsbericht]Der Markt für digitale Therapeutika wurde im Jahr 2021 auf 4.226,94 Millionen US-Dollar geschätzt und soll bis 2028 18.061,79 Millionen US-Dollar erreichen; von 2022 bis 2028 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 23,1 % erwartet.

Sichtweise des Analysten

Der Markt wird voraussichtlich durch die zunehmende Verbreitung von Smartphones in Industrie- und Schwellenländern, die Kosteneffizienz digitaler Gesundheitstechnologien für Anbieter und Patienten sowie die steigende Nachfrage nach integrierten Gesundheitssystemen und patientenzentrierter Behandlung angetrieben. Laut Kepios wird es im April 2021 weltweit 4,27 Milliarden Internetnutzer geben, was mehr als 60 % der Weltbevölkerung entspricht. Mit steigender Zahl wird auch das Bewusstsein für intelligentes Gesundheits-Tracking voraussichtlich zunehmen. Verbraucher in Industrieländern werden sich innovativer medizinischer Produkte zur Behandlung von Erkrankungen immer bewusster. Laut der Organisation für wirtschaftliche Zusammenarbeit und Entwicklung (OECD) stiegen die Gesundheitsausgaben im Verhältnis zum BIP im Jahr 2020 deutlich an, da sich die wirtschaftliche Lage in mehreren OECD-Ländern verschlechterte und die Gesundheitsausgaben stiegen. Infolgedessen verlagerte sich die Präferenz hin zu fortschrittlichen medizinischen Dienstleistungen, einschließlich der gestiegenen Nachfrage nach fortschrittlichen therapeutischen Geräten. Die Produktakzeptanz ist ein weiterer Aspekt, der das Marktwachstum vorantreibt.

Marktübersicht

Digitale Therapeutika bieten Patienten evidenzbasierte therapeutische Eingriffe, die sich auf die Behandlung von Krankheiten mit Programmen und das Management mithilfe hochwertiger Software konzentrieren. Digitale Therapeutika haben in den letzten Jahren Fortschritte gemacht und nutzen Technologie, um traditionelle klinische Therapien zu ergänzen oder möglicherweise zu ersetzen. Sie werden eigenständig oder in Verbindung mit Geräten, Medikamenten oder anderen Therapien eingesetzt, um die Patientenversorgung und die Gesundheitsergebnisse zu optimieren. Die wichtigsten Faktoren, die zum Wachstum des Marktes für digitale Therapeutika beitragen, sind die steigende Prävalenz chronischer Krankheiten, die Sorge um die Notwendigkeit, die Gesundheitskosten zu senken, sowie Partnerschaften und Kooperationen von Unternehmen. Das Wachstum des Marktes wird jedoch durch die Cyberbedrohung und die zunehmende Datensicherheit behindert, was die potenziellen Anwendungen im medizinischen Bereich einschränkt.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für digitale Therapeutika: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Markttreiber

Steigende Prävalenz chronischer Krankheiten treibt das Wachstum des Marktes für digitale Therapeutika voran

Chronische Krankheiten, darunter Herzkrankheiten, Schlaganfall, Diabetes und Fettleibigkeit, verursachen in jedem Land den Großteil der Gesundheitskosten. Laut einem Bericht der Weltgesundheitsorganisation (WHO) litten im Jahr 2020 weltweit 463 Millionen Erwachsene an Diabetes, und bis 2045 wird diese Zahl voraussichtlich auf 629 Millionen ansteigen. Im asiatisch-pazifischen Raum, in Europa sowie im Nahen Osten und Afrika ist die Prävalenz von Diabetes hoch. Die Krankheit ist hauptsächlich durch eine unzureichende Regulierung des Blutzuckerspiegels gekennzeichnet, da der Körper nicht in der Lage ist, das Hormon Insulin zu produzieren oder effektiv zu verwerten, und es gibt keine spezielle Heilung. Laut dem IDF Diabetes Atlas 2021, der von der International Diabetes Federation veröffentlicht wird, lebten in Nordamerika im Jahr 2021 rund 51 Millionen Menschen mit Diabetes, und bis 2045 soll diese Zahl auf 63 Millionen ansteigen. Außerdem leben in Südostasien rund 16,8 % der weltweiten Diabetiker. Bis 2035 werden voraussichtlich rund 130 Millionen Erwachsene in den USA an irgendeiner Form von Herz-Kreislauf-Erkrankungen leiden.

Die Fettleibigkeitsraten steigen in Industrie- und Entwicklungsländern weltweit aufgrund sitzender und ungesunder Lebensweisen rapide an. Laut Daten der Organisation für wirtschaftliche Zusammenarbeit (OECD) aus dem Jahr 2017 waren im OECD-Raum rund 19,5 % der erwachsenen Bevölkerung fettleibig. In Korea und Japan liegt diese Rate bei weniger als 6 %, in Ungarn, Neuseeland, Mexiko und den USA jedoch bei über 30 %. Darüber hinaus hat die Prävalenz in Australien, Kanada, Chile, Südafrika und Großbritannien im letzten Jahrzehnt rapide zugenommen: Mindestens 25 % der Erwachsenen sind fettleibig. In den USA, Mexiko und England wird bis 2030 ein Fettleibigkeitsgrad von ca. 47 %, ca. 39 % bzw. ca. 35 % erwartet.

Um das Management chronischer Krankheiten zu verbessern und Patienten mehr Behandlungsmöglichkeiten zu bieten, tragen digitale Therapeutika dazu bei, evidenzbasierte Therapielösungen bereitzustellen. Sie ermöglichen Patienten eine bessere Kontrolle ihrer Behandlung und bieten potenzielle Lösungen für das Management chronischer Krankheiten wie Diabetes. Daher treibt die steigende Prävalenz chronischer Krankheiten den Markt für digitale Therapeutika an.

Segmentanalyse

Anwendungsbasierte Erkenntnisse

Basierend auf der Anwendung ist der Markt für digitale Therapeutika in Atemwegserkrankungen, Erkrankungen des zentralen Nervensystems, Raucherentwöhnung, Erkrankungen des Bewegungsapparats, Herz-Kreislauf-Erkrankungen, Diabetes und andere Anwendungen segmentiert. Im Jahr 2021 hatte das Diabetessegment den größten Marktanteil bei digitalen Therapeutika, und es wird erwartet, dass dasselbe Segment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate (CAGR) auf dem Markt verzeichnen wird. Dies ist auf die weltweit steigende Zahl von Diabetesfällen, die hohe Prävalenz von Adipositas in Entwicklungsländern und die erheblichen Risiken und wirtschaftlichen Kosten zurückzuführen, die mit Adipositas-bedingten Krankheiten verbunden sind.

Diabetes ist eine lebensbedrohliche chronische Krankheit ohne spezielle Heilung. Sie wird hauptsächlich durch die Unfähigkeit des Körpers verursacht, das Hormon Insulin zu produzieren oder effektiv zu nutzen. Diese Unfähigkeit hindert den Körper daran, den Blutzuckerspiegel ausreichend zu regulieren. Es gibt zwei Arten von Diabetes, nämlich Diabetes Typ I, auch bekannt als Diabetes insipidus, und Diabetes Typ II, auch bekannt als Diabetes mellitus. Die Inzidenz und Prävalenz von Diabetes nehmen weltweit stetig zu. Typ-2-Diabetes ist die häufigste Form von Diabetes und hat parallel zu kulturellen und gesellschaftlichen Veränderungen zugenommen. In Ländern mit hohem Einkommen haben bis zu 91 % der Erwachsenen mit dieser Krankheit Typ-2-Diabetes. Laut dem Atlas 2021 der International Diabetes Federation (IDF) leben weltweit etwa 537 Millionen Menschen mit Diabetes, und bis 2030 wird diese Zahl voraussichtlich auf 643 Millionen ansteigen.

Vertriebskanalbasierte Erkenntnisse

In Bezug auf die Vertriebskanäle wird der Markt für digitale Therapeutika in Patienten, Anbieter, Kostenträger und Arbeitgeber unterteilt. Das Patientensegment hatte 2021 den größten Marktanteil bei digitalen Therapeutika. Es wird jedoch erwartet, dass das Anbietersegment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnet.

Digitale Therapeutika

Regionale Einblicke in den Markt für digitale TherapeutikaDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für digitale Therapeutika im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Verteilung digitaler Therapeutika in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

Umfang des Marktberichts über digitale Therapeutika

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2021 | US$ 4.23 Billion |

| Marktgröße nach 2028 | US$ 18.06 Billion |

| Globale CAGR (2021 - 2028) | 23.1% |

| Historische Daten | 2019-2020 |

| Prognosezeitraum | 2022-2028 |

| Abgedeckte Segmente |

By Anwendung

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktakteure für digitale Therapeutika: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für digitale Therapeutika wächst rasant. Die steigende Nachfrage der Endnutzer ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für digitale Therapeutika Übersicht der wichtigsten Akteure

Regionale Analyse

Nordamerika hatte 2021 den größten Marktanteil im Markt für digitale Therapeutika und wird seine Marktposition im Prognosezeitraum voraussichtlich halten. Zu den Faktoren, die das nordamerikanische Marktwachstum begünstigen, gehören der zunehmende Bedarf an Kostensenkungen im Gesundheitswesen, strenge Gesundheitsvorschriften, der wachsende Wettbewerb im Gesundheitswesen und schnelle technologische Innovationen. Darüber hinaus treiben die Präsenz großer Gesundheitsunternehmen und die zunehmende Nutzung digitaler Therapeutika das Marktwachstum in dieser Region voran. In Nordamerika verzeichnen die USA den größten Marktanteil im Bereich digitaler Therapeutika. Die digitale Gesundheitsversorgung boomt in den USA und eine Reihe von Faktoren wie die alternde Bevölkerung, die steigende Prävalenz chronischer Krankheiten, regulatorische Änderungen und die Verlagerung hin zu einer wertorientierten Versorgung unterstützen diese zunehmende Durchdringung der digitalen Gesundheit im Alltag.

Propeller Health, Canary Health Inc., NOOM INC., 2Morrow Inc, Teladoc Health, Welldoc Inc, FITBIT Inc, OMADA Health, Mango Health, Pear Therapeutics Inc und Happify Health gehören zu den führenden Akteuren im globalen Wachstum des Marktes für digitale Therapeutika. Mehrere andere wichtige Marktteilnehmer wurden analysiert, um eine ganzheitliche Sicht auf den Markt und sein Ökosystem zu erhalten. Der Bericht bietet detaillierte Markteinblicke, die den wichtigsten Akteuren helfen, Strategien für ihr Marktwachstum zu entwickeln. Einige Entwicklungen sind nachfolgend aufgeführt:

- Im November 2021 gab Pear Therapeutics, Inc. bekannt, dass es von der US-amerikanischen Food and Drug Administration (FDA) die Breakthrough Device Designation für seinen PDT-Produktkandidaten reSET-A zur Behandlung von Alkoholkonsumstörungen (AUD) erhalten hat. reSET-A erweitert potenziell Pears Sucht-Franchise, einschließlich der von der FDA zugelassenen Produkte zur Behandlung von Substanzgebrauchsstörungen (SUD) und Opioidgebrauchsstörungen (OUD).

- Im September 2020 gab Welldoc den Erhalt seiner neunten 510(k)-Zulassung von der Food and Drug Administration (FDA) für seine preisgekrönte Diabetes-Plattform BlueStar bekannt. Die neue Zulassung erweitert die Unterstützung bei der Insulindosierung auf die meisten Insulinarten, einschließlich der Titration von Bolus- und vorgemischtem Insulin bei Typ-2-Diabetes.

- Im Mai 2021 kündigte Teladoc Health, Inc. die Einführung von myStrength Complete an, einem integrierten Dienst für psychische Gesundheit, der Verbrauchern eine personalisierte, zielgerichtete Betreuung in einem einzigen, umfassenden Erlebnis bietet.

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends